KNTK - Kinetik Holdings: Growth Outlook Robust As Market Conditions Improve

2023-10-05 07:50:55 ET

Summary

- Kinetik Holdings has a high amount of debt, which has affected its margins and may lead to share dilution.

- KNTK operates in the Permian Basin and is embarking on ambitious expansion projects, but managing the financial aspects will be critical for growth.

- Earnings results for the company were mixed, but the dividend is currently over 11% and sustainable at a payout ratio of 74%.

Generally, I have been quite bullish on the gas and oil industry as I think the market fundamentals here remain very strong and the need for both commodities is unlikely to dissipate significantly in the coming decade at the very least. But what makes me somewhat worried when assessing Kinetik Holdings Inc. ( KNTK ) is the high amount of debt the company has managed to gather up and how it affected the margins currently. It seems that share dilution is a practice that will be kept up by the company for quite some time.

In regards to the valuation for KNTK that is also not something that is going in line with what I am looking for, unfortunately. What keeps me holding shares though is the dividend the company has currently, sitting at over 11% and decently sustainable at least at a payout ratio of 74%.

Market Fundamentals Remain Robust

KNTK operates as a pure play in the Permian Basin, a region known for its abundant oil and gas resources. However, despite the promising potential of this market. KNTK is embarking on ambitious expansion and connectivity projects within the Permian Basin. While these initiatives hold the promise of increased production and market reach, they come with substantial capital requirements. Managing the financial aspects of these projects and ensuring their successful execution will be critical for KNTK's growth and profitability.

Midstream Model (Investor Presentation)

The company is a very diversified midstream company that has managed to build out strong margins which has enabled it to keep up ambitious expansion spending. The net margins for example are at over 14% and the capital expenditures have only been increasing over the years, right now approaching $300 million very quickly.

Market Overview (Investor Presentation)

With the asset base, the company has I think they are in an excellent position to continue driving growth as both oil and natural gas remain in high demand in North America. Being a pure-play operator in the Permian Basin, KNTK finds itself in a highly coveted yet fiercely competitive market. While the Permian Basin offers immense potential for oil and gas exploration and production, KNTK faces the challenge of establishing its presence and thriving in an arena where numerous players are vying for a piece of the pie.

Earnings Results

The results from the last reports are varied as the top line missed estimates whilst the bottom line beat by $0.03 and ultimately ended up at $0.41 per share for the quarter. There is a tough market climate to navigate right now but in my opinion, KNTK did do a good job in the quarter and the slight drop in the share price I don't think was unexpected really. Going forward, I think seeing strong resilience in the bottom line and perhaps even expanding margins could justify the share price staying at this elevated level for some time more. However, the risk that market conditions deteriorate makes for a case that the share price could drop to a valuation more in line with where the rest of the sector is trading, a p/e of around 10 -11 instead maybe.

{kind=link}

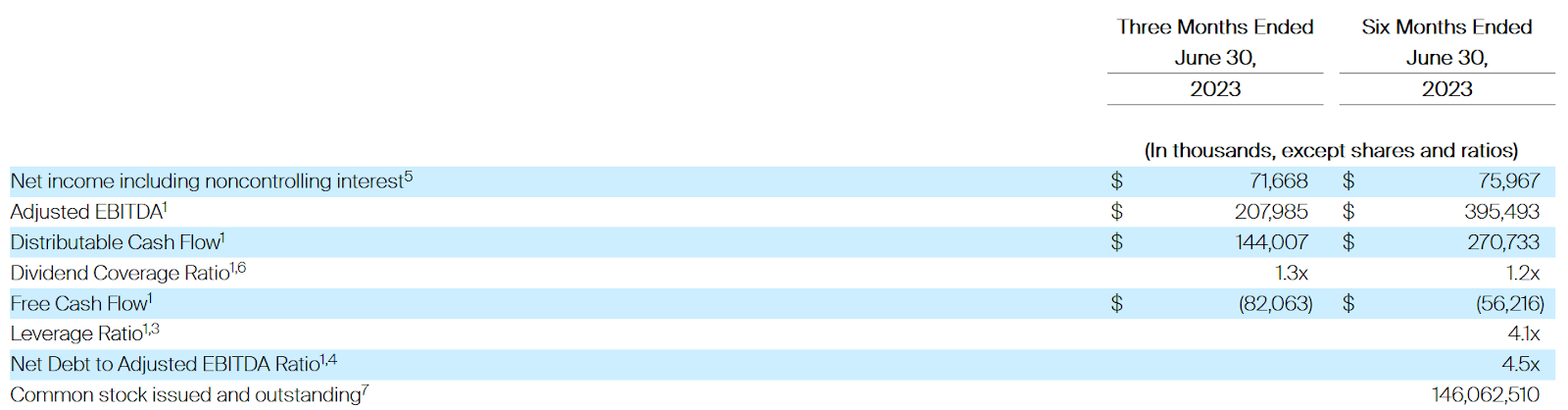

The DCF remained strong for KNTK and the possibility of further increasing or at least maintaining the dividend is strong I think. Looking at the share repurchase program though, it seems that the company themselves are agreeing that the valuation is too high. The last quarter saw $3.3 million used out of the total $100 million authorized for buying shares. That isn't a very large amount and I think KNTK will do well in holding off buying shares until the price drops and they would receive more value for both themselves and investors by doing that. Right now I would rather have that capital used for building up a dividend cash pile they can tap into if market conditions were to worsen significantly more.

Risks

KNTK is not entirely immune to market dynamics. The company remains vulnerable to price fluctuations in its industry, which can subsequently lead to volume declines. These volume reductions can pose challenges to the company's revenue and profitability. APA Corporation faced challenges due to declining rig counts in the Alpine High region, which posed significant setbacks to the company's operations. While the immediate impact of this decline has been evident, it's essential to acknowledge that the future remains uncertain, and there is no guarantee that similar challenges won't resurface, especially in a persistently challenging operating environment.

Debt Position (macrotrends)

Besides the risks of market volatility as commodity prices shift, I think that KNTK is also quite vulnerable to its debt position right now and there is an ample risk here that investors need to keep in mind. The debt position is one of the more worrying factors in my opinion and a reason for the hold rating I have for them right now. The long-term debts have been built up to $3.6 billion in total right now, up from $2.2 billion just 2 years ago. That sort of increase is worrisome as the market cap is just under $6 billion currently, meaning that KNTK has over half of its value in debts.

Interest Expenses (Seeking Alpha)

This has of course affected the interest expenses for the company, which right now is at the highest level ever for the company, $182 million. I think there is a pretty big chance that share dilution will continue to be a factor in raising capital for the company and paying down these expenses. This ultimately hurts the investors quite badly and right now results in the hold rating I have for the company.

Last Pointers

Right now I find that the valuation is too high for KNTK to invest. Paying a nearly 60% premium to the sector is not worth it and significantly introduces risk to a portfolio in my opinion if one were to buy right now. What makes me prone to have a hold rating though comes down to the dividend yield of over 8% currently. This is adequate to justify holding shares and capitalizing from that.

{kind=link}

If the share price could drop to a valuation of 10-11x earnings then I could see it being more reasonable. But right now, I think that you are overpaying for KNTK and will be rating it a hold instead for investors.

For further details see:

Kinetik Holdings: Growth Outlook Robust As Market Conditions Improve