KOYJF - Kemira: A Finnish Specialty Chemicals Company Trading At Just 5 Times EBITDA

2023-08-28 10:00:00 ET

Summary

- Kemira's performance in the first half of the year exceeded expectations, particularly in the industrial water division.

- The company reported a 40% increase in EBITDA compared to the first half of 2022.

- Kemira is planning to sell its oil and gas division.

Introduction

As explained in my article that was published last year , I mainly liked Kemira Oyj ( KOYJF ) for its relatively defensive characteristics, as this specialty chemicals company is very active in the water treatment industry. I wasn’t expecting much from 2022 as the company was originally guiding for a relatively flat performance and I thought that would already be a good achievement given the inflation-related cost pressure, so many other companies are experiencing these days. I have to admit, I was very pleasantly surprised with the performance of Kemira in the first semester

{kind=link}

Kemira has its main listing on the Helsinki Stock Exchange, where it is trading with KEMIRA as ticker symbol. The average daily volume in Finland is approximately 130,000 shares per day, making it the most liquid venue to trade in the company’s shares. As there currently are 153.6M shares outstanding, the current market capitalization is almost 2.18B EUR. Kemira pays a 0.62 EUR dividend for a yield of approximately 4.4% but as the Finnish dividend withholding tax is 35%, I don’t think the dividend should be a main consideration unless it is easy to reclaim the Finnish taxes.

A surprisingly strong result in the first half of this year

This article is meant as an update to the previous article. To get a more detailed overview of Kemira’s business model, I’d like to refer you to the older article.

While the paper and pulp business was weaker than expected (Kemira refers to the continuous destocking of inventory levels of the end users of the paper and cardboard), the water treatment and industrial division really picked up the pace and for the first time in the history of the company, that division generated a higher EBITDA than the paper and pulp division . That’s great because it also was one of my main reasons to initially invest in Kemira.

Kemira Investor Relations

Pulp & Paper revenue & EBITDA results can be found above, and the performance of the industrial water division is shown below.

Kemira Investor Relations

The total revenue in the first half of the year was approximately 1.75B EUR and this resulted in an EBITDA of 332M EUR. That’s about 40% higher than in the first half of 2022 while the Q2 EBITDA came in at 147.4M EUR, an increase of just over 15%. This definitely did mean the Q2 EBITDA was lower than in the first quarter, but that’s fine, as the weak performance in the paper and pulp division means we shouldn’t expect too much of this year. That being said, the company did reconfirm its full-year EBITDA guidance (which I will discuss later in this article) so it looks like the industrial & water treatment division will indeed make up for the weaker paper and pulp segment.

Kemira Investor Relations

Looking at the Q2 net income, the total EPS was about 0.42 EUR, which brought the H1 2023 EPS to 1.03 EUR.

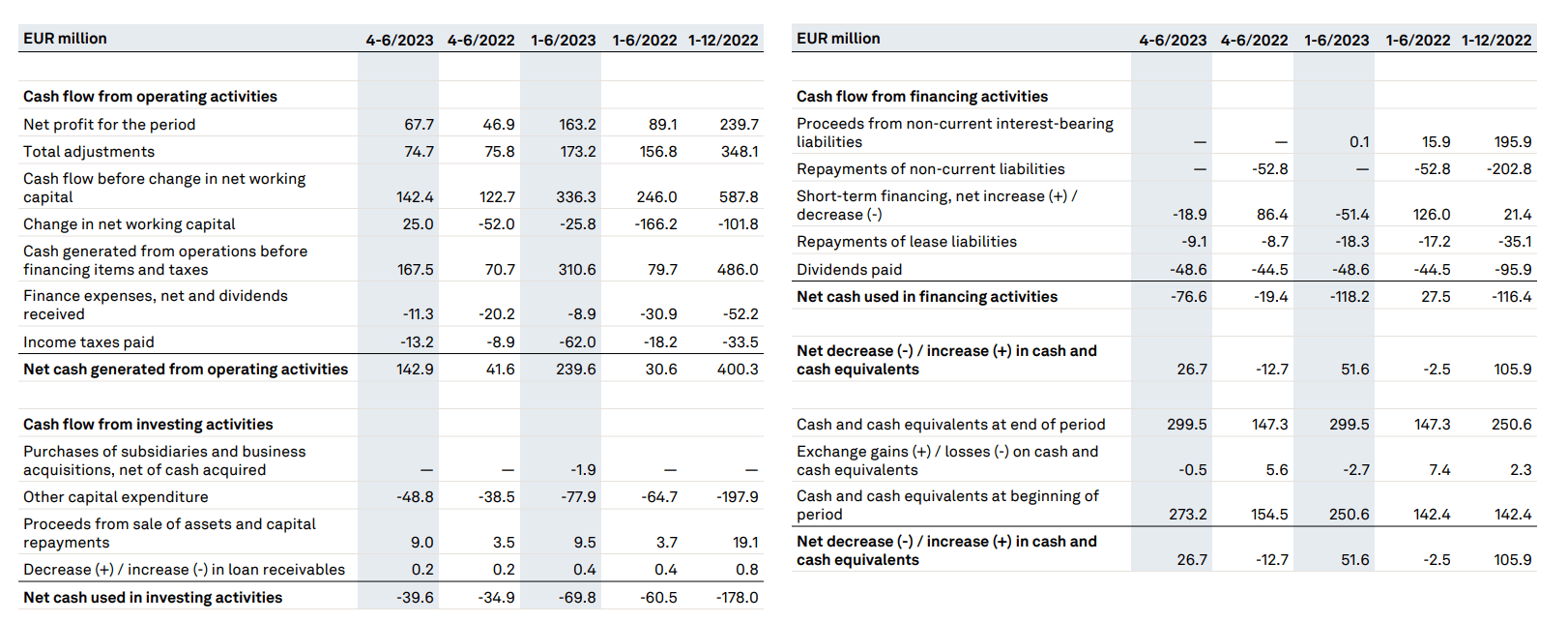

My initial thesis for Kemira was based on the free cash flow result of the company and the undervaluation based on that result, and that is still the case.

Looking at the H1 operating cash flow, we see the total operating cash flow was 240M EUR on a reported basis. This includes a 26M EUR investment in the working capital position but excludes the 18M EUR in lease payments. It also includes about 18M EUR in cash taxes that were not owed based on the H1 income statement. This means the adjusted operating cash flow was approximately 266M EUR.

{kind=link}

As you can see above, the total capex was approximately 78M EUR, which results in a 188M EUR free cash flow result. That is excellent, but we can’t just annualize that result as the total capex in the first semester was pretty light: traditionally, Kemira’s capex really ramps up in the second half of the year. So I’ll try to run the numbers based on the official guidance.

Despite already generating 331.5M EUR in EBITDA and 344M EUR in ‘operative’ EBITDA, Kemira is guiding for a full-year operative EBITDA of 550-650M EUR. The lower end of that range would indicate the H2 operative EBITDA would be more than a third lower than the H1 EBITDA, but just to err on the side of being cautious, I’ll use a 560M EUR operative EBITDA and a 540M EUR EBITDA on a reported basis. We know the total annual depreciation and amortization expenses currently run at 202M EUR resulting in a net EBIT of 338M EUR and a pre-tax income of 295M EUR. Applying an average tax rate of 22% (slightly higher than average), the net income would be 230M EUR, of which I expect 215-220M EUR to be attributable to the shareholders of Kemira. Divided over 154M shares, this indicates a full-year EPS of 1.41 EUR per share. The total sustaining and improvement capex will be around 155M EUR (with an additional 40-60M EUR in expansion capex, which means the sustaining free cash flow will be about 5–7 cents per share higher at close to 1.50 EUR per share.

Investment thesis

That makes the current share price quite appealing as the stock is trading at approximately 9.5 times earnings and a free cash flow yield of around 11% (and an EV/EBITDA multiple of just 5 based on the lower end of the EBITDA guidance for 2023). Sure, the paper and pulp division will need a few more months and perhaps quarters to recover, but in the end it will do so given that destocking and restocking is just the normal cycle a company goes through. Kemira enjoyed the tailwinds of the restocking and now just has to deal with the temporary headwind of the destocking. That’s life, and I am very happy to see the other division is stepping up the plate.

Kemira is also putting its feelers out to sell its oil and gas division (polymers are used to improve the oil recovery ratio in existing and semi-mature fields) so I am curious to see if it gets a fair price for that. I would be disappointed if that division gets sold at a multiple of less than 6-7 times EBITDA, no matter how cyclical being a supplier to the oil industry might be. The stock still is a ‘buy’ based on all metrics, even if Kemira only reaches the lower end of its EBITDA guidance.

I currently have no position in Kemira anymore after selling earlier this year, but I am interested in re-establishing a position on weakness.

For further details see:

Kemira: A Finnish Specialty Chemicals Company Trading At Just 5 Times EBITDA