KDP - Keurig Dr Pepper: U.S. Coffee Segment Performance Is Upcoming Catalyst

2023-08-05 08:44:57 ET

Summary

- Keurig Dr Pepper's US Coffee segment continues to show weakness.

- Management is optimistic about a potential recovery in the US Coffee segment in the latter half of 2023.

- I expect uncertainties in the challenging economic conditions to hinder the US coffee segment recovery.

Overview

My recommendation for Keurig Dr Pepper (KDP) is to remain neutral, as I continue to be concerned about the recovery of the US Coffee segment. So far, management has indicated that the trend is turning around, but I think the valuation will not reflect this optimism until actual results are reported.

Note that I previously gave a hold rating to KDP as I wanted to see a recovery in the coffee segment and also a clearer demand trajectory given the uncertain demand environment back then.

Recent results & updates

KDP reported 2Q23 revenue of $3.79 billion, a growth of 6.6% vs consensus expected growth of 4%. KDP adjusted earnings per share of $0.42 were also higher than the consensus estimate of $0.40. The organic sales growth [OSG] for each market segment was as follows: the US Coffee (-5.7%), US Refreshing Beverages (11.8%), and International (7.0%). Within US Coffee, sales of K-Cup pods fell 4.6% and 7.7% in volume, while sales of brewers fell 11%. Although gross margins increased slightly to 54.8%, the rise in OPEX was enough to reduce the EBIT margin by 37bps. KDP's overall performance was better than expected, as both its revenue and EPS figures surpassed consensus. While the company's U.S. Refreshment Beverages division saw double-digit growth in sales and strong margin expansion, the company's U.S. Coffee division continued to show weakness.

Regarding the US Coffee business, there remains a noticeable weakness, although I found the positive outlook from the management reassuring, as they anticipated that the lowest point would be in the 2Q23. In my opinion, there's a likelihood that the U.S. Coffee business will experience a favorable tailwind in the near future due to the easing of mobility comparisons. This, in turn, will lead to a recovery in the consumption of coffee at home during the latter half of 2023. (The management also highlighted that the at-home coffee category exhibited positive progress in July.) However, I do have reservations about assuming rapid and accelerated growth throughout the remainder of the year. This is because I believe the challenging economic circumstances could cause consumers to postpone or delay making larger discretionary purchases, such as coffee makers. As a result, this factor will probably continue to exert pressure on the segment's performance until the second half of 2023.

In terms of margins, I anticipate the US Coffee segment's gross margin to grow further through 2H23, thanks largely to the lagging effect of recent price increases mismatching against a declining input cost. However, I think operating leverage will be moderated this year because KDP is still investing in the company to drive long-term growth.

In sum, I think KDP has promising long-term growth opportunities to expand its share of the brewer as a result of its consistent focus on innovation and expansion of its core packaged beverage business. However, my neutral rating remains unchanged because I believe the uncertainty in the company's top line will remain an overhang, especially in the coffee business due to the macro pressure (which offsets the tailwind from easing of mobility comps).

Valuation and risk

{kind=link}

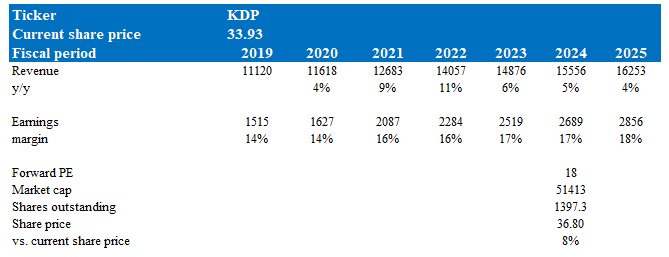

According to my model, KDP is valued $36.80 in FY24, representing an 8% increase, or, in other words, being fairly valued. This target price is based on my growth forecast of mid-single digits over the next two years, following management's FY23 revenue-guided growth rate. I also expect margins to improve after the near-term reinvestment.

I think the way for KDP stock to go up further will heavily depend on US Coffee performance, which is what investors are paying attention to, in my opinion. Until KDP reports results that suggest the trend has turned sustainably, I foresee valuation remaining at a discount to KDP's historical average of 19x. KDP is now trading at 18x forward revenue, which I expect to remain the same in the near term.

Valuation also faces the risk of KDP missing 4Q23 expectations as management stated that they anticipate only modest EPS growth in 3Q23, which raises concerns about how much can 4Q23 grow given the challenging and uncertain macro backdrop.

Summary

In conclusion, I remain neutral on KDP, given lingering concerns about the recovery of the US Coffee segment. While recent financial results exceeded expectations, the coffee division's weakness persists. Potential for a near-term tailwind in the US Coffee segment due to eased mobility comparisons could drive recovery in at-home coffee consumption later in 2023. However, uncertainties linked to challenging economic conditions may hinder rapid growth.

For further details see:

Keurig Dr Pepper: U.S. Coffee Segment Performance Is Upcoming Catalyst