KNTK - Kinetik Holdings: Hold This Stock For Solid Dividend Yield

2023-12-30 00:30:14 ET

Summary

- Kinetik Holdings is an energy firm that offers comprehensive gathering, processing, and transportation services in the Permian Basin.

- The company has experienced significant revenue growth in the past three years, driven by robust demand for oil and natural gas.

- KNTK has been consistently paying dividends and has a solid dividend yield of 8.94%, making it an attractive stock for dividend seeking investors.

- After comparing a forward P/E ratio of 19.07x with industry average P/E of 17.9x and considering industry demand, I think we can safely say that the company is fairly valued.

Investment Thesis

Kinetik Holdings ( KNTK ) is energy firm that delivers comprehensive gathering, processing, and transportation services. I will be examining the company’s financial history and its dividend payment safety. I will also be assessing the company’s valuation using the relative P/E ratio model.

About KNTK

KNTK is an integrated midstream energy firm that offers comprehensive gathering, compression, transportation, processing, and treating services in the Permian Basin. The company conducts its business in two reportable segments: Midstream Logistics and Pipeline Transportation. The Midstream Logistics segment offers three services: gas gathering & processing, crude oil gathering, and stabilization & storage services. Crude oil-related services are provided in the Texas Delaware Basin and include 90000 barrels of crude storage along with 220 miles of gathering pipeline. This segment contributes 99.84% to the company’s total operating revenues. The Pipeline Transportation segment includes equity interests in four EMI pipelines: Permian Highway Pipeline, Gulf Coast Express Pipeline, Breviloba, LLC, and EPIC Crude Oil Pipeline. The company owns 53.3%, 16%, 33%, and 15% equity interests in each of pipelines respectively. This segment generates 0.16% of the company’s operating revenues.

Financials

The crude oil price increased from $76 per barrel to $110 per barrel from January 2022 to March 2022 due to supply chain issues caused by the Russia-Ukraine war which has declined global oil supply to 101.7 mb/d (decrease of 190 kb/d) in November 2022. However, the industry has rebounded in the current year and I believe it can sustain this growth for a long period as oil & gas plays a crucial role in clean energy transition. The USA has boosted its natural gas production mainly to reduce carbon footprints and methane emissions as natural gas is considered comparatively cleaner than other fossils such as coal and diesel. Identifying this opportunity, the company has planned to expand its Permian Highway Pipeline with an incremental capacity of 550 MMcf/d. This expansion can facilitate the company to boost its deliveries of natural gas from the Permian to the U.S. Golf markets. In addition, it has also constructed Delaware Link, which is a residue gas pipeline of 30 inches to Waha with a throughput capacity of 1 Bcf/d. This pipeline will be operational from 1st October 2023. I believe these expansions can significantly accelerate the company’s growth as it increases the company’s operational capabilities and can help KNTK to increase its deliveries of natural gas which can make it well-positioned to address the growing demand. The company has also expanded its gas gathering system in New Mexico which includes 20+ miles of high-pressure pipeline. This pipeline is expected to be operational in 1Q24. This expansion can help it diversify geographically and give it a competitive edge by making its strong presence.

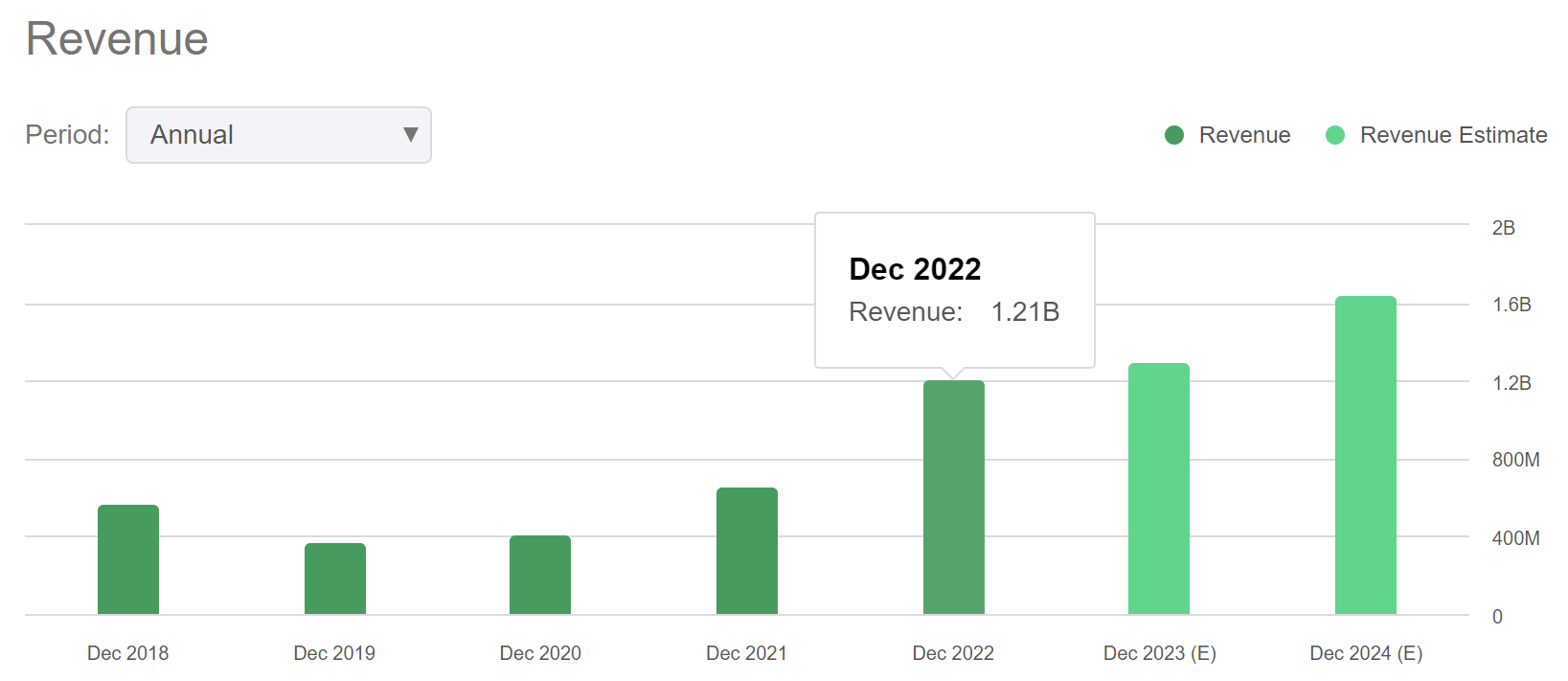

Revenue Trends of KNTK (Seeking Alpha)

{kind=link}

KNTK has witnessed spectacular revenue escalation in past three years which showcases its impressive growth trajectory. The company reported revenue of $662.04 million in FY2021 which is 61.4% increase compared to $410.18 million in FY2020. The reason behind this noteworthy growth was robust demand for NGL pipelines & natural gas and consistent inputs from the gathering & processing operation of the company. In FY2021, KNTK’s operating income margin (OIM) and net income margin ((NIM)) were 8.1% (OI of $53.5 million) and 0.22% (NI of $1.5 million), respectively. The company continued its growth momentum in FY2022. The revenue of $1.21 billion in FY2022 is 83.28% YoY growth compared to FY2021 revenue. This remarkable growth was result of increased volumes in Pipeline Transportation & Midstream Logistics. During FY2022, the company demonstrated a robust OIM of 12.4% (expansion of 430 bps compared to OIM of FY2021) which is equivalent to OI of $150.5 million. Additionally, NIM stood at 11.17% (expansion of 1095 bps compared to NIM of FY2021), reflecting NI of $135.5 million. This dramatic increase in the margins is the result of integration cost synergies , system optimization, ad valorem tax reductions, and relocation of projects. The margin expansion was partially resisted by low commodity prices in second half of FY2022. The company ended FY2022 with distributable cashflow ((DCF)) of $142.23 million and net debt of $3.39 billion.

The company recently reported its quarterly results. It reported operating revenue of $330.3 million in Q3FY23 which is surge of 1.57% YoY compared to $325.18 million in Q3FY22. The increase was mainly driven by increase in gas volume. KNTK reported $2.23 million in liquidity and adjusted EBITDA stood at $208.0 million. The company completed nine months of FY2023 with DCF of $418.8 million. It reported net debt of $3.63 billion at end of last quarter. The firm’s net income (including non-controlling interest) stood at $43.1 million which is decrease of 11.5% compared to $48.7 million in previous year’s same period. It reported EPS of $0.81 attributable to the firm (including non-controlling interest) and EPS of $0.21 attributable to class A shares.

The results were affected by macroeconomic pressures and fluctuations in the price of energy, however, as the scenarios are changing gradually due to the significant role of natural gas in energy transition, I believe the company can make the most of this opportunity as it is aligning with its plan to expand its pipeline system in multiple locations. As it expands its pipelines it can increase its market penetration and can expand its profit margins. Considering these scenarios, KNTK expects that FY23 EBITDA can be between $820 million to $860 million. The company believes that it can easily surpass volume levels of FY2022 and FY2023 in FY2024. Looking at current demand and economic situation, I think the company can easily surpass volume FY2022 and FY2023. The high prices of oil and natural gas confirm the demand for products is higher than the supply of the products. After taking into account high prices and demand for oil and natural gas I think we can confidently assume that revenue of FY2024 can easily beat the revenue of FY2022 and FY2023. Therefore I estimate revenue of FY2024 to be $1.55 billion. Since the demand & prices of oil & gas and the economic situation in FY2024 could potentially be similar to previous seven quarters, I am estimating net income margin of FY2024 by averaging net profit margin of the previous seven quarters. KNTK’s average net income margin is 17% which gives the EPS estimate of $1.76.

Calculation of Average Net Income Margin of KNTK (Value Quest)

{kind=link}

Dividend Yield

The company has been paying consistent dividend payouts for last three years. In FY2022, the firm paid a cash dividend of $0.75 in each quarter to class A shareholders. This dividend payout totaled $3 per share annually. This payout represented a dividend yield of 8.94% compared to the current share price of $33.57. In FY2023, it continued quarterly dividends of $0.75 in each quarter, which makes a solid dividend yield of 8.94%. The company has completed nine months of FY2023 with dividend coverage ratio of 1.2x which indicates that the dividend is safe. Even the management has stated that they are thinking about increasing dividend payments in coming period which provides assurance about future dividend payments. Even if the company continues to pay a dividend yield of 8.94% still this solid dividend yield makes KNTK an attractive stock to hold in the portfolio. The dividend yield of the company is significantly higher than sector median dividend yield of 3.51%.

{kind=link}

As compared to its key competitors such as DT Midstream ( DTM ), EnLink Midstream ( ENLC ), Frontline ( FRO ), Equitrans Midstream ( ETRN ), and Ultrapar Participações ( UGP ), KNTK pays significantly higher dividend yield. The company's dividend yield of 8.94% is 68.4% higher compared to its industry average dividend yield of 5.31%.

It can be wise choice for risk-averse investors seeking steady income. Observing the company’s current growth in pipeline expansion and the positive industry demand, I believe it can significantly increase its cash flows in coming years which can further help it to increase its dividend payout.

What is the Main Risk Faced by KNTK?

The company’s operating assets are mainly concentrated in the Permian Basin. This high concentration exposes the company to the risk of regional demand and supply fluctuations, water shortages, market limitations, weather conditions, and delays in the production of wells in this region. All these factors can disrupt the company’s operations and can impact its ability to serve its customers which can further contract its profit margins.

Valuation

The oil & natural gas industry is experiencing positive demand due to its prominence in reducing carbon emissions. I believe the company is well-positioned to capture the growing demand as it has recently executed its strategic plans of expanding its pipeline which can help it to increase its natural gas deliveries and further expand its profit margins. After considering all the above-mentioned factors, I am estimating EPS of $1.76 for FY2024 which gives the forward P/E ratio of 19.07x. After comparing forward P/E ratio of 19.07x with the industry average P/E of 17.9x and considering industry demand I think we can safely say that the company is fairly valued.

Calculation of Industry Average P/E Ratio (Value Quest)

{kind=link}

Conclusion

The industry is experiencing a healthy demand as natural gas is a comparatively cleaner fossil than coal and diesel which can be used to achieve net zero carbon emissions. The company has shown solid financial growth in last three years with help of strong demand in the market. The company has recently reported its quarterly results and performed well however it was negatively impacted due to macroeconomic pressures compared to the previous year. It is strongly aligning with its plan to expand its pipeline systems which can help it to increase its natural gas deliveries and further increase its profit margins. Its concentrated operations in Permian Basin might contract its profit margins due to adverse regional conditions. I believe the company’s expansion can help it to increase its cash flows and maintain its consistent dividend growth. The stock is currently fairly valued and investors can hold stock for solid dividend yield. After considering all the above factors, I assign a hold rating to KNTK.

For further details see:

Kinetik Holdings: Hold This Stock For Solid Dividend Yield