KNTK - Kinetik Holdings: Almost Too Cheap

Summary

- Kinetik Holdings was created around one year ago in early 2022 via the integration of Altus Midstream and EagleClaw Midstream.

- Subsequently, they saw better-than-expected cash flow performance and whilst the third quarter of 2022 was not as strong as the second, it was still decent.

- Despite this positivity, their share price is near 52-week lows, I suspect due to their constant dilution via their dividend reinvestment program.

- The lower their share price goes, the greater the risk of seeing their dividend payments grow too costly to fund by the start of 2024 when this program ends.

- At best, I still expect the size of their dividend payments will inhibit growth in the medium to long term and thus, I believe that maintaining my hold rating is appropriate.

Introduction

When last reviewing Kinetik Holdings ( KNTK ), it was pleasing to see better-than-expected cash flow performance, as my previous article highlighted. Despite this positivity, their share price nevertheless stayed under pressure and thus as it stands right now, it remains near 52-week lows. Oddly, it could actually be said their shares are almost too cheap due to their dividend reinvestment program, which in turn raises risks of inhibiting their growth in the medium to long-term.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

Author

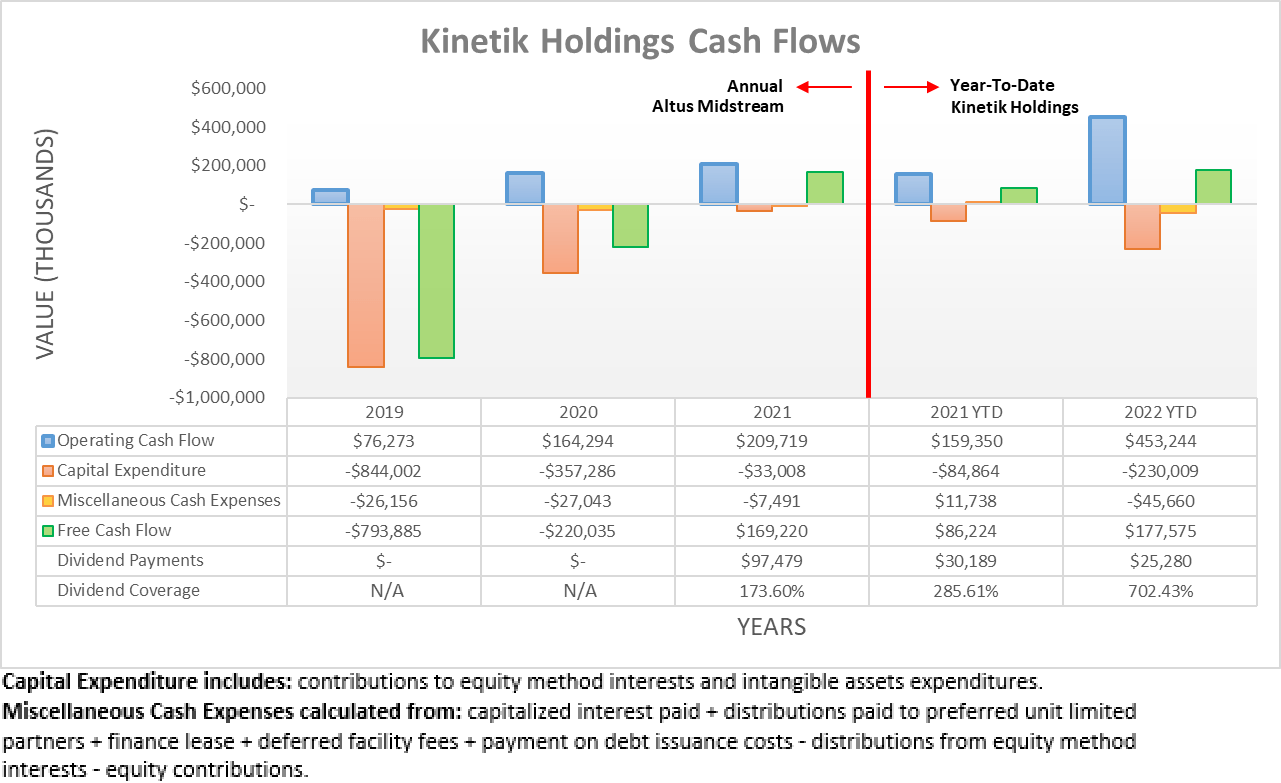

After seeing the integration of Altus Midstream and EagleClaw Midstream that ultimately formed Kinetik Holdings during the first quarter of 2022, it was positive to see better-than-expected cash flow performance during the second quarter when conducting the previous analysis. Likewise, this appears to have broadly continued into the third quarter with their operating cash flow powering ahead to $453.2m during the first nine months of 2022, thereby up very significantly year-on-year versus their previous result of $159.4m as their operational scale increases.

{kind=link}

Author

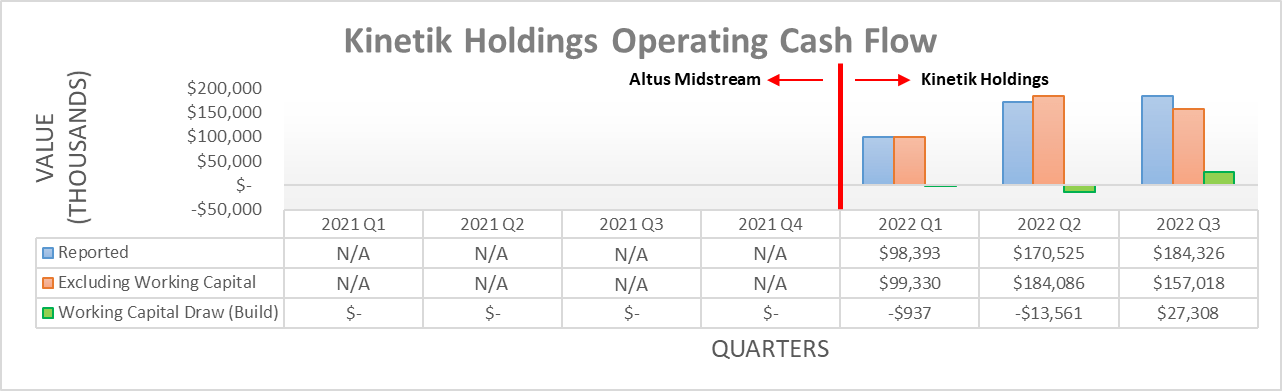

If zooming into their results on a quarterly basis, the third quarter of 2022 reported operating cash flow of $184.3m, which was a new record and thus surpassed their result of $170.5m during the second quarter. That said, if excluding their working capital movements, their underlying result was actually down sequentially during the third quarter to $157m versus the second quarter that saw an equivalent result of $184.1m. Whilst not a stunning result, it nevertheless remains well ahead of the first quarter that saw an equivalent result of only $99.3m.

Despite their otherwise decent results, their share price nevertheless struggled throughout 2022 with its current price of circa $32 near 52-week lows. Whilst the market was not necessarily strong, I suspect that a significant portion of the problem stems from their dividend reinvestment program that sees a portion of their dividends funded via issuing new shares in lieu of cash, which helps facilitate deleveraging. Obviously, more shares equal a lower share price, which creates a sizeable headwind given the third quarter of 2022 saw a staggering 85% of their dividends funded via this method, as per slide twenty-three of their January 2023 investor presentation . This same slide also shows they are planning to increase their dividends by 5% in the coming weeks now that 2022 is over, which will only increase the risk of making their dividend payments too costly to fund by the start of 2024 when they intend to finish this program.

Whether this strategy succeeds depends heavily upon their share price, which in my eyes, creates an odd situation whereby their shares are almost too cheap. A lower share price means more shares will have to be issued in accordance with their dividend reinvestment program, as their quarterly dividends are a fixed dollar value of $0.75 per share. When the third quarter of 2022 ended, their outstanding share count totaled 137,352,157 split between their Class A and Class C shares, whereas the second quarter ended with a count of 135,000,555. In theory, this means the recently ended fourth quarter should see an outstanding share count of circa 140,000,000.

If they lift their quarterly dividends by 5% as indicated, their new amount of $0.7875 per share would already cost a sizeable circa $441m per annum to fund, even if they end their dividend reinvestment program instantly but alas, there are no signs of such a move. Assuming they continue settling 85% of these dividend payments via new shares, this would require roughly 11,600,000 shares at their current price of $32.41, thereby adding around 10% to their outstanding count once considering the effects of compounding and thus pushing the cost to fund their dividend payments towards $500m by the start of 2024.

To relate this cost back to the scale of their company, the second and third quarters of 2022 saw underlying operating cash flows of $184.1m and $157m, respectively. If the average of $170.6m is annualized, it equals circa $682.2m, which does not leave much room to internally fund their capital expenditure given the first nine months of 2022 saw $230m, which annualizes to circa $300m. Whilst yes, 2023 and beyond may see stronger cash flow performance, this nevertheless remains uncertain and regardless, higher dividend payments will always inhibit growth, not just in the case of their dividend terms but also, in the case of their actual company. Plus, it raises the risks of further share price weakness because the dilution would grow even worse and thus make their dividend payments more burdensome to fund by the start of 2024, which is possible given the gloomy economic outlook that could weigh on the market.

{kind=link}

Author

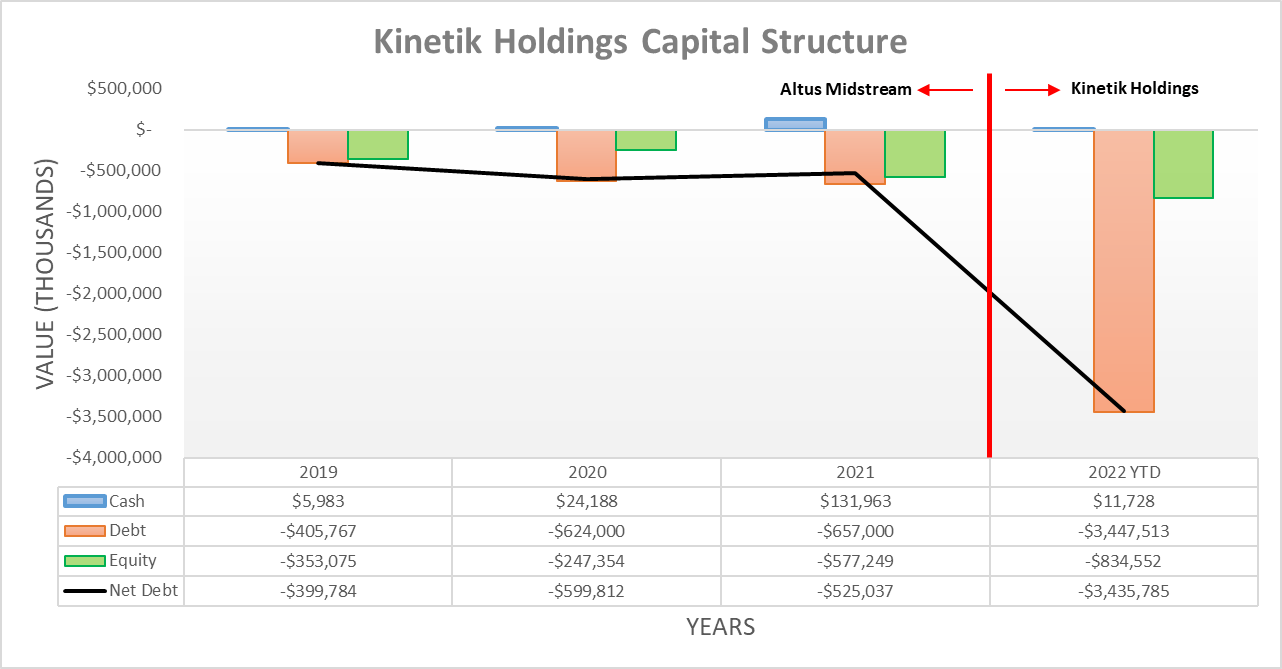

Despite another quarter of free cash flow and dilution via their dividend reinvestment program, their net debt is actually higher following the third quarter of 2022 with it landing at $3.436b, which is up materially versus the second quarter, as it was only $2.966b. The entirety of this $470m increase stems from the redemption of their preferred shares, which totaled $492.2m during the third quarter alone, as management completed one of their 2022 goals of cleaning up their balance sheet. Since this was more so a short-term result of capital structure optimization, their results for the recently ended fourth quarter should see their net debt resume its downward march. Likewise, the same can also be said for the year ahead given their aforementioned intent to retain their dividend reinvestment program running throughout 2023 to facilitate deleveraging.

{kind=link}

Author

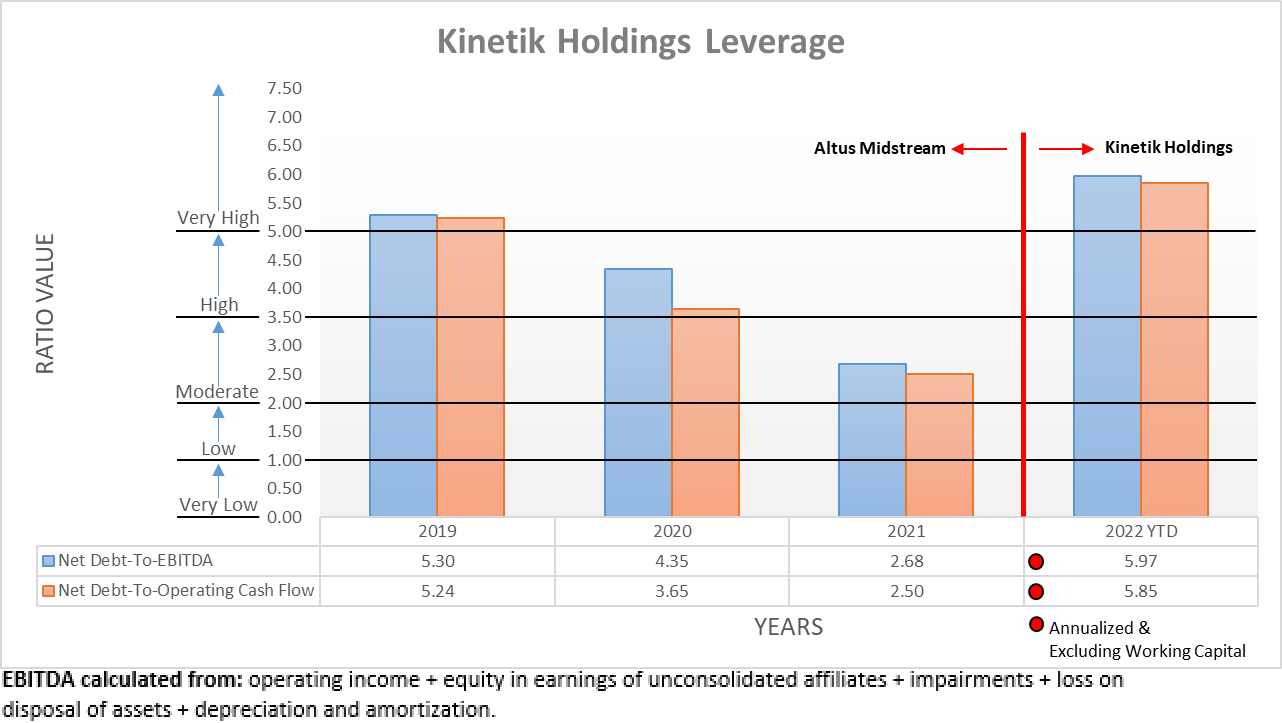

Unsurprisingly, their materially higher net debt following the third quarter of 2022 translated comparably into their leverage. As a result, their net debt-to-EBITDA increased to 5.97 versus its previous result of 5.46 following the second quarter. Meanwhile, their net debt-to-operating cash flow also followed in tandem, thereby increasing to 5.85 versus its previous result of 5.23 across these same two points in time, respectively. Since their leverage was already in the very high territory with results above the threshold of 5.01 following the second quarter, obviously this remains the case once again.

Although not necessarily ideal, this increase is obviously a short-term bump in the road, plus the increase is not too bad given they have cleaned up their balance sheet and thus no longer have to fund their preferred dividends. Furthermore, this should finally represent the high point before subsequently moving lower whilst they deleverage during 2023.

{kind=link}

Author

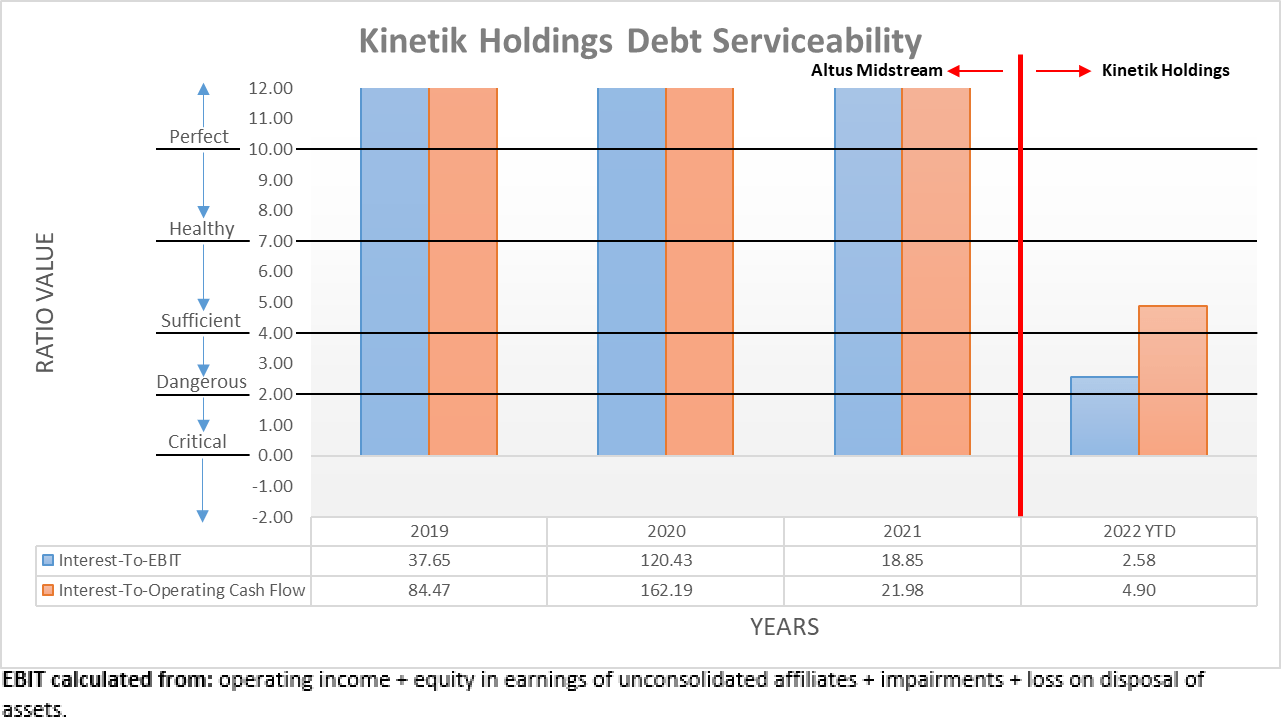

More debt normally equals worse debt serviceability and thus similar to their leverage, unsurprisingly this held true following the third quarter of 2022. To this point, their interest coverage as measured against their EBIT decreased slightly to 2.58 versus their previous result of 2.76 following the second quarter, which thankfully still remains sufficient. Whilst their interest coverage as measured against their operating cash flow produces a higher result of 4.90 that would be considered healthy, like always, I prefer to judge on the worse side. Similar to their leverage, this should improve itself as 2023 progresses and their debt heads lower and monetary policy likely does not tighten as rapidly as seen during 2022.

{kind=link}

Author

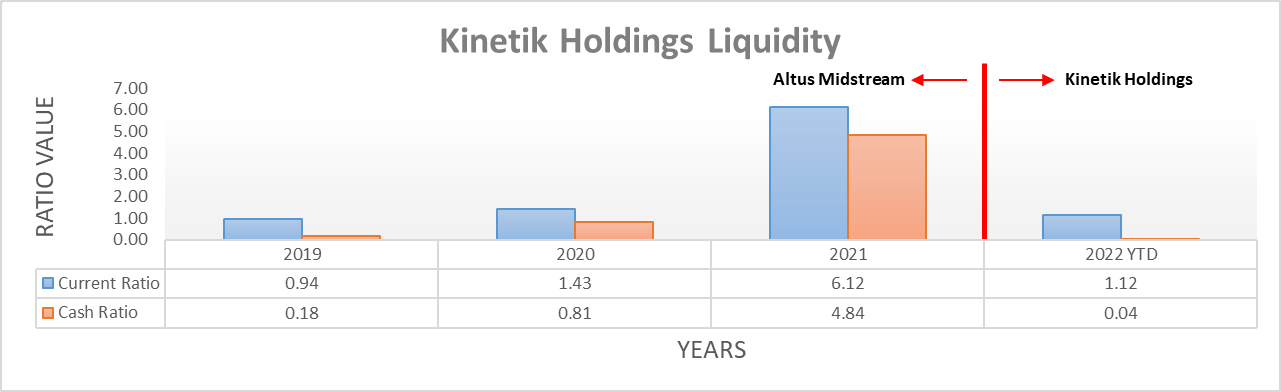

Despite hampering their leverage and debt serviceability, their higher net debt following the third quarter of 2022 did not impact their liquidity with their current ratio of 1.12 unchanged versus its previous result following the second quarter. Meanwhile, their cash ratio increased slightly to 0.04 versus its previous result of 0.02 across these same two points in time, respectively.

Apart from cleaning up their balance sheet via redeeming their preferred shares, they have also simplified their debt structure by refinancing all of their previous debt during the first nine months of 2022, which is particularly impressive given the prevailing monetary policy. The most notable benefit was extending their maturities, which in the case of their credit facility is extended until June 2027 and carries $775m of availability to bolster their otherwise low cash balance. Concurrently, their other two debt maturities, being the $2b term loan and $1b of senior unsecured notes, do not mature until June 2025 and June 2030, respectively.

Kinetik Holdings Q3 2022 10-Q

Conclusion

When it comes to picking up investments, normally they become more attractive the lower their share price goes, holding everything else constant. In this situation, their share price is almost too cheap because the lower it goes, the worse the dilution from their dividend reinvestment program. I personally do not see the point of dividends that are almost entirely funded via issuing new shares since the purpose of shareholder returns is returning cash to shareholders, as the name suggests and I especially do not see why it should potentially encompass dividend growth, as this just makes the dilution even worse. Even if their dividend payments do not grow impossibly large to fund following 2023, I still suspect their size will keep them risky and inhibit medium to long-term growth, thereby inhibiting their share price and thus once again, I believe that a hold rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Kinetik Holdings’ SEC filings , all calculated figures were performed by the author.

For further details see:

Kinetik Holdings: Almost Too Cheap