PPRUF - Kering: Stagnant Sales And Management Changes Don't Bode Well

2023-07-25 15:35:09 ET

Summary

- Kering SA has seen a 6.9% price decline since April, due to weak financial performance, particularly for Gucci, which accounts for half of the company's revenues.

- While its margins are attractive and attempts at reviving Gucci's growth are underway, management changes at the brand just before the H1 2023 results aren't a good sign.

- Kering's P/E is competitive compared to peers, but its performance and potential for growth is weaker, which can justify it. With an unclear future, the stock gets a Sell rating.

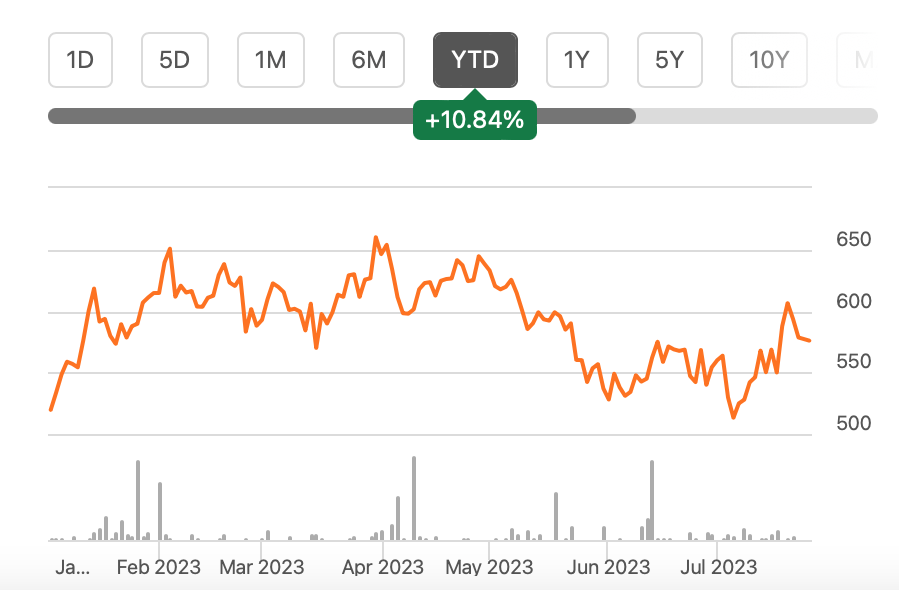

Since the last time I wrote about Gucci owner Kering SA ( PPRUF ) in early April, it has seen a 6.9% price decline. This isn't surprising, really. Even at the time, its financial performance was weaker than that of its counterparts. To be fair, though, in 2023 so far it has managed to rise by 11%. At the same time, it's worth mentioning that this is a slower increase than that seen by the S&P 500 Global Luxury Index, which is up by 22% .

Price Chart (Source: Seeking Alpha)

{kind=link}

But with its first half results (H1 2023) due later this week (Thursday, July 27 post-market ), could Kering be due for a price rise?

The Kering story so far

The last time I checked, Kering's full year 2022 sales growth was still strong, but had slowed down considerably in Q4 2022, even as its margins stays notably strong. I had gone with a Hold rating, considering the reopening of China's economy. There appeared to be potential for growth to pick up from the first quarter of 2023 (Q1 2023) onwards.

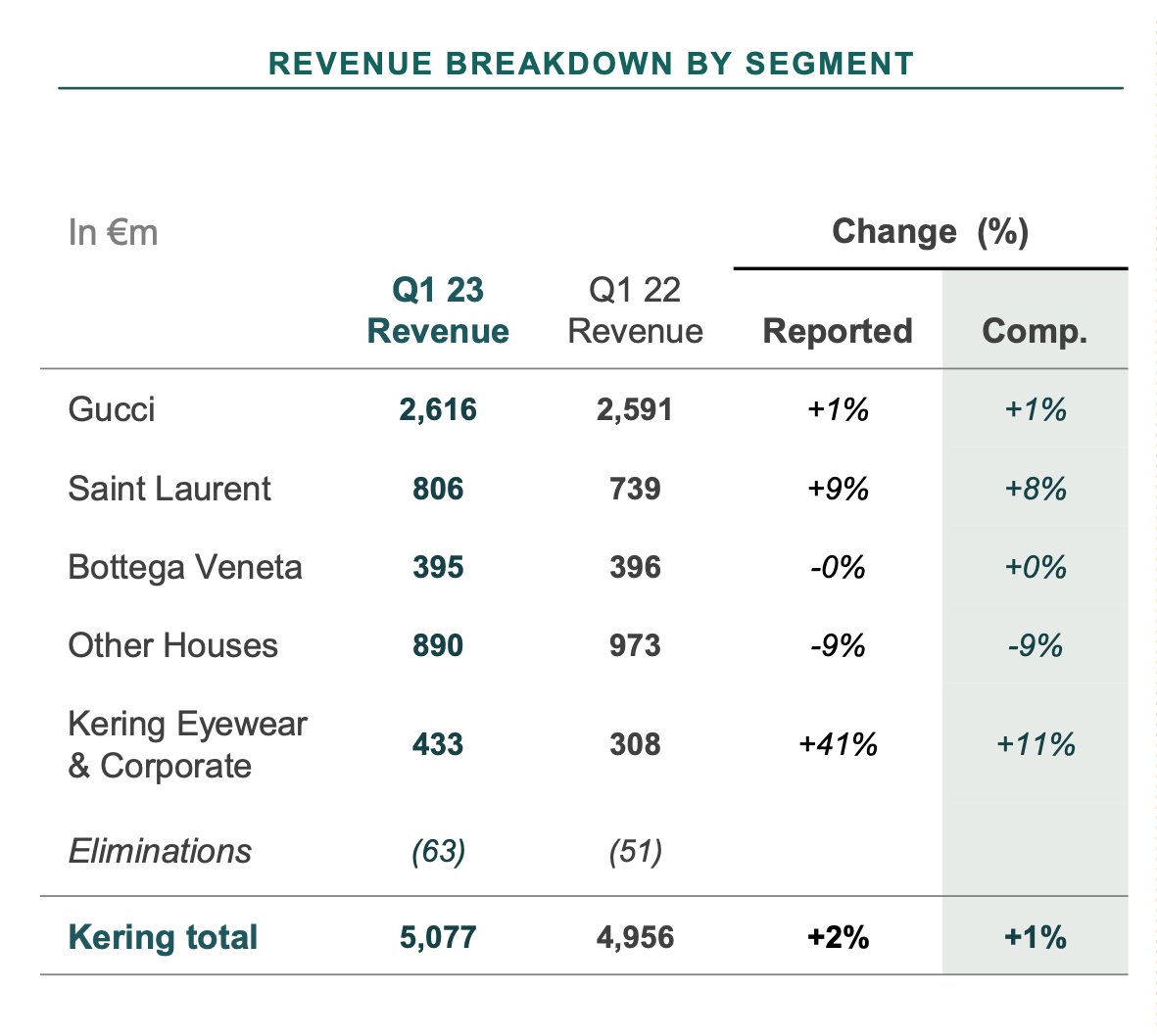

That hasn't happened quite as I had hoped. Kering reported an abysmal 2% year-on-year (YoY) reported sales growth and just 1% growth on a comparable basis in Q1 2023. Most notably, this was because of Gucci's slow-moving sales (see table below), which is a downer considering that it accounts for half the company's revenues.

The "Other Houses" revenue also declined sharply, which includes brands like Balenciaga and Alexander McQueen. This segment has a relatively lower revenue share, so its impact is lesser, but at 17% the share is by no means trivial. So, I would look out for the numbers for this segment in the upcoming results.

{kind=link}

The Gucci challenge

The challenge with Gucci is not just that it adds so much to Kering's top line. It also has the biggest margins across all the brands. At 35.6%, it exceeds the company's even otherwise strong overall recurring operating margins at 27.5% for 2022.

But if its sales continue to lag, it's only a matter of time before the margins decline too, which will make the company lose its competitive edge. So far, its operating margin is second only to the Birkin maker Hermès ( HESAY ) among luxury peers. Watching out for changes to the company's operating margin in the release of its results release will be important, keeping this in mind.

Regional growth disappoints

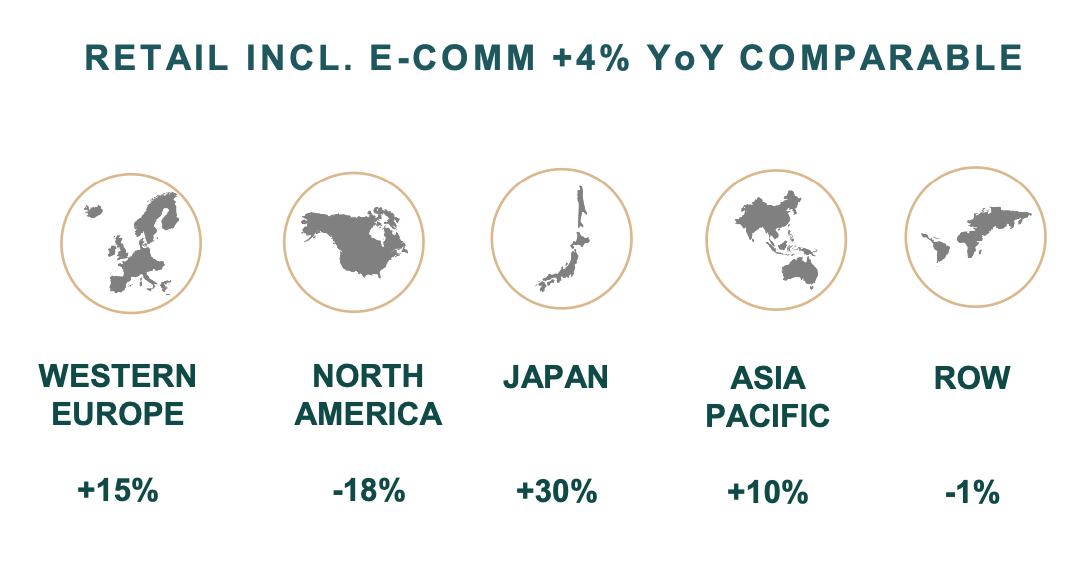

Additionally, the first quarter was a good indication of how revenues will move in its important Asia Pacific market, which has a 40% share in the total, since consumers in China spend big during the Lunar New Year early in the year. Kering has seen 10% year-on-year (YoY) retail sales from the region, which isn't bad, but it is soft compared to other luxury companies like LVMH ( LVMUY ) and Hermès .

It doesn't help that its North America sales have dropped drastically too (see chart below), which hasn't happened quite the same way for other luxury companies. Sure, they are slower than in other regions, but they have not swung deeply into demand drop as with Kering. There's nothing to suggest so far that the company's sales growth would have changed direction in Q2 2023.

{kind=link}

Hope for margin expansion

For H1 2023, however, even if sales remain weak, the company could see margin expansion. Producers' costs are falling more rapidly than consumer prices around many major markets like China, Eurozone and the U.S. Luxury fashion houses don't have to stress much over whether or not to pass on costs to end consumers, so they can maintain their margins anyway.

The catch here however is, that other luxury brands can see a commensurate rise in their margins too. And their faster sales indicate higher demand and the ability to raise prices too. To me, this implies that Kering's one competitive edge can be lost fast, but that remains to be seen for now.

Reviving Gucci

Unless of course, Gucci can come back with a bang. The company's certainly making moves to ensure a revival for the brand. It got new creative designer in Sabato De Sarno in February this year.

He earlier worked with big brands like Prada ( PRDSY ), Dolce and Gabbana and was most recently at Valentino for the past nine years. His first collection for the brand debuts in September this year, which will give a better sense of how his creativity is received.

But there's a catch here too. Last week, Gucci's CEO since 2015, Marco Bizzarri, stepped down . De Sarno was supposed to report directly into him. Management changes, while inevitable from time to time, create uncertainty for the stock. It certainly leaves me wondering what, if anything, it means for the brand's new creative head. Further, that this announcement comes close to the heels of Kering's H1 2023 results isn't a good sign.

The context for market valuations

Kering's valuations are quite attractive compared to its luxury peers, though. At 18.8x, its trailing twelve months [TTM] price-to-earnings (P/E) ratio is way lower than that for LVMH at 32.2x , Hermès at 62x and even Richemont ( CFRUY ) at 21.6x .

But there's a reason for them to trade higher. And that's their performance. All of them have seen stronger Asia-Pacific growth and positive Americas' growth, which is more than what can be said for Kering. Hermès, as noted above, already has a stronger margin than PPRUF as well, and LVMH and Richemont are awfully close to it, too. It's also worth noting that analysts expect is earnings to decline this year .

What next?

Instead of the scenario improving for Kering since the first time I wrote about it in October last year, it has actually worsened. Revenue growth has declined more than it has for peers, and its margins might not stand out among them for long.

Sure, it has appointed a new creative director, presumably to reinvigorate the sagging but important Gucci brand, but we are yet to see the fruits of his vision. In the meantime, the company's top management has moved around. Most significantly, Gucci's CEO, who De Sarno was meant to report into, has quit.

It's possible that a new CEO along with a new creative head can bring Gucci back to high growth. But for now, it's clear that Kering's relatively lower valuations compared to other luxury stocks is less a sign that it's a Buy, and more a signal of its weakness compared to them.

In fact, going by its Q1 2023 trading statement, I'm not entirely hopeful for its foreseeable future. Considering that its price has already risen YTD and over the past year, it's a good sign to exit. There are better performing luxury stocks to buy . I'm going with a Sell on Kering. If things show signs of improvement, this rating can be reconsidered.

For further details see:

Kering: Stagnant Sales And Management Changes Don't Bode Well