KDP - Keurig Dr Pepper: Strong U.S. Beverage Performance Outweighs The Coffee Decline

2023-11-15 22:24:06 ET

Summary

- Keurig Dr Pepper reports strong growth in beverage segments, driven by price increases and strong demand.

- The US coffee segment declined, but the decline has improved compared to previous periods.

- KDP's expansion into higher-growth product categories and partnerships with brands should drive long-term growth.

Overview

Note that I previously rated a hold rating for Keurig Dr Pepper ( KDP ), as I am expecting to see recovery in the coffee segment given the challenging macro conditions. In this post, I am revising it to a buy rating. Although the US coffee segment declined in 3Q23, the decline has improved when compared with previous period 5.7% decline. Apart from coffee segments, beverage segments saw strong growth, driven mostly by price increases. This shows that KDP's beverage demand is strong, which gives it strong pricing power. When compared to peers, KDP also outperformed them, and this further bolsters my belief in KDP.

Recent results & updates

For 3Q23 , KDP reported net sales of $3.81 billion or a year-on-year growth of 5.1%. The growth was driven by positive net price realization, which was offset by lower volume. Moving down the P&L, adjusted operating income grew by 3.1% to 25.9% of sales. Adjusted net income grew 1.8% to 17.6%.

KDP reports its performance in three segments. US beverages, US coffee, and international. In general, US beverages and the international segment both grew while coffee declined. For US beverages, sales increased by 5.9% year-on-year. It has a strong net price realization of 7.1% and a low volume decline of 1.2%. This performance is stronger than the US coffee segment, where it reported a net price realization of 3.1% but a volume decline of 6.3%. Looking at these figures, I would infer that the US market is more price-inelastic towards beverages than coffee. When I look at the revenue weightage, US beverages account for 59% of KDP's total sales. This is a good sign, as more than 50% of its sales are linked to the more price inelastic beverage product. I believe that its beverage segment will be its key growth driver moving forward.

On the other hand, the coffee segment accounts for about 26% of KDP's net sales, and net sales declined by 3.2% year-on-year. The coffee market is recovering at a slow rate due to the high cost of coffee, and recovery in the next quarter is unlikely as coffee prices have started to increase recently. Based on coffee cost slow recovery pace, I anticipate coffee growth to become positive only in 2025. There has been recent growth in the single-serve market. New buyers of coffee pods keep increasing their spending over time. Meanwhile, whole bean and ground coffee growth has been declining. Thus, I believe the driver for coffee recovery will be coffee pods rather than whole or ground coffees.

In order to ensure long-term growth, KDP has expanded its presence in higher-growth product categories through its portfolio of partnerships with brands like Nutrabolt, La Colombe , Vita Coco, and Electrolit. Energy, sports, and ready-to-drink [RTD] coffee are expected to outpace the company's core portfolio annually in growth over the next few years due to its strong growth in recent years. The dollar sales of energy drinks have grown from $4.5 billion in 2021 to $6.3 billion in 2023. As these brands take advantage of KDP's scale and distribution channels, these investments significantly increase KDP's addressable market and generate incremental sales, as many of the brands still have room to expand their retail presence and are expected to leverage the partnership aggressively. As more partnerships are formed and the brands grow in popularity, I anticipate a larger contribution to KDP's top line in the future. Given the current coffee headwinds, I believe that KDP's recent efforts to diversify beyond coffee will drive its long-term growth.

Valuation and risk

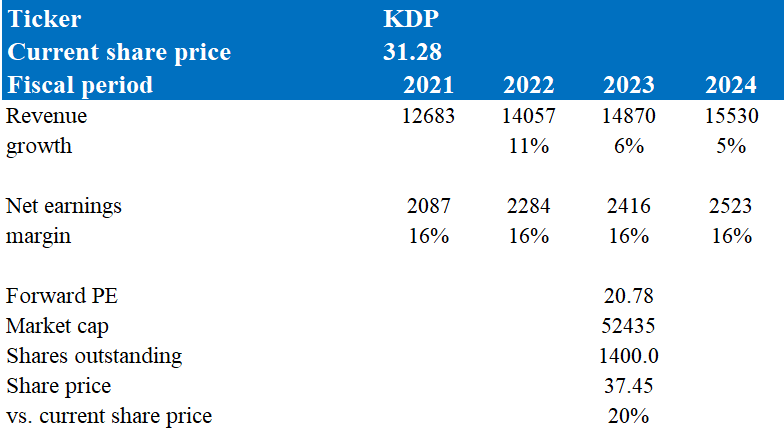

According to my model, KDP is valued at $37.45 in FY24, representing a 20% increase. This target price is based on my growth forecast of mid-single digits for 2023 and 2024. These growth rates are in line with market consensus as well as management's guidance. In the 3Q23 results, KDP guided net sales growth to 5-6% for the full year. These forecasts are reasonable given KDP's robust 3Q23 performance in its international and US beverage segments. Although US coffee did decline, its decline is lower than the growth of the US beverage and international segments. In addition, US coffee revenue only accounted for 26% vs. US beverage revenue of 59%. Thus, its negative impact on KDP on an overall basis is downsized given its lower weightage. Therefore, on the company level, net sales still grow despite coffee's decline.

{kind=link}

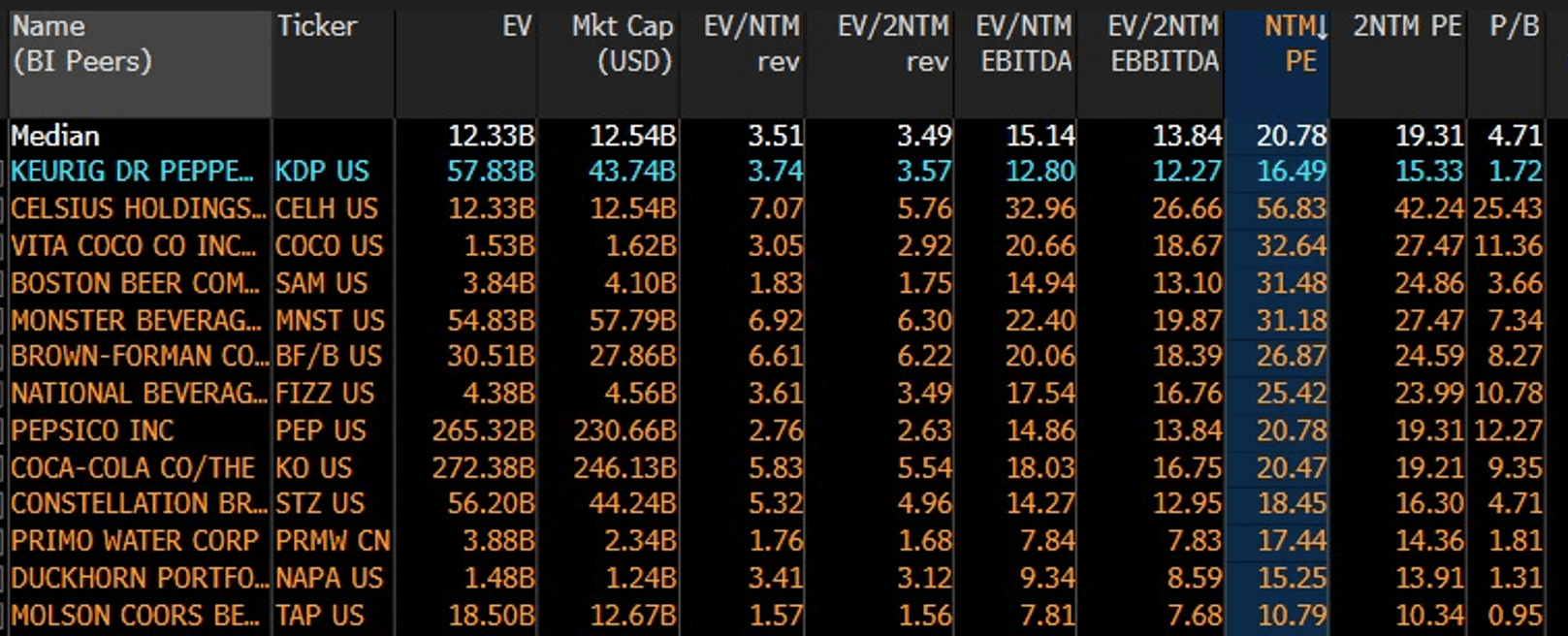

As of now, KDP's forward price/earnings stands at 16.49x, lower than peers' 20.78x. Given the fact that KDP has better margins and a similar 1-year growth outlook, I believe KDP should be trading at its peers' level. KDP's gross margin is 53% vs. peers' 50%, its EBITDA margin is 26% vs. peers' 19%, and its net margin is 13% vs. peers' 12%. In terms of 1-year growth, KDP is at 6%, while peers are at 6% as well. Thus, there is no reason why its current P/E is trading lower. With a potential gain of 20% and the strength of KDP discussed above, I am revising my rating to a buy.

{kind=link}

Runaway inflation might pose a risk to the KDP's revenue model. Although I have discussed that US beverages are relatively price inelastic, there is a limit to how much price KDP can increase before the volume decline outpaces the net price realization. If inflation starts increasing again and at unsustainable rates, KDP will be forced to raise prices due to the increasing cost. In addition, its price-elastic US coffee segment will be hit even harder. In those scenarios, KDP's revenue and margins will both be under immense pressure.

Summary

In summary, I believe KDP is a strong stock. In terms of beverage demand, it is very strong, as they are able to raise prices without much repercussion on volume, and this is a testament to beverage's pricing power. However, do take note that its coffee segment is not that robust as it is sensitive to price hikes. Based on the trend of coffee prices, recovery in the next quarter is unlikely. In order to combat the weakness in coffee segment, KDP has expanded into the higher-growth categories. It is trying to diversify beyond the weak coffee segment, and I expect this move to drive KDP's long-term growth. When compared to peers, KDP also outperformed them in terms of margins. On these notes, I am revising my rating to a buy for KDP.

For further details see:

Keurig Dr Pepper: Strong U.S. Beverage Performance Outweighs The Coffee Decline