KDP - Keurig Dr Pepper: A Leader In The Beverage Industry

Summary

- KDP is a leading coffee and beverage company in North America.

- KDP holds a wide array of leading brands in soft drinks, specialty coffee and tea, water, and others markets.

- KDP has achieved a debt reduction of $3.8 billion since the merger between Dr Pepper Snapple and Keurig Green Mountain.

Business Overview and Investment Thesis

Keurig Dr Pepper ( KDP ) is a leading coffee and beverage company in North America, with annual revenues in excess of $13 billion. KDP holds leadership positions in soft drinks, specialty coffee and tea, water, juice and juice drinks and mixers, and markets the #1 single serve coffee brewing system in the U.S. KPD is active in the approx. $200 billion North American non-alcoholic beverage market where the company maintains an unrivaled distribution system that enables its portfolio of more than 125 owned, licensed and partner brands. Some of its key brands include Keurig, Dr Pepper, 7 Up, Canada Dry, Snapple, Crush, Squirt, Sun Drop, Green Mountain, etc.

{kind=link}

KDP is an attractive company that offers stable returns through dividends and share buybacks. It is in a quite stable market, as such its growth is highly linked to inorganic growth through acquisitions. In fact that is how KDP was formed, through the merger of Dr Pepper Snapple and Keurig Green Mountain. More on this at a later stage. The company currently holds a market valuation of $50 billion, with the market providing a dividend yield of approx. 2.3%. It should be mentioned that the company is able to generate substantial free cash flows of $2.5 billion. Saying this, KDP also has to repay a significant amount of debt in the coming years, this debt came as a result of the previously mentioned merger. I believe it would be wise to hold and either wait for a more attractive entry point or wait until more debt has been repaid.

The Making of Keurig Dr Pepper

The company Keurig Dr Pepper came to be as a result from the merger of Dr Pepper Snapple and Keurig Green Mountain in 2018. The merger at the time created the seventh-largest company in the U.S. food and beverage sector and third-largest beverage company in North America. The main actors in this merger were JAB Holding, an investment firm holding investments in coffee and beverage, fast casual restaurants, pet care, and other industries and Mondelez International ( MDLZ ). JAB and Mondelez are still some of the biggest shareholders in KDP, with ownership of the company at 34% and 5.3% , respectively. It should be noted here that both parties have sold down part of their percentages in recent years.

The newly formed company had one main issue which was the high debt levels it had in its balance sheet. At the time of the merger KDP had debt levels of approx. $16 billion while it generated revenues of $11 billion. As you can see there is pretty significant discrepancy here. However, the company was able to generate substantial free cash flow which would allow the company to deleverage at a somewhat fast pace. Since then, management has done a great job, reducing debt to $12 billion as of the end of 2021. Let´s take a deeper look into the financials!

Financial Overview

KDP Financial Highlights (Company Annual Reports)

KDP is a leading coffee and beverage company in North America, with annual revenue in excess of $13 billion. During the trailing twelve months revenues stood at $13.6 billion, cash flow from operations of $3 billion, and free cash flow of $2.7 billion. This performance indicates an improvement compared to FYE 2021 financials.

During 2021, KDP generated revenues of $12.7 billion through its 4 segments consisting of Coffee Systems, Packaged Beverages, Beverage Concentrates, and Latin America Beverages. The company´s top revenue generating segments are the Coffee Systems and Packaged Beverages segments amounting to 84% of total revenues. However, it should be mentioned that the Beverage Concentrates segment generates the highest operating income margin, standing at 70% and 62% during 2021 and 2020, respectively. In essence the Beverage Concentrates segment only contributes about 12% to the company´s revenues but it contributes 36% to the company´s operating profit.

As it can be seen from the table above, KDP has increased its operating income in a consisted manner since 2019. Further to this, the company has also been able to decrease interest expense by about $100 million in the past years. This is a result of the substantial debt repayments since the company was formed. The improved financials have helped KDP to increase its margins with profit margin reaching 16.9% during 2021. It will be interesting to see if management can keep this levels or even improve them with time.

KDP is also able to generate a robust cash flow from operation, reaching $2.9 billion in 2021. Due to the relatively low capital expenditures, the company is able to keep above 85% of its cash flow each year. This is what helps KDP to pay debt at a fast pace as well as return value to its shareholders.

The company also holds a strong liquidity position, which currently stands at $4.9 billion, consisting of cash and cash equivalents of $925 million (as of the most recent quarter report ) and a $4 billion committed revolving credit facility. The reason for this strong liquidity position is the fact that KDP still has a relatively high debt position. As it will later be seen, management has done a great job deleveraging the company.

Shareholder Returns

KDP Shareholder Returns (Company Annual Reports)

Albeit at a weak growth rate, KDP has increased shareholder returns during the past 3 years. Management approved a dividend per share of $0.80 per share at the end of 2022. The board of directors also authorized a share repurchasing program of $4 billion. KDP just started using this program spending around $88 million in share repurchases during the first 3 quarters of 2022.

Due to the cash flow constraints which will be discussed in the following section, it is unlikely that investors will see a substantial increase in dividends or for the share buyback program to be used aggressively. It is more likely that investors will need to wait a couple of years for this to start happening.

Reducing Debt and Extending Maturity Profile

KDP Debt Overview (Company Annual Reports)

{kind=link}

From 2018 to 2021, management has paid down about $3.9 billion in debt. This has allowed the company to achieve a net leverage reduction from 9.8x in 2018 to 3.99x in 2021. Please note I am using a different net leverage formula than what the company uses. I am using cash flow from operations instead of Adjusted EBITDA as I believe we should always focus on the actual cash the company brings in. In its 2021 annual report, the company actually reported a net leverage decrease from 6.0x in 2018 to 2.9x at the end of 2021 . Regardless, in both instances it can be seen KDP has significantly decrease its net leverage position, which is a testament of what the company is able achieve.

KDP Debt Maturities (Company Annual Report)

{kind=link}

Management has spread-out the debt maturity profile of the company pretty well. Here it should be mentioned that the company will have to pay an average $1.4 billion every year between 2023 and 2025. This is of course if management does not refinance a portion of this debt. As an exercise, to understand the impacts of these debt repayments, let´s put the cash flow from operations against the cash outflows the company will face during the next 3 years. If we assume cash flow from operations will average about $2.9 billion per year, the company will have to pay about $500 million in capital expenditures, leading to a free cash flow of approx. $2.4 billion. With the current dividend per share at $0.80, we have a dividend payment of ~$1 billion. Finally, KDP will need to pay on average $1.4 billion on debt repayments for the next three years. Taking these cash outflows into consideration we can see that all the cash flow will be used.

Because of this the company will have a tough time doing share buybacks, bolt on acquisitions, or increasing dividends. Saying this, it should be noted that KDP currently holds a very robust liquidity position of $4.9 billion which gives it financial flexibility. From these calculations it can be appreciated that KDP will have constrains as a result of different cash outflows. Nonetheless, once debts are repaid, there will be more opportunities for growth.

Valuation

With the current market valuation at $50 billion, I believe the company is well priced. At the current share price, the dividend yield is ~2.3% with the opportunity to grow constrained by debt repayments in the near future. I believe there are other companies offering a more attractive dividend yield in this space.

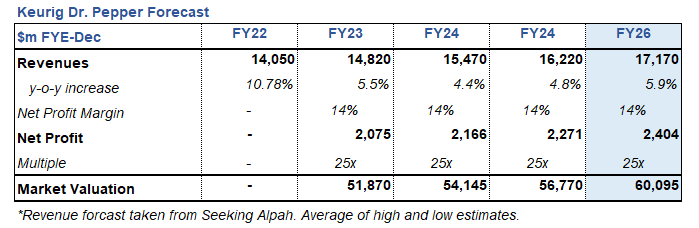

For the valuation of the company, I have used the market multiple method, using future forecasted earnings to a 25x multiple, which is largely in line with the multiple the market has given it since 2019. I have obtained the analysts' revenues forecast from Seeking Alpha data and have applied net profit margin of 14%. This is slightly conservative compared to the net profit margin from 2021 at 16.9%. I arrive at a market valuation of $60.1 billion by FYE 2026.

KDP Forecast (Seeking Alpha and Author´s Estimates)

{kind=link}

Risks

Customer Concentration:

During 2021, KDP stated in its annual report that its largest retailer was Walmart (WMT), representing approximately 16% of net sales. Any dispute or relationship break up with Walmart could have serious consequences for the company. This risk is somewhat low due to KDP extensive and well recognized bucket of brands. It should also be noted that Walmart does represent a significant percentage of sales for many players in the industry.

Competition:

As we all know the beverage industry is highly competitive with well established companies vying for market share. KDP runs the risk of competing in this environment. For example, KDP competes with Coca-Cola ( KO ) and PepsiCo ( PEP ) in CSD, NCB and Coffee categories. The company also competes with Kraft Heinz ( KHC ), Nestle ( OTCPK:NSRGY ) and J.M. Smucker ( SJM ) in the packaged coffee market. As it can be seen these are truly outstanding competitors KDP faces.

High Debt Position:

As mentioned throughout the article, KDP has a relatively high debt position which management has been able to reduce since the merger between Dr Pepper Snapple and Keurig Green Mountain. Although management has made great strides to deleverage the company, KDP still has pretty significant debt maturities between 2023 and 2025. The amount to be repaid crosses the $4 billion mark. This risk is mitigated by the company´s robust free cash flow generation.

Bottom Line

KDP is a company with robust financials and a strong presence in the ~$200 billion North American non-alcoholic beverage industry. KDP is able to generate substantial free cash flow of $2.5 billion, providing the company the resources to pay dividends while at the same time repaying debt. Speaking about debt, KDP will have to repay a substantial amount of debt in the coming years which will constrain a more aggressive shareholder return policy. Considering the latter, it may be wise to wait for a more favorable entry point or until a portion of debt has been repaid.

For further details see:

Keurig Dr Pepper: A Leader In The Beverage Industry