HXGBF - Keysight Technologies: Still Not A Buy Despite A Robust Rally

2023-05-17 18:17:06 ET

Summary

- Keysight Technologies reported Q2 2023 revenue of $1.39 billion, a 2.9% increase YoY, exceeding analysts' expectations.

- The company's Electronic Industrial Solutions Group saw a 17% revenue increase, while Communications Solutions Group saw a 3% decline.

- Despite positive results, the company's shares look more or less fairly valued, with a "hold" rating recommended for investors.

One of the more interesting companies on the market these days is a firm called Keysight Technologies ( KEYS ). The business has its hands in many different things, including work that involves it providing electronic design and test solutions that are used in simulations, design work, product validation, and more. It also provides customization, consulting, and optimization services, amongst other things. Even though the economy is on questionable turf right now, the enterprise continues to post consistent growth on both its top and bottom lines. The most recent example of this can be seen by looking at the financial results the company reported for the second quarter of its 2023 fiscal year. These just came out on May 16.

Although the bottom line was a bit mixed, revenue exceeded expectations and management provided guidance for the third quarter that seems to be in line with what analysts expect. All of this is great news. However, this doesn't necessarily mean that the company makes sense for investors to buy into at this time. Although I have no doubt that the company will do well for itself and its investors in the long run, shares do look to be more or less fairly valued on an absolute basis, even as they are on the cheap end of the spectrum relative to similar enterprises. And even though guidance did not turn investors off, it is clear that the firm will see some weakening in the second half of this year.

A mixed but positive quarter

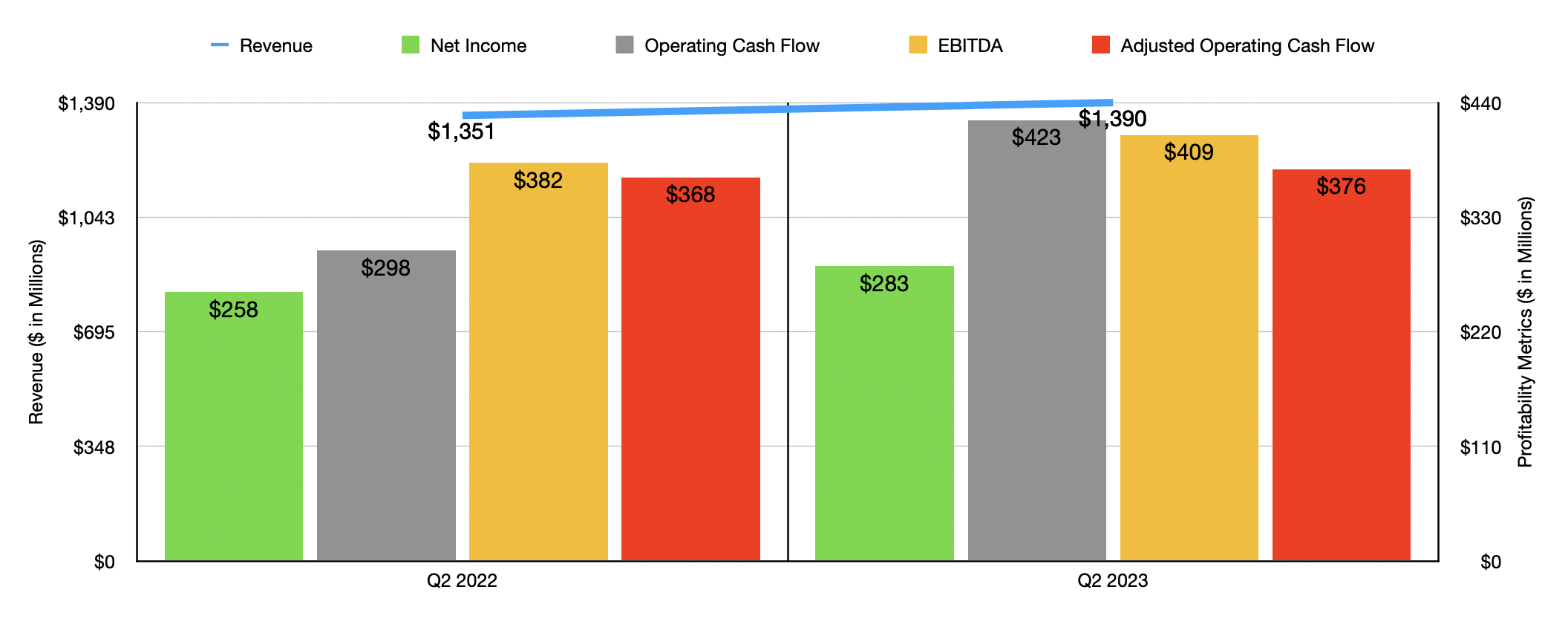

Keysight Technologies saw its stock price rise about 7.6% on May 17 in response to mixed but generally positive financial results covering the second quarter of the 2023 fiscal year that the company reported on after the market closed on May 16. For the quarter, revenue came in at $1.39 billion. That represents an increase of 2.9% over the $1.35 billion the company reported one year earlier. Although this may not seem like a big move higher, it did actually exceed analysts' expectations by $7.4 million. And to make matters better, sales growth would have been 5% had it not been for foreign currency fluctuations.

{kind=link}

Really, all of the growth reported by the company came from its Electronic Industrial Solutions Group. This is the part of the company that provides test and measurement solutions and other services for electronic industrial end markets. Revenue here spiked around 17%, growing from $388 million to $453 million. Management attributed this increase to growth across general electronics, semiconductor solutions, and next-generation automotive and energy technologies. This is not to say that everything at the company performed well. Its larger segment, called the Communications Solutions Group, reported a 3% decline in revenue, driven by a 7% drop in commercial communications. The picture here would have been worse had it not been for a 7% increase in revenue associated with radar, spectrum operations, space and satellite activities, and research in both 5G and 6G technologies.

On the bottom line, the company had results that were a bit more mixed. Earnings per share, for instance, came in at $1.58. This was $0.18 per share lower than what analysts thought it would be. But if we look at it from an adjusted basis, profits would have been $2.12 per share, beating forecasts by $0.17 per share. Personally, I am not a huge fan of adjusted earnings when those include share-based compensation being added back to the equation. But that accounted for $0.16 per share. All of the other changes were largely associated with things like tax adjustments, amortization of acquisition-related balances, and more. For context, the earnings per share reported by the company translated to net income of $283 million. That beat out the $258 million, or $1.41 per share, that management reported for the second quarter of the 2022 fiscal year.

Other profitability metrics for the company came in positive. Operating cash flow, for instance, jumped from $298 million to $423 million. If we adjust for changes in working capital, the increase was considerably smaller, with the metric growing from $368 million to $376 million. And finally, EBITDA for the enterprise totaled $409 million. That represents a decent increase over the $382 million reported one year earlier. The company's bottom line figures were costs that increased at a rate that was slower than revenue rose. While overall revenue for the company grew 2.9% year over year, its total operating costs inched up only 1.2%. This was thanks in large part to a 2.2% reduction in the costs of products and services.

{kind=link}

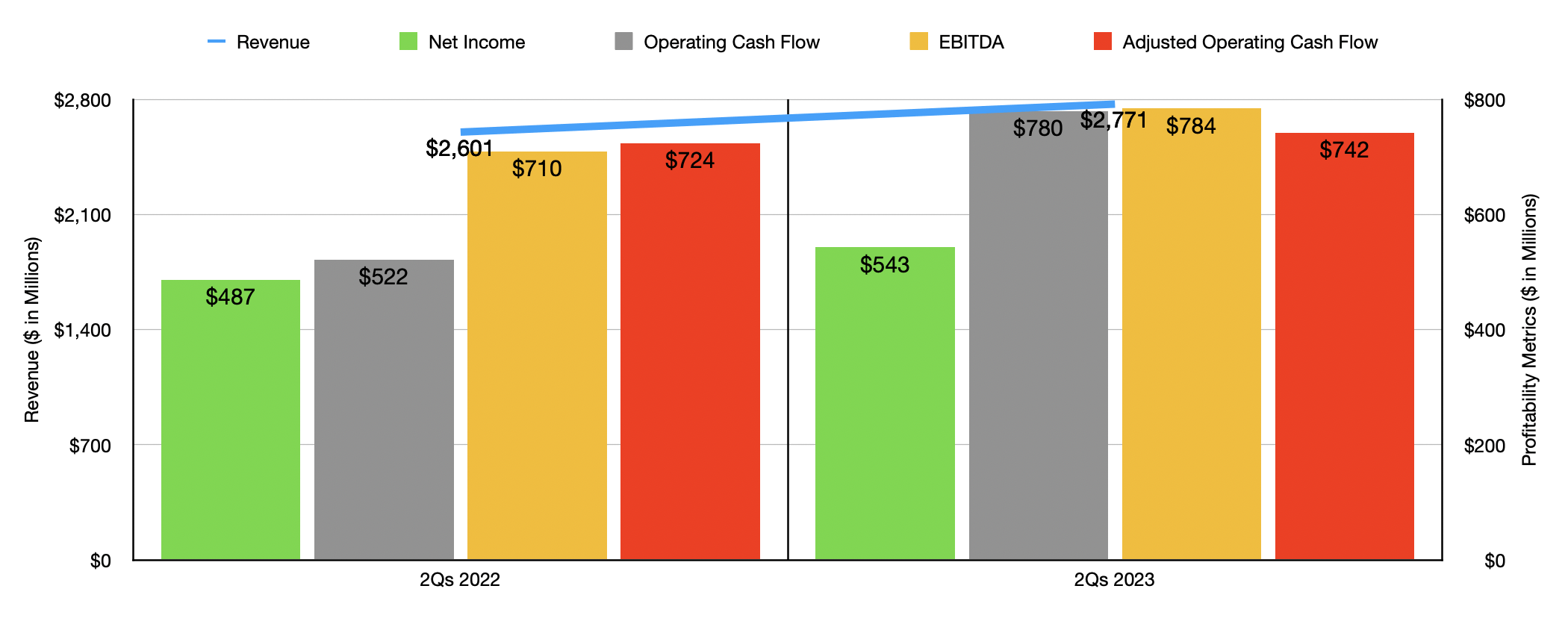

For context, you can also see, in the chart above, financial results for the company for the first half of 2023 relative to the same time of the 2022 fiscal year. Just as was the case with the second quarter alone, revenue, profits, and cash flows increased year over year. This is not to say that this will remain the case moving forward. Management does not provide guidance when it comes to 2023 as a whole. But they have provided guidance when it comes to the third quarter. They currently expect revenue to be between $1.37 billion and $1.39 billion. This is right in the range of the $1.38 billion that analysts anticipate. It's also around the $1.38 billion that the company reported in the third quarter of its 2022 fiscal year.

{kind=link}

Truth be told, I find this guidance to be a bit surprising. After all, in the second quarter of this year, the company reported orders of only $1.32 billion. That was 9.5% lower than the $1.46 billion the company reported one year earlier. And for the first six months of the year as a whole, orders of $2.62 billion happened to be 11.3% below the $2.95 billion reported for the same time last year. So it seems as though these weaker orders will cause revenue to more or less flat line, at least for now. But on the bottom line, we could be in store for some nice improvements as costs continue to rise at a rate that's slower than revenue growth. For the third quarter, management is forecasting earnings per share of between $2 and $2.06. Analysts are right in the middle there at $2.03. For context, in the third quarter of last year, profits per share came in at $1.87.

{kind=link}

Since we don't know what to expect for the 2023 fiscal year in its entirety, I decided to forecast financial results by annualizing the results we've experienced so far. This would imply a net income of $1.23 billion. Adjusted operating cash flow would be $1.58 billion. And EBITDA would come in at $1.72 billion. As you can see in the chart above, the company is trading at a forward price to earnings multiple of 22.7. The forward price to adjusted operating cash flow multiple is lower at 17.7. Meanwhile, the EV to EBITDA multiple should be about 15.9. This is aided by the fact that the company has cash in excess of debt totaling $705 million. The chart also shows how shares are priced using data from 2022. Using those results, shares would be a bit pricier. In the table below, you can see how shares are priced relative to similar firms. When it comes to both the price to earnings approach and the price to operating cash flow approach, even using data from our 2022 fiscal year, you can see that Keysight Technologies is the cheapest of the group. But when it comes to the EV to EBITDA approach, three of the five firms were cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Keysight Technologies |

| 24.9 |

| 18.1 |

| 17.0 |

| Hexagon AB ( HXGBY ) |

| 27.5 |

| 22.0 |

| 23.3 |

| Teledyne Technologies ( TDY ) |

| 26.1 |

| 21.7 |

| 16.7 |

| Zebra Technologies ( ZBRA ) |

| 34.5 |

| 39.4 |

| 13.7 |

| Trimble ( TRMB ) |

| 25.7 |

| 26.8 |

| 15.1 |

| Cognex Corporation ( CGNX ) |

| 51.7 |

| 40.7 |

| 37.0 |

Takeaway

Based on how the data is looking, it looks as though revenue growth it's definitely decelerating. Weak orders are proving to be a slight problem for the company. Even so, recent financial results were better than expected on the top line and, from an adjusted approach, on the bottom line. Ultimately, the company should continue to do well for itself in the long run, even if it does hit a bit of a speed bump along the way. But this doesn't make it a great prospect for investors at this time. Relative to similar firms, shares of Keysight Technologies are definitely near the cheaper end of the spectrum. But on an absolute basis, I would argue that they look closer to fairly valued. Given these factors, I have no problem keeping the company rated the 'hold' that I assigned it when I last wrote about it in August of last year. So far, that call has proven to be perhaps even a little aggressive. Because even after this nice increase in price, shares are down 8.1% compared to the 4.2% drop of the S&P 500.

For further details see:

Keysight Technologies: Still Not A Buy Despite A Robust Rally