KYCCF - Keyence: Still A Best-In-Class Operator But Too Pricey

2023-07-18 11:53:00 ET

Summary

- Keyence’s fundamentals remain best-in-class.

- But the company isn’t immune to global macro headwinds.

- Having re-rated significantly this year, the stock could be vulnerable to a reset.

In line with the rest of the TOPIX index, leading Japanese factory automation player Keyence Corporation ( OTCPK:KYCCF ) has floated on a cloud of optimism this year, mainly on hopes of new governance reforms led by the Tokyo Stock Exchange. If this year’s annual general meeting was any indication, however, there likely won’t be a quick fix anytime soon. In sum, Keyence’s payout ratio remains status quo at 20% or JPY300/share for FY24 – while this is an increase from the JPY200/share payout in FY22, it pales in comparison to the JPY2.2tn cash hoard (including investments), the company is sitting on and remains flat vs. FY23 levels.

Fundamentally, the machinery backdrop remains challenging as well, with key domestic and foreign peers signaling a weaker end-market outlook across Keyence’s geographic exposures. Similarly, industrial/manufacturing data has taken a turn for the worse globally, with PMIs slipping into contraction territory across the board. Against a deteriorating backdrop, Keyence has re-rated year-to-date (YTD), helped by record foreign flows into Japan and a healthy dose of multiple expansion. While I still like the company’s exposure to secular themes like automation and its best-in-class margin profile (see my prior coverage here ), the stock’s wider-than-usual valuation premium warrants caution here.

Holding on the China Reopening Promise as Global Macro Deteriorates

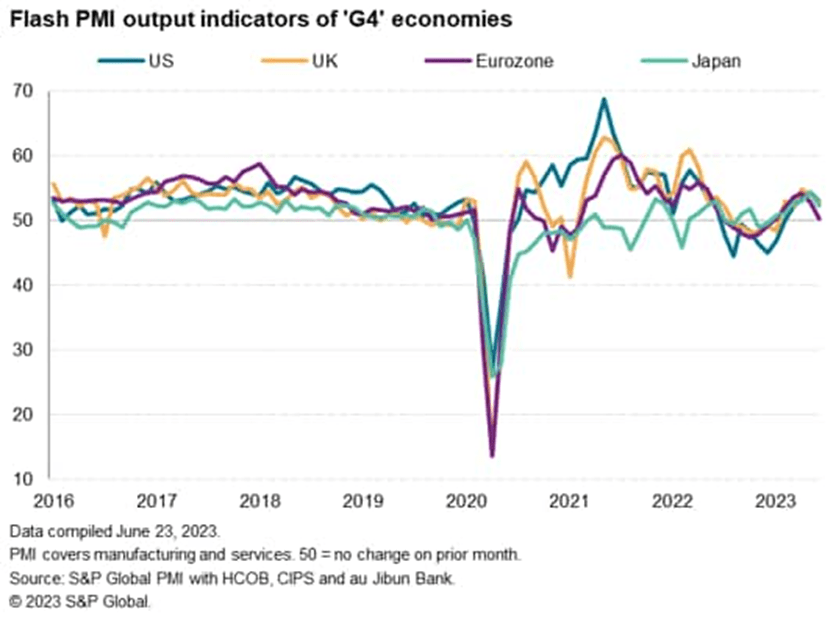

Having outperformed the TOPIX YTD on the back of China reopening hopes, Keyence’s continued rally despite the fading Chinese recovery is puzzling. While investors may be holding on to pending signs of improvement, the macro data has offered little hope. Despite a low base, China’s robot production has decelerated to +4% YoY, while its manufacturing PMI has posted consecutive months of sub-50 (i.e., contractionary) readings. Similarly, in Japan, Europe, and the US, manufacturing PMIs have dipped well below 50 for months now. So unless the Chinese recovery somehow broadens out (Q2 notwithstanding, given the easier YoY comparable), underwriting a weaker revenue growth algorithm for Keyence seems like a safe bet.

{kind=link}

S&P Global

One of my biggest concerns coming out of the full-year results was Keyence management’s decision to increase headcount (mainly overseas) in anticipation of demand growth post-reopening. While I have no doubt that the company will see sustained demand growth over the mid to long term given the secular automation tailwinds, it also entails opex pressure in the interim. To be fair, Keyence has pricing power, as demonstrated by its last price revision in October last year (within a 10%-35% range). Whether the company has enough in the bag to defend margins this year is another question, however, particularly with capex budgets on the decline amid the global growth slowdown. Management’s lack of investor communication could work against them here – having offered no update since last quarter’s upbeat commentary indicating intact automation demand and isolated demand weakness from semiconductors, a big reset could be on the cards next quarter.

{kind=link}

Keyence Corporation

Peer Readthroughs Validate the Case for a Guide Down Ahead

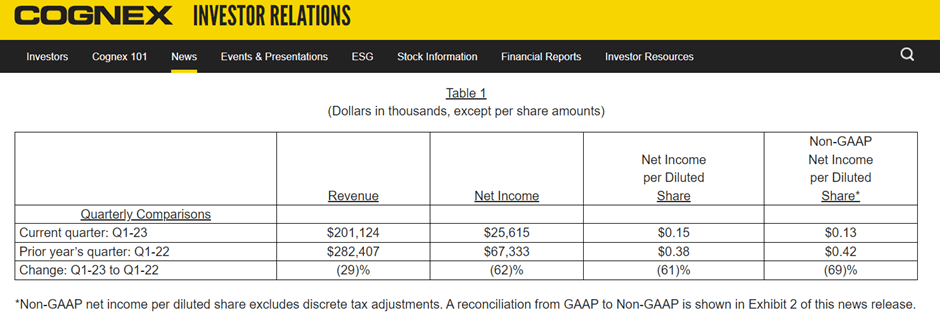

There wasn’t much fault in Keyence’s numbers last time around, with sales growth of +24% YoY (+12% YoY FX-neutral), outpacing its Japanese automation peers. Since then, however, global peers like Cognex ( CGNX ) have begun to show concerning signs of a revenue slowdown amid a challenging macro backdrop globally. To recap, Cognex saw a steep -29% YoY revenue decline (-26% YoY FX-neutral) in Q1 2023, citing capacity expansion delays for e-commerce clients and cautious spending across its end markets. By geography, the Americas and Asia-ex Japan saw the steepest revenue declines, followed by China which was down over 30% on consumer electronics weakness. Since then, Cognex management has rebased its Q2 sales growth guidance to down a low-teens percentage YoY – given China’s low Q2 base, the downward revision implies more weakness ahead. Similarly, Japanese machine tools manufacturer Okuma ( OTC:OKUMF ) cited demand headwinds from rising interest rates weighing on the machine tool demand outlook (down YoY for 2023). With PMI data deteriorating further since then, the readthrough from the machinery sector is decidedly negative.

{kind=link}

Cognex

Given Keyence’s overlapping end markets with the likes of Cognex, including in its key autos, electronics, and semiconductor end markets, the wave of downgrades doesn’t bode well for the upcoming results. While Keyence might show relatively more top-line resilience, helped by its larger and more diversified revenue base, the company is still at the mercy of the global cycle; hence, a sequential slowdown globally will hit the P&L, albeit with a lagged impact given the earlier fiscal cutoffs for the overseas subsidiaries. Margins are also a big concern, given Keyence’s high-teens percentage YoY increase in headcount (per its latest annual report ) will add pressure to the opex line at a time when weaker sales are set to drive operating deleveraging. The FX buffer will help slightly (note the stronger yen FX assumptions), so the continued yen decline will lend some support to guidance. Yet, it seems unlikely that FX alone will be enough to offset the earnings decline. And with the Japanese machinery sector already re-rating strongly this year, the optimism embedded in the price leaves Keyence vulnerable to a reset.

Still a Best-In-Class Operator but Too Pricey

With Keyence showing little progress on the corporate governance front at this year’s AGM, the YTD rally, buoyed by a renewed TSE-led governance reform push, seems unjustified. Alongside the rather unimpressive dividend payout (flat at 20% or JPY300/share), the global machinery backdrop continues to deteriorate, as highlighted by worsening manufacturing PMIs across the major economies. And as key peer Cognex’s underwhelming Q1 2023 showed, the macro data is translating into weaker revenue across the board. While Keyence has the pricing power to offset some margin pressure, it seems unlikely that there are sufficient levers in the P&L, particularly with management stepping up the global headcount last quarter. Yet, the YTD multiple expansion has taken the stock to a historically wide valuation premium at ~43x earnings, skewing the risk/reward firmly to the downside ahead of a machinery downcycle.

For further details see:

Keyence: Still A Best-In-Class Operator But Too Pricey