KNTK - Kinetik Holdings: A High Yielding Energy Play

Summary

- Shares of Permian midstream play Kinetik Holdings Inc. (KNTK) yield 8.7%, but with most shareholders opting into its dividend reinvestment program, dilution is increasing.

- The de facto PIPE arrangement will allow the company to more easily deleverage from 4.3 (currently) to its stated goal of 3.5 in 2023.

- With capex and dividend obligations likely to match or outpace distributable cash flow in 2H22, the recent insider buying merited a deeper dive.

- A full investment analysis follows in the paragraphs below.

Art is making something out of nothing, and selling it . - Frank Zappa

Today, we take a look at a high-yield midstream concern. The stock has seen insider buying and the company is trying to reduce the leverage on its balance sheet as well. The company recently transferred its stock listing from NYSE to the NASDAQ. An analysis follows below.

{kind=link}

Company Overview:

Kinetik Holdings Inc. ( KNTK ) is a Houston-based midstream energy concern with gathering, transportation, compression, processing, and treatment services for natural gas, crude oil, and natural gas liquids (NGLs) in the Permian Basin of West Texas. The company is the largest natural gas processor in the region's Texas Delaware Basin and fourth across the entire Permian. Kinetic is the result of a 2022 merger between Altus Midstream and EagleClaw Midstream in February 2022 - more on that deal shortly. Legacy Altus went public through a reverse merger in 2018 with its first trade executed at $95.50 per share, after giving effect to a 2-for-1 stock split in June 2022 and a reverse 1-for-20 reverse split in July 2020. Its stock trades just north of $34.00, translating to a market cap of just north of $4.3 billion.

The company is capitalized by two classes of stock. The 40.6 million shares of publicly traded Class A stock confer one vote per share and economic interest. The 94.5 million shares of privately held Class C stock receive dividends, one vote per share, and convertibility into Class A shares.

May Company Presentation

The Merger

Kinetik's roots began with the formation of EagleClaw Midstream in 2012. It acquired two other midstream businesses before it was bought by Blackstone ( BX ) in 2017. The following year, exploration concern Apache (now APA Corporation ( APA ) ) entered into an agreement with special purpose acquisition company Kayne Anderson Acquisition Corp. in which the former contributed its midstream assets, including options on ownership interests in (at the time) five pipelines, to create a publicly traded holding company anchored by Apache's production in the Alpine High resource play of the Permian. Named Altus Midstream, the Permian Basin pure-play was an attempt to unlock value as Apache still owned approximately three-quarters post-transaction. Under Blackstone, EagleClaw purchased additional midstream assets and merged with Altus, forming Kinetik in February 2022.

May Company Presentation

The company generates the preponderance of its gross profits from its midstream logistics business - primarily gathering and processing - and its ownership interests in four pipelines. The logistics segment has over 2 billion cubic feet per day (Bcfpd) of natural gas processing capacity with no federal land exposure. Its pipeline business consists of ownership interests in two natural gas pipelines (Permian Highway (55.5% ownership) and Gulf Coast Express (16.0%)), one NGL pipeline (Shin Oak (33.0%)), and one oil pipeline (EPIC Crude (15.0%)), all of which run from the Permian Basin towards markets on or near the Gulf Coast. These pipelines are fed by intra-basin pipelines fully owned by Kinetik. Its customer base of producers is over 30 strong, led by Apache.

May Company Presentation

Approximately 83% of its business is currently fee-based with the balance subject to commodity prices, although owing to hedging exposure is limited, with a $10 change in the price of a barrel of oil or a $0.50 per MMBtu movement in the price of natural gas impacting Kinetik's EBITDA by ~$4 million. The average contract life with its customers is 10.5 years with no near-term expirations.

Between the systems integration (which was completed in June 2022) and G&A cost reductions, Kinetik expects to realize more than $50 million of EBITDA synergies from the merger.

Giving effect to a secondary offering conducted by selling shareholder Apache in March 2022, the public currently owns 11.6% of Kinetik, with management (4.5%), Blackstone (49.6%), I Squared Capital (20.8%), and Apache (13.4%) holding the balance.

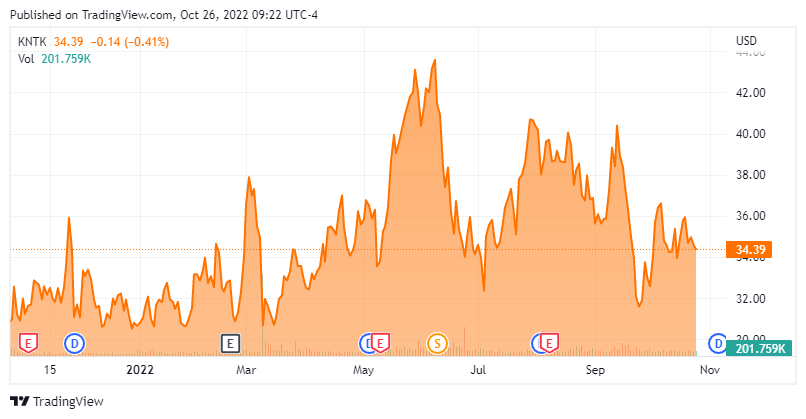

Share Price Performance

Given the reverse and forward stock splits in a two-year span, it is easy to ascertain that it has been a wild ride for Altus and now Kinetik shareholders. Pre-merger, Altus stock hit an all-time high of $104.80 a share (again, adjusted for splits) shortly after going public and eventually plunged to $4.70 a share during the negative oil price madness of May 2020. After regaining momentum, shares of (then) ALTM plunged 27% to $30.92 when the market did not react kindly to news of the EagleClaw merger in October 2021. Its first trade as Kinetik transacted at $30.92 a share on February 23, 2022. With the exception of the Apache sale (3.5 million shares at $29.00) that briefly depressed shares of KNTK in March, its stock has remained predominantly in a range of mid-30s to low-40s, buttressed by a $1.50 a share quarterly dividend. It should be noted that the proceeds from Apache's minor divestment are earmarked for production in the Permian that will support Kinetik's midstream logistics assets.

2Q22 Earnings & Revised Outlook

Along those lines, the biggest takeaway from the company's 2Q22 earnings report (announced on August 9, 2022) was an increase in FY22 capital expenditures, reflecting new commercial agreements and new capital projects as expansion in the Permian continues. In its first full quarter as a combined entity, Kinetik posted earnings of $0.06 a share (GAAP) and Adj. EBITDA of $207.9 million on revenue of $355.6 million. Its gross profit and Adj. EBITDA metrics were split ~65/35 midstream logistics/pipeline transportation. Given the recent combination and the different accounting treatments of its midstream logistics (revenue) and pipeline transportation investments (income), good comparators are in short supply. That said, on a pro forma basis, Adj. EBITDA improved 24% year-over-year and 9% quarter-over-quarter as processed volumes improved 7% and 5% (respectively) to 1.2 Bcfpd.

Kinetik also 'told' the market that it was a solid quarter by raising its FY22 Adj. EBITDA outlook from $790 million to $830 million (based on range midpoints) to reflect higher commodity prices across all three streams and new gathering and processing agreements coming online in 4Q22. To support the new commercial agreements, the company increased its capex budget for logistics by $42.5 million to $180 million. It also raised its pipeline capex guidance from $0 to $110 million to reflect a capital call for a 550 million cubic foot expansion of the Permian Highway pipeline that is 100% sold out with ten-year take-or-pay agreements and is expected to come online by November 2023. That call represents ~35%-40% of the company's total commitment. Two of its other pipelines are likely to expand in over the next 18 to 24 months.

Balance Sheet & Analyst Commentary:

As part of its financial report, management announced the completion of a balance sheet restructuring that refinanced its debt and retired $644.8 million of preferred stock. Factoring in the preferred retirement that finished in July 2022, Kinetic now holds net debt of ~$3.5 billion, consisting of a $2.0 billion loan that matures in 2025, a $1.0 billion Senior Note that matures in 2030, and ~$500 million drawn on a $1.25 billion revolving credit facility.

The company pays an attractive quarterly dividend of $0.75 for a current yield of 8.7% that (ironically) is acting as a de facto PIPE facility to finance capex, as well as the retirement of its preferred stock and (eventually) debt. The scheme is a dividend reinvestment plan [DRIP] that Kinetik's core investors - ~88% of total shares outstanding - have essentially committed to through 1Q24. So instead of distributing ~$102 million of cash in 3Q22, the company only disbursed $13.5 million, effectively diluting shareholders to the tune of 2.6 million shares. Everything is stock price contingent but based on its September 23, 2022 closing price of $32.07 and its current quarterly dividend, investors can expect Kinetik to raise $656.5 million over the next seven quarters while increasing the total shares outstanding from 135.0 million to 155.6 million. Although referred to as a "de facto PIPE", this DRIP option is available to all shareholders and the company expects to raise its dividend by 5% or more in 1Q23. Either way, it will make it much easier for the company to achieve its targeted net leverage of 3.5 by YE23. After completing the retirement of preferred shares in July 2020, net leverage stood at 4.3.

Over the past month, both J.P. Morgan ($42 price target) and Goldman Sachs ($37 price target) have initiated the shares as a Hold while Morgan Stanley ($44 price target) has maintained its own Hold rating. Mizuho Securities recently reissued its Buy rating with a $40 price target on KNTK.

CEO Jamie Welch is also not troubled about the DRIP 'financing' based on his September 21, 2022 purchase of 24,750 KNTK shares at $36.60.

Verdict:

Based on the current price, would-be investors can purchase Kinetik stock at a discount to Mr. Welch, collecting the 8.7% yield. Some may be concerned about the DRIP arrangement, especially in light of Kinetik's intention to raise the 'dividend-in-kind' at the onset of 2023 and the recent $142.5 million bump in projected capex. If one considers that the company generated distributable cash flow of $289.8 million in 1H22, which is nowhere near enough to cover its plans to outlay $220 million for capex and ~$177 million for dividend payments in 2H22, it underscores the importance of the DRIP, the validity of the concern, and the reason for the generous yield. That said, based on its recently revised 2H22 Adj. EBITDA forecast, it should generate ~$400 million of distributable cash flow in 2H22, which may (barely) cover the dividend if it were paid in cash, without going into further hock.

Although, in theory, a DRIP can improve a stock's low float, that is only true if the public is participating and not (in this instance) the tightly controlled ownership. The real jump in market liquidity won't occur until the core investors (like the selling shareholder sale by APA) start exiting the stock. That overhang is another contributor to its 9.4% yield. Pairing that dividend with a reasonable 9.6 EV/FY22E Adj. EBITDA ratio and its stock's high implied volatility, Kinetik would make an excellent covered call candidate. Alas, likely due to its low float, there is no market for KNTK stock options.

That said, located in the prolific Permian Basin with no federal land exposure and little commodity correlation through YE22 while trading at the low end of its multi-month range, shares of KNTK do seem worth a small investment for those with a high tolerance for risk.

The parties with the most gain never show up on the battlefield. - Naomi Klein

For further details see:

Kinetik Holdings: A High Yielding Energy Play