KMPH - KemPharm: Now A Rare Disease Play Upgrading To A Buy Rating

Summary

- We initiated KemPharm with a Sell rating in March 2021; since then, the stock has declined >40%, and now the stock is trading at an attractive enterprise value of $130m.

- AZSTARYS targeting ADHD has been approved, and it no longer contributes much to the stock price at this point. Arimoclomol targeting NPC is the next focus.

- We believe Arimoclomol should be considered as an option value rather than a high conviction bet due to some efficacy and safety overhang.

- We upgrade to a Buy rating based on the cheap valuation and potential optionality of Arimoclomol moving into 2023.

Key updates for investors

Since our first initiation report , the company has made considerable efforts to transition the company from an ADHD play to a CND-focused rare disease play ((NPC)). The biggest news was KemPharm acquiring Arimoclomol from Orphazyme, a distressed European biotech, in May 2022, for $12.8m.

"This strategic acquisition of arimoclomol is a transformative event that significantly expands our rare CNS disease development pipeline, bringing to KemPharm an NDA-stage, revenue-generating product upon which we intend to build commercial capabilities that allow KemPharm to create and retain value for the benefit of shareholders," stated Richard Pascoe, Executive Chairman of KemPharm. "Moreover, the financial structure of the acquisition combined with the revenue currently being generated by arimoclomol from the early access program in France affords us the opportunity to acquire the asset in a capital efficient manner that has the potential to create positive cash flow, while incurring no shareholder dilution."

Interestingly, the Arimoclomol acquisition will allow the company to gain a small source of cashflow from the early access program in France, which is the only country where unapproved candidates can receive reimbursements.

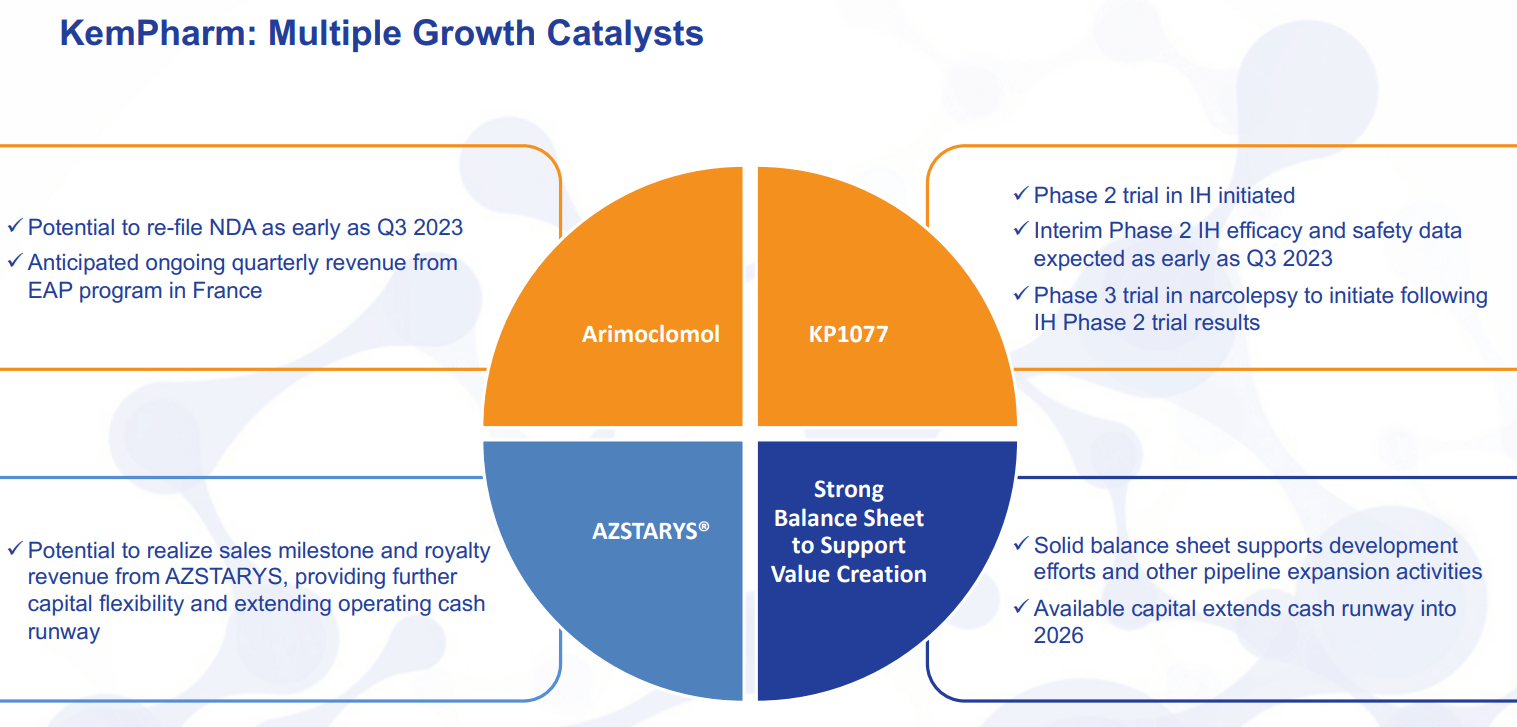

Key catalysts (Company IR presentation)

{kind=link}

Arimoclomol an interesting asset, but the risk remains

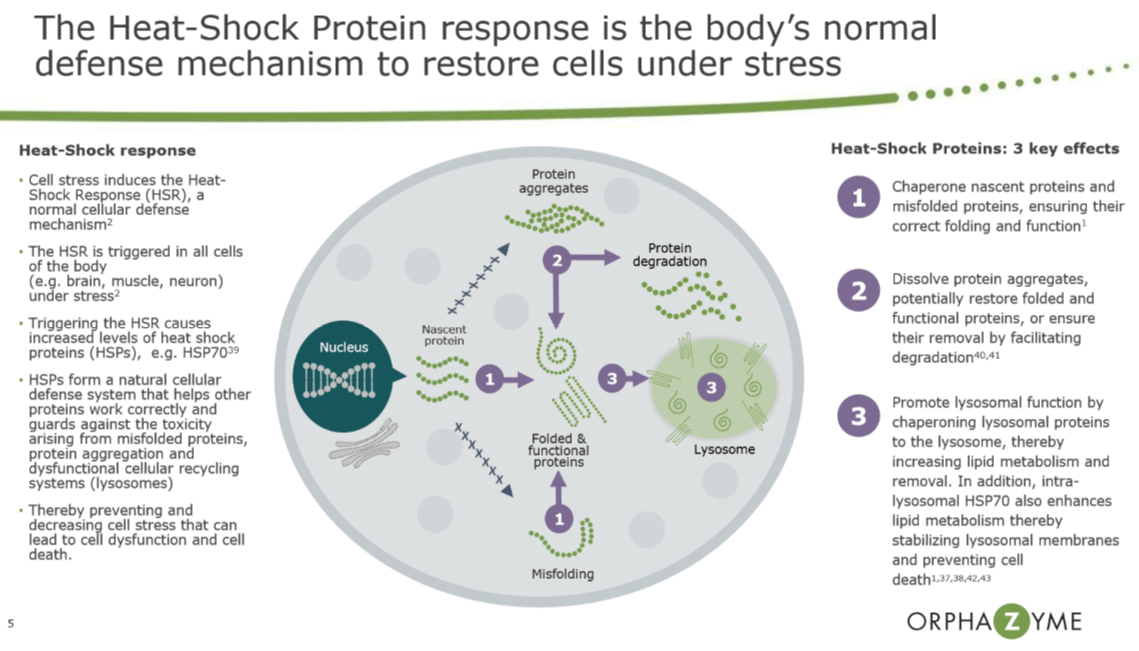

Arimoclomol is believed to stimulate a normal cellular protein repair pathway by activating molecular chaperones and activating heat shock response by acting on Hsp70. We believe this platform could have potential opportunity in many diseases. However, arimoclomol has a few chink in its armor, Orphazyme received a Complete Response Letter ((CRL)) from the FDA on Jun 17, 2021, regarding NDA for arimoclomol for the treatment of NPC.

The FDA identified three issues :

1) Additional evidence needed to support use of the NPCCSS as the primary instrument in measuring NPC disease progression.

2) Required additional analysis related to how missing data is handled for statistical analysis.

3) Required additional support and data related to confirmatory evidence of efficacy

The FDA did not request additional efficacy data in the CRL

Based on the managements' comment , after the Type A end-of-review meeting held last year, there was some interesting progress made regarding the resubmission of the NDA.

Type A End-of-Review Meeting was held on Oct 13, 2021:

- FDA agreed to allow a reanalysis of the 5-domain NPCCSS removing the cognition domain.

- FDA agreed to a rescoring and a reassessment of the swallowing domain including a qualitative study to further validate that domain.

- FDA agreed to further discussions regarding the primary instrument, NPCCSS, the analysis of the data after rescoring and the need for additional confirmatory evidence prior to resubmission of the NDA.

Based on the constructive meeting with the management, KemPharm seems to be planning to resubmit a NDA for arimoclomol in NPC around Q3 2023. Although, the management indicated that no new issues or concerns have been raised by the FDA and no new efficacy trial has been proposed by FDA, we believe it is possible that they request another clinical trial or pre-clinical trial which can delay the process. On a positive note, if approved, the drug may be eligible for a Rare Pediatric Disease Priority Review Voucher, which can be sold to another pharmaceutical company. The last two vouchers were sold in 2022 for around $110m each.

Niemann-Pick Type C is a fatal rare disease without an approved treatment

Niemann-Pick Type C ((NPC)) is a rare genetic, and progressive disease caused by mutated NPC1 and NPC2 genes that impair the ability of the body to recycle cholesterol and other lipids. This damage to the body's tissue, including the brain. For the pediatric population, this condition can be very fatal, starting from the first month after birth. The key symptoms of NPC in the pediatric patient population are:

- Jaundice

- Cholestasis

- Failure to thrive, or growth deficiencies

- Enlargement of liver and spleen

- Hearing loss

- Loss of muscle tone

- Cerebellar ataxia

For adult patients, NPC is usually an progressive disorder that is not diagnosed until adulthood and can lead to cerebellar ataxia, dysarthria, dysphagia, cognitive impairment, and other movement disorders such as dystonia or tremor.

Currently, the only available treatment is Miglustat (approved in the EU, used off-label in the US), a glucosylceramide synthase inhibitor, which is a competitive inhibitor of the enzyme glucosylceramide synthase that catalyzes the first step in glycosphingolipid ((GSL)) synthesis, the glycosylation of ceramide. It was shown to delay the onset and progression, but it is not a disease-modifying therapy and also cannot be used in patients under 6 years old, limiting its use case order children.

Arimoclomol mechanism of action (Orphozyme)

{kind=link}

The key pathophysiology of the disease is known to be caused by NPC1 and NPC2 genes, which are mutated and cause protein products to be misfolded. Arimoclomol is unregulated and sustains HSP70 expression, which can chaperone NPC1 to both prevent and correct protein misfolding, directly improving lysosomal function. Furthermore, intra-lysosomal HSP70 enhances lipid metabolism and stabilizes lysosomal membranes, and prevents cell death.

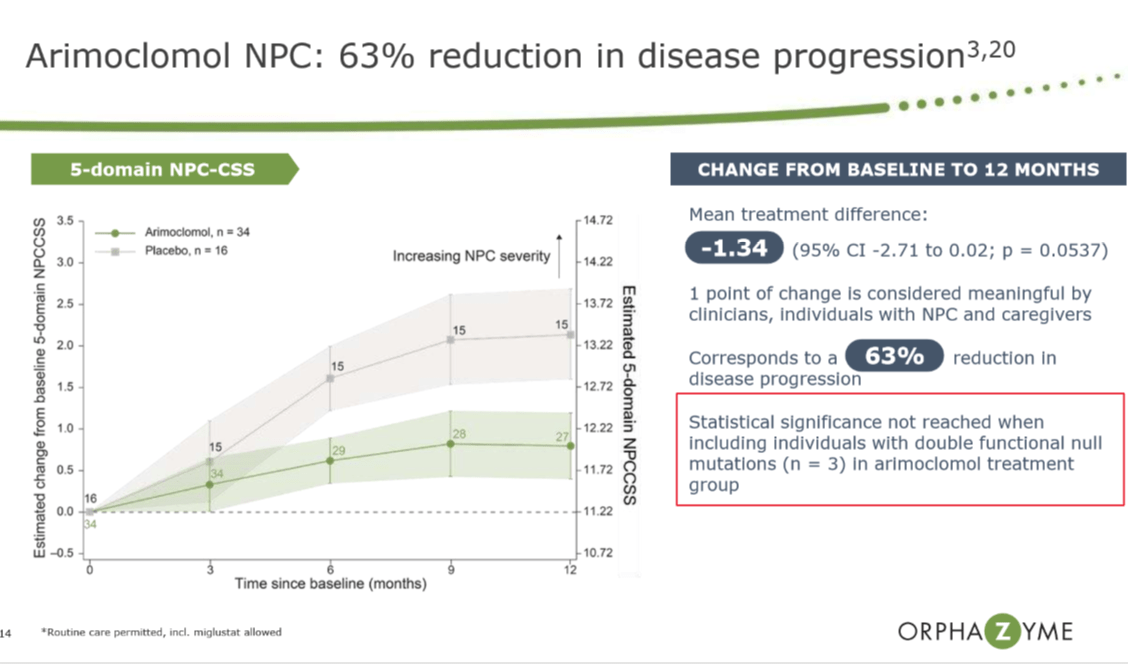

The phase 2/3 trial was promising, although the cognitive endpoint did not meet statistical significance.

The phase 2/3 trial was a double-blind, placebo-controlled study that enrolled patients who are 2-18 years old and diagnosed with either NPC1 or NPC2 (Miglustat only showed benefit in older age children aged>6 years old). 5-domain NPC CSS score was used to evaluate the efficacy of the drug:

- Ambulation - is the ability to walk without the need for any kind of assistance

- Fine motor skills

- Swallow - highly linked to mortality

- Cognition

- Speech

Arimoclomol phase 2 data (Orphazyme deck)

{kind=link}

5 endpoints were met. However, the trial showed no benefit in cognition. However, this is fairly de-risked at this point as FDA agreed to allow a reanalysis of the 5-domain NPCCSS, removing the cognition domain. We highlight that Miglustat received approval in Europe based on the 5 domain NPCSS data. Also, we note that arimoclomol did not meet the co-primary endpoint, CGI-I, which may or may not be a concern as CGI-I is known to have high sensitivity but low specificity and we see NPCCSS to be a more credible measure. We are also not worried about restoring and reassessing the swallowing domain, as the efficacy shown in the previous phase 1/2 trial seems compelling enough to us.

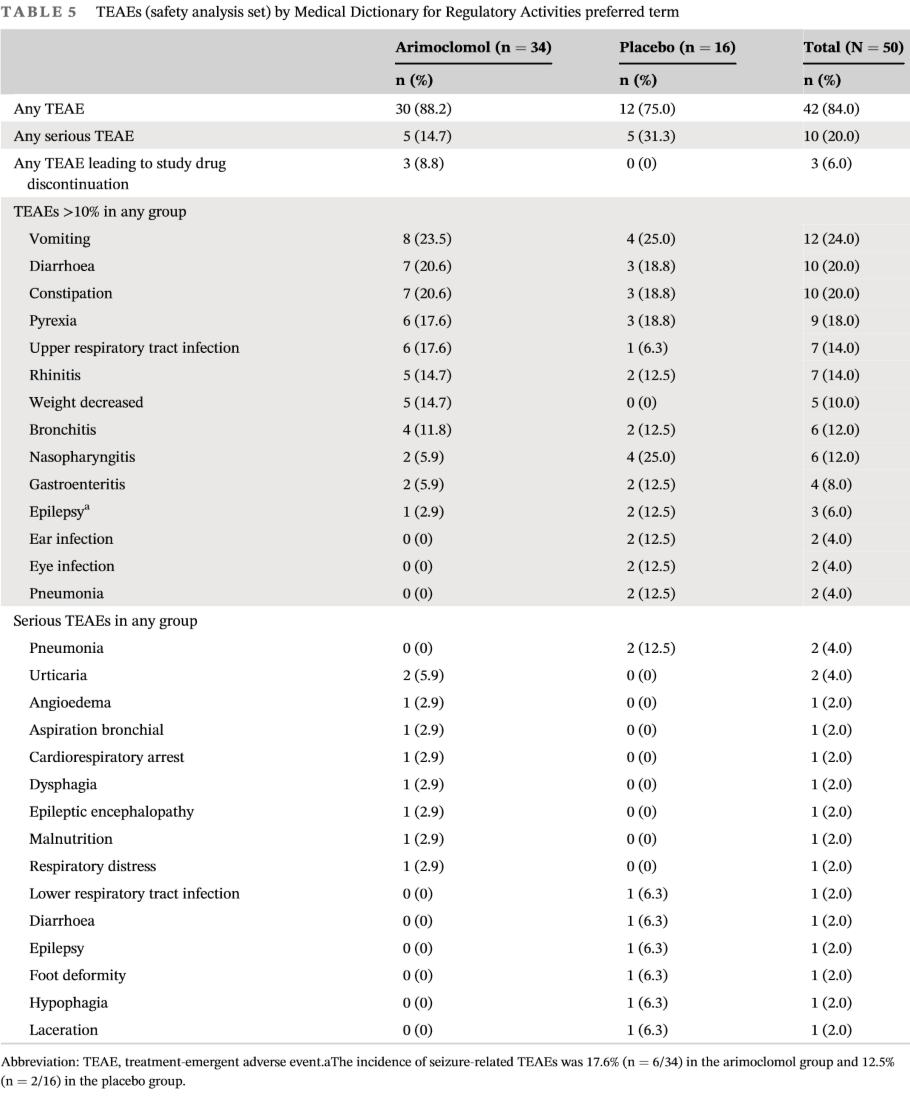

Regarding safety, three patients withdrew from the study in the drug arm due to urticaria/angioedema, and one patient died due to cardiopulmonary arrest. Based on this side-effect profile, the FDA requested another QT trial, which doesn't seem to be published by Orphazyme. Therefore, some safety-related overhang remains, albeit these side-effects may be due to NPC disease and not drug related. KemPharm seems to have additional 4 year safety data, which we believe will elucidate potential uncertainties around the safety of the asset.

Safety of arimoclomol (Efficacy and safety of arimoclomol in Niemann-Pick disease type C: Results from a double-blind, randomised, placebo-controlled, multinational phase 2/3 trial of a novel treatment)

{kind=link}

Azstrays expected to generate single-digit royalty steam for the company

The prodrug in both AZSTARYS is a serdexmethylphenidate targeting ADHD, and it is designed to offer extended-duration and once-a-day dosage form. In March 2021, FDA approved NDA for Azstrays, in patients who are six year and older, and Corium, the marketer of the product, launched Azstrays in the US around Q3 2021. For a detailed analysis of the clinical profile, please refer to our previous initiation article . However, since the approval, we have not seen any detailed information about how much royalty income the company received, which makes us think commercialization is not going well as planned. This is not surprising considering a small biotech is marketing the product where there is a high degree of competition from big pharma's brand name products and generics available. The company provided qualitative updates on the commercial uptake stating:

- Steady growth in prescriptions during market introduction phase in both breadth and depth of prescribing.

- Increasing number of pharmacies ordering AZSTARYS based on geographic areas in which Corium places sales representatives.

- Initial regional launch in 2021 and early 2022 focused on geographies with product coverage.

- As of July 2022, National field team deployed comprised of ~175 field sales reps.

- Held first AZSTARYS National Sales Meeting in July 2022 in connection with National launch.

- Significant market access success, with coverage of almost 145 million lives and preferred status for 35 million of those covered lives.

Source: IR Presentation

{kind=link}

Risks

Clinical risk remains as KemPharm has multiple ongoing trials. Competitive risk remains as ADHD is a highly genericized market. Capital raise risk remains, as the company may need to raise additional capital to fund its high cash burn.

Conclusion

We are upgrading KemPharm's rating to a buy rating because of a better risk/reward set-up at the moment with i) significantly cheaper valuation and rock-bottom market expectation, an enterprise value of ~$130m, and solid cash runway until 2026 with ~$107m of cash on hand, ii) potential optionality from arimoclomol and its potential approval in 2024, and iii) potential royalty income expected from Azstrays. At this point, we believe it makes sense to own a small optioned-size position.

For further details see:

KemPharm: Now A Rare Disease Play, Upgrading To A Buy Rating