KIM - Kimco Realty Corporation: Small Shop Risk Appears Manageable

2023-06-12 08:00:00 ET

Summary

- A recent bank study projects 50,000 retail stores will close over the next five years, with small stores most at risk.

- Small shop leases provide 46% of Kimco Realty's annual revenue.

- We assess the risk to Kimco Realty, and conclude the risk is manageable.

Investment Thesis

Kimco Realty Corporation (KIM) is the largest U.S. publicly traded shopping center REIT. It owns and operates open-air, grocery-anchored shopping centers, concentrated in the dense, high-income, first-ring suburbs of top markets. Smaller footprint leases (Small Shops) provide 46% of KIM's revenue.

A study by Swiss bank UBS Group AG (UBS), reported under dramatic headlines in Retail Dive and elsewhere in April 2023, projects a net reduction of 50,000 retail stores in the U.S. by 2027.

Primarily due to rising e-commerce penetration and restricted credit, these closures would reduce the 940,000 current U.S. retail store count by 5%. Smaller retail establishments are projected to be particular vulnerable.

Based on an assessment of KIM's Small Shop stores, I conclude that the risk to KIM is manageable; my rating for KIM is unchanged.

Introduction

I recently wrote an article assessing Kimco Realty Corporation, Regency Centers (REG), and Federal Realty (FRT), the three largest shopping center REITs.

One of the comments to that article raised the issue of the potential impact of retail store closures in those centers. The UBS study projects that smaller firms are particularly at risk.

I decided to take a look at KIM's Small Shops in this environment. Although they don't exactly map to the broader retail threat UBS suggests, I believe this analysis provides a useful risk assessment for KIM.

KIM is the primary focus of the article, but REG and FRT are also discussed to provide both context and points of comparison.

KIM, REG, and FRT don't provide quite the same data on their tenants in general or small shop in particular, so the comparisons are imperfect, but useful.

Gross Leasable Area ((GLA)) is measured in thousands ((K)) of square feet ((SF)). Revenue is measured in Annual Base Rent ((ABR)).

Company data is from Q1 2023 Supplementals, Investor Presentations, and Earnings Calls.

We will review the USB study, look in some detail at Small Shops, estimate the impact of the risks UBS raised, look at three Small Shop tenant categories, and wrap up with an investor takeaway.

The UBS Study

UBS predicts that over the next five years, 50,000 net retail stores (ex. gasoline and food service) will close, with the smaller, undercapitalized, and undifferentiated stores most at risk. This study was widely reported; the most detailed report I found includes UBS slides and is here .

The three hardest hit categories - clothing and accessories (14,000 stores closed, 12% of existing stores), consumer electronics (9,000 stores, 20%), and home furnishing (4,000 stores, 9%) - project an average closure rate of 13% and account for 54% of the closures.

Sporting goods (2,400, 10%) and office supplies (2,200, 32%) account for another 9% of closures. Auto parts, home improvement, and retail grocery are projected to see minimal impact.

That's the base case and assumes the recent 4% retail growth rate continues; a protracted US recession might increase closures to 70,000-90,000.

The base case appears to be roughly half the impact of the 2008-2009 Great Financial Crisis, but significantly more severe than the COVID related closures during 2020.

There is a long term trend toward larger retail chains. From 2007 to 2019, firms with less than 500 employees closed over 40,000 stores, firms with more than 500 employees opened 17,000 stores.

Smaller retail firms, with fewer than 20 employees, account for 57% of total retail stores. Firms with fewer than 500 employees account for 68% of total stores.

E-commerce penetration is projected to increase from 20% currently to 26%, with 25% of online sales fulfilled by retail stores.

The increasing requirement to have the infrastructure (staff and software) to support an omni-channel model - e.g. buy online or in store, pick up in store, ship from store, return to store, and same day delivery adds an additional cost and technology hurdle for small businesses.

Small Shops

We will look at the definition of a Small Shop, occupancy levels, contribution to ABR, distribution of ABR by tenant category, and who occupies the shops.

Small Shop vs. Anchor

KIM, REG, and FRT all distinguish between an Anchor and a Small Shop lease on the basis of size. All three define a "small shop" lease as < 10K SF, and an anchor lease as >= 10K SF.

To provide a sense of scale, the average size of KIM's shopping centers is 171K SF. Big box "category killer" and warehouse store tenants occupy about 110K SF. Major grocers are typically 50-60K SF. Banks are 4K SF, fast food/quick service restaurants 2-4K SF, phone stores 2K SF.

A KIM shopping center has 20 leases on average. A single shopping center might have one or more anchors and two dozen small shops, but there is considerable variation. See for example this 492K SF shopping center, anchored by a 128K SF HEB grocery (private), with 6 junior anchors and 48 Small Shops.

Note that a small footprint lease (i.e. a Small Shop in this discussion) may be held by a very large corporation or a single location family owned firm.

Small Shop Occupancy

Occupancy is 4-7% lower for small shops than anchors for all three REITs. The variance among these REITs is 2.1%, with KIM in the middle.

Occupancy Q1 2023 (Company data, Table by author.)

KIM total occupancy in Q1 was 95.8%, just below the 96.4% all time high. Occupancy is probably approaching practical sustainable limits.

The relatively small differences in results for both Small Shop and Anchor among all three REITs suggest that they all have effective leasing operations, and that dramatic gains are unlikely.

KIM has per the 2023 Q1 Supplemental approximately 10,700 leases to 4,900 tenants. About 85% of leases are Small Shop, with hundreds of leases expiring every quarter. Management is essentially deluged with current market feedback.

Small Shop Contribution to ABR

Small Shops are important to ABR. As a rough rule-of-thumb, Small Shops contribute about half of total ABR for these shopping center REITs; it's 46% for KIM, 56% for REG, 40% for FRT.

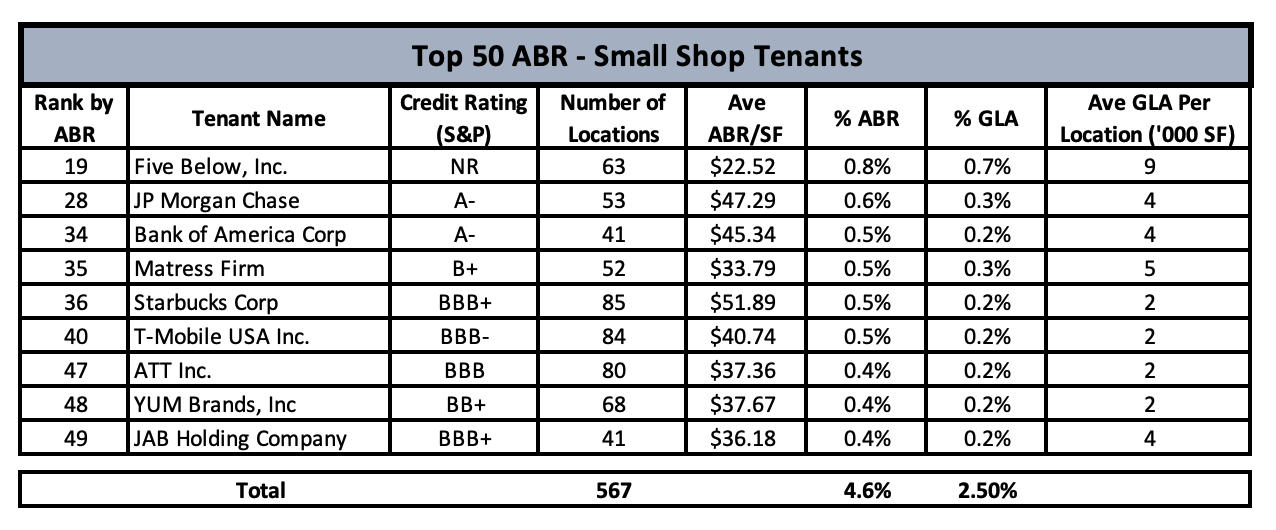

There are nine Small Shop tenants among KIM's Top 50 Tenants by ABR; the Q1 Supplemental provides some additional data. The credit ratings of these more important Small Shop tenants are fairly strong. These nine tenants generate 4.6% of ABR from 2.5% of GLA, i.e. a 1.8 ABR/GLA ratio.

Small Shop Tenants in KIM's Top 50 by ABR (Data from KIM Q1 Supplemental, table by author.)

{kind=link}

By comparison, the top 25 tenants average $13.66 ABR/SF, and 34K SF per location. As a group the top 25 generate 31% of ABR from 42% of GLA, a 0.74 ABR/GLA ratio.

Distribution of ABR By Category

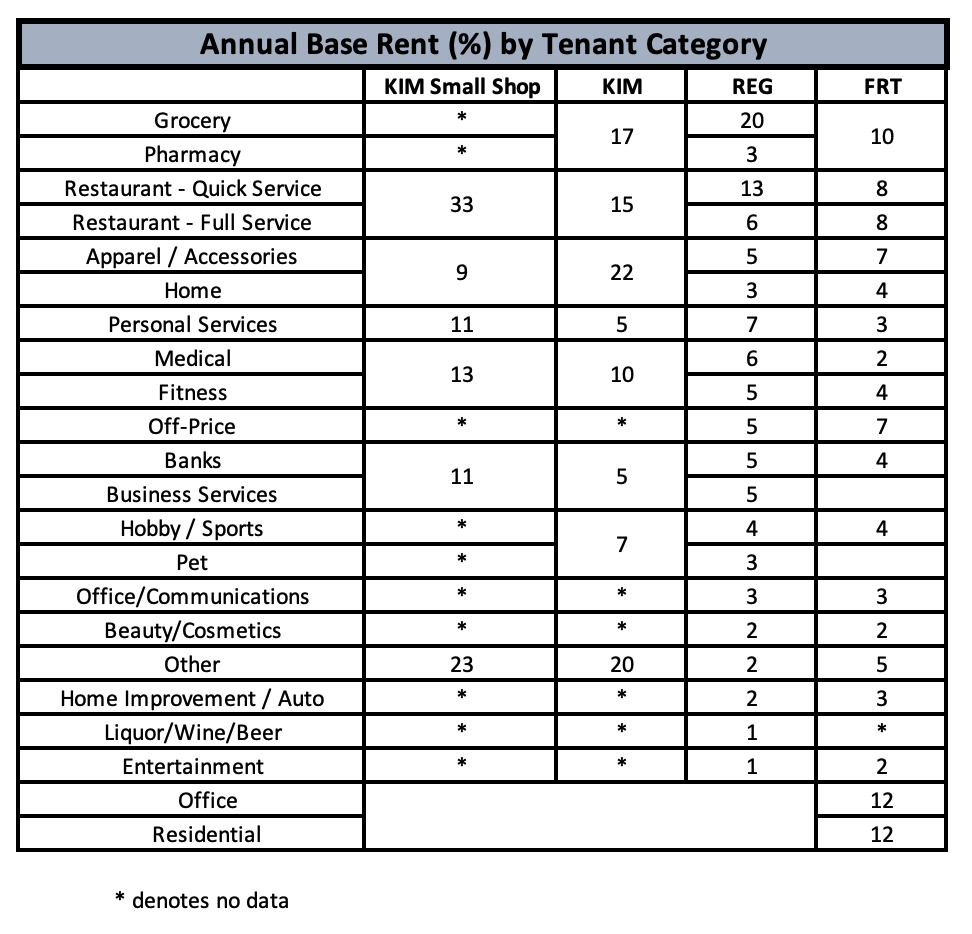

The table below shows the distribution of ABR by category. It includes the distribution for the total portfolio (both Small Shop and Anchor) for KIM, REG, and FRT, and the KIM Small Shop portfolio. The level of detail reported differs a bit between REITs and is reflected in the structure of the table.

{kind=link}

What's In KIM Small Shops

KIM presents two views of their Small Shop tenants.

First, they provide a six bucket breakdown of Small Shop ABR by categories; restaurants are 33%, medical/fitness 13%, personal services 11%, banks/business services 11%, and home/apparel/accessories 9%, with 23% classified as other.

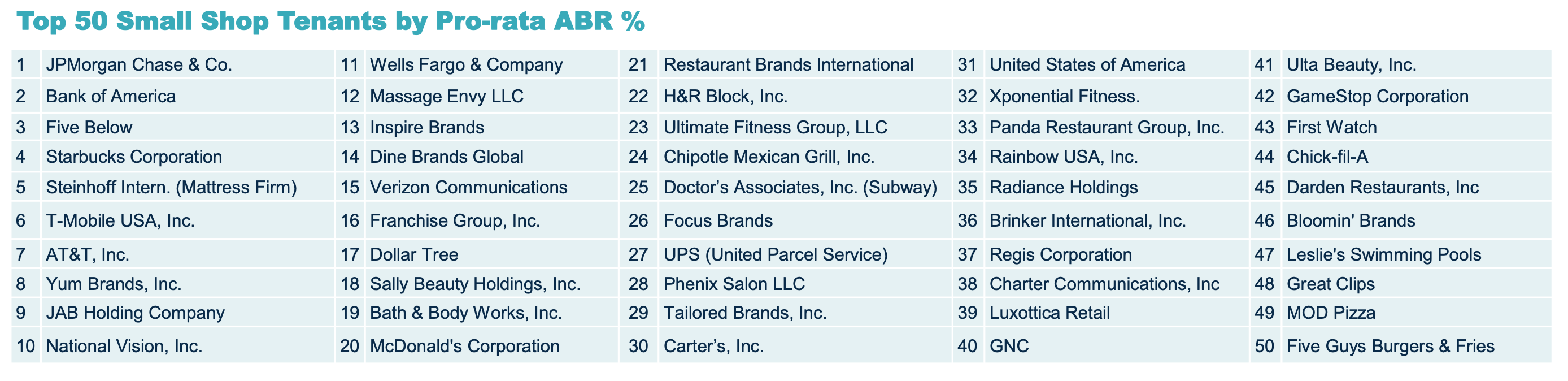

Second, they provide a list of the Top 50 Small Shop Tenants by ABR. These 50 firms are all national brands, and account for 2000+ stores, 27% of Small Shop ABR, and 13% of Portfolio ABR.

KIM Small Shop Top 50 Tenants (KIM Q1 Investor Presentation)

{kind=link}

Local Tenants

KIM also provides the split of ABR between national/regional (78%) and local (22%) tenants. Note that this split is for the total KIM portfolio, but we also know that none of the local tenants made the Small Shop Top 50 ABR list.

While there will be a few anchor sized locals, a very large percentage of locals are Small Shops, and are smaller firms than the Top 50; almost all the higher risk smaller, undercapitalized, and undifferentiated shops will fall into this category.

KIM provides an eight bucket breakdown of local ABR (i.e. 22% of the total ABR) by categories. Of the local ABR, 73% is from restaurants, medical/fitness, personal services, financial services, groceries, drugs, and hobby/pet. That leaves 9% in the home/apparel/accessories category and 16% in other.

Estimated Impact

Putting this all together, we can make an estimate that UBS's highest risk profile - the smaller small shops (i.e. local) in at risk categories - might be 2-6% of KIM's total ABR, depending on what is in the "other" category.

If we use at 15% shop closure rate for the 5 year period (see the UBS study above), that suggests KIM might lose ~ 1% of ABR over that period.

Let's look at some additional data to see if this looks reasonable.

Selected Categories

We will look a bit deeper into a sample of three tenant categories - restaurants, consumer electronics, and banks.

Restaurants

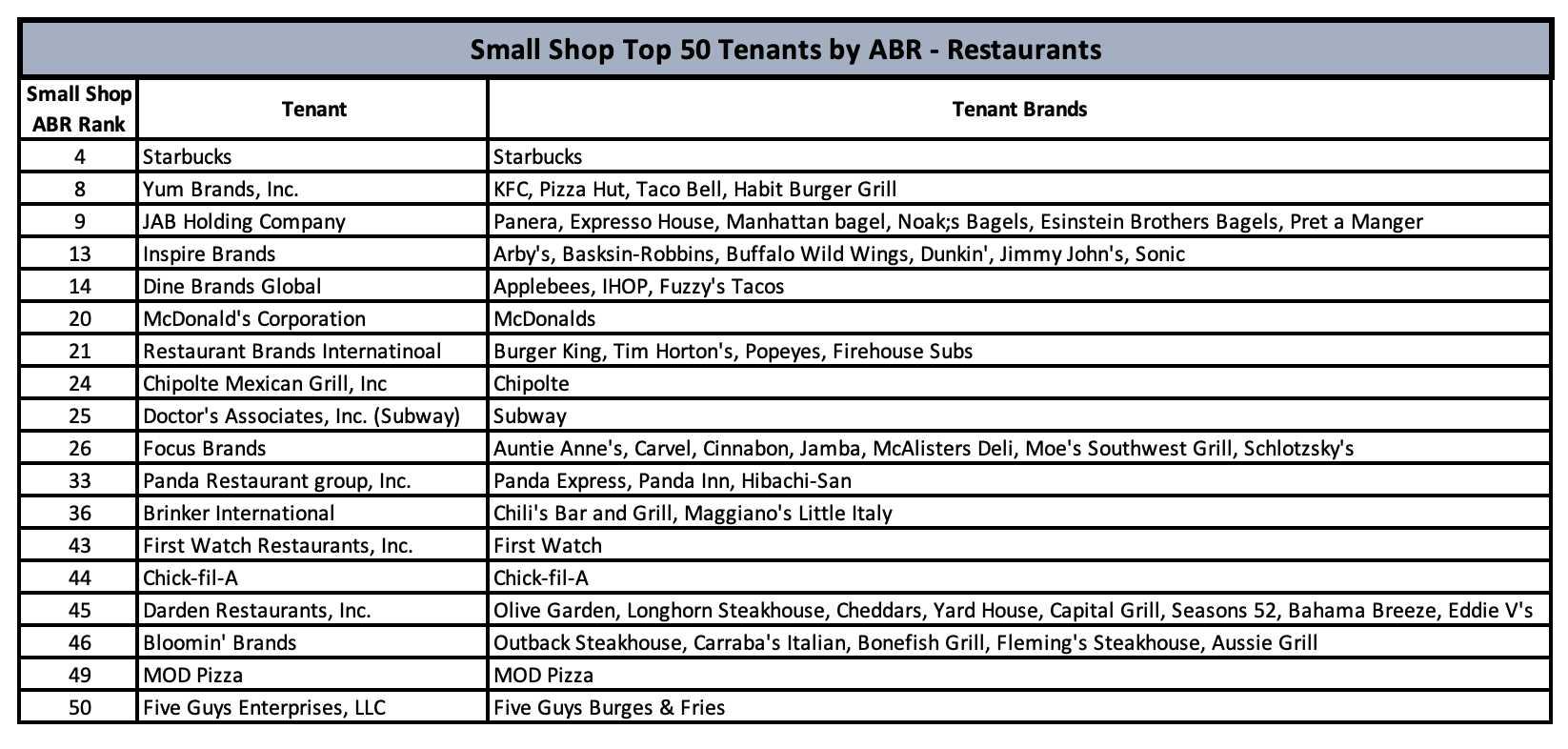

Restaurants are the largest category in KIM's Small Shops, providing 33% of Small Shop ABR.

There are 18 restaurant tenants in the Small Shop Top 50. I've added the brands these tenants operate in the table below (not all brands may be active in KIM properties).

KIM Small Shop Restaurants (KIM Q1 2023 Investor Presentation, company websites. Table by author.)

{kind=link}

Restaurants also make up a significant fraction of Small Shops for REG and FRT.

Overall REG gets 19% of ABR from restaurants, a bit more than KIM.

REG provides a list of Top 30 Tenants by ABR. These include only two restaurants tenants: are #14 Starbucks (NASDAQ: SBUX ), 87 stores with 0.8% ABR, and #17 JAB Holdings (private), 60 stores with 0.7%.

FRT has only one restaurant in the Top 25 Tenants by ABR; # 23 Starbucks, 41 stores with 0.58% ABR.

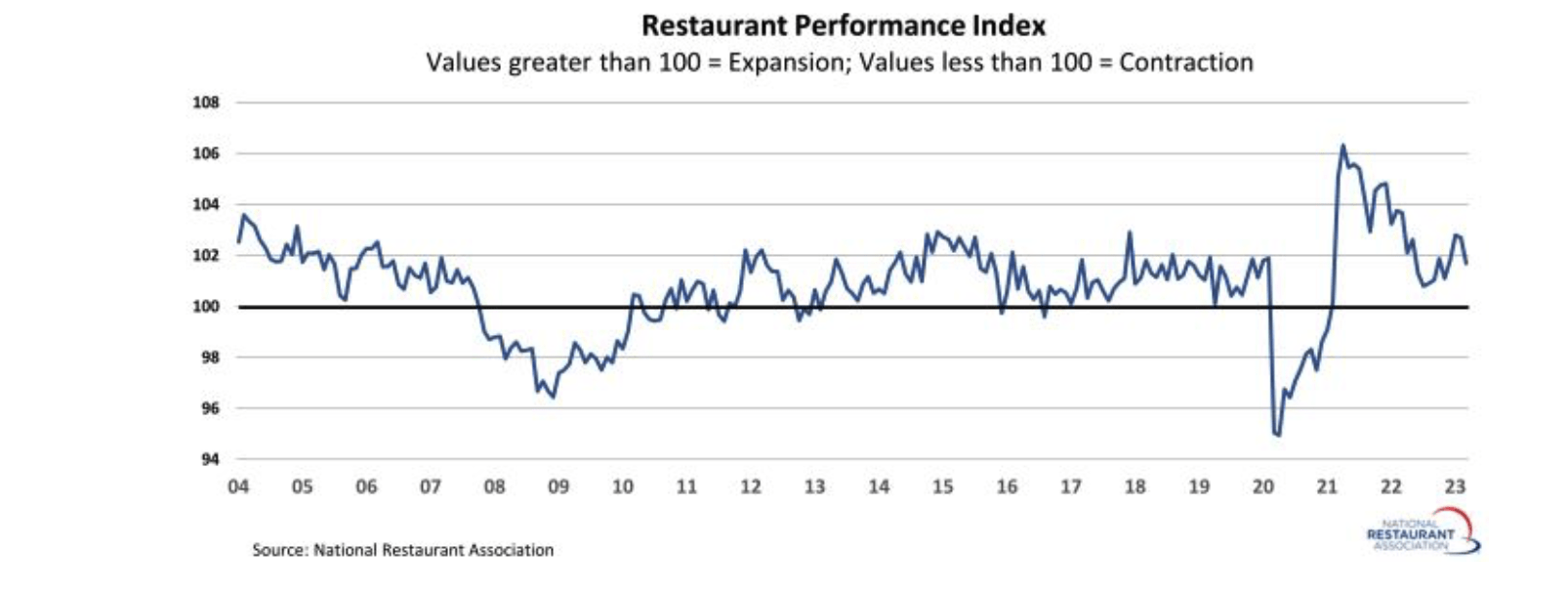

The National Restaurant Association (NRA) maintains a Restaurant Performance Index compiled from survey data. It includes both Current and Expected (6 months forward) information. This provides a useful comparison to both the Great Financial Crisis in 2008-2009, and Covid impact. Note that the impact of COVID restrictions was more severe than the financial crisis.

Restaurant Performance Index (National Restaurant Association)

{kind=link}

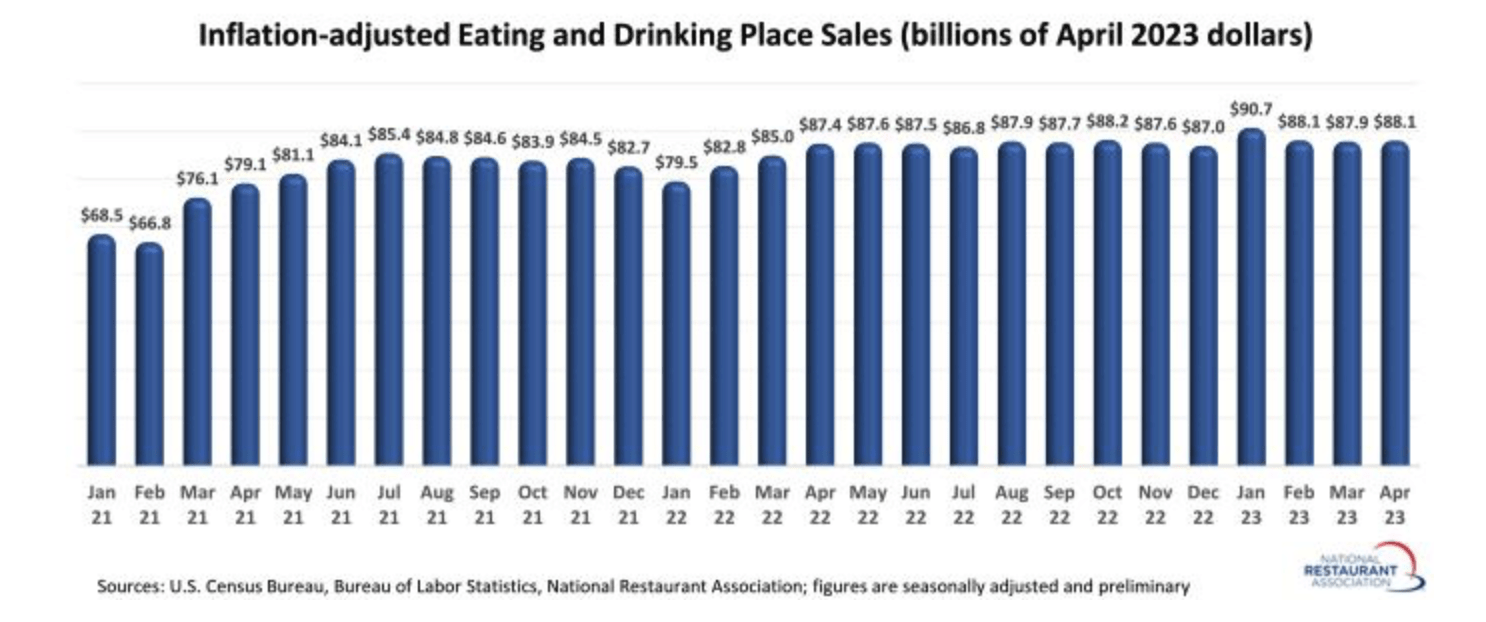

The NRA also provides data on inflation adjusted sales, noting that "April represented the 14th time in the last 15 months that restaurant sales growth outpaced gains in overall retail sales". Sales and traffic data by month for the last year is available here .

{kind=link}

Restaurants are a large part of the Small Shop mix, and absent Covid style restrictions, don't seem to present a particular risk.

Consumer Electronics

The UBS study identified consumer electronics stores as the second hardest hit category, predicting 9,000 store closures.

Based on 2020 data , Amazon (NASDAQ: AMZN ), Best Buy (NYSE: BBY ), Apple (NASDAQ: AAPL ), and Walmart (NYSE: WMT ) are the top 4 consumer electronics retailers by revenue in the U.S. None are Small Shop tenants.

Among these four, I think only Best Buy, with about 1,000 stores in the U.S., presents any real risk, although its currently enjoys a BBB+ credit rating. Best Buy is #15 on KIM's Top 50 Tenants list. With 23 stores, and an average GLA/location of 42K, it contributes 0.9% of ABR.

GameStop (NYSE: GME ) was #12 in consumer electronics revenue in 2020, and currently ranks #42 in KIM's Small Shop list (they don't provide a store count). A May 2023 report shows 2,959 GameStop stores in the U.S. Recent Seeking Alpha articles on GameStop have been quite negative.

All three major phone companies rank in the top 15 in Small Shops, but in aggregate represent only about 1.2% of KIM's total ABR.

Bank Branches

Banks are #1, #2, and #11 in KIM's Small Shop tenant list. They are JPMorgan Chase & Co. (NYSE: JPM ) with 53 locations and 0.6% of total ABR, Bank of America Corp. (NYSE: BAC ) with 41 locations and 0.5% ABR, and Wells Fargo & Company (NYSE: WFC ).

The number of bank branches is declining. The Federal Deposit Insurance Corporation (FDIC) reports that there were 70,875 branches of insured commercial banks in 2022, down 10% from 78,924 in 2017.

One might reasonably expect the gradual reduction in branch banks to continue. However, the banks are attracted to same high density affluent suburbs that attract KIM, so those reductions may fall elsewhere.

Management is Awake to the Issues

Management of the shopping center REITs appears very much aware of the issues facing their tenants, as demonstrated by both investor presentations and questions and comments in earning calls. E-commerce is perhaps the biggest issue.

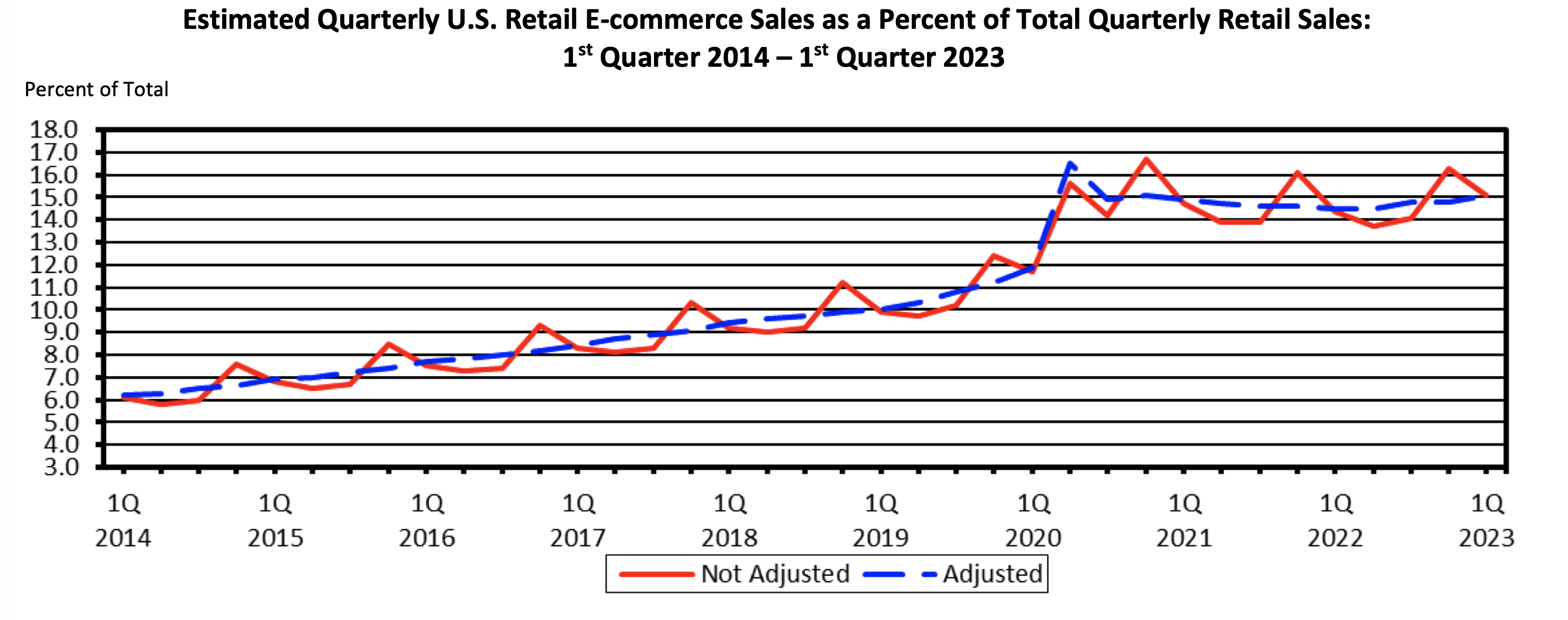

The U.S. Department of Commerce announced 18 May 2023 that Q1 2023 e-commerce sales increased 7.8 percent (±1.6%) from the first quarter of 2022 while total retail sales increased 3.4 percent (±0.4%) in the same period. E-commerce sales in the first quarter of 2023 accounted for 15.1 percent of total sales. (Note that this is a lower number than UBS uses.)

US E-commerce Fraction of Retail Sales (US Department of Commerce)

{kind=link}

In their Q1 2023 Investor Presentation, KIM points out some short to medium term positives for shopping centers, both in space availability and the active response to e-commerce:

- record low supply of new retail space

- near record low number of retail store closures in 2022 and 2023

- the growth of omni-channel including last mile delivery from retail stores

- direct to consumer and traditional mall brands moving to open air shopping centers

- increased use of buy online pick up in store (BOPIS) model, curbside pickup, and work from home

BOPIS is estimated to account for 9.6% of US retail e-commerce sales by 2025, with the primary attraction being same day pickup.

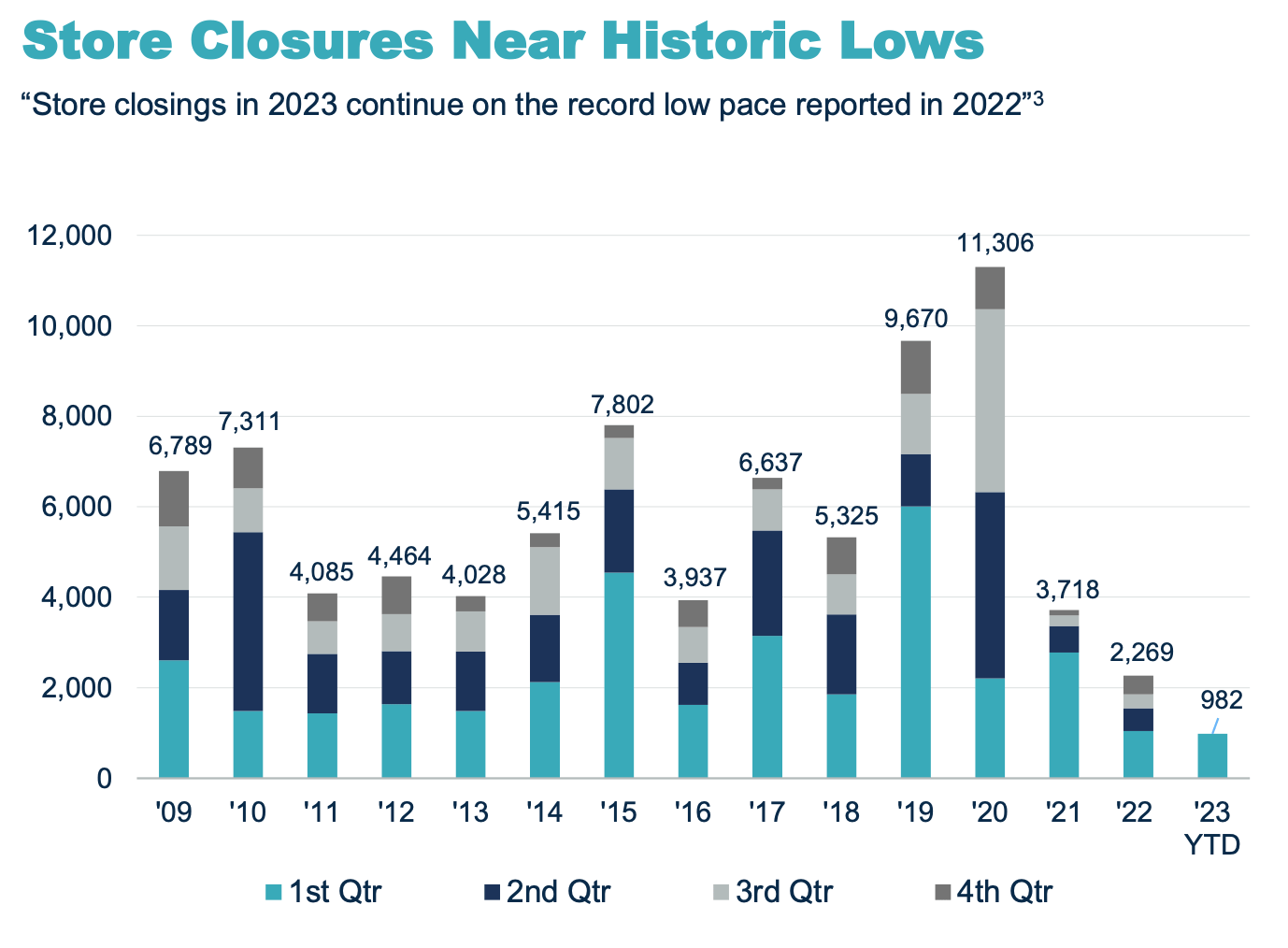

New retail development is the lowest in 13 years, and store closures are at historic lows (I believe this is gross, not net, store closures). UBS reports significant net store adds in 2021.

Record Low Store Closures (KIM Q1 2023 Investor Presentation)

{kind=link}

One observation here is that what one might term the "business as usual" rate - say the 2011 to 2019 period between the GFC and COVID - is about 5,700 store closures per year, i.e. closures are not rare.

Discussion of small shops is routine in earnings calls.

From the KIM Q1 Earnings Call:

The [small] shop space, as you've seen it with our occupancy growth continue to be the bright spot. We can drive a higher small-shop occupancy rate than we've ever experienced before. And again, it's because of that diversity of demand.

Now, it's going to be interesting if the economy really does get worse and there is a pullback. [Post Covid] I think we're starting from a higher-quality, higher credit portfolio of small shops today.

Again from the KIM Q1 Earnings Call:

[Tougher lending standards for small shops] is something that we're very closely monitoring, because we would anticipate that there would be the one that would be most impacted by the pullback of local and regional banks and their ability to lend. Right now we haven't seen a material impact.

FRT provides a slightly different breakdown of local small shops: 35% anchors, 12% mid-tier (5-10K SF), 18% national/regional < 5K SF, 10% local < 5K SF.

From the FRT Q1 2023 Earnings Call :

Meanwhile, small shop occupancy gains continued unabated during the quarter, and increased 50 basis points. That’s a total increase in small shop occupancy of 270 basis points since Q1 2022. The quality of our shop tenants and the discerning way that we choose them at our properties is where we create a ton of value.

We don't do kind of first-time mom-and-pops, we don't have those type of businesses here. They are almost always adding a store or food use from strong cash flow at another location, whereby they're expanding into the third or the fourth or the fifth store.

For the first time in almost two years, we are seeing tenant bankruptcies in retail, as selective businesses struggle to compete in a challenging economic environment of higher interest rates and diminished government subsidies from the pandemic.

Risks

What could go wrong without thesis that the stress on Small Shops predicted by UBS is manageable? I don't see anything that's not been widely discussed.

- A recession might be deeper and longer than expected.

- Interest rates might be higher for longer, with more restrictions on both business and consumer credit.

- Regulatory constraints on business (e.g. COVID style lockdowns, energy use) might occur.

Investor Takeaway

The recent UBS study projects an average annual net closure rate of about 1% for U.S. retail stores over the next five year, with three categories - clothing and accessories, consumer electronics, and home furnishing - accounting for 54% of the 50,000 projected closures. Small, undercapitalized, and undifferentiated stores are particularly at risk.

Small Shop leases are important - they provide 46% of KIM's total ABR, contributing at a significantly higher ABR/SF rate than Anchor tenants.

KIM's 50 top Small Shop tenants (13% of total ABR) are all national firms. Only 22% of KIM's total portfolio ABR is from local firms, and about 75% of this falls in e-commerce resistant categories.

Based on the available data on ABR contributions in total and by category from Small Shops and local firms, we estimate that KIM might lose ~ 1% of ABR over 5 years due to the impacts UBS projects. Even at 2x this estimate, this risk should be manageable.

A review of three categories - restaurants, consumer electronics, and banks - suggests this estimate is reasonable.

The e-commerce risk to brick and mortar retail is well recognized. Both retailers and landlords - particularly shopping centers REITs with premium locations and sophisticated management - are adapting. Businesses that are vulnerable to e-commerce are being actively replaced by those that are resistant - restaurants, personal services, etc. You can't get a haircut online, and while you can order a pizza online, it's actually cooked in a nearby small shop.

This analysis of KIM's small shop portfolio does not change my assessment from a few weeks ago. I still rate KIM a Hold under the Seeking Alpha system. Personally, I retain a full position as a long-term core holding.

For further details see:

Kimco Realty Corporation: Small Shop Risk Appears Manageable