CGNX - Keyence: Anticipating Earnings Deterioration Downgrading To A Sell

2023-10-18 08:38:01 ET

Summary

- Keyence stock's rating is downgraded from buy to sell due to falling earnings visibility and increasing macro concerns.

- Concerns over weak capital investment activity in Asia and rising caution in Japan pose near-term challenges for Keyence.

- The negative macro environment, including a potential US recession and geopolitical tensions, further contribute to the downgrade.

Investment thesis

We are updating our view on Keyence ( KYCCF ) and downgrading our rating from a buy to sell, given near-term concerns over falling earnings visibility, and increasing macro concerns into CY2024. Our previous call has resulted in a 50% drawdown, but we believe there is further downside risk.

Quick primer

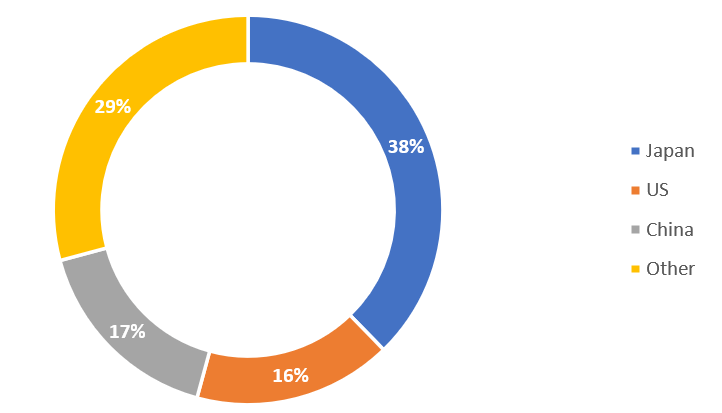

Based in Osaka Japan, Keyence is the global leader in sensors and machine vision systems. Its key competitive advantages are product innovation and a high-speed product development cycle. Domestic sales contribute around 40% of total revenue (although this may include some China-bound business), followed by China with 17% and the US with 16%. Keyence is a fabless manufacturer and it is company policy to ship products for next-day delivery.

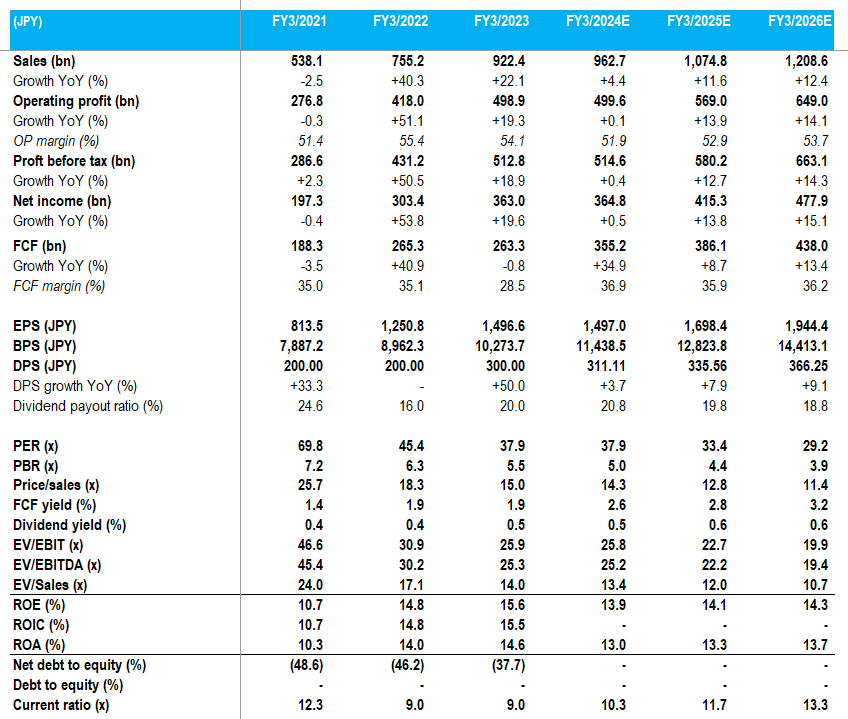

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

Sales mix by geography - FY3/2023

Sales mix by geography - FY3/2023 (Company)

{kind=link}

Updating our view

We are updating our view from September 2021 , where we rated the shares as a buy, with some reservations based on capex trends. After two strong years of growth, consensus forecasts show flat earnings growth for FY3/2024 (please see key financials table above), despite Q1 FY3/2024 results recording 15.8% sales growth.

Keyence's limited disclosure hinders analysis, but we use Cognex ( CGNX ) as a proxy to understand present business conditions and assess the earnings outlook. We note that Cognex shares have been underperforming Keyence since early 2021; we put this down to three factors: 1) headwind from a strengthening dollar, 2) relatively high exposure to China, and 3) high dependence on the traditional automotive sector.

Whilst Keyence has a diversified customer base, China is the second-largest reported market. There is no doubt that the company is a global leading quality cyclical with operating margins of 50% plus, but our buy rating has seen a near 50% drawdown. We want to assess whether there is scope for recovery, or whether it is time to exit.

Some concerns in the near term

Q1 FY3/2024 results included comments from management regarding weak capital investment activity by customers in Asia, as well as rising caution in Japan. This tallies with what Cognex disclosed in its earnings call for Q2 FY12/2023 results where there was weakness in consumer electronics and semiconductor capital equipment markets in China and other Asian markets.

Cognex's guidance for the current quarter was negative, with expectations of a sequential decline in Q3 FY12/2023 sales due to weakening demand for factory automation equipment, with demand from the consumer electronics sector expected to remain sluggish. This is a negative read-across for Keyence, as China's exposure has grown the most over the last 2 years.

Indication of a negative macro environment

CY2023 has experienced a resilient US economy, with Japan's GDP looking robust driven by exports. The current forecast for 2024 by the IMF points to real GDP growth remaining relatively unchanged YoY, with more of the same as the world economy expected to sustain a mild growth rate of 2.9% - this does not sound like it will lead to a material recovery YoY for any capital good company including Keyence.

With volatile market conditions, global consumer confidence remains low and businesses are less inclined to commit capital. Increasing financing costs places project appraisals under greater scrutiny. Our view is that 2024 will see a slowdown scenario spread to other geographies such as the US and Japan, lowering earnings visibility. Fitch is expecting a mild US recession in H1 CY2024. Recessions are temporary and a new economic cycle will pave the way for an earnings recovery; however, we do not believe the shares are currently pricing in a deterioration in earnings.

China remains a bugbear with its weak housing market and its impact on the wider economy. Geopolitical risk is rising with tensions in the Middle East, fueling negative business sentiment. Despite Keyence's strong market position, we believe customer factory automation capex demand will be on a downtrend.

Valuation

With outstanding returns and a strong track record, Keyence's shares deserve to trade at a premium. On consensus estimates, PER FY3/2025 33.4x does not sound too stretched. However, EV/EBITDA of 22.2x is a high multiple, leaving limited room for valuation support.

With a cash-rich balance sheet, some market observers believe that shareholder returns will improve. However, consensus maintains a 20% payout ratio, and as a company known to furrow its own path, we do not believe this is a high-priority issue.

Current valuations do not look attractive, given the near-term weakness in earnings visibility although this has been partly priced in. Our key concern is the likelihood of continued weakness into FY3/2025, which will be viewed as a negative surprise.

Thesis catalyst

I expect Q2 FY3/2024 results will see limited underlying earnings growth when excluding the weak Japanese yen. I expect the company comments on delayed recovery in China and Asia and a slowdown in US demand.

Risks to the thesis

Factory automation capex begins to recover, driven by normalizing interest rates and rising consumer confidence pushing up demand for products such as autos and consumer electronics. China's economy begins to ramp with order flow from the US and Europe.

Conclusion

Our previous buy rating has been unsuccessful. However, given the current situation over concerns over customer capex and geopolitical risks, we believe there is further downside. Increasing shareholder returns is a viable option for the company. Still, we believe management does not view the share price as a key performance indicator, focusing more on operating margins and maintaining a strong and overcapitalized balance sheet. With limited scope for earnings upside surprise, we downgrade to a sell.

For further details see:

Keyence: Anticipating Earnings Deterioration, Downgrading To A Sell