HLIO - Kennametal: Still Appealing If Guidance Holds

Summary

- Kennametal had something of a rough start to its 2023 fiscal year, with sales rising but profits and cash flows pulling back in the first quarter.

- This is disappointing, but management's guidance still suggests that the company is a solid prospect.

- Add on top of this how cheap shares are, and it likely warrants further upside from here.

Because of concerns that are facing us today, you might not think that a company focused on metal cutting tooling and other products, as well as on the production and sale of various infrastructure products, would make for an attractive investment opportunity. But one business that does precisely this that has so far done quite well considering the circumstances we are facing is Kennametal ( KMT ). Although from a profit and cash flow perspective, the company has started its 2023 fiscal year off in a rather rough fashion, current guidance provided by management does not look awful when it comes to the 2023 fiscal year in its entirety. It is likely that shares will be a bit more expensive moving forward from a valuation perspective than they were previously. But considering how shares are priced even factoring that in, and when compared to similar firms, I think that some additional upside for investors is still on the table.

A rough start

Back near the end of October of last year, I wrote an article taking a bullish stance on Kennametal. In that article, I talked about how well the company had done from a revenue and profit perspective, as well as the share price appreciation perspective, over the prior several months. All things considered, I believed the company to be a robust operator in its space that the market rewarded appropriately. Even that being the case though, I felt as though there was some additional upside for investors moving forward. Because of this, I kept the ‘buy’ rating I had assigned the company previously. Thus far, that call has proven to be the right one. You see, while the S&P 500 is up 3% since then, shares of Kennametal have generated upside of 5.3%. And since I first assigned abolish rating on the company back in July of last year, the stock is up 23.1% compared to the 5.5% the broader market has achieved.

{kind=link}

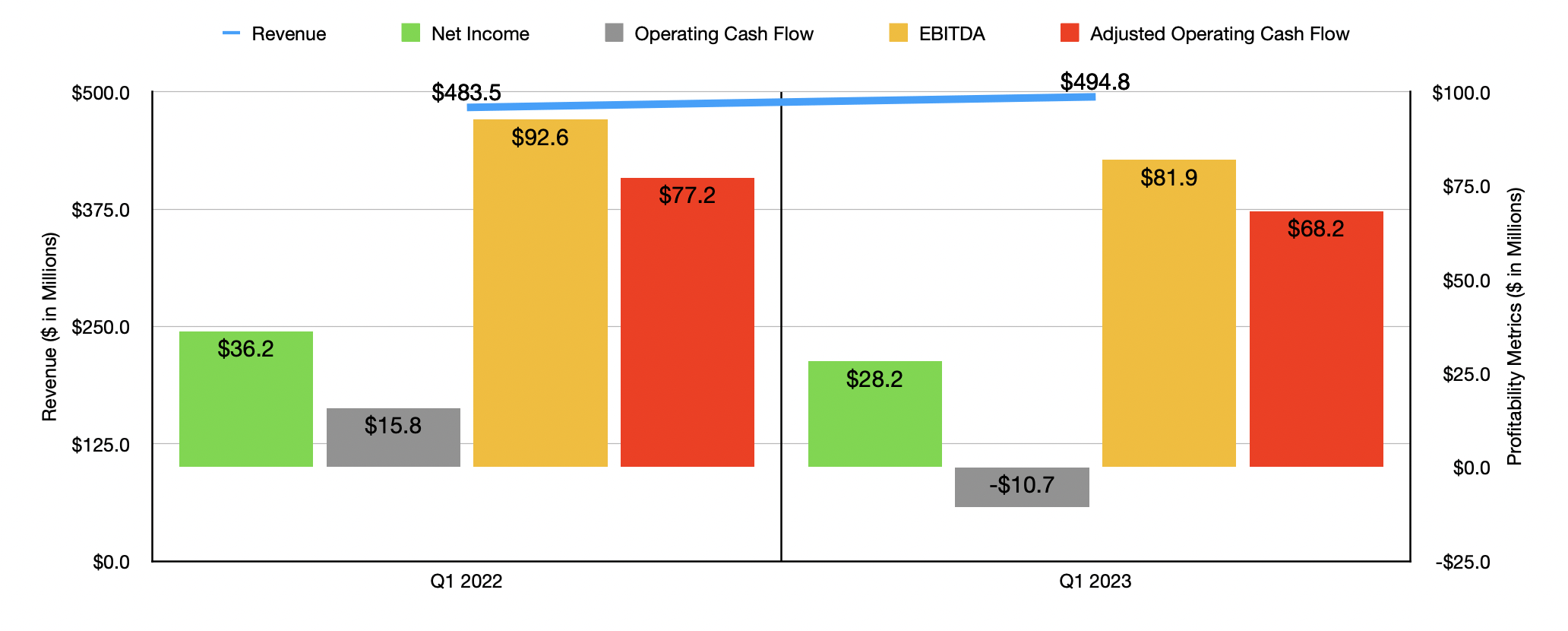

When I last wrote about the company, we only had data covering through the end of its 2022 fiscal year. Fast forward to today, and we now have data covering through the first quarter of 2023 . During that time, sales for the business came in at $494.8 million. That's 2.3% higher than the $483.5 million reported only one year earlier. At first glance, this looks anything but impressive. But actual organic growth for the company was a robust 9%. This was largely offset though by a 7% hit caused by foreign currency fluctuations. The strongest end market for the company from a growth perspective was the aerospace market. This makes a tremendous amount of sense when you consider the lag that the aerospace industry would see coming back to life following the COVID-19 pandemic. Even after factoring in the painful foreign currency fluctuations the firm had to deal with, revenue to those end market users jumped 18%. This was followed by the 11% experienced by the energy market. This is also logical when you consider how high oil and gas prices had risen over the past year or so. Higher pricing means higher profits and higher profits mean more investment.

Unfortunately, bottom line results achieved by the company came in a bit weak. Consider net income. During the first quarter, profits totaled $28.2 million. That's 22.1% lower than the $36.2 million reported the same time one year earlier. This was driven in part by a decline in the company's gross profit margin from 33.2% to 32.3%. Even though the company benefited from higher pricing on its products, increased sales volumes, and a favorable product mix, it was negatively impacted by higher raw material costs totaling $17 million, foreign currency fluctuations of $12 million, and $5 million from temporary supply chain disruptions. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, fell from $15.8 million to negative $10.7 million. If we adjust for changes in working capital, it would have dropped from $77.2 million to $68.2 million. And over that same window of time, EBITDA also pulled back, falling from $92.6 million to $81.9 million.

One really great thing about management now having reported data for the first quarter is that they also provided investors with guidance for 2023 as a whole. For the year, they are anticipating revenue of between $2 billion and $2.08 billion. This will be, unfortunately, not much different from the $2.01 billion reported for the 2022 fiscal year. Earnings per share, meanwhile, should be between $1.30 and $1.70. At the midpoint, that would translate to net income of $123.2 million. That's down from the $144.6 million the business generated in 2022. When it comes to operating cash flow, management said to expect free cash flow conversion of at least 100% of net income and capital expenditures of $100 million to $120 million. Using the midpoint figure there, this would work out to operating cash flow of $233.2 million. It's unclear whether management is assuming that working capital adjustments will be ignored or not. My interpretation of it is that this operating cash flow figure is comparable to the official GAAP operating cash flow that the company achieved in 2022 of $181.4 million. According to my own estimates, EBITDA for the company should be around $347 million.

{kind=link}

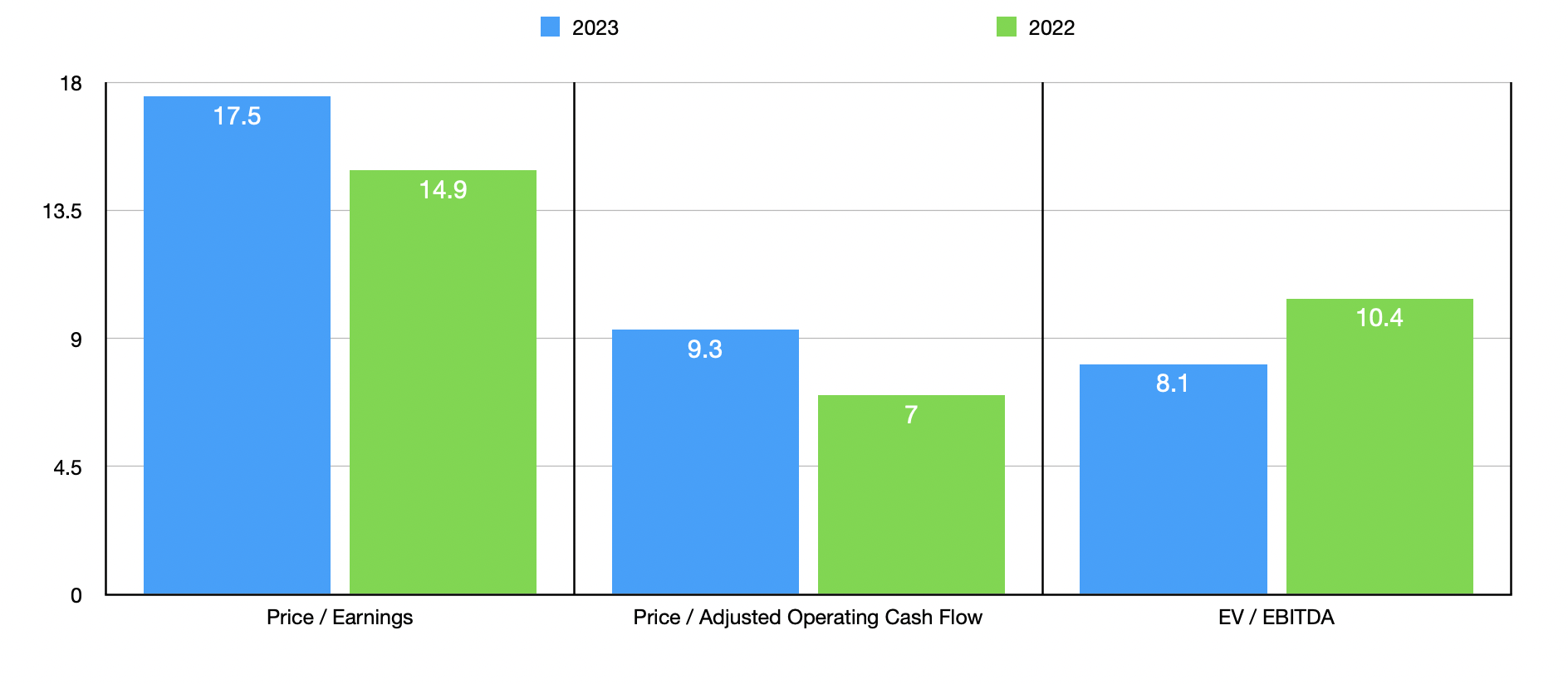

Based on these figures, the company is trading at a forward price to earnings multiple of 17.5, a forward price to adjusted operating cash flow multiple of 9.3, and a forward EV to EBITDA multiple of 8.1. If you look at the chart above, you can see how this pricing stacks up against house shares would be priced using data from its 2022 fiscal year. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 18.7 to a high of 88. Using the price to operating cash flow approach, the range was from 18.2 to 37.4. And when it comes to the EV to EBITDA approach, the range is from 11.9 to 17.5. In all three cases, Kennametal was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Kennametal |

| 17.5 |

| 9.3 |

| 8.1 |

| Barnes Group ( B ) |

| 88.0 |

| 26.9 |

| 17.5 |

| Kadant ( KAI ) |

| 19.7 |

| 18.3 |

| 12.0 |

| Helios Technologies ( HLIO ) |

| 18.7 |

| 18.6 |

| 11.9 |

| ESCO Technologies ( ESE ) |

| 29.9 |

| 18.2 |

| 15.6 |

| Mueller Water Products ( MWA ) |

| 25.3 |

| 37.4 |

| 12.5 |

Takeaway

The data that we have at our disposal today suggests to me that the 2023 fiscal year may not be as great as some might have wanted. Revenue might increase modestly and two of the three profitability metrics for the company are set to worsen. For some investors, this may be a sign to look elsewhere for opportunities. But when you consider just how cheap shares are compared to similar firms and you factor in that shares look affordable on an absolute basis, I believe it's difficult to rate the company anything lower than a soft ‘buy’ at this time.

For further details see:

Kennametal: Still Appealing If Guidance Holds