KIM - Kimco Realty: UPREIT And Away

Summary

- Kimco Realty is demonstrating strong operating fundamentals across its high quality portfolio.

- Its new UPREIT structure should provide benefits in its ability to attract sellers.

- KIM stock is attractively valued at present for long-term dividend investors.

Inflation has been on top of mind for many people over the past year, and understandably, quantitative tightening has many investors skittish around stocks.

However, I continue to believe that we are in a temporary lull, and that when all is said and done, investors will want to rotate back into hard assets like real estate and infrastructure, which are among the best positioned for what the future may hold.

This brings me to Kimco Realty ( KIM ), which has a high quality portfolio while remaining at an appealing valuation. In this article, I highlight what makes Kimco a sound buy for long-term dividend investors.

Why KIM?

Kimco Realty is the largest owner and operator of open air shopping centers in North America, with 526 centers spread across the U.S. covering 91 million square feet of gross leasable space. It has a long track record in this industry, having been around for more than 60 years, and having been publicly traded since 1991.

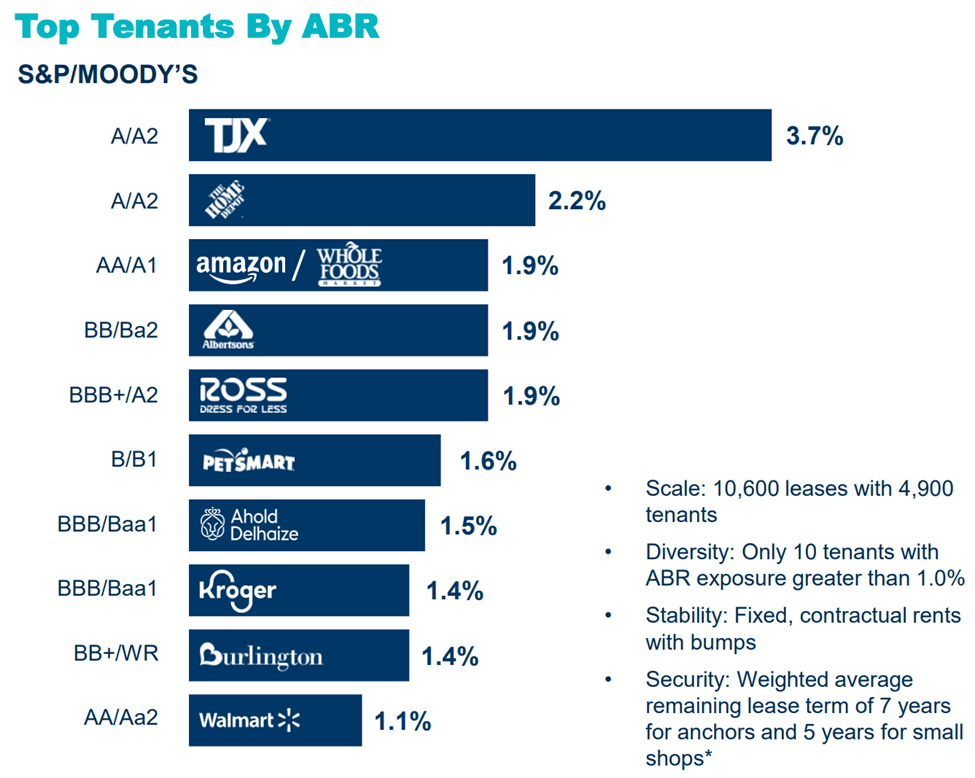

Kimco bills itself as being "first in last mile", reflecting the essential nature of its community centers. This is reflected by the fact that 81% of its annual base rent is derived from grocery anchored centers. Beyond grocers, KIM also leases to highly visible tenant such as TJX ( TJX ), Home Depot ( HD ), and Ross Stores ( ROST ). As shown below, these tenants along with Whole Foods ( AMZN ) and Albertsons ( ACI ) comprise KIM's top 10 tenants.

{kind=link}

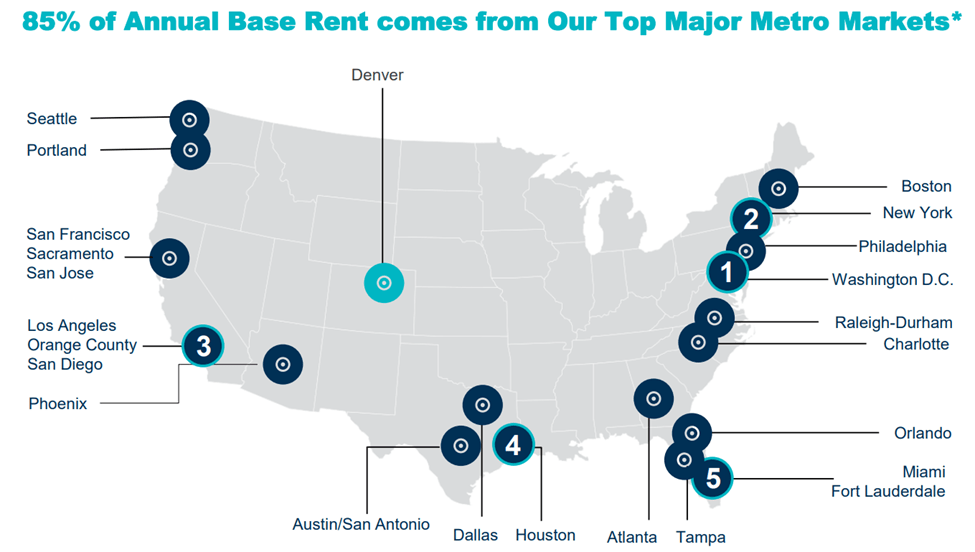

Moreover, 83% of its ABR stems from Coastal and Sunbelt markets, and KIM's coastal markets exceed U.S. median income by 22% and KIM's Sunbelt markets are estimated to see 67% higher population growth over the U.S. average in the next 5 years.

{kind=link}

Meanwhile, KIM continues to see strong tenant demand, as reflected by portfolio occupancy growing by 20 basis points sequentially and 120 bps YoY to a strong 95.3% in the third quarter. Importantly, small shop occupancy sits at 90%, comfortably above the 85% level that's generally considered to be good for shopping center REITs.

In addition, small shops, which come with a higher rent per square foot than that of anchors saw faster occupancy growth at 90 bps sequentially and 190 bps YoY. This contributed to a strong 16.5% rent spread on new leases and contributed to a same property net operating income growth of 3.1% over the prior year period.

Importantly, Kimco carries a strong BBB+ credit rating from S&P, which helps it to secure attractive cost of financing. While its net debt to EBITDA ratio of 6.3x is slightly above the 6.0x level that I prefer to see, it's not surprising considering KIM's ongoing portfolio transformation, which includes adding high value multifamily units onto its mixed use properties, which should drive incremental value on its land.

Moreover, KIM monetized $301 million or roughly one quarter of its Albertson's stake during the fourth quarter and retains 28.3 million shares of Albertsons. As such, this provides a strong backstop in supporting KIM's balance sheet.

Risks to KIM include potential for tenant bankruptcies when certain brands like Bed Bath & Beyond ( BBBY ) fall out of favor with consumers. However, management appears to be on top of the situation as it unravels, as noted during the recent conference call :

In the event we are able to recapture these Bed Bath and Beyond spaces, we have a variety of backfill candidates such as grocers, dominant omni-channel players or off price retailers, many of which have already showed interest in those boxes. With virtually no new supply in over a decade, our strong credit tenants are finding it difficult to meet their new store opening targets and have been aggressively pursuing opportunities.

Another recent development is KIM's decision to reorganize into an UPREIT structure. I see this as being a positive move for future acquisitions. That's because future sellers will have the option to receive operating partnership shares in KIM in a tax-deferred manner that in some ways resemble a 1031 exchange, benefits of which are highlighted by Hoya Capital in a report this week:

While REG is perhaps the "highest quality" retail REIT, valuations appear rich relative to its larger peer KIM - a name that we believe has similar catalysts for an upward valuation re-rating sparked in part by its adoption of the UPREIT structure last month - a format now utilized by most REITs to streamline acquisitions in a tax-deferred manner. The UPREIT structure allows property owners to exchange their property for ownership shares in the REIT in a "like-kind" transfer known as a 721 Exchange - which has similar benefits as the more commonly known 1031 Exchange.

Importantly for dividend investors, KIM currently pays a 4.2% dividend yield that's well covered by a 59% payout ratio based on Q3 FFO per share of $0.41. Lastly, I find KIM to be attractive at the current price of $21.70 with a forward P/FFO of 13.7. This is considering the quality of the enterprise, strong operating fundamentals, and a positive outlook under the new structure. Analysts have a consensus Buy rating with an average price target of $24 .

Investor Takeaway

Kimco Realty is an attractive investment for dividend investors looking to capitalize on high quality retail centers. It is well positioned for growth and boasts strong operating fundamentals, a solid balance sheet, and an attractive 4.2% dividend yield that's well covered by cash flows. It looks poised to benefit from its UPREIT structure, which allows for tax advantages for sellers. For these reasons, I believe KIM is a good stock to consider for long-term dividend investors.

For further details see:

Kimco Realty: UPREIT And Away