KMB - Kimberly-Clark: What To Look For In Upcoming Earnings And Why Problems Persist

2024-01-10 13:56:43 ET

Summary

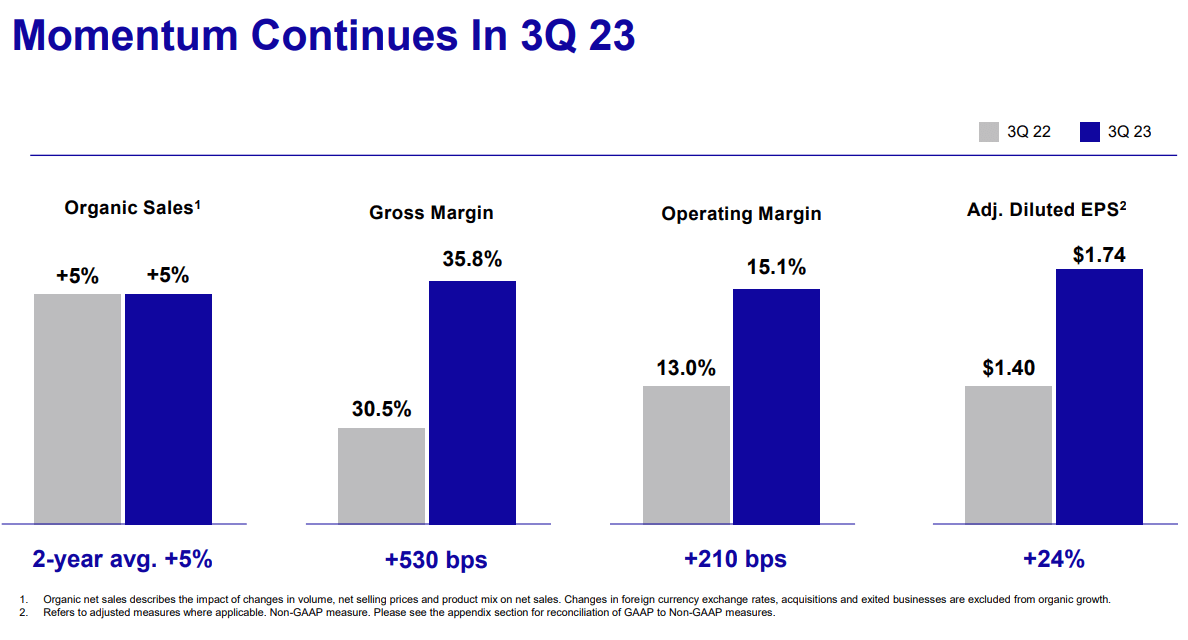

- Kimberly-Clark Corporation continued to underperform the sector even as its margins skyrocketed in 2023.

- I explain why the market has not rewarded the company with higher multiple over the past year, in spite of the progress made.

- The company is still poorly positioned against its peers, and recent capital allocation decisions have done little to change that.

After years of being bearish on Kimberly-Clark Corporation ( KMB ) stock, last year I turned somewhat neutral on the back of macroeconomic tailwinds and easing of commodity prices.

Over the course of 2023, I expected margin improvements within the company, and yet there were some important risks that were likely to continue to weigh on the share price. Few months later, KMB has indeed delivered higher margins, but the share price continues to lag behind other peers in the consumer staples space.

Now that we are two weeks away from the company's announcing its full year results ( expected January 24th), I would like to highlight some key areas that investors should be focused on. I would also explain why the recent margin improvements were not sufficient to propel KMB share price higher and instead things have only gotten worse in 2023.

Where Is Return Coming From?

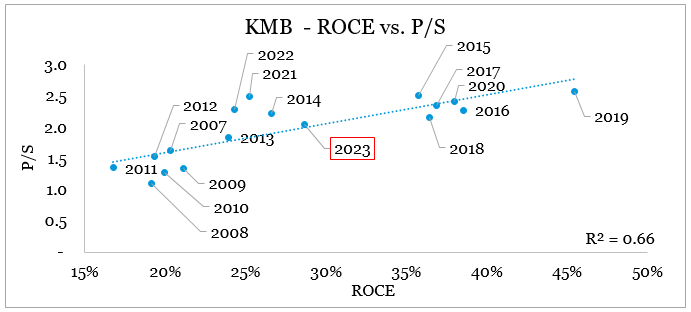

Sustainability of return on capital employed is the key metric to focus on when it comes to assessing Kimberly-Clark's competitiveness and the potential for a multiple repricing. As we see from the graph below, over the long-run, ROCE exhibits a relatively strong relationship with the stock's price/sales multiple.

prepared by the author, using data SEC Filings and Seeking Alpha

{kind=link}

As of the end of third quarter of 2023 (the last reported one) and based on the current share price, KMB trades at a price/sales multiple that is in-line with the company's return on capital employed.

When we compare the current period to the FY 2022 on the graph above, we could get an idea of why KMB continued to underperform, in spite of the improving ROCE on the back of the company's higher margins in 2023. The reason is that in 2022, KMB was trading at a much higher sales multiple to what the company's ROCE was suggesting, as the market was expecting a very large improvement in margins that did not materialize.

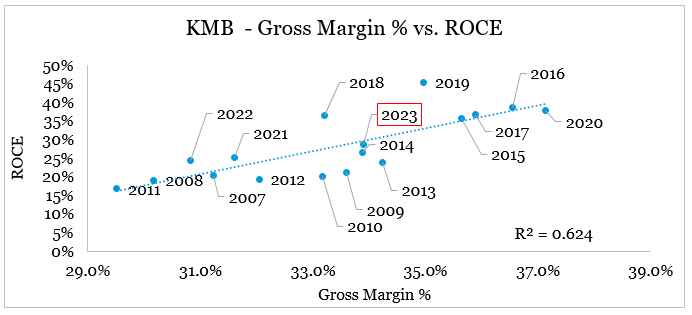

When we plot a similar graph to the one above, but instead with KMB's gross margin on the x-axis and its ROCE on the y-axis, we could see that gross profitability is one of the key drivers of the company's return on capital.

prepared by the author, using data SEC Filings and Seeking Alpha

{kind=link}

Although the gross margin improving from 31% in FY 2022 to nearly 34% for the past 12-month period is very impressive, at this point in time it appears that the company is essentially done with any pricing initiatives. Instead, the management relies heavily on volumes improving going forward as price increases have come to an end.

We expect volume trends to continue improving as we cycle prior pricing actions and continue to invest in our brands. We also continue to make excellent progress on margin recovery. (...)

We're not ready to call '24 yet but I think volume -- we cycled most of our big pricing actions from last year. And so we would expect volume trends to continue to improve as we drive our commercial programs and invest behind our brands.

Source: KMB Q3 2023 Earnings Transcript (emphasis added).

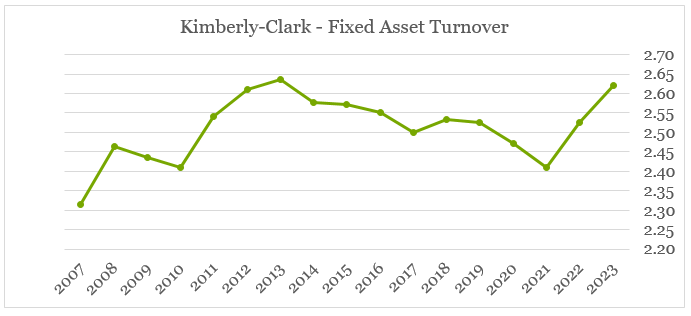

This is likely to have a dampening effect on the company's gross margin and should instead drive higher asset turnover. At the moment, Kimberly-Clark's fixed asset turnover is already at record highs, which makes me skeptical of any meaningful improvements based on further volume increases in FY 2024.

{kind=link}

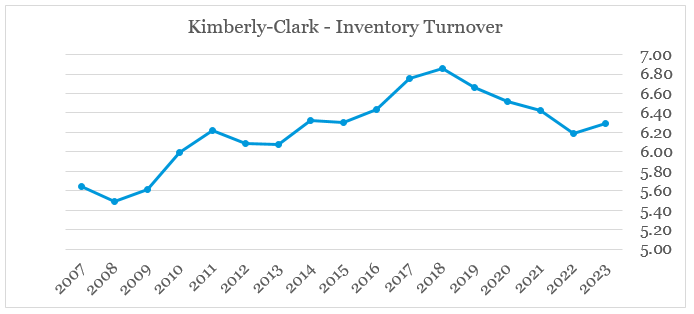

Inventory turnover is an area that investors should keep a close eye on during the current year, as higher volumes should also translate into higher turnover of inventories.

{kind=link}

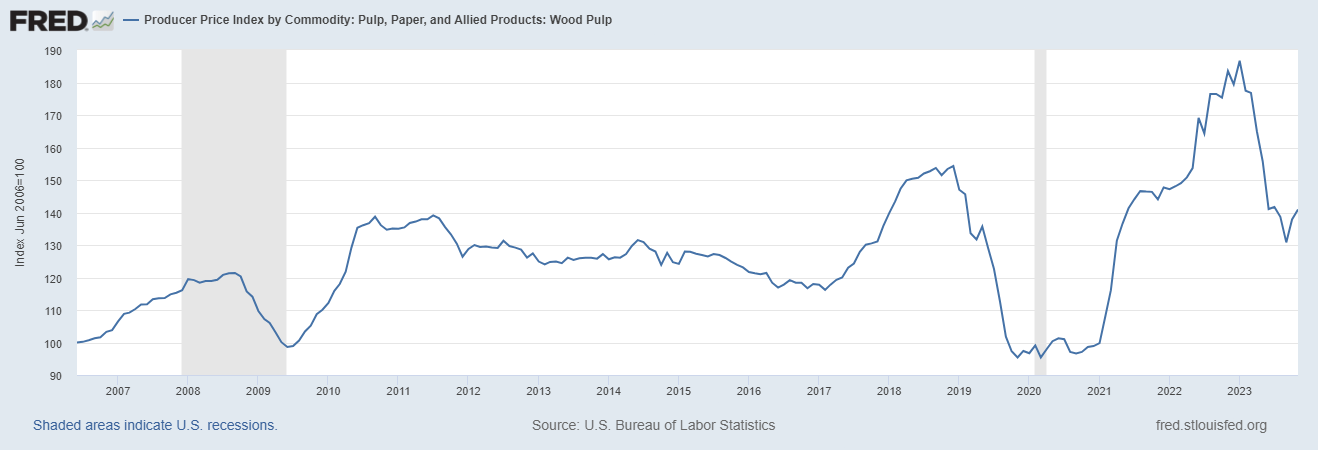

Last but not least, during 2023 KMB benefited heavily from the cool-off in commodity prices which helped the company achieve the gross margin improvement we saw above.

{kind=link}

In Q4 of 2023, costs are still expected to be a tailwind and it appears that this trend could continue in the short-term.

And so in the quarter -- so our first quarter were -- the costs actually were favorable . And so that's a significant inflection point for us. I do expect input cost to be a modest tailwind going forward but don't expect necessarily that there's going to be a lot that's come behind that.

Source: KMB Q3 2023 Earnings Transcript (emphasis added).

It also appears that the falling commodity prices had a much stronger impact on margins than the combined impact of KMB's pricing initiatives and volume growth. That is why, we saw a very modest improvement in organic sales, while margins skyrocketed.

{kind=link}

Therefore, should commodity prices remain favorable, KMB shareholders could enjoy strong returns in 2024, but in my view this hardly justifies a bullish investment thesis for the company. On top of that, KMB continues to have significant problems when it comes to capital allocation.

Doubtful Decisions On Capital Allocation

During 2023, it became clear that one of the largest recent acquisitions for Kimberly-Clark - the one for Softex Indonesia business in 2020 - has now resulted in shareholder value destruction.

At the time, when hype around pandemic-induced demand was running high, the target company was called a leader in the fast-growing Indonesian personal care market.

{kind=link}

But only three years later, KMB has already impaired the vast majority of the acquired intangible assets - notably brands, distributor and customer relationships.

In the second quarter of 2023, we conducted forecasting and strategic reviews and integration assessments of our Softex Indonesia business, acquired in the fourth quarter of 2020 , and with performance below expectations since acquisition, we revised internal financial projections of the business to reflect updated expectations of future financial performance. (...)

These intangible assets were recorded as part of the Personal Care business segment and included indefinite-lived and finite-lived brands and finite-lived distributor and customer relationships . As a result of the interim impairment assessments, we recognized impairment charges, principally arising from the impairment charge of $593 related to the Softex business (...)

Source: Kimberly-Clark Q3 2023 10-Q SEC Filing (emphasis added).

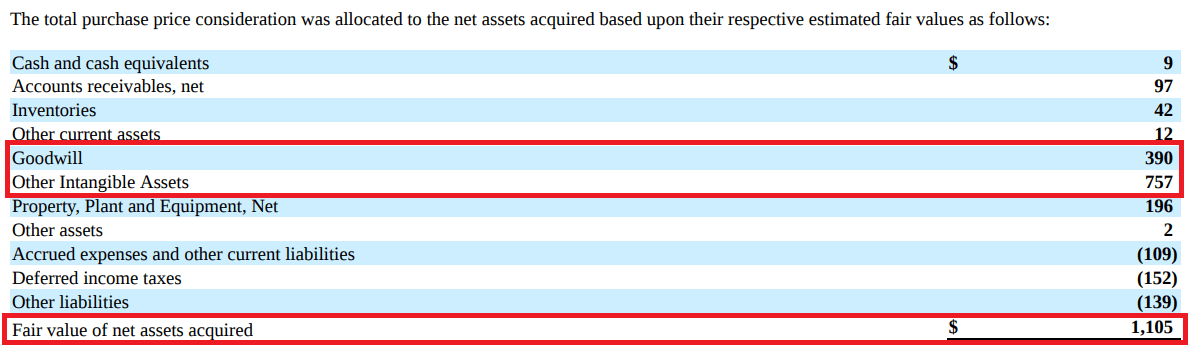

To get an idea of the scale of this impairment, down below is an extract from the purchase price allocation reported in KMB's 2020 annual report. We could see that the current impairment represents roughly half both of the acquired intangible assets and goodwill and total fair value of net assets acquired.

{kind=link}

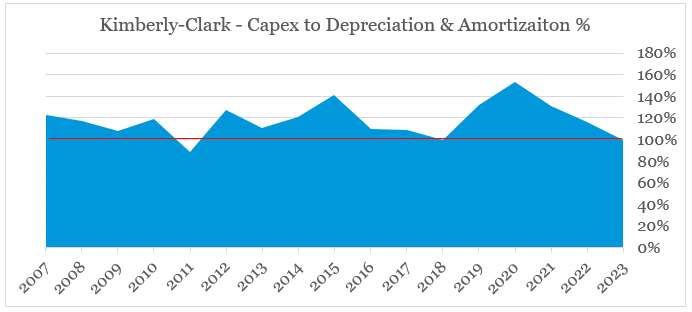

This is significant for such a large deal and in my view is a major red flag when it comes to long-term capital allocation at KMB. Even when it comes to internal growth, the company's capital expenditure is already below the annual depreciation and amortization expense which signals a lack of growth opportunities.

{kind=link}

Conclusion

In a nutshell, the macroeconomic environment would likely be supportive for Kimberly-Clark's business in 2024, and that business is in a good position to at least retain its higher margins. Investors, however, should keep in mind that the business has not changed dramatically in recent years and is heavily reliant on commodity prices continuing to fall. To make matters worse, in 2023 it became clear that the management is not making the right decisions when it comes to long-term capital allocation.

For further details see:

Kimberly-Clark: What To Look For In Upcoming Earnings And Why Problems Persist