KDP - Keurig Dr Pepper: The Recent Share Price Drop Might Not Last For Long

2023-04-08 04:23:05 ET

Summary

- Keurig Dr Pepper share price has been under pressure over the recent months due to higher than expected drop in profitability.

- Beverage segments, however, continue to perform well and would most likely offset weaknesses in coffee.

- Investors, however, should not expect a quick rebound in the company's free cash flow.

With the likelihood of a recession in 2023 increasing sharply in recent months, more investors are rightfully so looking to increase their exposure to low-risk areas of the market, such as consumer staples.

On the other hand, however, investors should also be careful of short-term speculation within the sector as passive investing vehicles have attracted enormous amount of capital over the past decade. Therefore, a rapid sector rotation could cause some of the most popular names to deviate significantly from their fair value.

Keurig Dr Pepper Inc. (KDP), however, is among the high quality consumer staple businesses that at the same is not exposed to passive income flows to the same extent that companies like Coca-Cola (KO) and PepsiCo (PEP) are.

Since I first covered the business in 2021, KDP has been performing at par with the S&P 500 and the consumer staples sector as measured by the Consumer Staples Select Sector SPDR® Fund ETF (XLP).

Over the past few months, however, KDP has been significantly underperforming the market as its largest peers in the soft drinks space are once again trading near all-time highs.

Although higher volumes in consumer staples ETFs could largely explain this dynamic, KDP's results for 2022 also played a major role in the company's recent disappointing performance.

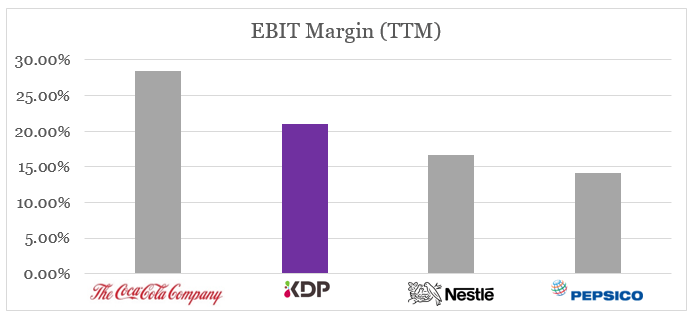

Retaining Industry-Leading Profitability

Even though KDP is much smaller than Coca-Cola (KO), PepsiCo (PEP) and Nestle (NSRGY), its strong brand portfolio and highly efficient operations in North America allow the company to retain industry-leading margins even when compared to the top-tier competitors.

{kind=link}

When properly accounting for intangible assets, this profitability also results in exceptionally high returns on capital.

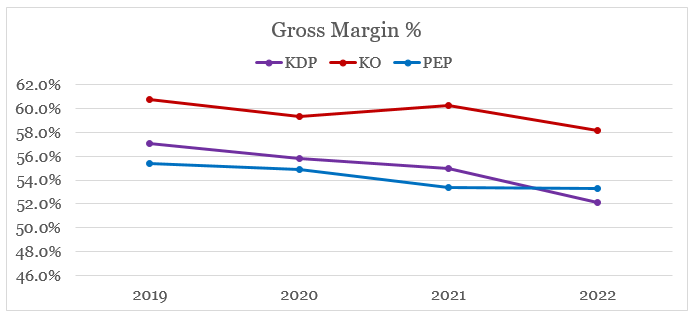

Nevertheless, the recent surge in raw material costs has put enormous pressure on gross margins and in 2022 KDP noted a far larger decrease than its peers in the non-alcoholic drinks space.

{kind=link}

The management blamed timing in price increases and lagging productivity as the main factors behind this large drop gross margins.

Adjusted gross profit grew almost 8% and gross margin contracted 170 basis points, due to the timing of pricing and productivity lagging double-digit inflation.

Source: KDP Q4 2022 Earnings Transcript

During the latest conference call, the management has also made clear that they now expect a substantial improvement in gross margins during 2023 as they plan to step-up brand investment activities.

(...) we expect a substantial improvement in our gross margin , but it will not go back to 2019 level . But we said before, we would like to invest in marketing. So we will be reinvesting in marketing. So you will not see the flow through from gross margin to OI all the way.

Source: KDP Q4 2022 Earnings Transcript

Even though margins are expected to remain below 57% (the 2019 level), the 2022 level of 52% leaves plenty of room for improvement.

Given that inflation remains elevated, this would suggest that KDP will step-up its pricing efforts. So far, the coffee segment has been lagging the most when it comes to offsetting the cost of raw materials through price increases.

This has not been a problem unique to KDP, with Nestle's Nespresso segment noting a decline in underlying operating profit to CHF 1,388m in 2022 from CHF 1,475m a year earlier, while sales remained flat.

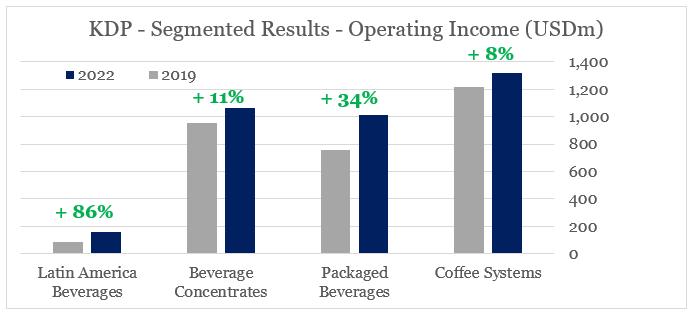

Growth of Keurig system also appears to be slowing down due to the challenging retail environment from the impressive 8 million new households being added in 2018-21 period.

Having said that, the pressure for Coffee Systems to deliver will be enormous as the segment saw a mere 8% growth in operating income since 2019.

{kind=link}

Luckily, the rest of KDP portfolio continues to perform exceptionally well, which would allow the company to temporarily subsidize the coffee segment, if needed. The highest margin segment - Beverage Concentrates, which has operating margins of 60% and above, noted an impressive growth in 2022 on the back of high price increases and positive volume mix.

Beverage Concentrate had an exceptional year in 2022. Net sales grew 16.4% with net pricing up 14.7% and volume mix up 1.7% . Dr Pepper brand drove the performance largely reflecting the expansion of Dr Pepper Zero Sugar and a strong in-market support.

(...) Beverage Concentrates adjusted operating income grew 16.9% .

Source: KDP Q4 2022 Earnings Transcript

The recent developments in Packaged Beverages were not very different with the segment expected to be among the major drivers of KDP's margin expansion in 2023.

Packaged Beverages operating income is expected to be strong in 2023 with margin expanding, due to a better relationship between pricing and inflation and we expect the segment's underlying performance to be even stronger, driven by gross margin expansion , partially offset by marketing investments .

Source: KDP Q4 2022 Earnings Transcript

Overall, KDP is in a good position to offset weaknesses in coffee through its high quality beverages portfolio. Therefore it is likely that KDP would be able to close down the performance gap with the rest of the XLP over the next year.

Free Cash Flow Considerations

In addition to profitability issues, however, KDP's recent results shed some light to some other areas that investors should be mindful of.

Firstly, the company noted a large increase in its inventory levels, from $894m in 2021 to $1,314m during 2022. This has resulted a large drop in Days Inventory Outstanding ((DIO)), which was not offset by the company slightly higher Days of payables outstanding.

{kind=link}

Within the company's annual report, the management has indicated the need to meet customer service levels as the reason for the increase. To say the least this sounds too generic and ambiguous.

(...) the increase in DIO reflects our efforts to restore inventory to meet customer service levels.

Source: KDP 10-K SEC Filing

When looking at the inventory breakdown, the increase is largely within the finished goods category.

{kind=link}

Given the fact that finished goods includes the purchases of brewing systems from third-party manufacturers (see below), it appears likely that either KDP has ended up with higher brewing systems inventory due to the recent slowdown or that there is significant increase in the prices of these appliances.

{kind=link}

If it is the latter, KDP would likely struggle to improve its gross margins within the coffee segment due to this significant increase in the cost of brewers.

Moreover, in this scenario it would be reasonable to expect inventory increase to continue to be a headwind for KDP's free cash flow.

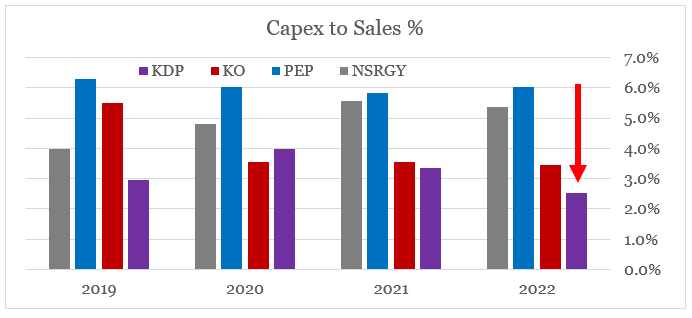

In addition, KDP has also significantly reduced the amount of capital expenditure in recent years as it has become a more asset-light business. However, in 2022 its capex numbers fell significantly and are now by far the lowest as a percentage of net sales within the peer group.

{kind=link}

With Capex likely to revert back to historical levels, working capital being a headwind and KDP management being committed to spend more on brand building activities, the company's free cash flow should come under pressure.

Conclusion

KDP does not appear to be benefiting from the recent sector rotation to the extent that Coca-Cola and PepsiCo do. The company's large drop in gross profitability is also contributing to the wide performance gap with the broader consumer staples sector.

Looking ahead, however, the company is well-positioned to offset weaknesses in the coffee segment as the strong brand portfolio allows for continued price increases. Having said that, investors should look carefully for any further inventory increases beyond the company's current sales growth. Higher capital expenditure is also to be expected in the coming years which would put more pressure on free cash flow.

For further details see:

Keurig Dr Pepper: The Recent Share Price Drop Might Not Last For Long