STMEF - Key Considerations For Those Contemplating A Position In Navitas Semiconductor

2023-06-27 16:26:20 ET

Summary

- Navitas has been on fire this year (over 150% returns YTD); we highlight why this is one of the most exciting stories in the semi universe.

- Despite high forward valuation multiples, Navitas' expected revenue growth of 95% over the next three years comfortably outpaces competitors in the GaN and SiC markets.

- Investors should be cautious of potential risks, including the dilution effect, long sales cycles, and its elevated exposure to China.

- We appreciate ongoing institutional investor participation, but the risk-reward on the charts suggest a long position would not be too conducive at this juncture.

Introduction

This year, semiconductor stocks (as represented by the SPDR Semiconductor ETF ( XSD )) have done a solid enough job, delivering roughly 2x the returns of the benchmark index (~13%). Within this portfolio, the stock of Navitas Semiconductor ( NVTS ) has fared exceedingly well, registering triple-digit gains and delivering over 6x the returns of XSD. Is NVTS worth its salt? Read on to find out

YCharts

Why Navitas Semiconductor Should Be On Your Watchlist

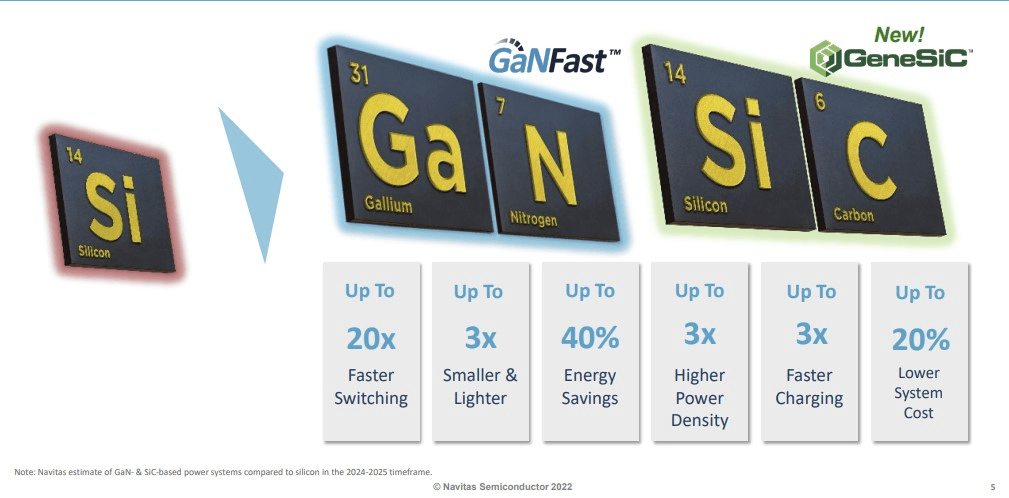

Navitas Semiconductor, a fabless semi-entity, was established in 2013 but began commercialization only in 2018. The company's core competence lies in the field of gallium nitride (GaN) power IC (integrated circuits) technology, which is typically adopted in mobile charging applications (in charging equipment for smartphones, laptops, home appliances, etc.).

Currently, the power supply of these electronic devices is mostly driven by silicon-based solutions (Si) which often lack ample power density, have sub-par power switching speeds, are slower to charge, and don’t generate ample energy savings (relative to the same output of power via GaN based systems).

{kind=link}

GaN-based solutions sought to address these challenges (the image above contextualizes the benefits that GaN-based tech could bring relative to Si-based offerings), but then again there were barriers to further adoption as most GaN transistor offerings in the market were “non-integrated” (the transistor did not have the support of a specialized silicon driver) and couldn’t provide the requisite protection.

NVTS then came along with the first GaN “integrated” IC offering which negated the deficiencies of the non-integrated alternatives, whilst also leading to higher energy savings and lower costs.

NVTS management now believes that whilst the total power semi-market will likely only grow at 6% CAGR through FY26, the GaN device market will likely grow at a whopping 117% CAGR during the same period!

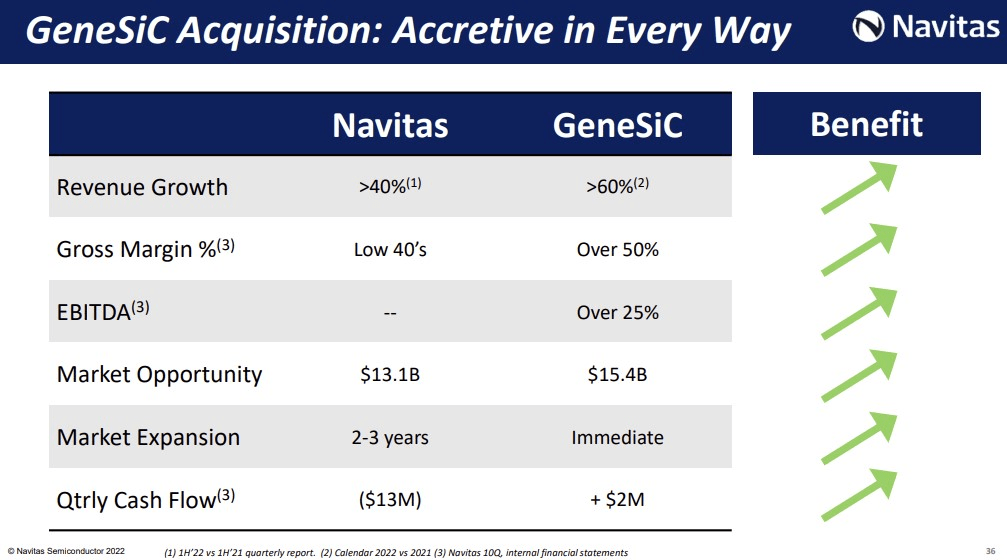

Besides GaN, NVTS is also attempting to build clout in the design of silicon carbide (SiC) power devices, and in that regard, acquired GeneSiC Semiconductor last year.

The acquisition of GeneSiC catapults NVTS to a different league, as it enables the company to offer its expertise in high-margin markets (such as EVs, solar, industrial, data center) that require high power applications and higher device voltages (up to 6500V).

Investor Presentation

As seen above, the GeneSiC acquisition will not only help NVTS become a more diversified business (see revenue profile below vs what it was in 2020) with exposure to a range of high-growth end-markets, but it will also help the company step up its margin profile as the former’s average gross margins are over 50%. NVTS now expects its overall margins to improve every quarter till the end of the year when it will likely cross the 45% mark. In the long-term the company wants to get group GMs to trend over 50%.

{kind=link}

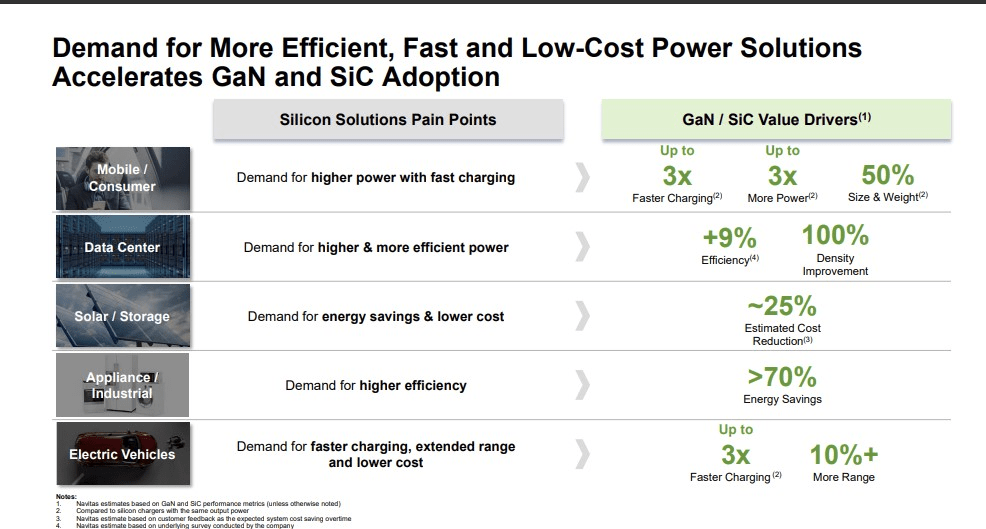

It's difficult to imagine why GaN and SiC tech won’t penetrate across various end markets listed below, given the superior degree of power, charging, and efficiency specs they offer

{kind=link}

According to Yole Group, in another 4-5 years, 30% of the legacy power silicon (Si) market will be displaced by GaN and SiC.

What Do The Forward Valuations Look Like?

Consensus estimates suggest that NVTS will likely only turn profitable by FY25, making the P/E metric redundant. However, if one considers the stock’s forward EV/sales metric (based on the FY24 revenue figure), some of you may get put off by it, as it is priced at a 15% premium to its historical average multiple of 7.8x.

YCharts

Crucially, if one were to draw up a comparative list, including some of NVTS’s noted publicly listed competitors, both from the GaN and SiC avenues, the valuation quotient would be even more glaring, with NVTS currently priced at a whopping 78% premium over the peer set EV/Sales average of 5x!

YCharts

However, before you turn away, let's also consider the degree of medium-term revenue growth one is getting at those lofty multiples. The image below shows you the sales growth potential of all these competing entities over the next three years, except for Transphorm ( TGAN ) whose forecasts only extend till FY24 (the CAGRs are a function of YCharts Sell-side estimates over the next three years).

YCharts

Well, on that front, Navitas Semi comfortably trounces the rest of the pack with expected revenue growth of 95% which is almost 4x the pace of average. If management can execute and convert a greater degree of the humungous revenue pipeline discussed previously, who’s to say NVTS can’t hit triple-digit growth percentage numbers?

Risks

NVTS, like a lot of young, high-growth companies is deep in the red (last year it reported positive net income largely on account of a favorable change in the fair value of warrants and earnout liabilities), and not quite in a position to generate ample internal funds to fuel its growth ambitions. NVTS’s cash balance which stood at nearly $270m at the end of FY21, has been dropping every quarter since, falling by -62% in aggregate ($100m)

YCharts

Meanwhile, even though Navitas Semi's revenue growth explosion has been very exciting to watch, it's also worth considering that total operating expenses as a function of those revenues have continued to trend up in recent years. This could be a result of a longer-than-expected sales cycle where NVTS' clients typically take time to not only test and evaluate the company’s products, but then also take additional time to commence production of their own products. The sales cycle only closes when that’s done.

Seeking Alpha

Thus, investors should brace themselves for ample dilution effects, as the company will keep tapping the markets to raise funds just as it did last month . The share count has been trending up over time (33% growth in the share count since the listing date), and after coming in at 156.8m shares outstanding in Q1, management now expects it to hit 162m by Q2.

YCharts

Then, no matter how appealing a stock's long-term cardinal story looks, one shouldn't dismiss the impact of geopolitical issues , and how this can always topple the buy case, particularly as it relates to China, where semiconductor -related tensions often rear their ugly head. FYI, NVTS’ most important foreign geographical region is China ( 38% of group sales).

Closing Thoughts - Other Stock-related Considerations

Stakeholders of NVTS may be enthused to note that the stock continues to garner increasing attention from the guys with deep pockets- the institutional cohort. Since late last year, till late May '23, the institutional investor club has increased their ownership in NVTS stock every other month.

YCharts

Their predilection towards NVTS is likely driven by favorable sell-side positioning where seven out of the eight analysts have either a ‘Buy’ or a ‘Outperform’ rating on the stock.

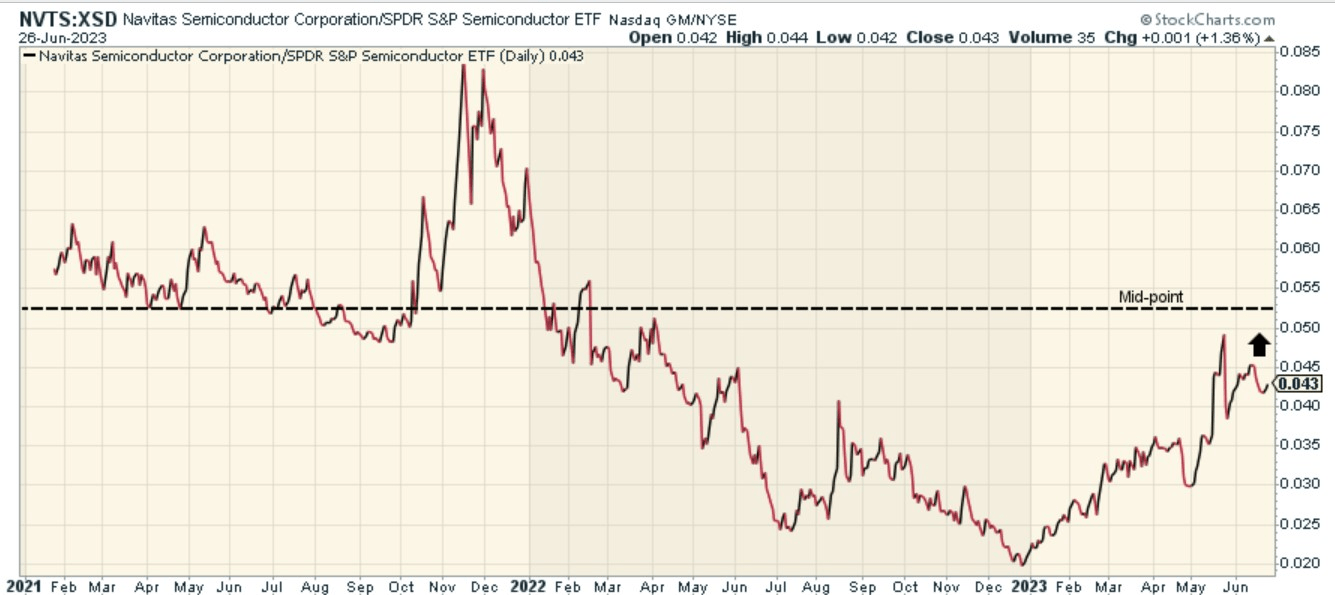

So, at this juncture, would Navitas stock be considered a good mean-reversion pick within the broad semiconductor universe? Well, you could say it may continue to benefit from some rotation momentum, as the relative strength ((RS)) ratio of NVTS versus the SPDR Semi ETF has still not breached or crossed the mid-point of its trading range, but you’d like to think that this would have been a more rewarding trade at the end of last year, when the RS ratio was at record lows. Now that trade isn’t as compelling.

{kind=link}

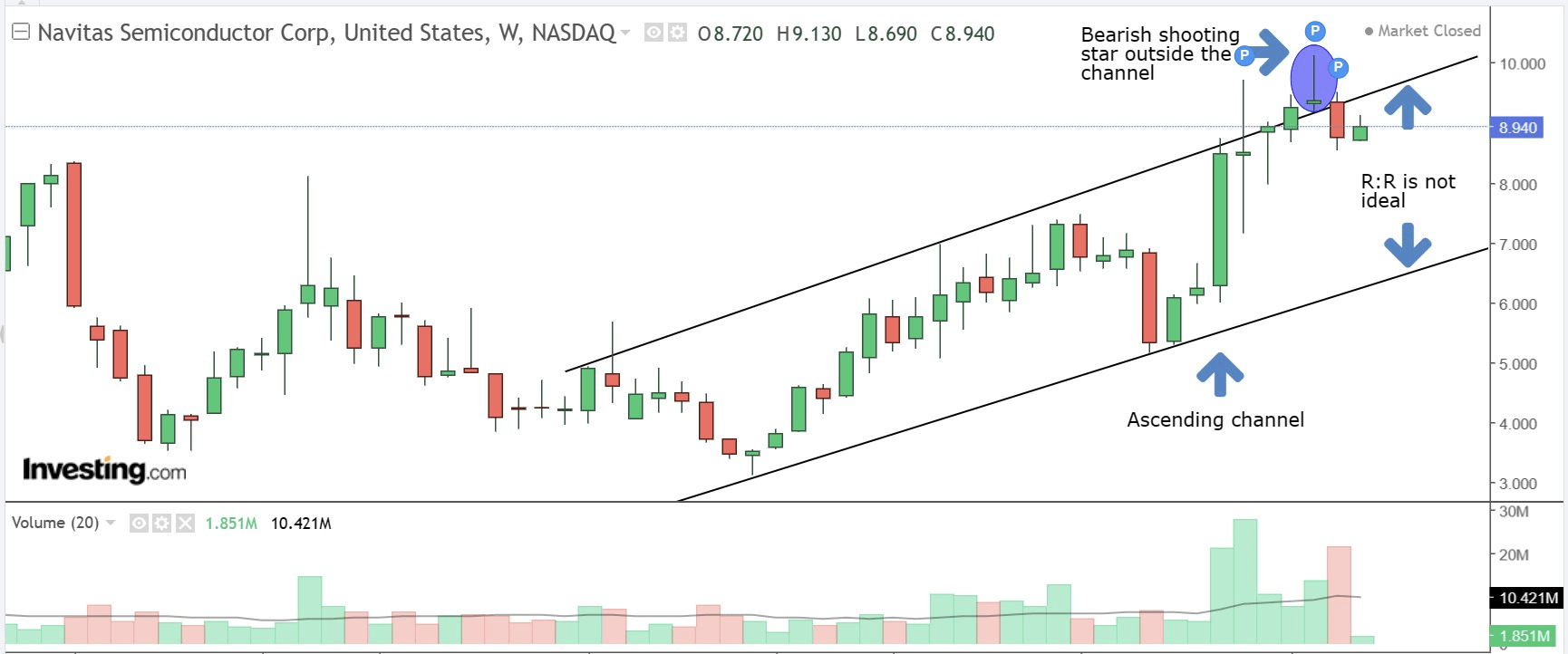

Then, on the standalone weekly chart of NVTS, one has been enthused to note that the stock has been trending up since late December 2022 in the form of an ascending channel. Last month we saw the stock breakout of this channel but in a few weeks, it could not sustain the momentum and we ended up seeing a candle with a long upper wick as buying momentum ebbed (the shooting star candle which usually signals a reversal in price action).

{kind=link}

The stock has now dropped back into its old channel, and we feel investors would do well to wait for a pullback towards the $7-$8 levels (which is closer to the lower boundary of the channel) before a long position is considered.

For further details see:

Key Considerations For Those Contemplating A Position In Navitas Semiconductor