KFS - Kingsway: Run-Rate Adjusted EBITDA Of $20 Million As Acquisitions Resume (Rating Upgrade)

2023-10-25 21:51:05 ET

Summary

- The company has announced two acquisitions over the past two months, the first ones under its KSx program since November 2022.

- While they were made at higher multiples than before, Kingsway’s EV/EBITDA ratio should improve.

- Kingsway now has an adjusted EBITDA run-rate of around $20 million, and I think the company should be trading at above 12x EV/EBITDA.

Introduction

In June, I wrote an article on SA about Kingsway Financial Services (KFS) in which I said that it looked expensive based on fundamentals and that I was concerned that it hadn't added a new company to its Kingsway Search Xcelerator (KSx) platform for over 7 months.

Well, Kingsway Financial Services has completed two acquisitions over the past two months which should push its run-rate adjusted EBITDA to around $20 million per year. In addition, I think the company booked decent Q2 2023 financial results, and considering the market capitalization has fallen by just over 20% since my previous article, I feel comfortable upgrading my rating on the stock to speculative buy. Let’s review.

Overview of the recent developments

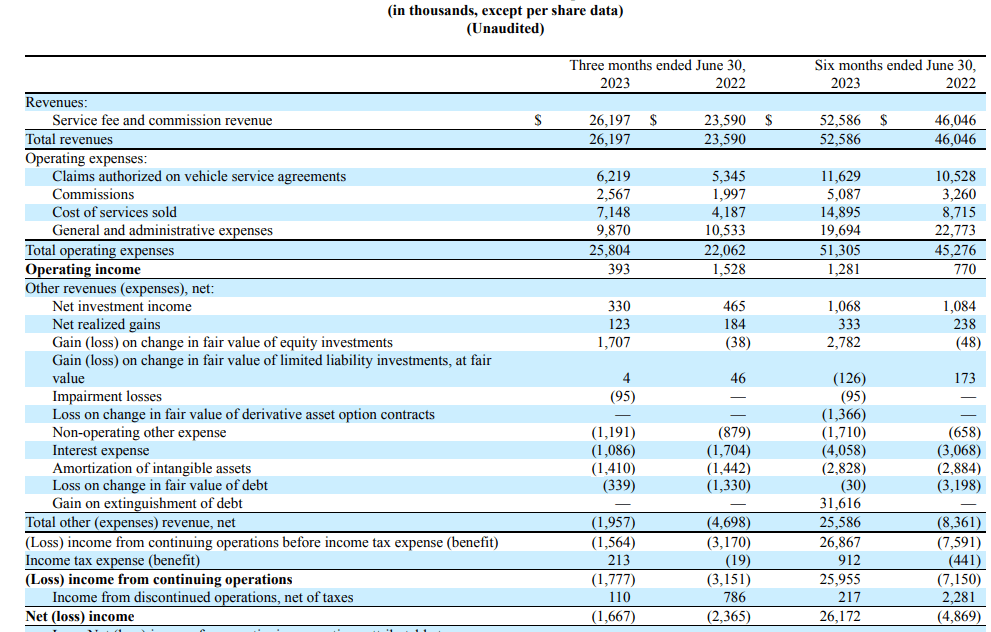

If you aren't familiar with the company or my earlier coverage, here's a brief description of the business. Kingsway was established in 1989 as a specialty insurance company but it had to embark on a restructuring plan in the midst of the Great Recession as many of its insurance contracts were significantly mis-underwritten. The company pivoted to the extended warranty services business through several small purchases over the following years and then in 2021 it decided to focus on investing in small and growing companies with recurring revenues and high margins that have an asset-light business model under a program that is today called KSx. By the end of 2022, Kingsway had bought three companies at between 4x and 4.5x EV/EBITDA - outsourced accounting and HR firm Ravix for $11 million, financial executive solutions provider CSuite for $8.5 million, and staffing agency Secure Nursing Service ((SNS)) for $10.9 million. In addition, Kingsway sold its home warranty business, PWSC, and the majority of its property business between July 2022 and February 2023 in a bid to strengthen its balance sheet. Looking at the latest available financial results, we can see that revenues rose by 11.1% year on year to $26.2 million in Q2 2023. The revenues of the warranty business went down by $2.4 million to $17 million, with $2.1 of the decrease being attributable to PWNI which was sold in July 2022. The revenues of the KSx companies, in turn, soared by 121% to $9.2 million mainly thanks to the addition of CSuite and SNS in November 2022. Adjusted EBITDA went down to $1.8 million from $3.1 million a year earlier but this was due to the sale of PWNI. Excluding the financial results of the latter, the combined pro forma adjusted EBITDA of Kingsway for Q2 2023 came in at $3.4 million compared to $3.3 million a year earlier. The company said that its run-rate adjusted EBITDA for its operating companies was at $18 million to $19 million on a TTM basis. In addition, I find it encouraging that interest expenses decreased by over a third to $1.1 million considering many companies are being negatively affected by rising interest rates nowadays.

{kind=link}

Looking at the balance sheet, Kingsway continued to decrease its debt load as its net debt came in at $27.9 million as of June compared to $35.8 million as of March and $37.9 million at the end of 2022. That being said, the company’s net debt could be slightly higher at the end of 2023 as it announced two acquisitions over the past two months – software developer Systems Products International on September 11, and clinical trial site management and recruitment services provider National Institute of Clinical Research on October 23. The price for Systems Products International was $2.7 million while 95% of National Institute of Clinical Research is being bought for $7.9 million. Yet, I think that this is a positive development as these are the first acquisitions for 2023 under the KSx program after a long pause and the two companies have combined annual revenues of $9.2 million and EBITDA of $1.5 million on a TTM basis ( for Systems Products International, financials were revealed at a conference call at the 3:50 mark here ). While the EV/EBITDA multiples for both acquisitions are much higher than previous purchases (9x for Systems Products International and 6.9x for National Institute of Clinical Research), they should still improve Kingsway’s multiples. The company has an enterprise value of $211.9 million as of the time of writing and is trading at 11.5x EV/EBITDA using the midpoint of the $18-19 million adjusted EBITDA run-rate given by the company. Assuming conservatively that the acquisitions of Systems Products International and National Institute of Clinical Research increase net debt by $10.6 million (combined purchase price) and their combined EBITDA remains unchanged at $1.5 million for the foreseeable future, the enterprise value would grow to $222.5 million while the midpoint of the adjusted EBITDA run-rate increases to $20 million, pushing down the EV/EBITDA multiple to 11.1x. As Kingsway is accelerating its shift to asset-light businesses with high growth and strong margins, I think the company should be worth over 12x EV/EBITDA and there is now a decent margin of safety here thanks to the recent share price weakness (the market capitalization is down just over 23% over the past two months).

Turning our attention to the downside risks, I think that there are two major ones. First, some of the KSx platform businesses are sensitive to macroeconomic headwinds which means that revenue and EBITDA growth could face challenges in the current environment due to high interest rates and slowing economic growth. Second, Kingsway’s warranty business has been struggling lately with negative revenue growth, and with a lack of catalysts on the horizon, this seems unlikely to change in the next few quarters.

Investor takeaway

Kingsway has resumed acquisitions under its KSx platform following a pause of 10 months and although the latest two acquisitions were made at higher multiples than before, they should still improve the company’s EV/EBITDA ratio. In my view, Kingsway should be trading above 12x EV/EBITDA based on an adjusted EBITDA run-rate of $20 million, and the slump in the market capitalization over the past two months has created a good opportunity to open a position here.

For further details see:

Kingsway: Run-Rate Adjusted EBITDA Of $20 Million As Acquisitions Resume (Rating Upgrade)