KIM - Kimco Is Attractive For Income Seeking Investors

2023-10-30 05:15:58 ET

Summary

- Kimco's stock has lost 18% of its value in the past year, but the company has been raising its dividend.

- The increase in interest rates has negatively affected real estate stocks, but Kimco remains attractive for dividend-oriented investors.

- Kimco reported strong Q3 results, with solid same-store net operating income and a high occupancy rate.

Shares of Kimco ( KIM ) have had a challenging twelve months, losing about 18% of their value. Since I recommended shares last October , they have returned a disappointing -10%. As I expected, the company has been raising its dividend, up from $0.22 to $0.24 with another penny increase possible in the next two quarters. However, the larger-than-expected increase in interest rates has been a more meaningful drag on real estate stocks and valuations, outweighing the dividend. However, after examining its Q3 results, KIM still is an attractive stock for dividend-oriented investors, in my view.

{kind=link}

In the company’s third quarter , KIM generated $0.40 of funds from operations (FFO), beating estimates by $0.01. Alongside these results, it tightened full year guidance to $1.56-$1.57 from $1.55-$1.57. Overall, the company reported strong results with same-store net operating income of 2.6%. Kimco gets about 82% of its rent from grocery-anchored shopping centers, which have held up much better than malls, given they are largely open-air and that grocery shopping has proven more resilient to e-commerce trends.

Indeed, grocery sites drive 90bp higher net operating income than non-Grocery locations. During the quarter, occupancy stood at 95.5%, down from 95.8% last quarter. This is up 160b from the end 2020 but still 90bp below 2019, as the company’s operations have largely, but not totally, returned to normal from COVID disruptions. The reason occupancy fell sequentially is that the final Bed Bath & Beyond leases have been vacated, a 37bp drag in the quarter’s occupancy.

While BBBY’s liquidation has been a headwind for occupancy, I view it as a medium-term positive. First, given the company’s struggles, Bed Bath & Beyond was not driving meaningful customer traffic to Kimco’s shopping centers. Bringing in better stores should help the vibrancy of those centers and make other units more leasable. Moreover, BBBY was paying below market rent, given benefits given to it when it was a more powerful anchor. Kimco is capturing a 38% spread on 14 released Bed Bath and Beyond leases; it expects over 20% on the other 12. While the current vacancy is reducing revenue, when these new leases begin at higher rates, we should see a meaningful boost to profits.

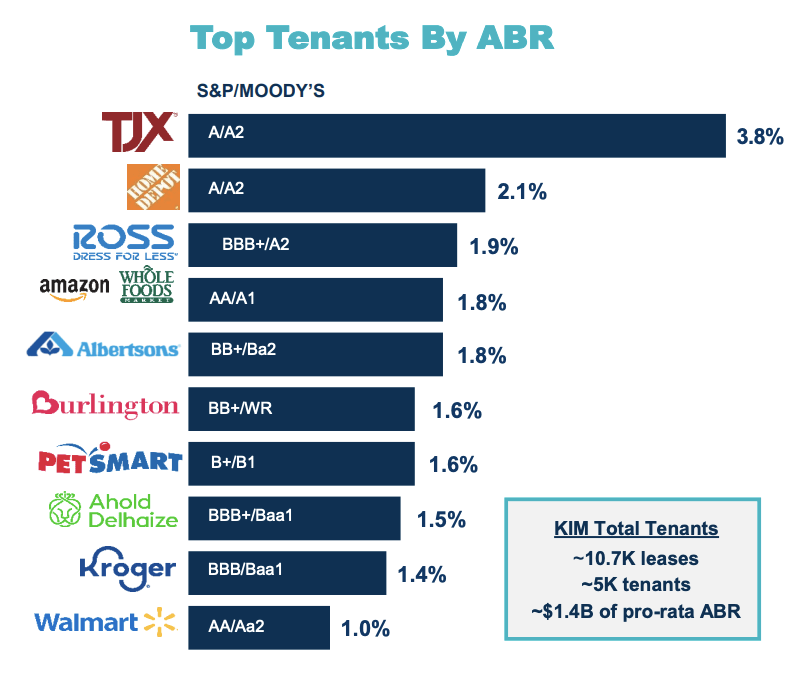

With the BBBY issues clearing through, I would also note that Kimco’s primary tenants are high-quality firms, from Home Depot ( HD ) to Walmart ( WMT ) and Kroger ( KR ). I do not foresee meaningful large tenant bankruptcies over the medium term. Kimco has a well-balanced portfolio with 53% of revenue coming from anchors and 47% from smaller tenants. Its 91.1% small-shop occupancy is back at a record, another sign of post-COVID normalization.

{kind=link}

New leases are providing a 35% uplift to rent levels, with the BBBY releasing playing a significant role in this. However, renewals are also strong with an 8.8% benefit as these rents are brought up to market levels. Kimco has about $52 million of potential growth just from continuing to bring leases up to market levels, a potential $0.07-$0.08 (or 5%) lift to FFO. Again, this is just from gradually bringing rents to where the market is today, not needing any further improvement. As the new leases take effect, rent per square foot rose by 1% sequentially to $20.19.

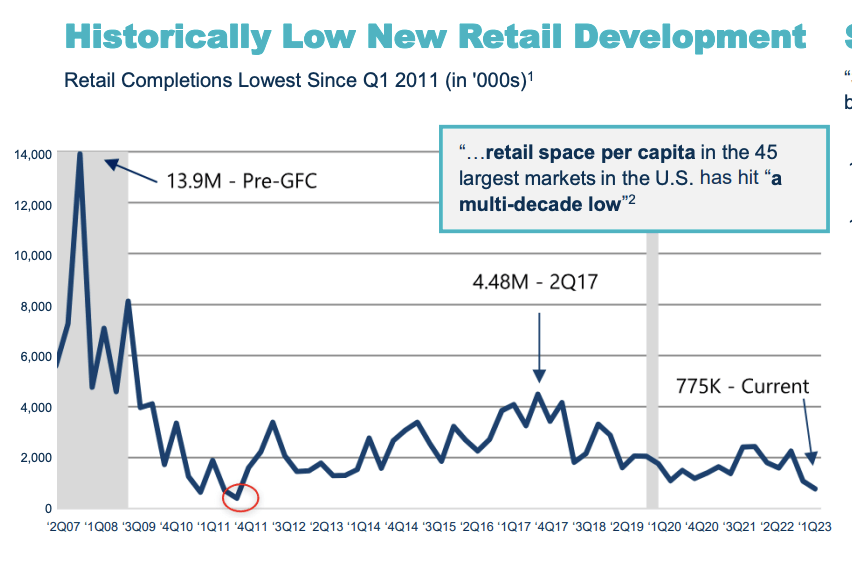

A major reason why KIM is seeing strong leasing activity is because the overwhelming consensus on retail real estate has been so negative. Let me explain what I mean by that. Prices are set by supply & demand. Because there has been widespread concern about retail demand over the long-run, few have been willing to invest in new supply. That lack of supply has kept the market tight as demand has held-in better than expected, particularly for grocery-centers, which have much different fundamentals than large, enclosed malls. In fact, retail construction is now running at multi-decade low levels, down over 80% from 2017.

{kind=link}

If a retailer wants to expand, it is not as though there are plenty of new construction sites for it to occupy. It needs to find an available existing site. That is why they are paying up for leases with Kimco seeing strong demand for the BBBY openings. This is also because Kimco operates in high-quality suburbs in the fast-growing Sun Belt and in higher-income enclaves in the Northeast and West Coast, making its locations relatively attractive.

To increase its Sun Belt penetration, it will be closing its purchase of RPT Realty ( RPT ) in 2024, which will be modestly accretive to FFO/share, improving the overall dividend coverage ratio while providing more exposure to fast-growing markets in Florida, like Tampa. Management also expects $34 million of synergies.

Alongside earnings, KIM increased its quarterly dividend to $0.24 from $0.23, giving shares a 5.7% yield. Over time, management targets a mid-70’s% payout ratio—it was 79% in Q3. As it starts getting revenue from new BBBY tenants it should be back towards this target. It also aims to expand 12,000 multifamily units from 9,600 as it builds mixed-used retail/residential centers, providing a bit of diversification to earnings. KIM also targets 6-6.5x debt-to-EBITDA leverage; it is at 5.9x currently.

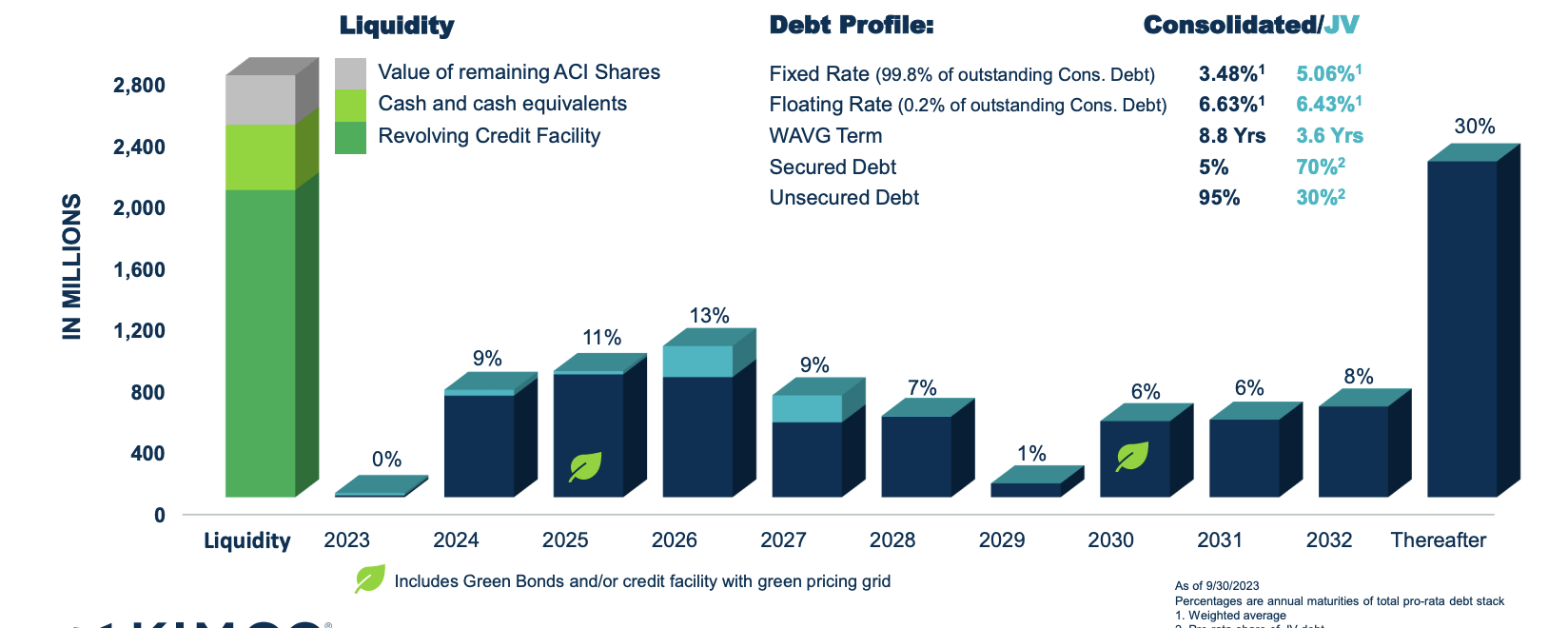

While higher rates weigh on real estate valuations and the attractiveness of dividend stocks, KIM’s business itself is not that negatively impacted by higher rates thanks to the fact leverage is a bit below its long term target. Its debt is also 99.8% fixed rate. 50% of its debt matures in 2030 or later, meaning the amount it will be rolling over at higher rates will only modestly impact interest expense. Finally, management is aiming to be self-funding growth projects as much as possible to limit its need to borrow at elevated rates.

{kind=link}

Overall, Kimco’s business has performed in-line with my expectations. Leasing activity is strong. It is working through BBBY’s bankruptcy, and we are seeing solid same-store income growth. In fact, it raised its full year NOI growth guidance to 1.75-2.25% from 1-2% previously.

Additionally, it has monetized $282 million of its Albertsons' ( ACI ) stake. It still has a remaining 14.2 million share stake worth just over $300 million as of October 27 th . A special dividend will be declared in November to stay within REIT tax compliance.

When Kimco disposes of the rest of its Albertsons’ stake, likely in 2024, there is the potential for a further dividend payment, and those proceeds will help fund growth projects, which is why I do not anticipate it to need incremental borrowings next year. That stake is worth about $0.50/share.

Kimco is trading at just 11x FFO. Its assets are relatively immune from retail pressures, given its grocery-centric position. If rates rise another 100bp, I expect to see all real estate stocks under pressure, as a 5.7% dividend is not as attractive if the 10-year treasury is at 5.5%. However, unlike a bond, these dividends can grow over time. While I do not necessarily see rates falling, it seems that most of the increase has likely occurred. With a 5.7% yield and 3-5% dividend growth prospects, I continue to like Kimco for income-seeking investors, and I would be a buyer here.

For further details see:

Kimco Is Attractive For Income Seeking Investors