TNET - Kforce Q2 2023 Earnings Preview: Taking A More Cautious Approach

2023-07-13 13:25:56 ET

Summary

- The Federal Reserve's focus on softening the employment market to combat inflation has led to a downgrade in the stock of employment solutions firm Kforce from 'buy' to 'hold'.

- Kforce's revenue in Q1 2023 was 2.6% lower than the previous year, with net income falling from $19.2 million to $16.2 million, and operating cash flow cut in half.

- Despite recent encouraging employment data, the Federal Reserve's intent to pull jobs out of the economy to combat inflation could change the picture for the worse.

At this point in time, the Federal Reserve is focused on softening the employment market. This is the only tool that they seem to have at their disposal to combat inflationary pressures. They are doing this by ratcheting up interest rates with the hopes that doing so will cause the economy to weaken. These concerns led to a rather significant cut back in the number of employees at technology firms late last year and early this year. But beyond that, the labor market has remained robust. Even so, with that goal from the central bank, you may think it would be unwise to invest in any company that's focused on providing employment solutions, particularly in the technology sector. One firm in this market that has been fundamentally attractive as of late has been Kforce ( KFRC ). Despite broader concerns about the economy, share price performance has been very close to what the broader market has experienced in recent months. This is likely because of how firm the labor market has remained. In the near term, I expect this to continue. But because of how shares are priced compared to similar firms and because of the likelihood that the economy will eventually take a step back, I have decided to downgrade the stock from a ‘buy’ to a ‘hold’ for now.

The picture has changed

Back in early February of this year, I decided to write an article regarding Kforce with the goal in mind of determining whether the company made for a sensible prospect or not. In that article, I acknowledged that the firm had done quite well on both its top and bottom lines in recent years. Shares of the stock were also priced at attractive levels. These two factors led me to be confident enough in the company to rate it a ‘buy’ to reflect my view at the time that shares would likely outperform the broader market for the foreseeable future. Since then, the S&P 500 has increased by 6.8%. By comparison, Kforce has seen upside of 6.1%. While this trails the market as opposed to beating it, it is attractive enough that I don't consider this necessarily a loss.

{kind=link}

Author - SEC EDGAR Data

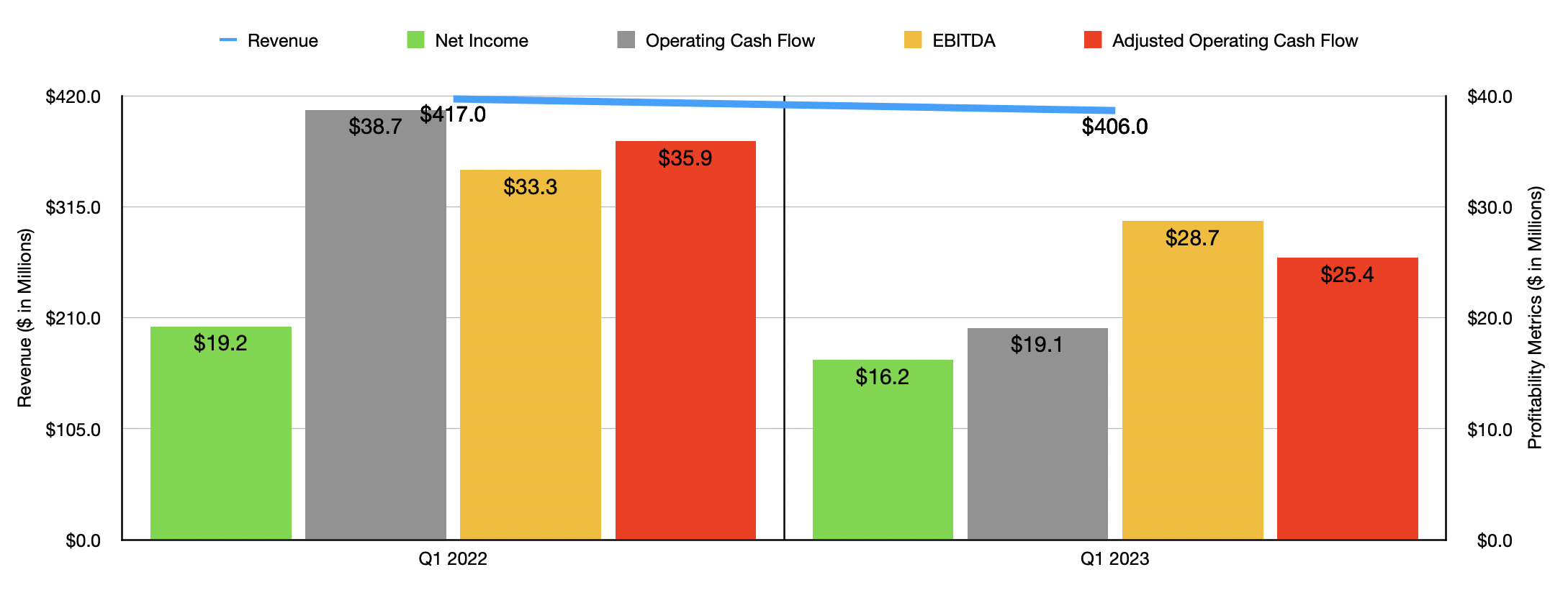

A lot can happen in the span of five or six months. That is especially true when you're talking about the current economic environment we are dealing with. I felt, then, that now would be an appropriate time to revisit the enterprise. And what I found is that there has been some weakening from a fundamental position. As you can see in the chart above, revenue during the first quarter of the company's 2023 fiscal year came in at $406 million. That's 2.6% below the $417 million the firm generated the same time one year earlier. It's important to note that the vast majority of the company's revenue comes from the flex contracts that it has dedicated to the technology space. Total hours billed under this category declined enough to cause revenue to drop $7.7 million. On the financial and accounting side of the business, which is a much smaller piece of the pie for the company, the impact here was $17.5 million to the negative. The company was able to increase its billing rate and that kept revenue from falling further. Under the technology side of things, this change helped revenue to the tune of $16 million. And under the finance and accounting side, it helped by $3.4 million.

{kind=link}

Author - SEC EDGAR Data

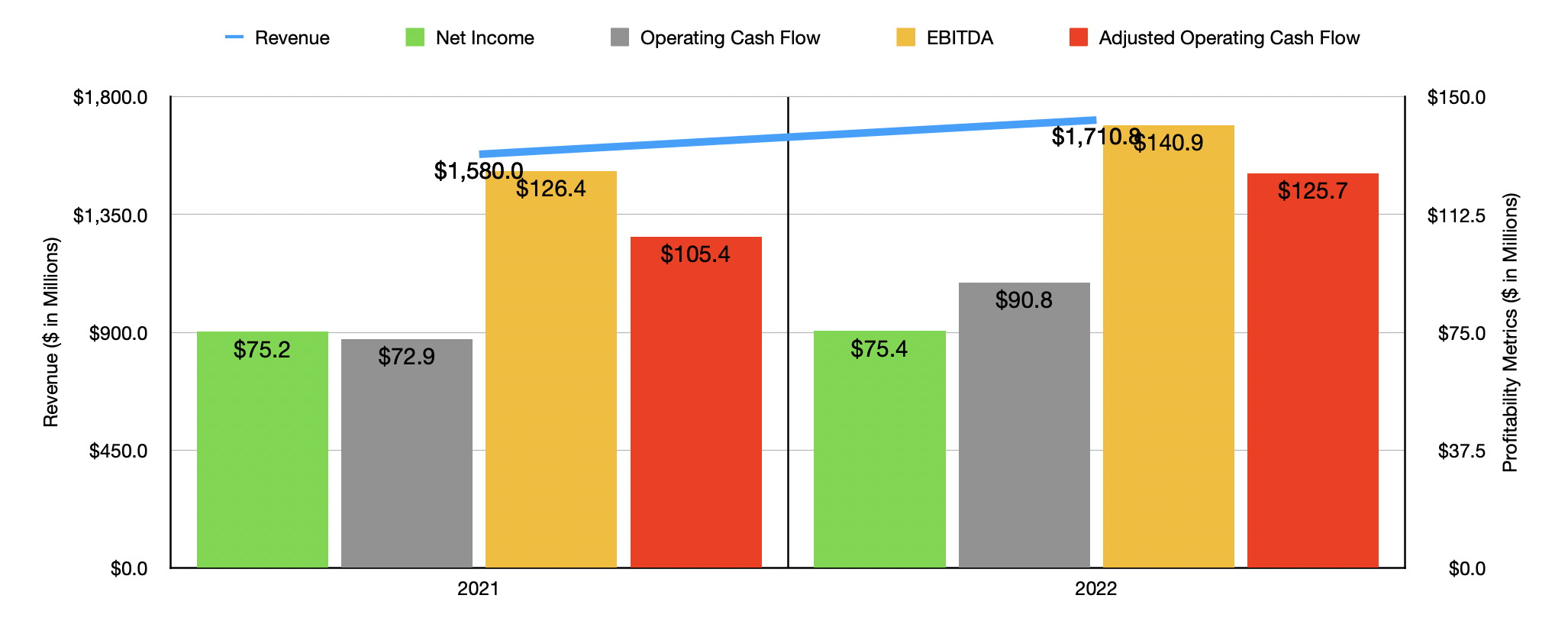

On the bottom line, the picture for the company worsened even more. Net income fell from $19.2 million to $16.2 million. We saw operating cash flow cut roughly in half from $38.7 million to $19.1 million. Even if we adjust for changes in working capital, we would have seen the metric decline from $35.9 million to $25.4 million. And finally, EBITDA for the company dropped from $33.3 million to $28.7 million. To put in perspective just how different the first quarter of 2023 has been compared to the same time last year, we need only look at data for 2022 compared to 2021 . These results can be seen in the chart above. Revenue, profits, and cash flows all rose year over year in 2022, driven by strong demand for the company’s services.

{kind=link}

Author - SEC EDGAR Data

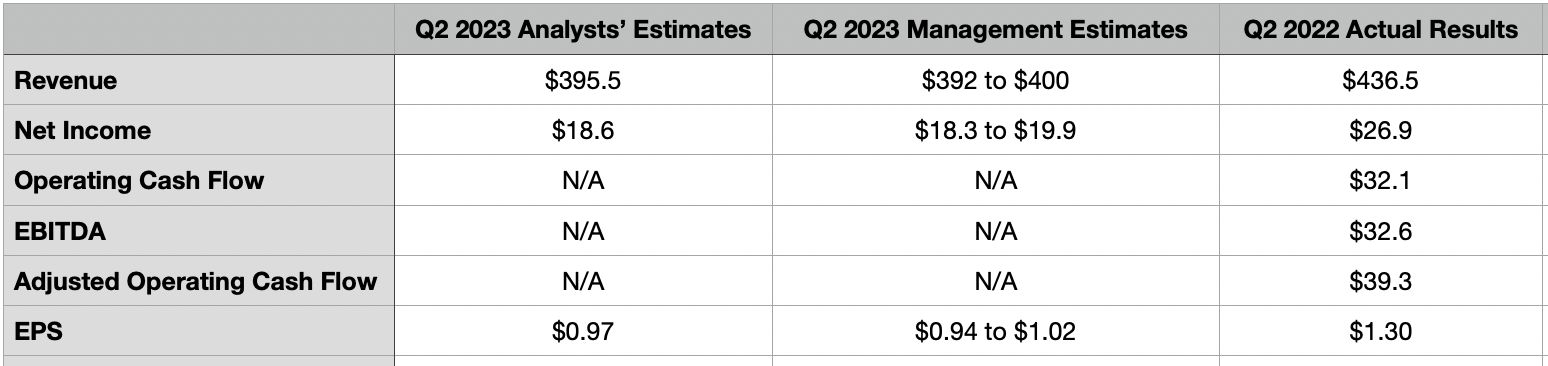

Management has provided some guidance when it comes to the second quarter of the year. Just like with the first quarter, revenue is expected to fall. Management is currently forecasting sales of between $392 million and $400 million when the firm announces results after the market closes on July 31. That compares to the $436.5 million the company reported one year earlier. Analysts, meanwhile, believe that sales would be about $395.5 million. Bottom line expectations are also worse year over year. Last year, the company generated net profits of $1.30 per share. Management is currently forecasting profits per share of between $0.94 and $1.02. At the midpoint, that would imply net profits of $19.1 million. Analysts, meanwhile, are forecasting profits per share of $0.97, or total net income of $18.9 million in all. Estimates have not been provided for other profitability metrics. But in the table above, you can see what the rest of these looked like for the second quarter of 2022. More likely than not, these will also fall year over year.

{kind=link}

Author - BLS.gov Data

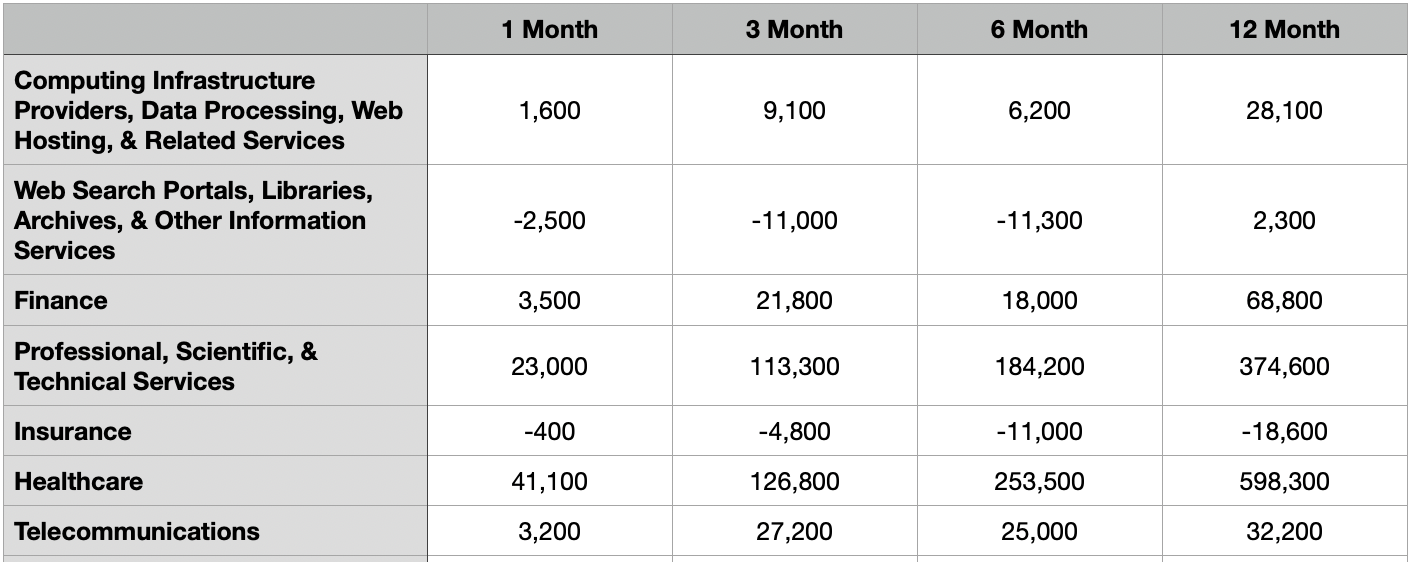

There is some hope that both analysts and management will be incorrect. Recent employment data, for instance, has mostly been encouraging. Using data from June of 2023, the financial activities sector added about 3,500 jobs. The professional, scientific, and technical services sector added 23,000, while the computing infrastructure providers, data processing, web hosting, and related services sector added 1,600. The only weakness involved the web search portals, libraries, archives, and other information services sector, with a decline of 2,500 jobs. You can likely tell that these sectors don’t perfectly match the breakdown of solutions provided by Kforce, but I tried to match up services it provides as much as possible with what the employment data shows. The firm also does provide services for customers in the insurance, healthcare, and telecommunications industries. With the exception of the insurance side of the picture, these sectors showed positive results for the most recent month shown. As you can see in the table above, I also looked at data for the past three months, the past six months, and the past year. For the most part, the overall picture for these areas have been promising. Of course, it's important to keep in mind that the Federal Reserve is intent on pulling jobs out of the economy in order to combat inflation. So this picture could change. But at the moment, it still remains decent.

{kind=link}

Author - SEC EDGAR Data

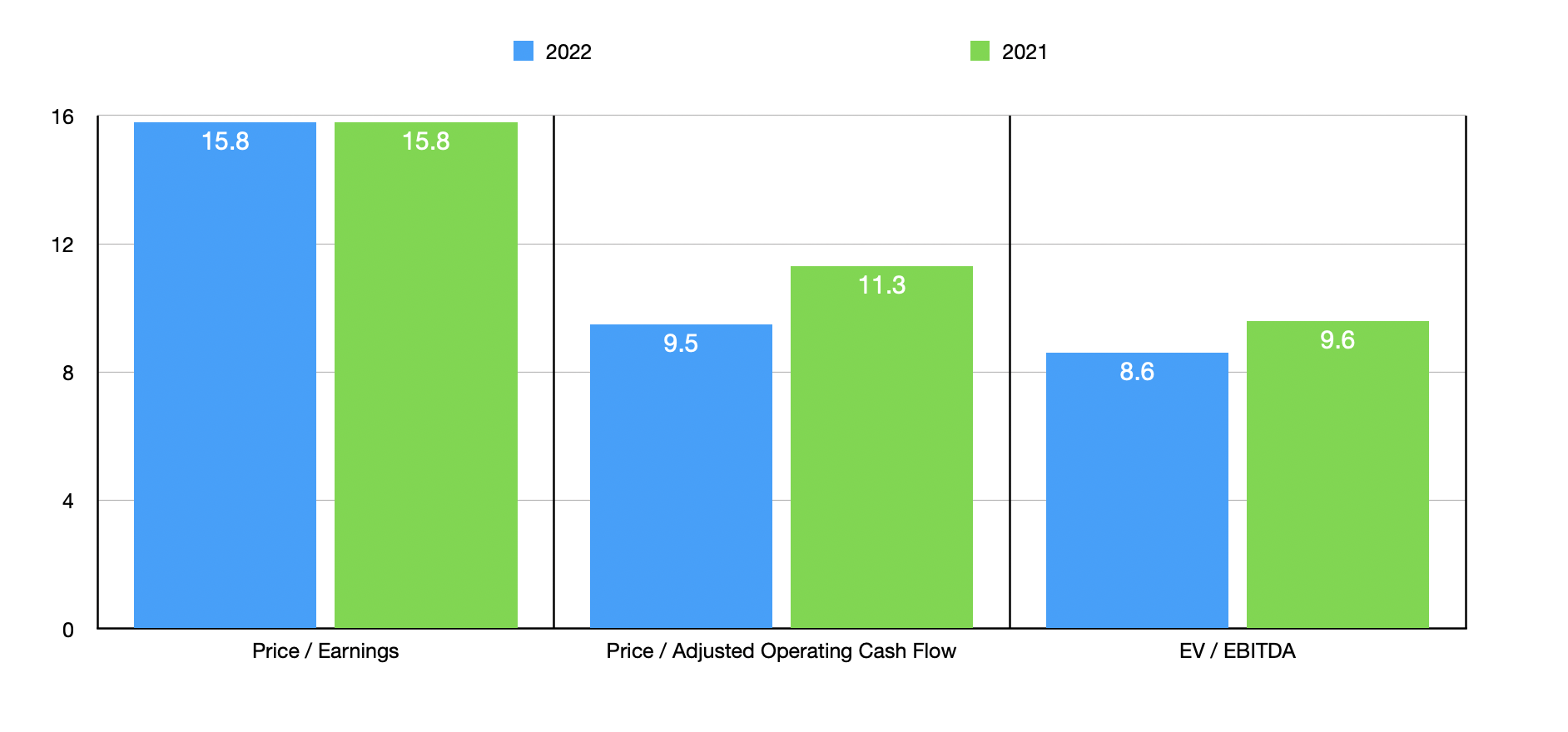

When it comes to valuation, shares of Kforce remain attractively priced. In the chart above, you can see how the stock is priced using data from both 2021 and 2022. Using the 2022 figures, I then compared the company to five similar firms in the table below. Using the price to earnings approach, three of the five companies ended up being cheaper than it. When it came to the price to operating cash flow approach, this number dropped to two. And when you look at the EV to EBITDA approach, two companies were cheaper, while another was tied with it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Kforce |

| 15.8 |

| 9.5 |

| 8.6 |

| Insperity ( NSP ) |

| 21.6 |

| 13.4 |

| 12.3 |

| ManpowerGroup ( MAN ) |

| 11.5 |

| 8.7 |

| 6.3 |

| TriNet ( TNET ) |

| 16.5 |

| 21.0 |

| 8.6 |

| ASGN Inc. ( ASGN ) |

| 15.0 |

| 11.3 |

| 9.5 |

| Korn Ferry ( KFY ) |

| 12.6 |

| 7.5 |

| 5.3 |

Takeaway

Based on the data provided, I understand why the market might be a bit cautious when it comes to a company like Kforce. I definitely think that more caution is warranted based on recent financial results and expectations for the second quarter of this year. Current employment data suggests to me that the picture might not be as bad as feared. But even so, there's no telling what the picture might look like as time progresses. The stock is fairly attractive at this moment. But relative to similar firms, it looks fairly valued to me. All of these facts combined lead me to feel as though downgrading the firm from a ‘buy’ to a ‘hold’ would be prudent at this time.

For further details see:

Kforce Q2 2023 Earnings Preview: Taking A More Cautious Approach