KNTK - Kinetik: Starting Valuations A Plus Economic Leverage Balances The Debate

2023-09-13 06:46:31 ET

Summary

- Kinetik Holdings Corp is an integrated midstream energy company operating in the Permian Basin.

- The company reported Q2 FY'23 revenues of $335.5mm, with growth in its midstream logistics segment and pipeline transportation revenues.

- KNTK is on track to meet its production goals and has hedged over 20% of its FY'24 commodity-linked gross profit exposures.

- However, the company's low returns on capital and capital-intensive nature present challenges to growing intrinsic value.

- Net-net, rate hold.

Investment summary

Kinetik Holdings Corp (KNTK) is an integrated midstream energy company operating in the Permian Basin. The company offers a suite of services in the gathering, transportation, compression, processing, and treating of natural gas. KNTK's capabilities extend to gathering, stabilization, storage, and transportation of both oil and NGLs as well.

The company's equity stock has bounced hard off '23 lows but has failed to extend the bid pas its '22 range. This report will unpack the latest investment updates for the company, and examine what it could do over the coming periods should it continue at its steady-state of operations. Net-net, there are positive points to discuss, including production upsides, and potential value in the starting multiples quoted by the market as I write. But this is a capital-intensive business that is returning sub-par rates of return on the capital tied up in the business. This doesn't align with our core investment tenets. As such, the investment debate is balanced in my view. Net-net, rate hold.

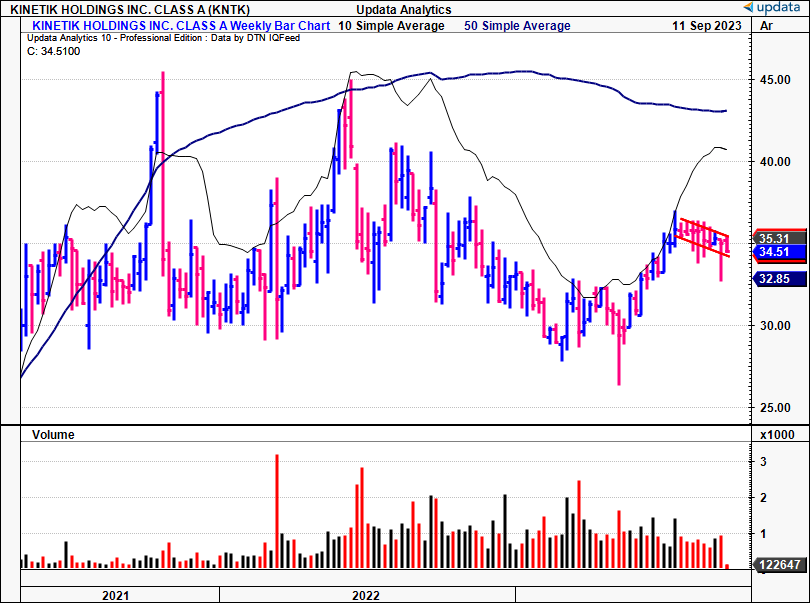

Figure 1. KNTK Weekly price evolution, 2021-date

{kind=link}

Critical facts to investment debate

Brief overview of operations

KNTK's midstream logistics segment offers essential gas gathering and processing services. The segment boasts productive robust infrastructure that includes >1,500 miles of low and high-pressure steel pipelines. These are positioned throughout the Delaware Basin.

KNTK also holds strategic equity interests in four EMI pipelines operating in the Permian Basin. These also provide access to various points along the Texas Gulf Coast. The company has a 53.3% equity interest in Permian Highway Pipeline LLC, and a 16% equity interest in G ulf Coast Express Pipeline LLC- both of which are operated by Kinder Morgan. KNTK also holds a 33% equity interest in Shin Oak , operated by Enterprise Products Operating LLC , and a 15% equity interest in Epic Crude Holdings, LP.

The company is also constructing the Delaware Link Pipeline , which is expected to be completed in Q4 this year. This pipeline, spanning 40 miles, is expected to have an estimated capacity of ~1Bn cubic feet per day.

1. Unpacking Q2 FY'23 numbers

- Breakdown of income + divisional growth

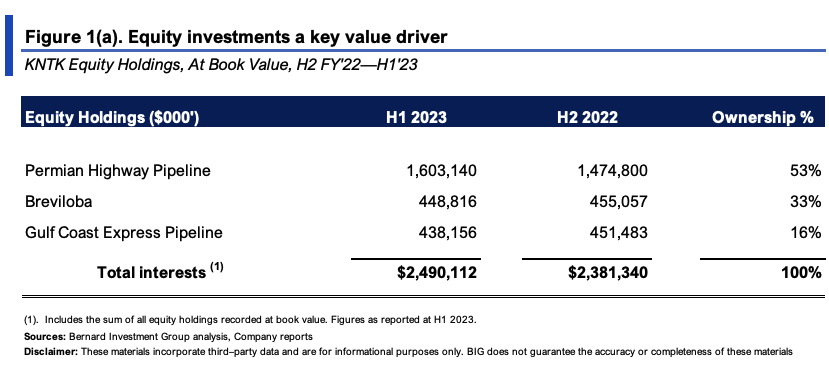

KNTK put up revenues of $296.2mm in Q2 , down from $335.5mm last year. The downsides were on product revenues ($191.4mm from $229.6mm). Still, the company grew its client base to >35 clients during the quarter, processing 1.48Bn cubic feet of natural gas per day ("Bcf/d"), a 10% sequential increase from Q1. It has processed 1.42Bcf/d for the YTD. On this, it booked net income of $71.7mm (including all minority interests, as seen in Figure 1(a)).

{kind=link}

Breaking down the segments by the numbers, observe the following:

- KNTK's midstream logistics segment grew adj. EBITDA of 15% YoY to $138mm in Q2. Growth was underscored by the upsides in gas volume and a 10% increase in fee-based revenue.

- Pipeline transportation adj. EBITDA was up 6% YoY booked $75mm. Increased volumes and improved margins on critical pipelines such as the Shin Oak and Epic Crude assets underscored the profit growth.

The divisional breakdown on Q2 is observed in Q2. As noted, NG, NGLs and condensate brought in the bulk of turnover (~66%), with gathering and processing sales making up basically all the remainder. Of the revenue clip, the Permian Highway Pipeline brought in $99mm, Breviloba $46.6mm and $90.8mmm from the Gulf Coast assets.

BIG Insights

- Production and investment downstream

Moving into H2, the company is on track to meet or exceed its goal of 1.6 Bcf/d by yearend. Management is eyeing adj. EBITDA to trend towards $800mm-$860mm. Critically, it has budgeted CapEX below $150mm for the remainder of the year, and I'd note it's already ploughed back in $195mm in CapEx this YTD.

For its midstream logistics business, it allocated $65mm in H1, while $130mm was invested in its pipeline transportation arm. Cost management has offset some cost increases in its non-operated pipelines, which is a plus. It's also worth noting the company finished the quarter on a leverage ratio of 4.1x (debt to adj. EBITDA).

Critically, management said it has hedged >20% of its FY'24 commodity-linked gross profit exposures. Given the volatility in spot markets for oil and NG, this was a prudent move and will lock in the respective forward rate. Because of the hedged exposure, management expects a positive impact to the profit mix. It projects a reduction in commodity-linked gross profit (decreasing as a percentage of total gross) of ~10% throughout FY'24.

2. Analysis of economic levers

The drivers of value for KNTK over the last 3 years are observed in Figure 3 (all figures in a rolling TTM basis). The growth in sales and incremental operating margins, net of tax, are taken as the drivers to operations. Whereas, the changes in NWC and fixed assets are taken as the investment drivers (note: changes to intangibles are included here, but not used in projections later; changes to acquisitions are included in fixed asset charge).

Since FY'22, sales growth was 12.1%, well above global GDP rates. Operating margins were relatively stable, averaging 21.2% over this time. A corporate tax rate of 22.7% is presumed for an accurate comparison of NOPAT.

In the last 3 years, the company invested $0.148 for every new $1 in sales, made up predominantly of changes to fixed assets. In other words, for every $1 in sales growth, it required an additional $0.09 of incremental investment toward fixed capital.

BIG Insights

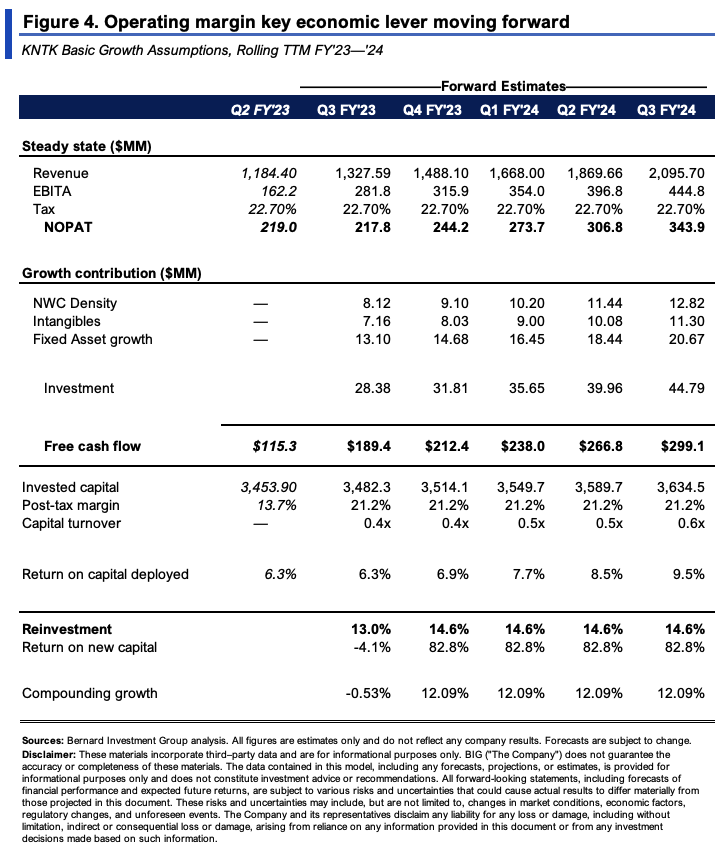

A thoughtful exercise is to carry these stipulations forward to see the 'trajectory' KNTK is on at its steady state of operations. This is detailed in Figure 4. The assumptions are that sales growth will continue at ~12% into 2024, that operating margins will be stable, and that investment needs will remain in line with the c.14.5% rate going forward.

In Q2 FY'23, $3.4Bn of capital was employed to run the business, producing $219mm in NOPAT, just 6.3% trailing return on investment. This is an economic headwind to the investment debate here. I'd be looking for KNTK to do 12%+ to fire up the investment cortex.

What shows is that if KNTK continues at its current growth rates, it could spin off $212mm in FCF this year, following a $27mm investment to growth (net of $127mm of CapEx on top of this). Should profits grow at the current rate, this could yield strong incremental returns on capital of ~82%. Curiously enough, the rate of return for shareholders would be driven at the margin of ~21%, as capital turns are low at ~0.4-0.5x of sales. This could be a headwind to the company repricing at higher multiples going forward, because 1) the returns on existing capital below 10%, with reinvestment rates at the c.14% mark.

Ideally, however, you'd see the profitability numbers stretching up. And you'd need more than 12% sales growth to get there, plus, operating margins would need to shift higher in my view. For example, 16% sales growth gets you to $217mm in FCF this year, whereas a 25% operating margin gets you to $255mm in owner earnings this year. This is a c.400bps increase to both, but the latter gets you $43mm in FCF. Hence, the company's forward estimates are most sensitive to operating margin vs. sales. This squares off with the economics of the business. It is difficult to differentiate the 'offering' from competitors. All KNTK's peers offer roughly the same 'product' and/or 'service'. Thus, is it operating leverage that drives the investment value.

{kind=link}

Valuation and conclusion

The stock trades at 14x forward earnings and 10.4x forward EBITDA. Both of these are premiums of 32% and 77%, respectively. I would suggest this is a difficult valuation to work into if the sector is so compressed. But you're also getting a 33% forward cash flow yield buying KNTK today, and that is immense value in my view.

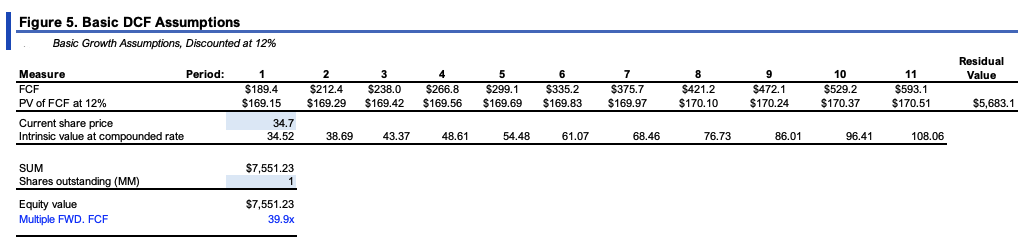

Extending the analysis from Figure 5 forward to the coming 5 years, this gets you to $7.5Bn in market value, around 45% value gap as I write. It would appear the current market multiples offer an attractive starting valuation relative to the cash flows KNTK can produce going forward. This is a potential bullish point and must be factored in to a long-term economic thinking on KNTK.

{kind=link}

In short, there are several bullish points to uncover in the KNTK investment debate. One is the potentially attractive starting multiples, currently at 14x earnings and a 33% cash flow yield. The other is the potential upsides of any improvement in operating margin gets the company's forward cash flows.

But this is a capital intensive business that is not recycling capital at returns higher than what I can get elsewhere. A c.6-7% ROIC each period doesn't cut the mustard in my opinion, as I'm looking for compounders that can return 12%+ on the capital required to run the business. Further, asset-heavy businesses tend to face challenges in an inflationary environment. Replacement costs, running costs, and overall financing are typically more challenged, despite the conventional thinking that 'tangible assets' offer inflation protection. Net-net, despite the positives discussed, it would appear there are more selective opportunities elsewhere. I am still constructive on the valuation numbers spat out here today. Pending on what the company does in H2, this could change the thesis. Net-net, rate hold.

For further details see:

Kinetik: Starting Valuations A Plus, Economic Leverage Balances The Debate