KDP - Keurig Dr Pepper: Buy For Dividend Growth And Safety

Summary

- Keurig Dr Pepper is the market leader in single-serve coffee systems and K-Cup pods.

- The company has well-known coffee, soda, water, tea, and other brands.

- The firm has built a third non-alcoholic distribution network.

- Revenue, earnings per share, and the dividend are growing.

- The stock is undervalued.

As any long-time owners of a non-alcoholic beverage stock will tell you, they are great for dividend growth and safety. Indeed, Coca-Cola ( KO ) has created significant wealth for many shareholders. In fact, the company is a leading dividend growth stock with 61 years of increases and one of the longest dividend-paying stocks. But what about other non-alcoholic stocks?

Today, we discuss Keurig Dr Pepper ( KDP ), the third leading non-alcoholic beverage company in the United States. It was created from the merger between Keurig Green Mountain and Dr. Pepper Snapple in 2018. The company is relatively new in the current organization but is returning cash to shareholders through a growing dividend. Moreover, the valuation is below its normal range and more reasonable than its two larger competitors. Hence, we view Keurig Dr Pepper as a buy.

Overview of Keurig Dr Pepper

The merger of Keurig Green Mountain and Dr Pepper Snapple Group in 2018 created Keurig Dr Pepper. The merger also created a third sizeable non-alcoholic beverage distribution network. Before, Coca-Cola and PepsiCo ( PEP ) were the only two companies controlling a distribution network.

In addition, the firm owns popular and well-known brands, like Dr. Pepper, Canada Dry, Sunkist, A&W, 7UP, Schweppes, Bai, Mott's, Snapple, Keurig, Green Mountain, etc. Also, the company has numerous partner brands because of its distribution network and market leadership for single-serve coffee K-Cup pods. These include Dunkin' Seattle's Best, Tim Horton's, Peet's, Caribou, Maxwell House, etc.

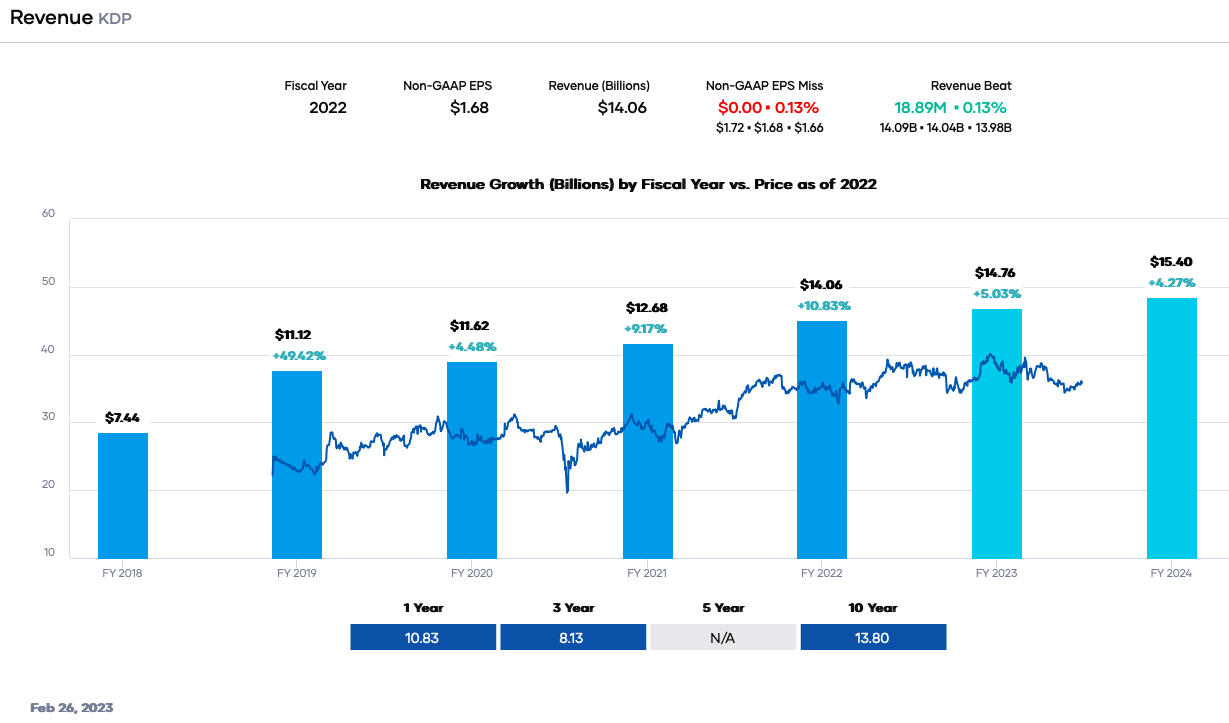

Total revenue was $14.06 billion in the fiscal year 2022.

{kind=link}

Revenue and Earnings Growth

Keurig Dr Pepper is successfully growing revenue and earnings per share driven by three competitive advantages: strong and growing brands, a primary distribution network, and market leadership in single-serve coffee systems and K-Cup Pods.

Since the merger, revenue has risen from a little over $11 billion in 2019 to over $14 billion in 2022. This period includes the tough pandemic stretch of 2020 to 2021. While other beverage companies struggled, Keurig Dr Pepper grew revenue because of its market leadership in single-serve coffees. Also, it was less dependent on sales in restaurants, sports venues, theaters, etc., than some competitors. Hence, revenue has grown at an 8.13% CAGR in the past three years.

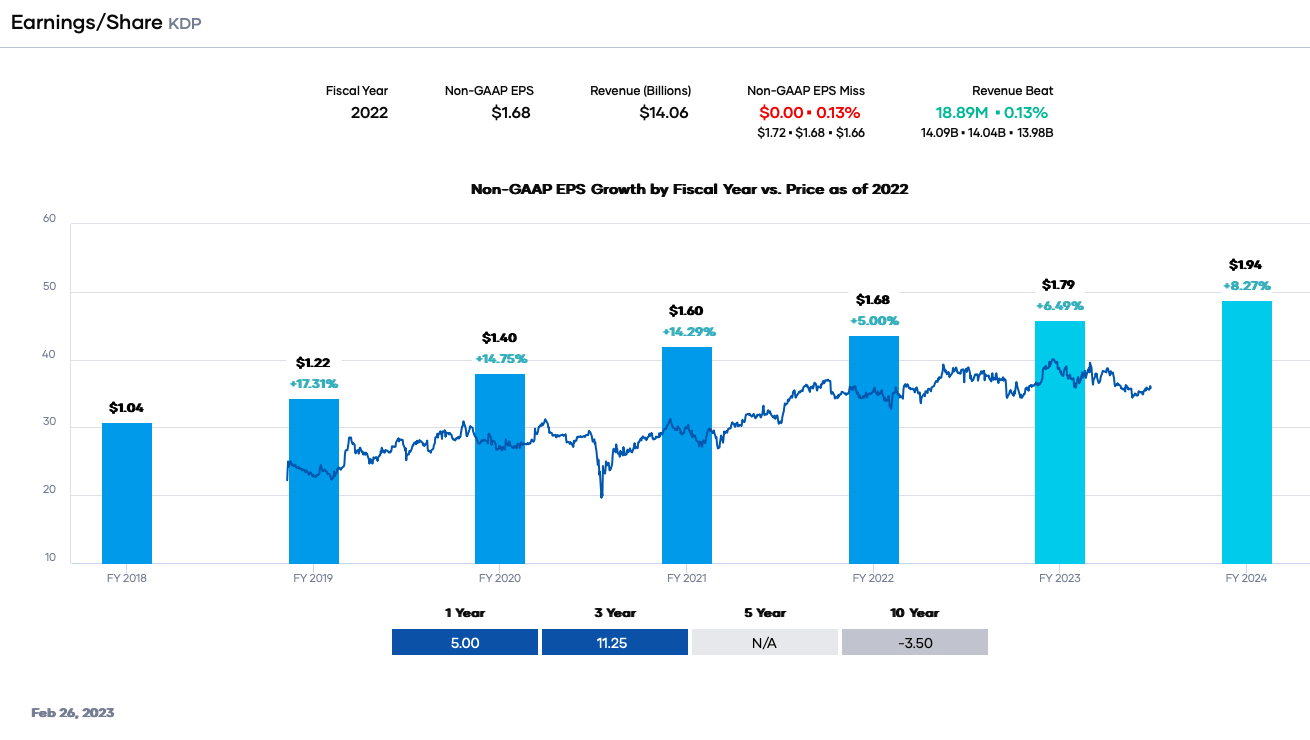

Earnings per share are also growing at a decent clip, from $1.22 in 2019 to $1.68 in 2022. The 3-year growth rate is 11.25% CAGR. Earnings are projected to grow in fiscal years 2023 and 2024.

{kind=link}

Revenue growth may slow in the next two years because of high inflation. Strapped consumers are undoubtedly cutting back. That said, the company should generate more growth as its Keurig coffee makers gain market share, and it sells more non-alcoholic beverages through its network. New strategic partnerships with Nutrabolt, Athletic Brewing Company, and Red Bull in Mexico will help drive the top and bottom lines.

Next, the Keurig single-serve brewing system is increasing penetration into American homes. According to the latest earnings release, the number has risen from 28 million households in 2018 to 38 million at the end of 2022. Families continue to buy brewing systems because they are simple to use. By selling more brewing systems, the firm adds incremental revenue, but more importantly, it facilitates the sale of higher quantities of coffee K-Cup Pods creating repeat revenue. Keurig Dr Pepper sells its own pods but also from its long list of strategic partners. Furthermore, consumers that buy pods are more likely to purchase new models of brewing systems in the future.

Keurig Dr Pepper's Risks

The main risk for Keurig Dr Pepper is competition. The firm competes against Pepsi and Coca-Cola, both significantly larger companies. Based on revenue, Coca-Cola is about three times larger, while Pepsi is about six times larger. Note that Pepsi also sells salty snacks. Based on market capitalization, both larger competitors are nearly five times larger. Coca-Cola and Pepsi compete directly with Keurig Dr Pepper in essentially every market segment, like carbonated soft drinks, energy drinks, water, teas, etc. Pepsi is not a significant player in coffee, but Coca-Cola acquired Costa Coffee in 2019. It is expanding distribution and innovating. Coca-Cola has the ability and financial resources to compete effectively.

The second risk to Keurig Dr Pepper is exposure to large retailers like Walmart ( WMT ), Target ( TGT ), and Costco ( COST ). Losing one or more distribution channels will negatively affect volumes and sales.

Dividend Analysis

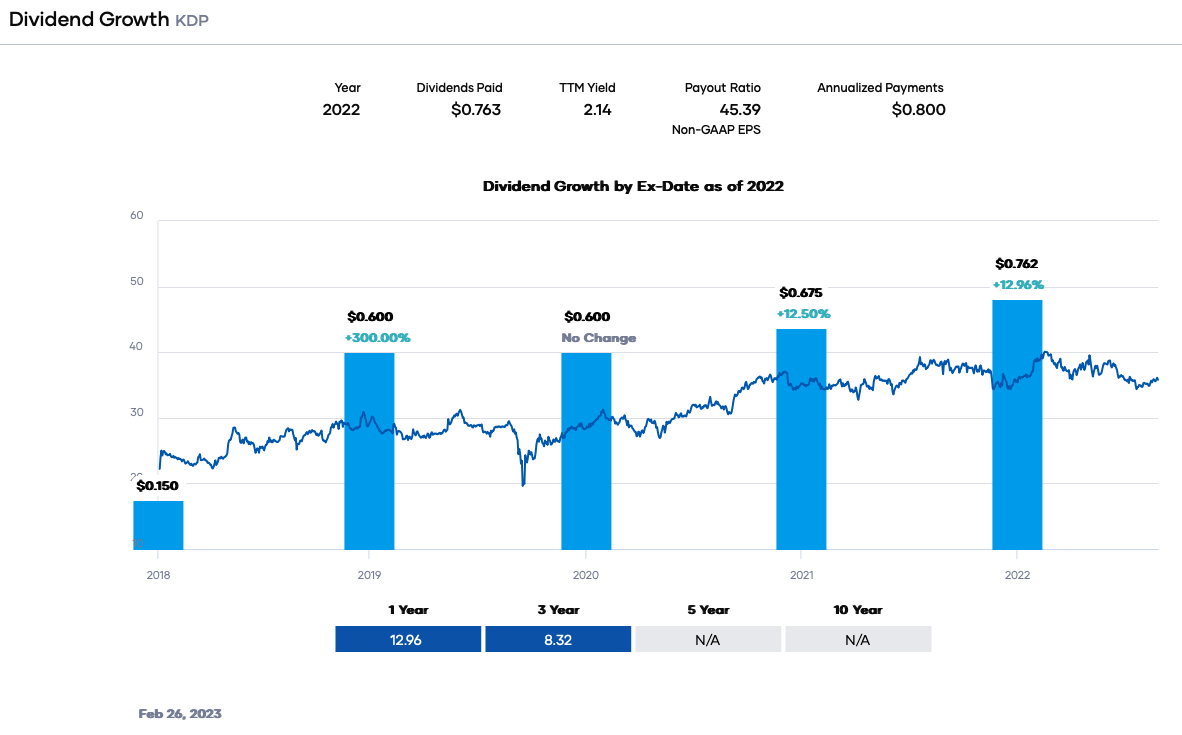

Keurig Dr Pepper has a dividend yield of 2.24%, based on a forward dividend rate of $0.80 per share. The yield is more than the usual average yield since the merger. Also, the dividend yield is more than the average of the S&P 500 Index at 1.69%.

The company has increased its annual dividend for three consecutive years. The growth rate is approximately 8.32% CAGR. The last quarterly dividend increase was $0.80 per share from $0.75 in Q3 2022. Further, the moderate earnings payout ratio provides room for future growth, especially when combined with the growing revenue and earnings per share.

{kind=link}

Keurig Dr Pepper has solid dividend safety based on earnings per share, free cash flow ((FCF)), and the balance sheet.

Consensus estimates for the fiscal year 2023 are $1.79 per share, and the annual dividend rate is $0.80 per share. These values result in a forward payout ratio of roughly 45%. Our payout ratio threshold is 65%, indicating the dividend is safe with room to spare.

Keurig Dr Pepper generated about $2,837 million in FCF in the fiscal year 2022 and in the last twelve months. The dividend needed around $1,080 million, resulting in a dividend-to-FCF ratio of ~38%. This value is excellent and below our limit of 70%.

The company has $535 million in total cash and short-term investments versus $399 million in short-term debt, $554 million in current long-term debt, and $11,266 in long-term debt. Interest coverage is approximately 4.3X, and the leverage ratio is nearly 3.5X. But Keurig Dr Pepper has been reducing total debt and leverage since the peak immediately after the merger.

The company has a BBB/Baa2 lower-medium investment grade credit rating from S&P Global and Moody's. However, debt is not concerning for dividend safety because the firm should lower debt further based on its solid FCF.

Valuation

Keurig Dr Pepper's stock price is slightly up YTD at +0.68% but is pressured because it reported mixed results for the latest quarter. The 1-year return is down somewhat at (-2.35%). The stock is trading at a P/E ratio of 20X, below its range in the trailing three years.

The consensus analyst earnings estimates are now $1.79 per share for 2023. We will use 21X as a value for the earnings multiple accounting for its strengths and offset by competition and leverage. Notably, this value is lower than that of Coca-Cola and Pepsi. Hence, our fair value estimate is $37.76. The current stock price is ~$35.79, suggesting that Keurig Dr Pepper is undervalued based on consensus fiscal 2023 earnings.

Applying a sensitivity calculation using PE ratios between 20X and 22X, we obtain a fair value range from $35.80 to $39.38. Hence, the stock price is approximately 91% to 99% of the fair value estimate.

Estimated Current Valuation Based On P/E Ratio

| P/E Ratio |

| 20 |

| 21 |

| 22 |

| Estimated Value |

| $35.80 |

| $37.59 |

| $39.38 |

| % of Estimated Value at Current Stock Price |

| 99% |

| 95% |

| 91% |

Source: dividendpower.org Calculations

How does this calculation compare to other valuation models? An EV/EBITDA, multiple analysis from FinBox, gives a fair value estimate of $39.67 per share. The model assumes a forward multiple of 15.2X. Portfolio Insight's blended fair value model combining the P/E ratio and dividend yield gives a fair value of $40.94 per share. Finally, the Gordon Growth Model gives $40, assuming a 6% dividend growth rate and an 8% desired rate of return.

The four-model average is ~$39.55, indicating Keurig Dr Pepper is undervalued at the current price.

Final Thoughts

Keurig Dr Pepper is the third major non-alcoholic beverage company in the United States. It probably has a long-term growth trajectory because of its leadership in single-serve coffee brewing systems and K-Cup Pods. Moreover, the firm has well-known brands and created its own distribution network. The dividend should probably grow further, and the stock is undervalued now. We view Keurig Dr Pepper as a long-term buy.

For further details see:

Keurig Dr Pepper: Buy For Dividend Growth And Safety