KGSPY - Kingspan Group: Getting Increasingly Attractive

2023-09-18 10:30:00 ET

Summary

- Kingspan, an Irish building materials company, has experienced lower revenue in the first half of the year due to price deflation and increasing building costs in Western Europe.

- Despite the disappointing revenue, Kingspan has shown strong margins and a 2.5% increase in EPS compared to the first half of last year.

- The company has announced an offer to acquire Nordic Waterproofing, but it is unlikely to be able to fully acquire the company at the offered price.

Introduction

Kingspan ( OTCPK:KGSPF ) ( OTCPK:KGSPY ) is a large Irish company focusing on building materials, and more specifically insulation and insulated panels (which, combined, account for almost 80% of the total revenue in the first half of the year. It hasn’t been an easy first semester for the company as there was some price deflation while Western Europe is dealing with increasing building costs.

{kind=link}

The company has a history of strong cash flows but as it is a leader in its segment, the stock has never been really cheap and I was hoping the recent weakness would make the valuation more appealing.

{kind=link}

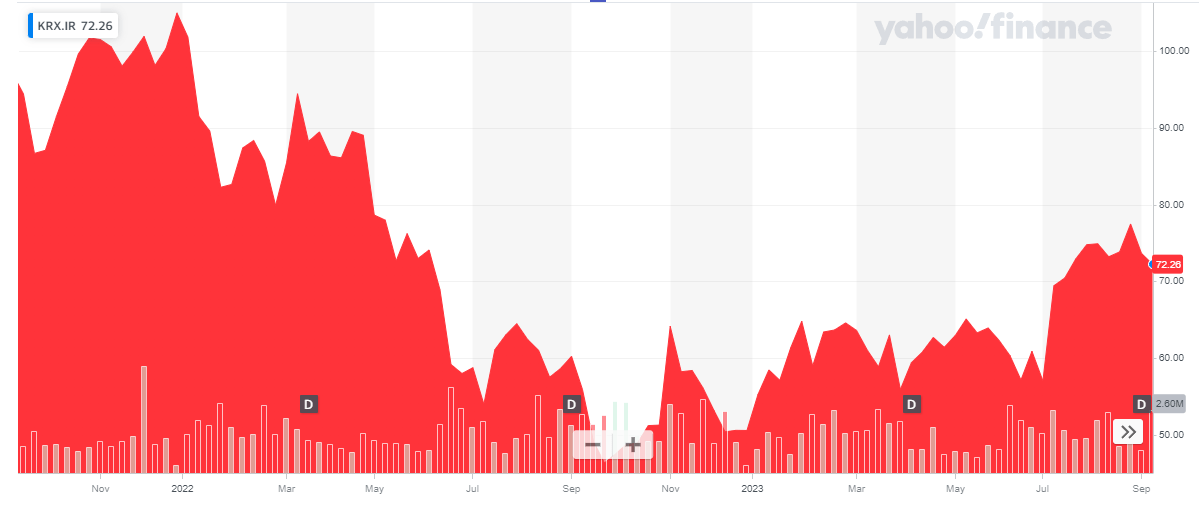

Kingspan is an Irish company and has a primary listing on the Dublin Stock Exchange where it is trading with KRX as its ticker symbol . With an average daily volume of just over 360,000 shares, interested investors should definitely focus on the Irish listing given the average daily monetary value of 25M EUR. The current market capitalization of Kingspan is just over 13B EUR. I will use the Euro as base currency throughout this article.

A closer look at the financial results: lower revenue, but strong margins

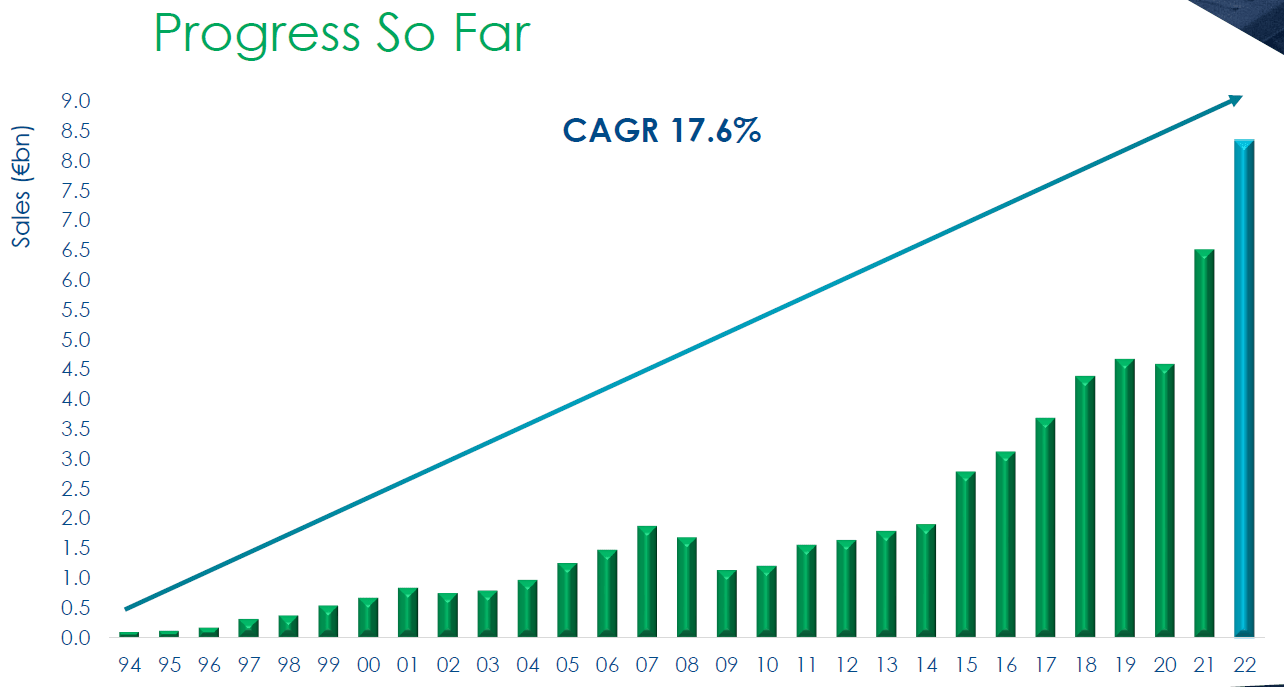

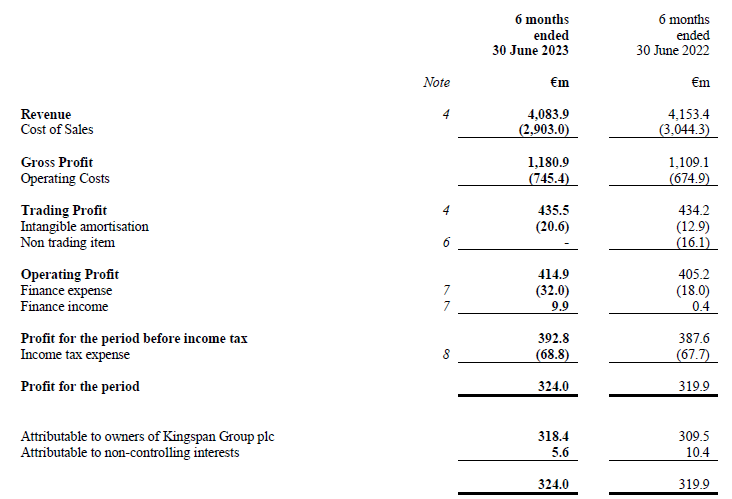

Whereas a supplier like Legrand mentioned it was able to hold its ground in a construction and building market that is contracting, Kingspan is definitely feeling a negative impact. The company reported a 2% revenue decrease in the first half of the current financial year, and the underlying revenue on a comparable basis decreased by 8% as the positive impact of recent acquisitions added about 7% to the revenue. This means we should expect a revenue stagnation this year, but that’s not necessarily bad news. As you can see below, Kingspan has had some bumps along its 30 year growth trajectory but has grown its revenue by an impressive 17.6% per year since 1994 through a combination of organic and M&A driven revenue growth.

{kind=link}

Is this unexpected? Not really. The construction sector can be pretty cyclical and in Kingspan’s case it’s also important to acknowledge the COGS decreased by in excess of 4% and this ultimately resulted in a gross profit increase of in excess of 6%. The trading profit remained flat due to the 10% increase in other operating expenses while the operating profit increased by just over 2% to 415M EUR thanks to lower amortizations and non-recurring items.

{kind=link}

The total interest expenses increased as well and this resulted in a pre-tax income of 393M EUR and a net income of 324M EUR. And of that amount, 318.4M EUR was attributable to the shareholders of Kingspan, resulting in an EPS of 1.75 EUR. That’s a 2.5% increase compared to the first half of last year.

So long story short, the revenue was disappointing, but the gross margin definitely improved and the higher finance expenses were somewhat compensated for by the lower non-recurring items.

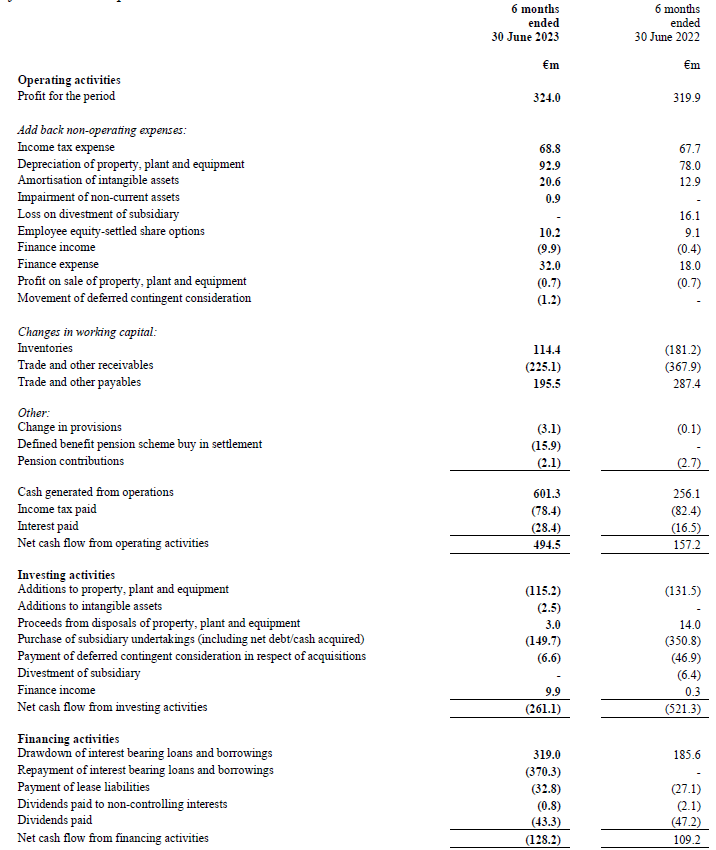

As most of my readers know, I usually focus on a company’s free cash flow performance as it excludes the amortization of the intangibles and shows how much cash flow a company is really generating.

The reported operating cash flow generated by Kingspan in the first half of the year was 495M EUR but this includes 78.4M EUR in taxes paid although only 68.8M EUR was due (based on the H1 income statement). Additionally, there was a positive impact from working capital changes to the tune of 85M EUR and we still need to deduct the 33M EUR in lease payments and the 1M EUR in dividends to non-controlling interests.

{kind=link}

This means the adjusted operating cash flow was approximately 386M EUR. And with a total capex of 118M EUR (including 2.5M EUR spent on intangibles), the underlying free cash flow was approximately 268M EUR.

That is indeed quite a bit lower than the attributable net income of 318M EUR and this difference could easily be explained by Kingspan’s investment push. The total depreciation and amortization expenses increased to 113M EUR but the total capex was approximately 151M EUR (118M EUR in capex and 33M EUR in lease payments) and that 38M EUR difference covers almost the entire difference between the free cash flow and the net income.

A second element is the 16M EUR cash payment into its pension scheme. That is not an expense but it does represent a net cash outflow and that obviously also weighed on the operating and free cash flow results.

As of the end of June, Kingspan had 761M EUR in cash, 258M EUR in short-term debt and 1.88B EUR in long-term debt (this excludes lease liabilities and the deferred contingent consideration) for a total net debt of 1.37B EUR. Considering the EBITDA in the first half of the year was 528M EUR and the analyst consensus estimate for the full-year EBITDA is 1.06B EUR, the debt ratio is very acceptable and the company will likely end the year with a net debt to EBITDA ratio of less than 1.5 (of course subject to changes in the working capital position).

Meanwhile, M&A remains a possibility . Earlier this month, a news story hit the wires how Carlisle Companies ( CSL ) rejected an informal approach from Kingspan . Both companies have similar market capitalizations so a merger could potentially make sense but Kingspan has subsequently downplayed the news and said it is not actively engaging with Carlisle .

That doesn’t mean Kingspan is sitting on its hands. It also announced it is making an offer to acquire Nordic Waterproofing for 160 SEK per share but as the offered premium is relatively low and as Kingspan was forced to make an offer after exceeding the 30% share position threshold and it looks like this offer is just a pro forma bid to respect the takeover regulations and I don’t expect Kingspan to be able to fully acquire Nordic Waterproofing at that price level.

Investment thesis

I realize Kingspan has never been cheap and it isn’t even cheap right now. But with a strong market position, a ROIC that has been consistently in the high-teens and the cash flow performance still intact in what definitely was a difficult first semester, I may initiate a small starter position.

While I’m usually not too keen on large M&A deals, I also acknowledge Kingspan’s management has a decent record of integrating acquisitions into the corporate structure. But I would rather see Kingspan continuing to gobble up smaller players in its industry (like Nordic Waterproofing) instead of pursuing a mega-deal with Carlisle.

I am in no rush to go long Kingspan as the share price has been trading between 50 and 60 EUR for the majority of this year before breaking out over the summer. I am waiting for weakness before buying the stock.

For further details see:

Kingspan Group: Getting Increasingly Attractive