KNDGF - Kindred Group: A Volatile Long-Term Buy

Summary

- The value proposition remains but recent capital markets day objectives fall short.

- Regulatory risk is high and the recent Dutch case shows the potential impact of future regulatory changes. Online gambling continues to have a negative image.

- US market remains a question mark. Profitability and competition issues linger with management indicating a future top 10 market position objective.

- Management is focused on the new proprietary Kindred Sportsbook Platform and scaling, although the EBITDA margin expected in 2025 is lower than recent years' average.

- A potential merger or sale continue to be on the table.

Investment Thesis

I believe Kindred ( KNDGF ) to be a long-term buy if you can accept the volatility caused by potential ESG-related short-term headwinds. It's my conviction that the most significant headwinds for the company are behind it and that the return to the Dutch market together with easier comps should return the stock to previous prices and more.

Business

Founded in 1997 and currently headquartered in Malta, Kindred is the fourth biggest digital entertainment group in the world (by gross winnings revenues). They account for 9 brands under poker, casino, and sportsbook categories with the biggest markets being the UK, Belgium, France, and, hopefully, the Netherlands. To have more control over their software offerings, they acquired in 2021 B2B Estonian game creator, Relax Gaming.

By the end of 2021, Kindred employed 2055 employees in over 13 offices worldwide. It's primarily listed in the OMX Nasdaq Stockholm with a market cap of ~21Bi SEK.

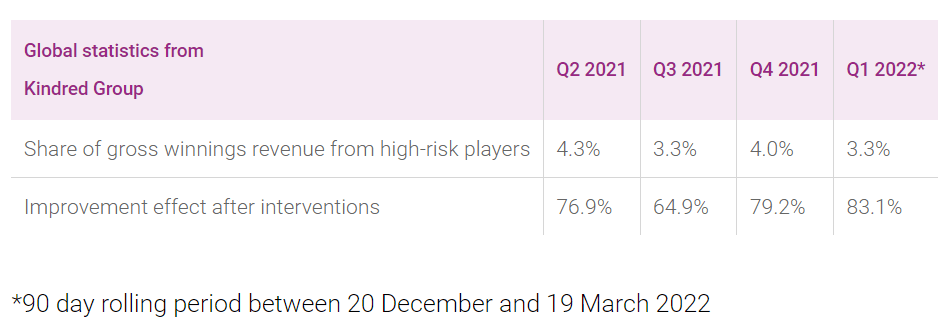

There has been a growing effort made, by the company, to change the paradigm of gambling to a more sustainable way with a clear objective of achieving 0% revenue from harmful gambling by 2023 . Kindred estimates that 3.3% ( Q1'22 data ) of their revenue is derived from these "high-risk players" and wants to implement AI technology to achieve their 2023 goal. This push is essential in a morally and socially acceptable way, but also because it stops the actions of governments tacking it and limiting their activities.

{kind=link}

They have been through a recent 6 months "cool-off" period regarding the regulation of the Dutch market which severely impacted the overall business. At the moment, the online gambling license has been issued to them and they are over expectation regarding market share recovery.

Macro Environment and Sector

Kindred is recovering from tough comps created by the COVID-19 massive online shift in gambling and we are starting to see an overall slowdown in economies worldwide due to multiple external factors like the war in Ukraine and inflation. These situations represent a complicated environment for businesses to operate in and although I believe that online gambling will do okay in a recession, this is still a cyclical business and it will be affected by a downturn.

The gambling market, especially the online one, is expected to grow CAGR close to double-digit in the next years . The increasing transition from physical to online gambling seen in recent years should remain high, although at a smaller rate. This growth is seen on a bigger scale in the US market where Kindred is pursuing a decent market position overall, management hopes to be top 10 in the future. This general market trend is providing "tailwinds" to the sector and we see some loss-making US operators already with significant valuations, showing that investors acknowledge the bright future of the industry.

Competition is fierce and we are seeing the impacts of it in the US where no company is currently able to be profitable, Europe's markets are more mature with established players operating for some years now. I see the main competitors of Kindred being: Betsson ( BTSNF ), Entain ( GMVHF ), Flutter Entertainment ( PDYPF ), Kaizengaming, and DraftKings ( DKNG ).

Economic Analysis

In recent years, we have seen Kindred growing revenues above industry growth rates (~13% CAGR since 2017) implying success in their business model and also quality all-around. One of the things I have to give credit to Kindred is the sustainable and steady growth that they have been doing over the past years, this appears to be the opposite of what other competitors are doing who pursue growth at all costs.

Kindred KPIs (Kindred's website)

Having the awareness to take COVID-19 boom years with a "grain of salt", this is a very asset-light model that provides great returns on almost every level. Their ability to produce results with the assets and capital owned is fantastic. The online gambling industry works with a negative working capital model, allowing them to finance the business with deposits from customers and suppliers. They also have a low debt level which due to the regulatory risk involved, I tend to agree that they should be careful with leverage.

Worth highlighting the cash generation abilities of Kindred, it's a very cash-generative business, with profits matching the cash from operations, even in periods with major unexpected events, as we saw in recent times. Potential dividends and buybacks going forward should be attractive.

{kind=link}

Potential Sale or Merger

We have been seeing some US funds buying large positions in Kindred lately. The main one is Corvex Management which has been building up a considerable ownership position of more than 10% and quickly began influencing the board to consider a merger or a sale. This scenario is possible if we take a look at recent events in the sector and see that there might exist more prominent players moving into the space ( the case of Disney ) or the consolidation of existing companies like the, now abandoned, merger idea between Entain and DraftKings.

Well, Kindred has a low debt balance sheet, good know-how, and experience in the industry, strategic established positions worldwide and belongs to a list of low-multiple (cheap in comparison to the rest) gambling operators together with Betsson and, before it was bought by MGM , LeoVegas ( LEOVF ).

Although an investment shouldn't be based on this possibility, I believe this should be taken into consideration when assessing the potential upside of Kindred.

Future Outlook and Evaluation

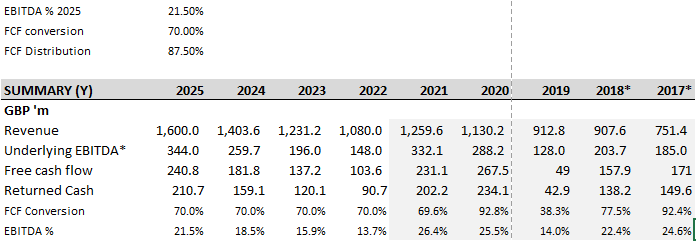

At the recent Capital Markets Day in London, management presented clear guidelines going forward into 2025. The idea is to have 1.6BI GBP in revenue (organic), an EBITDA margin between 22% and 21%, and a distribution of 75% to 100% FCF (after M&A). The release was below my expectations, especially over the low 2025 EBITDA margin positioned below historical averages. Underlying EBITDA for the record high 2021 COVID-19 period was 332M GBP, quite close to the 2025 goal of 344M GBP. I'm hoping that management illustrated a very conservative view of the future and that we might see some upside potential going forward.

{kind=link}

This future projection is considering a linear evolution of the EBITDA margin, with the recovery from the Dutch market and also the gradual implementation of the Kindred Proprietary Platform to model the path until 2025.

Assumptions for DCF (own data) DCF Model (Own and Kindred's data)

Using just the cash distributed to the shareholders in a 4-year DCF model with a 12.4% WACC, I get to a fair value of roughly 125 SEK. This target represents a potential upside of more than 30% from the current price. While this is just an approximation target, it shows the potential of the business and the (unfair) beating that it took because of short-term headwinds.

Company and Sector Risks

Even believing in a positive outcome, there are two main risks to take into consideration when assessing Kindred with the first being the regulatory risk limiting their ability to operate in one or more markets, a similar situation to what happened in the Dutch case. This situation relates to the ongoing regulation happening across Europe, at the moment, we are seeing examples in the UK ( Entain comment ) and Norway ( recent developments ). I believe this to be more of a sector risk overall.

The second risk is concentrated more in the development of additional competition wars as we see in the US market since I don't see (yet) any clear moat for the companies. Competition driving increasingly better bonuses and more compelling odds will consequently lower the returns and profitability of operating participants. I consider the new Kindred Sportsbook Platform a suitable idea to mitigate this risk by differentiating their offer.

Conclusion

Kindred operates in a problematic environment pushed by competition and low ESG scores, which might require an extra margin of safety for the entry price. Still, I do see value in the characteristics of the sector, management, past sustainable growth, and long-term thesis. I believe it's now undervalued when looking at the future outlook, despite wanting to see more of a recovery before committing further. The possibility of further industry consolidation, in the form of a merger or a sale, could also provide some capital appreciation upside to the stock.

For further details see:

Kindred Group: A Volatile Long-Term Buy