SBUX - Keurig Dr Pepper: Nice Dividend Defensive Downturn Play

2023-07-10 07:50:19 ET

Summary

- Coffee and other consumer defensive staples will be in demand both in the shopping cart and the stock market should we run into an economic road bump.

- Down 20% from its 1-year level highs is a pretty nice pullback versus the broader market.

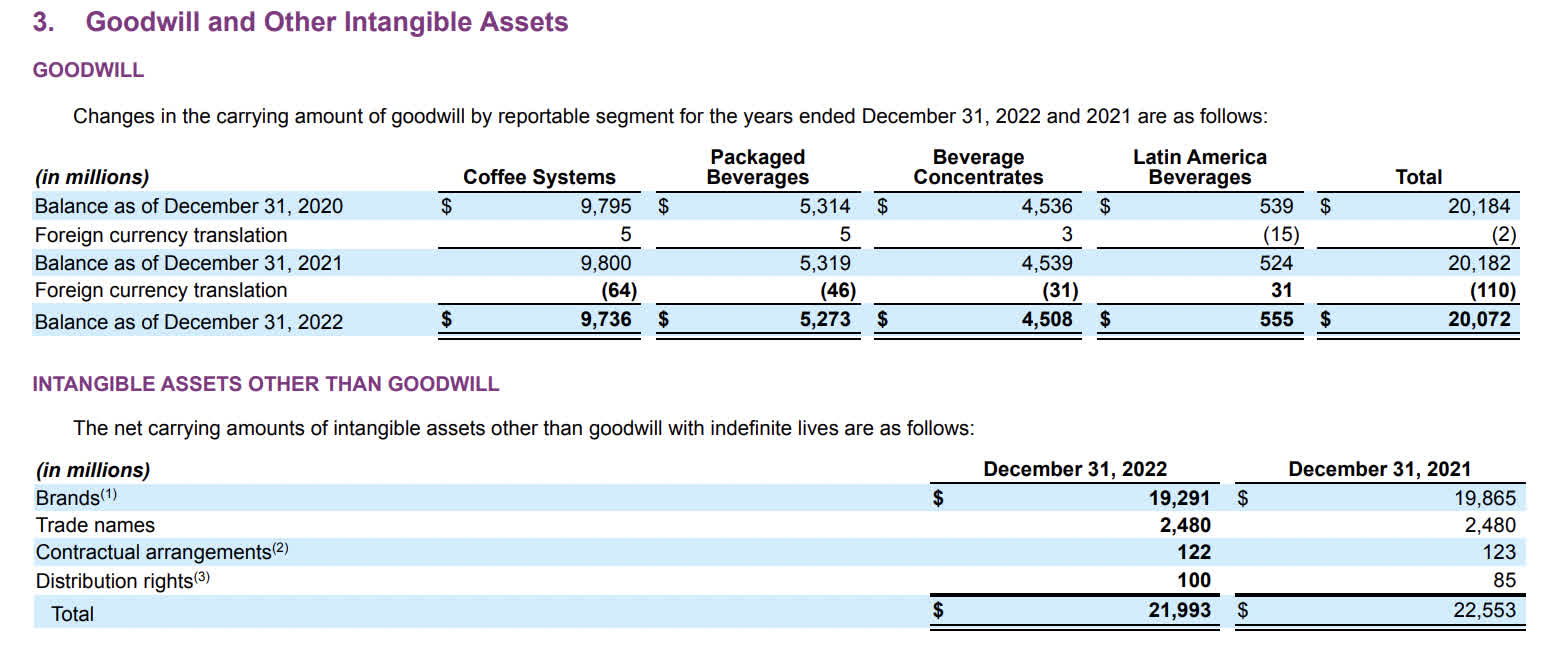

- Keurig Dr Pepper carries a lot of intangible assets and goodwill on its balance sheets post-merger of Keurig and Dr. Pepper. This results in write-offs that hurt GAAP performance.

- Non-GAAP is certainly the way to look at KDP.

- Furthermore, the investment into the energy drink market should pay off nicely.

Headline

In my previous article hunting for ideas that may be defensive plays in case a recession pops up, The J. M. Smucker Company ( SJM ), piqued my interest. It owns Folgers, the antithesis product of Starbucks Corporation's ( SBUX ) expensive beans and lattes. Some valued commenters also brought up Keurig Dr Pepper ( KDP ). The makers of the Keurig coffee pod beverage dispensers and pods are now ubiquitous in every hotel room and many an American household.

Coffee and other consumer defensive staples will be in demand both in the shopping cart and the stock market should we run into an economic road bump with the looming student debt repayments on the horizon. Combine this with Bank of America's ( BAC ) CEO Brian Moynihan predicting it will take at least until 2025 to get inflation back in line with FED expectations and we have some catalysts for consumer budget cutting. Let's take a look to see if the stock is fairly or overvalued.

The chart

Down 20% from its 1 year level highs is a pretty nice pull back. It's still down more than double the broader market ETFs like the SPDR S&P 500 ETF Trust ( SPY ) or the Vanguard S&P 500 ETF ( VOO ).

What they do

From the most recent financial year 10-K :

Keurig Dr Pepper Inc. is a leading beverage company in North America, with a diverse portfolio of flavored CSDs, NCBs, including water (enhanced and flavored), RTD tea and coffee, juice, juice drinks, mixers and specialty coffee, and is a leading producer of innovative single serve brewing systems. With a wide range of hot and cold beverages that meet virtually any consumer need, KDP key brands include Keurig, Dr Pepper, Canada Dry, Snapple, Mott's, Clamato, Core, Green Mountain Coffee Roasters and The Original Donut Shop.

KDP has some of the most recognized beverage brands in North America, with significant consumer awareness levels and long histories that evoke strong emotional connections with consumers. KDP offers more than 125 owned, licensed and partner brands, including the top ten best-selling coffee brands and Dr Pepper as a leading flavored CSD in the U.S. according to IRi, available nearly everywhere people shop and consume beverages.

KDP most recent proxy statement

{kind=link}

Valuation model

This is a very stable company that exhibits an established brand name and a minor moat if you will. They have ongoing capital expenditures that are less than depreciation and amortization. Why is this desirable? It means they can lay out less capital in forward years than past and continue to sustain their business. If they can also grow earnings through inflationary incremental revenue increases and or stock buybacks, then you have a winner.

These are the types of companies, as laid out in Robert Hagstrom's The Warren Buffett Way , that are both excellent alternatives to risk-free fixed income [since there is growth in earnings yield and usually dividend payments] and are desirable for mergers and acquisitions. Let's take a look at the "owner earnings model" for Keurig Dr Pepper as laid out in the book.

All numbers in millions courtesy of Seeking Alpha

- TTM Net Income: 1,318

- Plus TTM Depreciation and Amortization: 713

- Minus CAPEX: (306)

- Equals Owner Earnings: 1,725

- Discounted at risk free rate of 4.07% [10 YR Treasury]= Fair market cap of 42,383

- Divided by shares outstanding [1403] = $30.2

The stock seems to be trading right at or slightly higher than fair.

Sector grades

SeekingAlpha

Here we see a large divergence between GAAP and Non-GAAP. The company carries a lot of intangible assets and goodwill on its balance sheets post-merger of Keurig and Dr. Pepper. This results in write-offs that hurt GAAP performance. Non-GAAP is certainly the way to look at this company.

{kind=link}

Let's take a look at the breakdown of total assets:

Seeking Alpha

With total assets about double equity capital, there's a lot of write offs for years to come. This is a typical non-GAAP EBITDA cash flow story.

ROIC

Here we will look at the management in a couple of different ways. Return on Equity ROE and Return on Invested Capital, ROIC. In the case of fairly stable companies that don't have to invest a lot in CAPEX, ROE can sometimes be more relevant in looking at taking a company private, as debt can be restructured or paid off.

All numbers in Millions courtesy of Seeking Alpha

Return on Equity :

- TTM Net Income= 1,318

- TTM Total Equity= 25,102

- 1,318/25,102 = 5.2%

Return on equity is rather paltry at 5.2%. Let's see where we get when debt is added to the equation and use earnings before interest. Taxes are factored out and are assumed to be 14.2%.

Nopat (net operating income after taxes)/total LT + ST borrowings + total equity

- Nopat=EBIT X (1- tax rate)= 2861 X (1-14.2%)= 2454

- TTM total equity= 25,102

- TTM Long term debt + short term borrowings = 9,929 LT + 1,178 ST = 11,107

- NOPAT/ Invested Capital= 2454/36,209= 6.7%

Interesting, Keurig Dr Pepper is doing a decent job employing debt. If we recalculate just the return on equity model to simply look at the yield on this adjusted cash flow metric of $2.454 Billion versus the TTM net income, the Equity return on adjusted EBIT is 9.7%. An acceptable return.

Margins

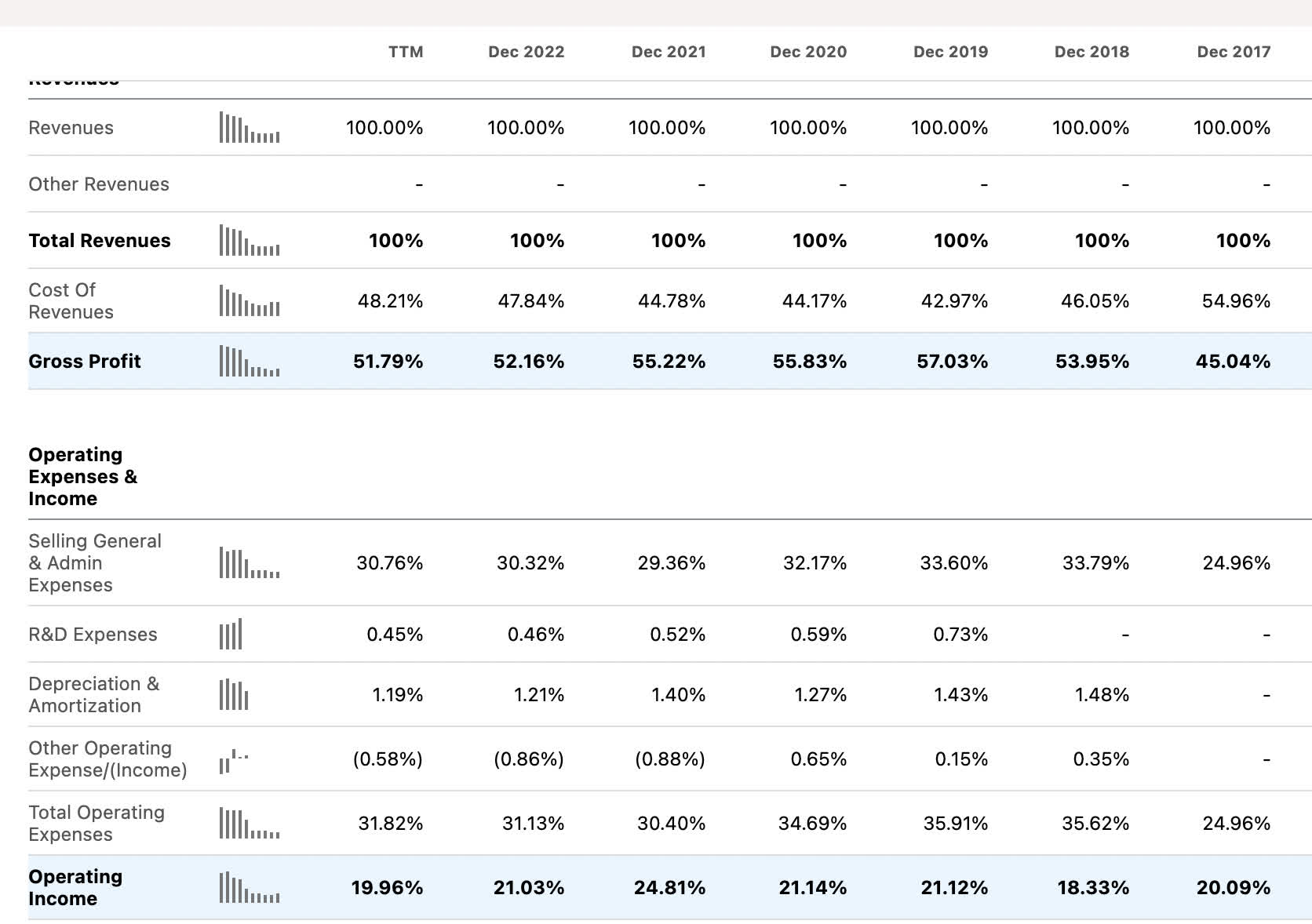

{kind=link}

Gross margins look great, operating margins are not bad either. With the net income margins around 9.2%, the margins get cut in half at each step down the income statement from gross to operating to net.

With current interest expense of $528 million and total interest-bearing capital as noted above at $11,107 Billion, this is an average cost of debt of 4.75%. That's pretty decent. They have also recently been upgraded by Moody's :

New York, April 03, 2023 -- Moody's Investors Service ("Moody's") today upgraded Keurig Dr Pepper Inc.'s ("KDP") senior unsecured ratings to Baa1 from Baa2 and affirmed the company's Prime-2 commercial paper rating. The rating outlook remains stable. The upgrades reflect KDP's continued strong operating performance and consistent improvement in financial leverage following the merger of Keurig and Dr Pepper Snapple Group in 2018. Moody's expects the company to continue to perform well over the next 12-18 months and focus on reducing financial leverage further.

The rating change also recognizes management's new and more conservative financial policy with a commitment to further reduce leverage to a range of 2.0x-2.5x net debt to EBITDA (company calculated, 2.8x as of December 31, 2022) through both debt repayment and EBITDA growth.

As noted above, Keurig Dr Pepper is making efforts to reduce leverage. Let's take a look at the balance sheet trends.

Balance sheet trends

2018 was the date that Keurig acquired Dr. Pepper and the debt trends are reflected in the total long-term debt. The company is doing a great job of reducing debt, let's take a look at the progress on a 5-year slice:

Paying down debt from around $15.5 Billion to $11.97 in 5 years is impressive. To me, the debt pay-down aspect is even more attractive than the other elements surrounding Keurig Dr Pepper's story.

The buyback element has also just begun post-merger, with the reduction in shares strategy looking to be more consistent going forward. Reducing both debt and equity should improve all the management metrics for ROE and ROIC as the denominators are quickly decreasing.

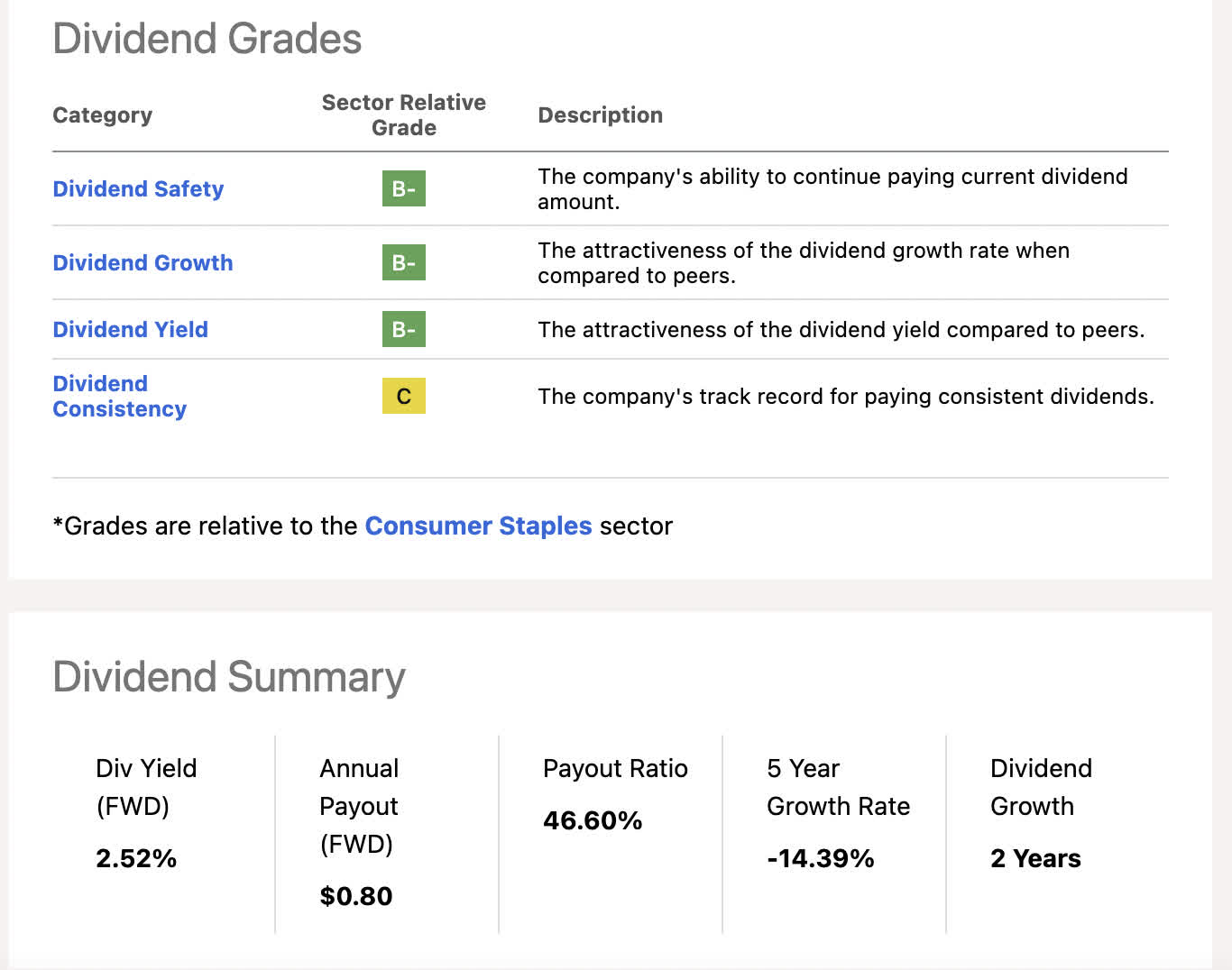

The dividend and free cash flow

{kind=link}

Good coverage. Not the growth rates we're looking for over the 5 years, but again, this time increment contains a merger. With 2 years of growth and recent stability elements between CAPEX and D&A, this dividend looks set to provide consistent payment and growth going forward. The one-year growth rate is near 6% .

Free cash flow coverage

- TTM Free cash flow per share of $1.32

- Forward payout of $0.80 per share

- Free cash flow payout ratio of 60.6%

Catalysts

{kind=link}

Income sources are nicely distributed amongst coffee systems at 51%, packaged beverages at 31% and beverage concentrates at 37%. This is one of the better income distribution mixes you will see from a company regarding even distribution. The coffee makers/systems are still the most prevalent part of the equation and one I would consider a growth catalyst harkening back to the J.M. Smucker thesis .

Coffee is a necessary staple for many of those that may have their budget impacted by student debt repayment. Cheaper, more sustainable coffee solutions may be on the docket.

KDP most recent proxy statement

{kind=link}

Getting the brewing systems into the households begets coffee pod sales. Similar to a smartphone that corners you into its app store. When I first encountered the Keurig pod machines I thought this would never work. I was wrong. This is becoming the quickest solution to grabbing a quality, fast cup of coffee before heading out the door.

Furthermore, the investment into the energy drink market should pay off nicely to boot:

Keurig Dr Pepper (KDP) has invested US$863m for a 30% stake in US energy-drink and recovery-beverage maker Nutrabolt.

The "strategic partnership" also includes a long-term sales and distribution agreement for Nutrabolt's energy drink brand C4, KDP said in a statement today.

From next year, C4 will be sold in the "vast majority of KDP's company-owned direct store distribution territories".

Risks

Rates are continuing to rise and Keurig Dr Pepper is quickly trying to pay down debt to lower their WACC and general debt load. The coffee systems are not cheap, but the investment would result in a lower cost per cup over time versus a to-go coffee experience. I could be overestimating the U.S. consumers' logic ability and the initial investment in a coffee system could be looked at as discretionary. The catalyst could wind up being the risk.

Conclusion

The stock is close enough to fair value to consider it a fair buy. We would normally want to be buying about 15% below intrinsic value, but the debt and equity reduction elements are clearly outlined both in the statistical evidence and Moody's guidance/upgrade. The risk-free long rate has risen quite a bit since I first looked at the company. The market seems to be pricing in longer inflation than originally thought. The nicely covered 2.52% dividend is a plus that I would expect to continue growing. Reiterate fair buy for the defensive investor expecting a recession.

For further details see:

Keurig Dr Pepper: Nice Dividend Defensive Downturn Play