ICE - Key Markets Built To Meet Investor Needs

2023-10-17 03:53:27 ET

Summary

- Electronic trading has transformed financial markets, but unfortunately benefiting intermediaries at the expense of investors.

- Recent new exchanges have failed to compete with established ones because they offer nothing investors need.

- An investor-focused exchange could offer new securities designed around investor needs. It could provide stability, equal access to the best price, and lower costs for investors.

Introduction

The primary force driving the change in financial market structure since the year 2000 is the advent of electronic trading. Electronic trading has greatly improved execution speed and reduced trading costs for everybody in the three key financial markets - short-term corporate debt, Treasury securities, and equities. This article explains how, with the advent of electronic trading, investors became outsiders in these three most important markets. It proposes a simple cure that will ensure equal access to all.

A new exchange that focuses on investor needs would be in a far better position to compete with the old guard - CME Group, New York Stock Exchange, NASDAQ, and CBOE - than were the recent de novo stock exchanges - IEX, MEMX, and LTSE. These newer exchanges limited the market access of investors in some cases. In every case, the new exchanges did not make enough positive difference to potential issuers to attract them. Any new exchange must address the question of listing new issues. Nonetheless, the successful futures markets of the CME reveal that one way of creating new listings is for the exchange to create its own listed securities.

Because of inequities resulting from electronic trading, investors have become second-class citizens of the old-school financial market space, no longer receiving equal access to the best bid and offers in these three most important financial markets. Instead, a disproportionate share of the gains from electronic trading have gone to market intermediaries like exchanges and broker-dealers.

Moreover, the market structure resulting from electronic trading has other undesirable properties. Most notably the evolving market structures produced by electronic trading have destabilized markets unnecessarily.

Electronic trading has not lived up to its promise to provide access to the market's best bid and offer to investors. In all three markets, the enormous speed advantage electronic trading produces has been twisted and then turned into a barrier to investors.

This article describes the three markets’ surprisingly similar structures, showing how these structures benefit market insiders at the expense of investors. These markets are so important that I call them collectively our financial markets’ centerpiece.

This article builds upon my earlier piece , “Three Markets. A Fix.” This article explains how to build and manage an investor-friendly market centerpiece that improves the market environment for investors in many ways. The proposed market center does more than give retail investors a better deal - equal access to the market's best bid and offer. It also provides investors with investments that have greater stability in a financial crisis, greater market transparency for regulatory purposes, and a lower cost of investing for all. Its success, however, would come in part at the expense of older markets that do not meet these same standards.

The Once-Evolving Technology of Financial Markets Has Stalled

The competition from new exchanges for trading volume in the common stock sector has seemingly ended. Recent new stock exchanges (IEX, MEMX, and LTSE) have failed to capture a significant market share.

Yet the rapid increase in volatility of interest rates and the attendant increase in financial market volatility in the broader financial marketplace of the post-COVID crisis financial era has created opportunity. Financial markets are now on fallow ground - an opportunity for a central marketplace to bump the old-school stock and futures exchanges aside by offering instruments and trading technology that better meets the needs of investors.

Most importantly, a de novo exchange needs a new and different agenda - serving investors instead of issuers and intermediaries.

Other practitioners and market regulators have noted the existing financial market shortcomings, here and here . Major market regulators are proposing new regulations that have attacked both spot markets and derivatives markets. Regulators see that market insiders systematically line their pockets by depriving ordinary investors of access to the higher quality prices those insiders enjoy.

But importantly, regulators cannot successfully meet their obligation to ensure financial markets serve investors' needs until private sector investors identify an alternative to the existing market structure.

Desirable Improvements That Result from a Different Market Agenda

An exchange with a different focus - on investors instead of issuers - could introduce properties that are very different from the status quo.

Here is a list of feasible market improvements, along with the shortcomings of the markets now.

-

Stable instruments and market pricing in high volatility environments . The markets for corporate and Treasury debt are unstable during changes in market perception of risk. The Fed has been forced by the collapse of the Money Market Mutual Funds (MMMFs) -- the investor-facing instruments of the market for the short-term debt - twice since the shift to electronic trading.

-

Market stewards accessible to market regulators. The commercial paper market is an over-the-counter market, lightly regulated with no central management. None of the three markets has a single private sector market steward with market-wide decision-making power. Only the futures markets have market-wide management accessible to market regulators.

-

Equal access to the best prices. No insider and outsider markets. Broker-dealers in all three of these securities markets have used the effects of high-speed trading to split the markets into insider and outsider markets.

-

Elimination of unnecessary clearing expenses. DTCC-provided assurance of rights of corporate governance is an unnecessary cost because rights of ownership matter only to activists - a reality proven by ETFs that split ownership from income flow. Central marketplace assumption of responsibility for clearing - like futures markets - would substantially reduce the cost of transactions by bypassing the DTCC.

-

Financial instruments that meet the needs of investors, not issuers. Stock exchanges serve IPO candidates first, commercial paper banks serve issuers first, and the Treasury handcuffs securities dealers demanding they meet Treasury wishes. In other words, broker-dealers and corporate securities issuers have designed the markets to attract issuers, taking investors for granted. Issuers have the ability to anoint chosen exchanges and other intermediaries as their primary listing venue, giving them great leverage in exchange decision-making.

The Structure of Central Markets Now

Common properties

The common characteristics of these three markets suggest a single investor-focused market center could use a single market structure to counter problems in these three markets. This article identifies the post-electronic trading properties of the stock market’s structure and then identifies equivalent structure and market participants of the other markets. The article then proposes changes that would dramatically change the way investors use financial markets.

Stock exchanges

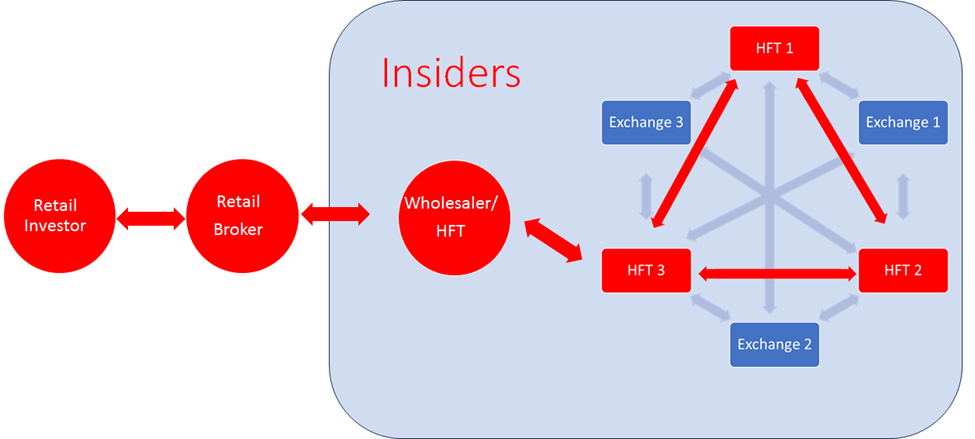

The stock exchanges were the second major market after financial futures to automate exchange trading. Most importantly, electronic trading of common stocks has developed into a split insider/outsider market. The graphic below identifies the important stock market participants and their interactions.

-

Investors - originate purchase orders.

-

Brokers - broker investor orders. Brokers receive a fee (Payment for Order Flow, (PFOF)) from market Wholesalers in exchange for investor orders. Wholesalers then become over-the-counter ((OTC)) counterparties to investors.

-

Wholesalers/High Frequency Traders (HFTs) - broker-dealers pay PFOF to retail brokers to execute customer orders at off-market prices. These OTC transactions with Wholesalers deny retail investors access to the inside market. The HFTs then offset their OTC trades with investors by reversing them at insider prices.

-

The stock exchanges and other transaction platforms that focus their efforts on attracting insiders - issuing firms on one hand and high frequency traders (HFTs) on the other. These trading platforms have proliferated to the point where only HFTs can survive inside market trading unscathed.

The graphic below displays the structure of equities markets today.

Electronic Market Structure (Author)

{kind=link}

Following the introduction of electronic trading, firms called High Frequency Traders (HFTs) made a living by collocating their own computers with exchange transaction engines, stocking them with algorithms that exploit (through arbitrage) small differences between prices on one exchange compared to another.

The exchanges jumped on the HFT bandwagon in response to opportunities to collect fee income associated with HFT trading. The domination of the inside market by HFTs induced the exchanges to proliferate to increase arbitrage opportunities. As a result, the exchanges became exchange management firms, each firm adding multiple new exchanges, clones of themselves, to expand HFT arbitrage opportunities.

This development left investors’ brokers with a quandary - given more than 15 exchanges, each of them changing their bids and offers at the speed of light, brokers unintentionally sent orders to an exchange that had a lower quality price than another, thus breaking the rules of the SEC’s National Market System.

To avoid the impossible task of identifying the exchange with the best price, retail brokers accepted payment from a broker-dealer/wholesaler to fill their customer orders without worrying about the current best price in the market. Every market insider wins from this arrangement.

-

The retail brokers sell their orders to be executed OTC in exchange for a payment from their selected wholesaler.

-

Wholesalers then have a constant stream of below-market orders to execute off the market, reversing them by placing the same order for their own portfolio at a better insider price.

-

Exchange management firms benefit from the insider system because they own multiple exchanges, reaping exchange fees from as many as five separate exchange subsidiaries, all providing the same transactions. Everybody wins except investors.

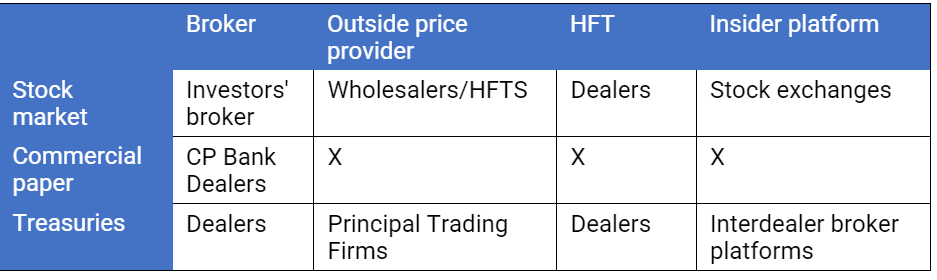

Components of Three Markets (Author)

{kind=link}

Comparing Markets for Short-Term Corporate Debt to the Stock Market

Commercial paper ((CP)) (short-term corporate debt) . The CP market provides historically the worst service to non-bank participants among the three markets. This is because investors have historically left the sale of their CP to commercial banks. Indeed, a corporation will often give all its business to a single bank. Commercial banks in turn do little to compete with their peers in the banking community. Thus, there is no central liquid market for short-term commercial paper.

The Chicago Mercantile Exchange improved investor knowledge of short-term corporate interest rates when it introduced Eurodollar futures in 1980. However, this solution to the opacity of the corporate debt market ultimately failed. The spot financial instrument that settles a Eurodollar futures contract, a London interbank wholesale deposit, is both without a secondary market and characterized by only a few eligible Eurodollar issuers. Yet, the LIBOR rate that the London market traded was reactive to changes in market risk and available during market crises that produced havoc in the CP market.

Nonetheless, the shortcomings of the Eurodollar spot market finally ended it. The Federal Reserve and the Bank of England combined forces to put an end to the CME Group’s Eurodollar futures contract, by ending LIBOR. The fatal flaw of Eurodollar futures was market regulators’ well-founded belief that LIBOR is so illiquid that market insiders could easily manipulate it.

Markets for Treasury securities. Dealers in the markets for Treasuries have followed the practices mandated by the Treasury and the Fed. This is reasonable since these agencies represent taxpayers. Without the influence of the Treasury and the Fed, taxpayers would have no representation in the market for Treasury debt.

Nonetheless, a market participant or participants that successfully put Treasury investors’ interest first would increase the demand for Treasury investments. This would benefit all market participants. The seeming conundrum that causes skepticism about this possibility is that nobody has developed an investment that satisfies the majority of the market centerpiece requirements above.

Stability. The closest thing in the current retail-friendly Treasury marketplace is the Money Market Mutual Funds (MMFs). However, these funds have collapsed in the two most recent episodes of market volatility, the ’08 financial crisis and the COVID-19 Crisis.

Market Stewardship . The changes that the MMMFs have made to satisfy market regulators are all the result of legislation. Regulators have forced greater stability during crises - suggesting that an investor-friendly investment firm could design and issue a more stable investment without the need for regulation.

Equal access to the best prices. No insider and outsider markets. In the market for Treasuries, the Fed’s custom of approving each government securities dealer but otherwise not restricting broker-dealer behavior leaves the Treasury securities market with a government-mandated population of insiders. To access inside prices on term Treasury-based instruments, an investor-friendly market would need to design Treasury-based instruments that meet investor needs instead of Treasury needs. The dealers now have access to inter-dealer exchange-like platforms that encourage HFT participation and permit access only to the government securities dealers.

How an Investor-Friendly Exchange Would Work

There are four basic failures of the three center markets now. Other failures listed above are the result of these four. The failures all have straightforward solutions.

-

Investor exclusion. Failure to provide equal access to investors.

-

Market stewards inaccessible to market regulators.

-

Listing securities that meet issuer needs, not investor needs.

-

Assuring market stability.

Investor exclusion. The futures markets provide certainty of equal access by making the exchange clearinghouse a counterparty to both buyer and seller. This guarantees that the best bid and offer are available to all. A de novo exchange could easily add this feature to a spot market, so long as the marketplace itself issues the securities traded.

Market stewards inaccessible to market regulators. A futures-style clearing system where the exchange is a counterparty to buyers and sellers assures that the exchange is aware of market instability and accessible to regulators.

Listing securities that meet investor needs. Assurance that securities meet investor needs is a daunting but essential task. The evidence of the existing market structure is that issuers control the structure of the markets they choose for their primary listing, since without an issuer, there is no security to trade.

If so, the only way a de novo exchange can list investor-friendly securities is to create and list these securities itself.

Assuring market stability. The exchange issues the traded instrument collateralized according to exchange rules. Thus, sellers that exit the market will receive a portfolio of securities identified by the rules of the exchange. The exchange can prevent squeezes by delivering readily marketable collateral issues.

Conclusion

The speed and efficiency with which investors get their purchase orders executed electronically have masked the remaining inefficiency of the current securities market structure. These inefficiencies will remain hidden until investors’ brokers offer an alternative that better meets investor needs.

Our current market structure has many shortcomings. These shortcomings follow from the incentives of market intermediaries - the exchanges and exchange-like trading platforms and broker-dealers. The exchanges and broker-dealers have organized their current market structure to attract new listings. This focus on listings at the expense of investors on the other side of market transactions is sensible when listings are a decision of corporate issuers. An exchange without primary listings is missing a major source of revenue and prestige. The new exchanges have learned how critical attracting listing firms are.

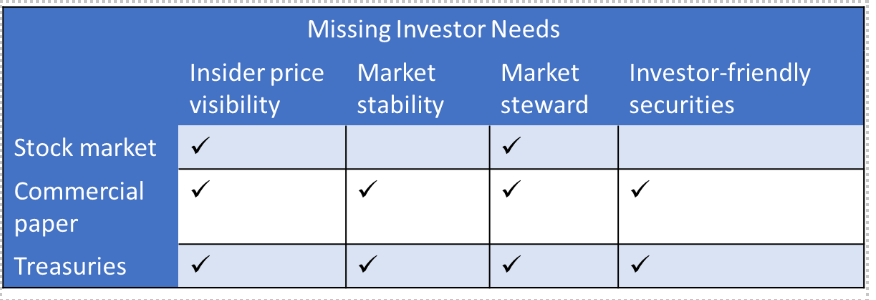

{kind=link}

The table above checks the boxes that represent the missing investor-friendly characteristics of each of the three markets.

The table indicates the relative investor friendliness of the stock market. It is more stable than the other two markets despite the fact that individual stocks are typically more volatile than debt securities. Stock market participants design stocks to facilitate investor needs. For example, stock market customs such as listing a single issue rather than many improves liquidity.

This primacy of listing in the decision-making of the old-line exchanges exposes an avenue that might create inroads in market share.

An exchange that issues the securities it lists in a way that appeals to investors is in a much better position to meet investors’ needs - both retail investors and institutions. The article shows some of the primary improvements to market structure that an exchange motivated to attract investors would seek to add.

The conclusion I draw from this investigation is that there are two keys to de novo exchange success.

-

Successful new listings.

-

Listed instruments that meet an unmet investor need.

In addition, a de novo exchange can offer investors and market regulators.

-

More stable versions of important market securities.

-

A reliable market steward.

For further details see:

Key Markets Built To Meet Investor Needs