TRP:CC - Kinder Morgan Q1 Earnings Preview: What To Watch For

2023-04-17 08:30:35 ET

Summary

- The management team at Kinder Morgan is expected to announce financial results covering the first quarter of the company's 2023 fiscal year in the coming days.

- The current forecast is mixed, but overall guidance for 2023 is promising.

- Given how cheap KMI shares are, the firm does offer investors upside prospects moving forward.

Historically speaking, the traditional energy market is incredibly volatile. While price fluctuations, driven by small imbalances between supply and demand, can cause turmoil in the fossil fuel space. But not every segment of the energy market is like this. One space that actually has a surprising degree of stability is the midstream/pipeline market. Although revenue might fluctuate significantly, bottom line results are largely based on volume, with most companies in the space moving in the direction of minimum volume commitments. As big a fan as I am in this market, I only own stock in one of the players. That firm is not the subject of this article. But one of the companies that is most appealing in this space outside of the one that I own is Kinder Morgan ( KMI ). And the exciting thing for investors is that, in the coming days, the management team at the company is expected to announce financial results covering the first quarter of the company's 2023 fiscal year. Leading up to that point, there are some things that investors should anticipate. But absent anything significantly negative coming out of the woodwork, I can't imagine the company not offering investors enough upside to warrant a solid ‘buy’ rating at this time.

Kinder Morgan headline news and cash flows

Just as is the case with most any company, the initial focus when management reports financial results for the first quarter of the company's 2023 fiscal year after the market closes on April 19th, will be on certain headline news. Revenue is one of these metrics. At present, analysts are forecasting sales of $4.75 billion. If this comes to fruition, it would translate to a rather significant increase compared to the $4.29 billion the company reported only one year earlier. Very likely, any sort of sizable increase would have been driven by a change in energy prices. A growth in total product sold and transported, driven by additional projects coming online, will very likely be the cause of this move higher and will more than offset any impact associated with price changes.

{kind=link}

Author - SEC EDGAR Data

On the bottom line, analysts are forecasting earnings per share of $0.30. This would be only slightly above the $0.29 per share the company reported the same time one year earlier. This would translate to net profits of $677.4 million for the quarter, up from the $667 million in profits generated in the first quarter of 2022. Because of the nature of its operations, Kinder Morgan should not see significant fluctuations on its bottom line based on changes in the energy market.

According to management, about 61% of the forecasted EBDA that the company should generate this year should be from take or pay contracts where the company is entitled to payment regardless of throughput. Another 26% should come from fixed fees that are collected irrespective of commodity prices and that are based, instead, on volume. Collectively, this makes up the lion's share of the firm's bottom line. This structure means that the company has very little exposure to fluctuations in energy markets that could cause it to experience significant disparities between the price at which the product comes to it and the price at which it leaves. That's why bottom line results have the potential to be so stable.

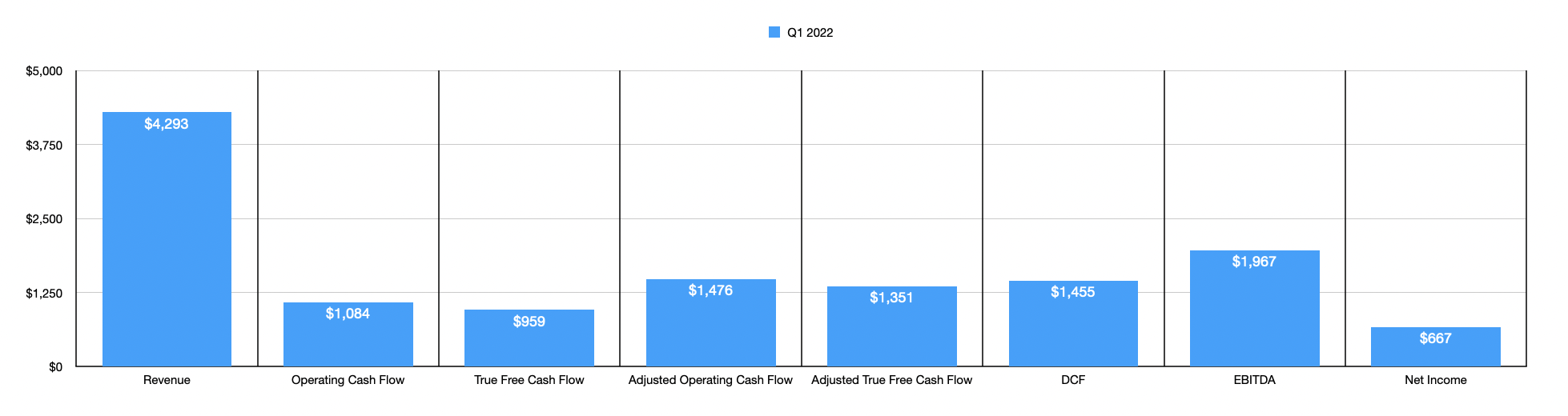

I would make the case that, while net profits are never irrelevant, they aren't the most important metric that investors should be paying attention to. This would be the realm of cash flow data. Analysts have not really provided any guidance on this. But for context, last year during the first quarter, the company generated operating cash flow of $1.08 billion. If we adjust for changes in working capital, the figure would have been higher at $1.48 billion. Meanwhile, EBITDA should be around $1.97 billion. DCF, or distributable cash flow, was $1.46 billion. Another important metric that I like to look at is what I refer to as ‘true free cash flow’. This takes operating cash flow and strips out from it the capital expenditures that are needed in order to keep operations running as they are today. They don't penalize the company for growth capital expenditures. In the first quarter last year, this metric was $959 million, with the adjusted figure for it totaling $1.35 billion.

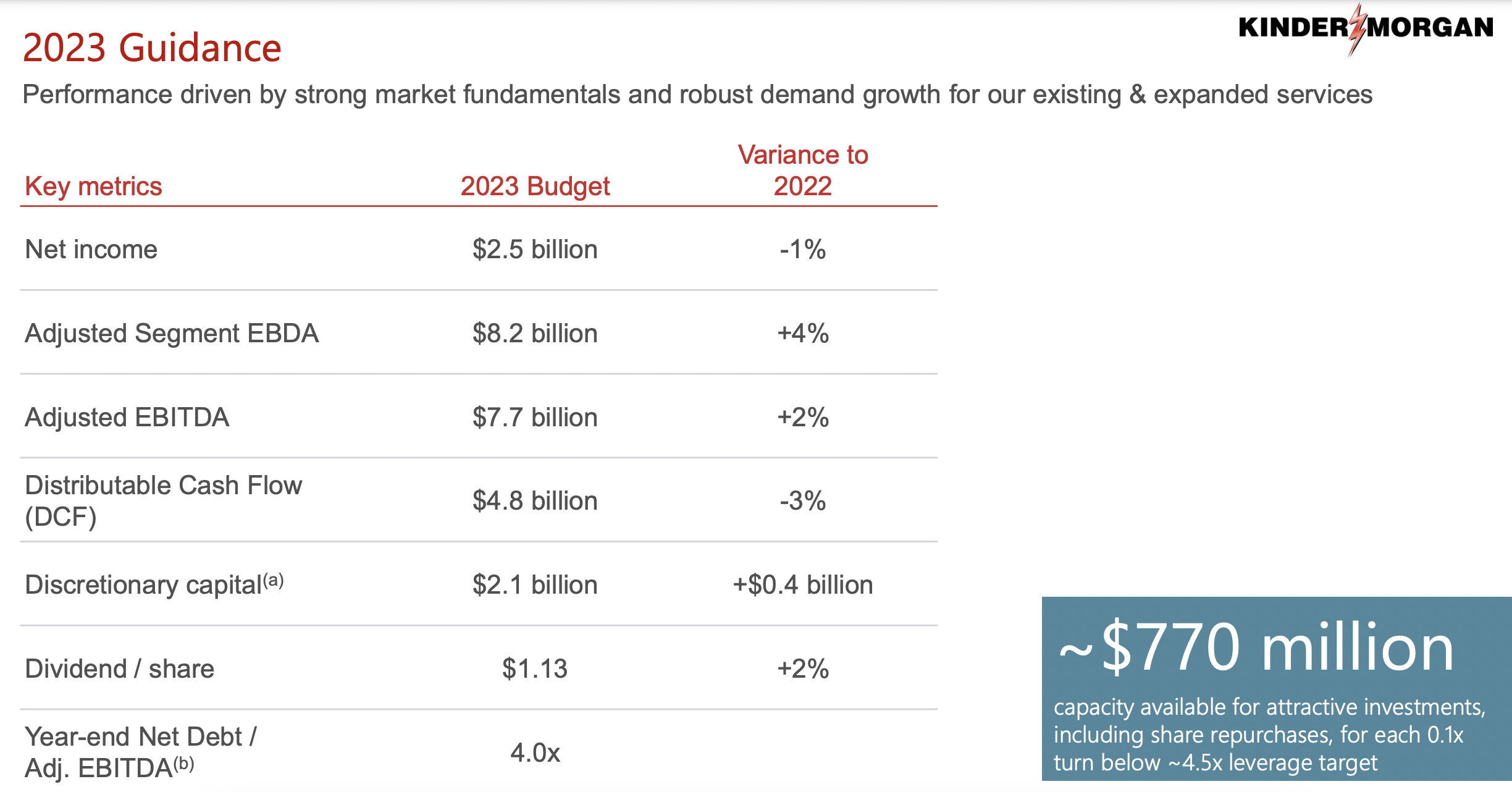

This brings us to the incredibly important discussion of what management is currently forecasting for 2023. On the bottom line, the company has provided guidance for two particular cash flow metrics. DCF for the year is forecasted to be $4.8 billion, while EBITDA is slated to come in at about $7.7 billion. By comparison, last year, DCF was just under $5 billion, while EBITDA totaled $7.5 billion. These results are not terribly different year over year. So it wouldn't be a surprise if results experienced in the first quarter are very similar to what they were at the same time last year.

{kind=link}

Author - SEC EDGAR Data

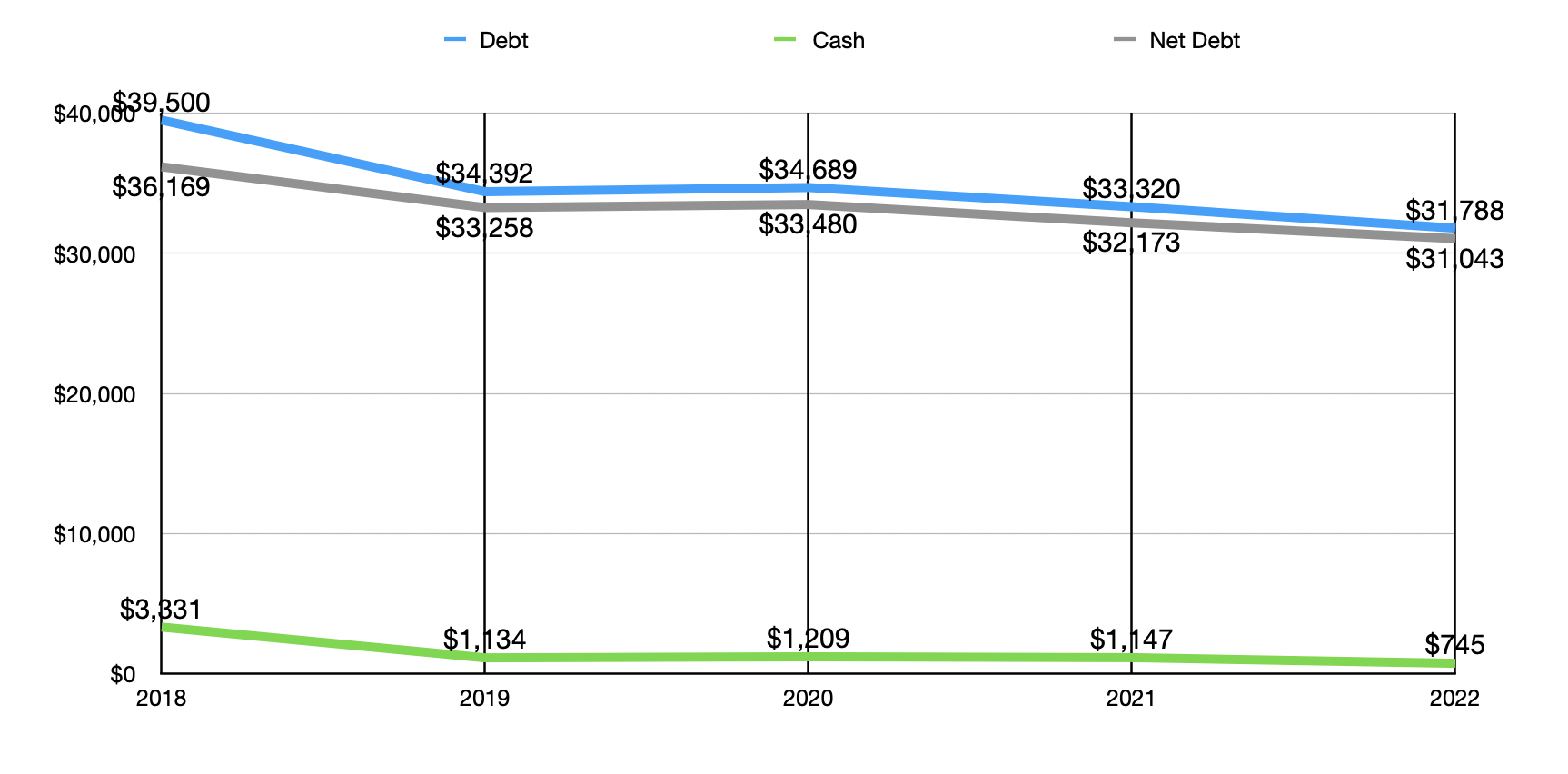

Another thing investors would be wise to keep a close eye on would be the amount of leverage the company has. This has been a common complaint amongst the investment community. The good news is that management has made progress on it in recent years. In 2018, for instance, the company ended the year with net debt of $36.17 billion. Every year since then, with the exception of 2020 when debt worsened, we have seen an improvement compared to the year prior. At the end of last year, it came in at $31.04 billion. That translates to a net leverage ratio of 4.13. This is far from being high in this space. In fact, the company could probably take on some additional leverage without any problem. But given the historical trend, I imagine that debt reduction will continue to take place moving forward.

{kind=link}

Kinder Morgan

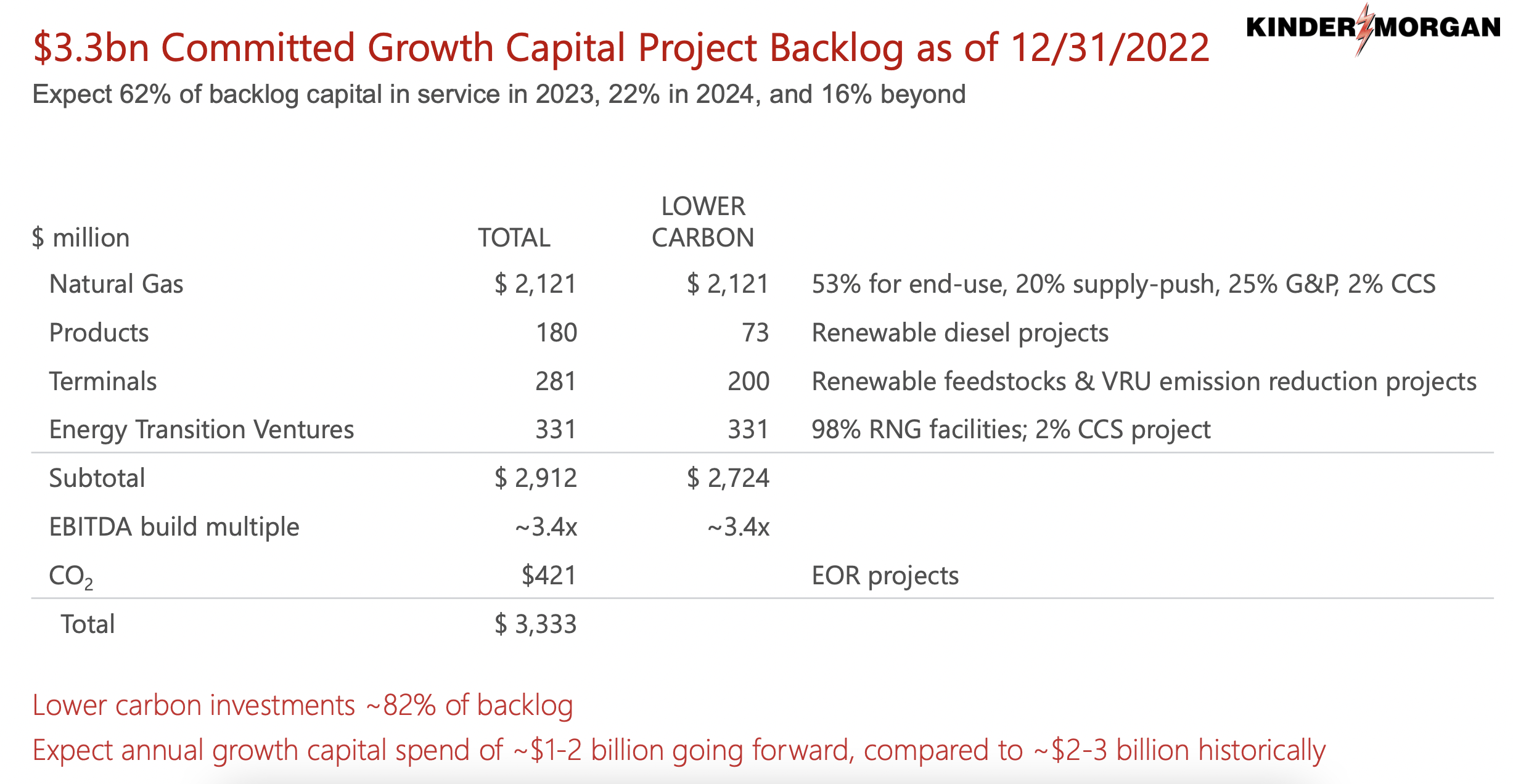

Outside of the financial data, investors should be paying attention to some of the growth-oriented projects that management has embarked on. As of the end of the 2022 fiscal year, for instance, Kinder Morgan had growth capital project backlog of $3.33 billion. The largest portion of this falls under natural gas, with planned expenditures of $2.12 billion. This is followed by a rather distant carbon dioxide budget of $421 million. 62% of this backlog is expected to be completed and the projects in service this year. Another 22% should be completed in 2024. This is another reason why I believe that debt reduction will become an even greater priority moving forward. Historically, the company has spent about $2 billion to $3 billion on growth capital expenditures each year. But after this year, management is expecting this number to drop to between $1 billion and $2 billion. This will leave significantly more capital to allocate toward debt reduction, share buybacks, and dividends.

{kind=link}

Kinder Morgan

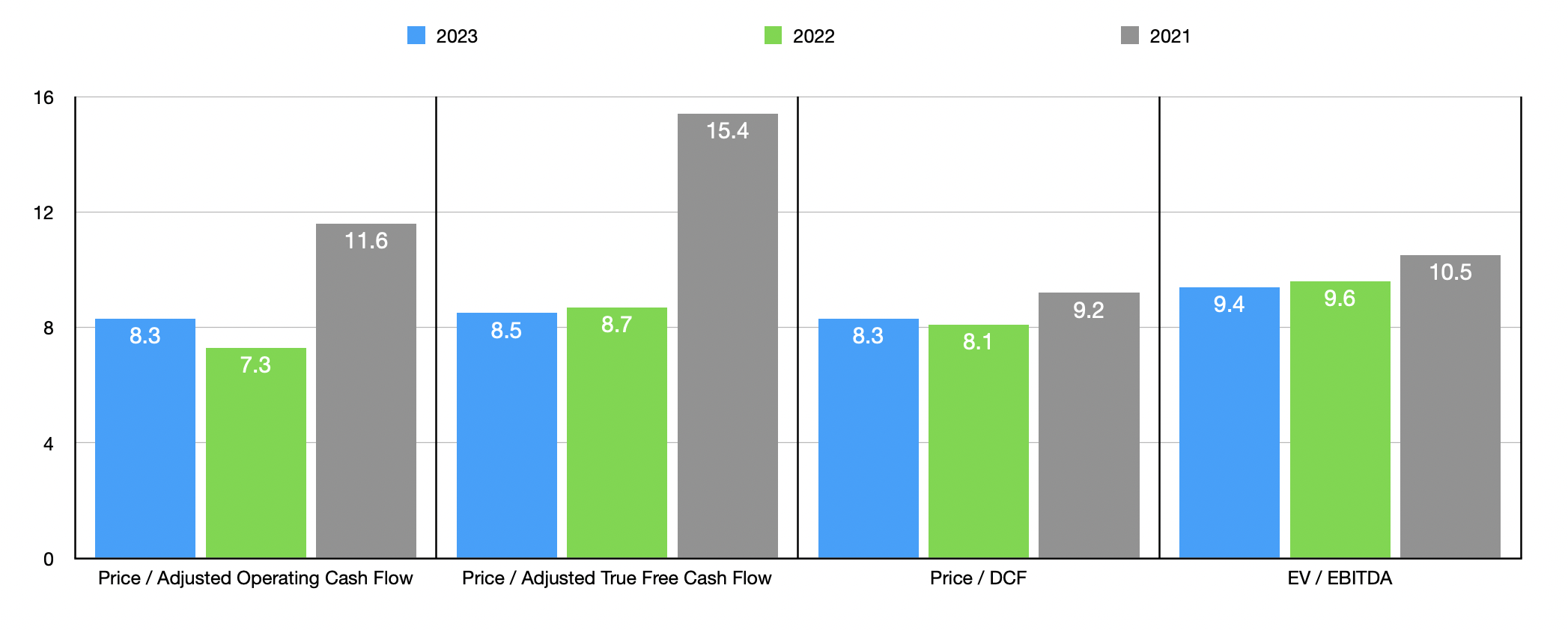

All of the operational data aside, one reason why I really like Kinder Morgan is that shares of the company look cheap. If we assume that other profitability metrics will rise this year at the same rate that EBITDA it's forecasted to, with the exception of DCF since we already have guidance there, we should anticipate some positive results. For instance, the adjusted operating cash flow of the company should be about $4.8 billion, while the adjusted true free cash flow of the business should come in only slightly lower at $4.7 billion.

{kind=link}

Author - SEC EDGAR Data

Taking these figures, I was easily able to value the company using multiple different approaches and utilizing data from 2021, 2022, and forecasts for 2023. These results can be seen in the chart above. Meanwhile, in the table below, you can see how shares in the company are priced compared to similar firms. Using the price to operating cash flow approach, I calculated that three of the five companies were cheaper than our prospect. This number drops to two firms if we look at it from the perspective of the EV to EBITDA multiple.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Kinder Morgan |

| 7.3 |

| 9.6 |

| Williams Companies ( WMB ) |

| 7.6 |

| 11.0 |

| Energy Transfer ( ET ) |

| 4.4 |

| 7.6 |

| Cheniere Energy ( LNG ) |

| 3.7 |

| 11.3 |

| MPLX LP ( MPLX ) |

| 7.0 |

| 9.0 |

| TC Energy Corporation ( TRP ) |

| 8.6 |

| 18.1 |

Takeaway

Fundamentally speaking, Kinder Morgan is an excellent company. Long term, I have no doubt that the firm would do quite well for itself and its shareholders. KMI stock is cheap on an absolute basis, while being more or less fairly valued compared to similar firms. I don't like that management is planning to focus less on growth after this year. But the upside is that this will leave more capital for other interesting use cases. Given all of these factors, as well as the firm's continued commitment to debt reduction, I do believe that the ‘buy’ rating I assigned the stock previously still makes sense. But of course, this could always change based on what is reported for the first quarter. And that is why investors would be wise to keep a close eye on the data that comes out.

For further details see:

Kinder Morgan Q1 Earnings Preview: What To Watch For