KNSA - Kiniksa Pharmaceuticals: Early 2024 Corporate Update A Mixed Bag

2024-01-05 16:29:47 ET

Summary

- Kiniksa Pharmaceuticals, Ltd.'s phase 2 results for KPL-404 in rheumatoid arthritis were unimpressive, and the company should quickly switch focus to other indications.

- The commercial uptake of Arcalyst continues to impress with net sales guidance exceeding consensus.

- Kiniksa plans to expand its sales force for Arcalyst, which is expected to drive further better-than-expected growth in the recurrent pericarditis market.

Shares of Kiniksa Pharmaceuticals, Ltd. ( KNSA ) were volatile after the company provided one very positive update on Arcalyst and another update that I can only say is mixed at best, but essentially negative – the phase 2 results of KPL-404 in patients with rheumatoid arthritis ("RA"). My view on KPL-404 remains the same – the company should quickly put the RA trial behind it and focus on other less prevalent diseases where this candidate can make a difference. The focus should quickly turn back to the commercial uptake of Arcalyst, and it continues to impress, with the full-year net sales guidance range of $360-380 million coming in well above the $351.5 million consensus.

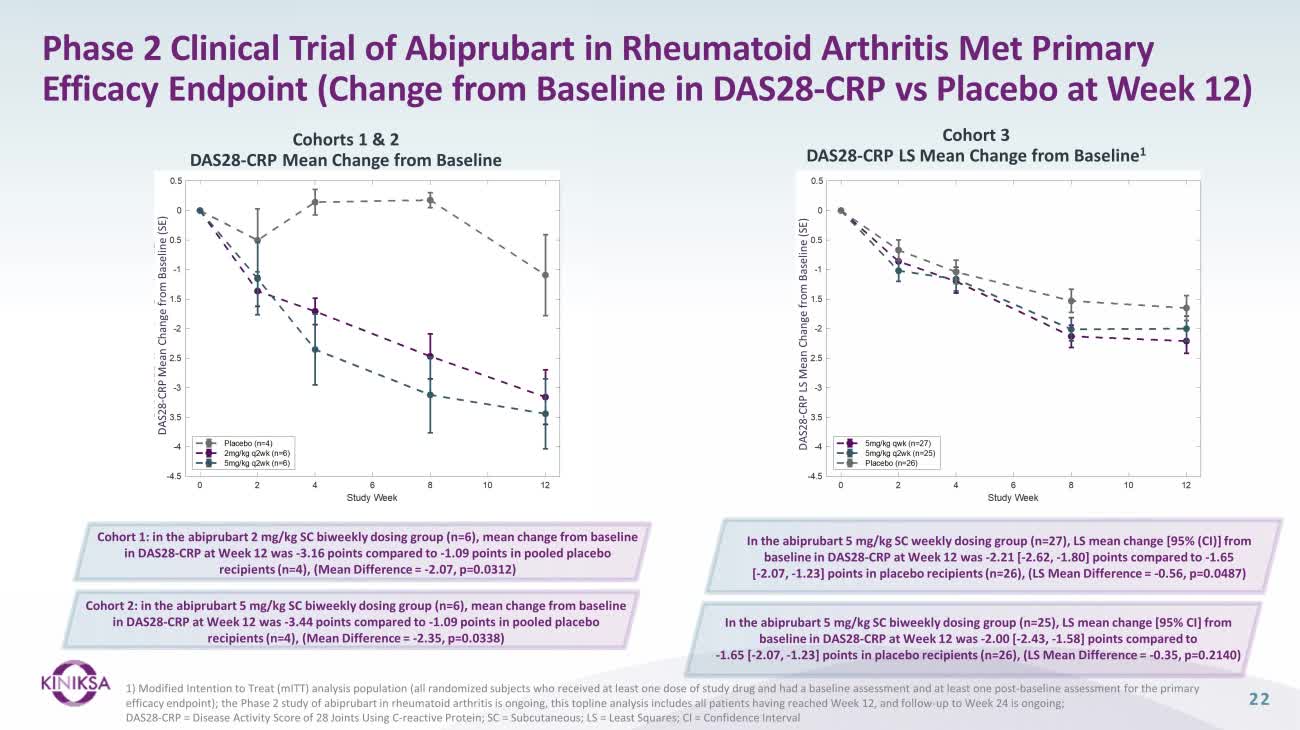

KPL-404 (abiprubart) delivers unimpressive RA data

I said last year that this was not a catalyst worth waiting for and that rheumatoid arthritis should not be an indication of interest for this asset because there are more interesting and less prevalent diseases to go after and because the data from competitors was not particularly impressive either. It turned out KPL-404 was no different and it too has failed to impress in the RA population.

The two initial cohorts of KPL-404 looked good compared to placebo but such is the nature of very small cohorts as it can provide false signals. The larger third cohort provided a better glimpse of how effective KPL-404 was on the primary efficacy endpoint of DAS28-CRP – it was barely numerically better than placebo, and the results did not reach statistical significance. The mean change from baseline was in line with data Horizon, now part of Amgen ( AMGN ), reported with dazodalibep.

Kiniksa Pharmaceuticals investor presentation

{kind=link}

Granted, there are some positive biomarker signals even in the third cohort and safety looked clean, but overall, KPL-404 does not look like a promising candidate for the treatment of rheumatoid arthritis.

This is not the end of RA trial updates. There is still cohort 4 where KPL-404 is dosed every four weeks and this cohort should inform the dosing schedule for future trials.

My view remains the same – the company should quickly move on and start trials in indications where there are better efficacy signals and where KPL-404 can be priced as a rare disease drug.

I was not assigning value to KPL-404 in RA, or other indications, so, the unimpressive results make no difference to my expectations.

Arcalyst continues to perform well; the 2024 guidance range looks realistic

I was initially impressed by the full-year 2024 Arcalyst revenue guidance as it was well above the Street consensus, but I do wonder if it was provided to limit the damage from the unimpressive KPL-404 data and whether we will see the company beat and raise throughout 2024. Even so, Arcalyst’s trajectory looks strong, and it would not be a disaster even if the net sales end up at the low end of the $360-380 million guidance range.

Management does have a mixed guidance record. At the start of 2022, they guided for full-year Arcalyst net sales of $115-130 million and kept it unchanged throughout the year, and delivered $122.5 million, which was right at the mid-point of the initial and only guidance range.

Management got better at managing expectations in 2023 when the initial guidance range was $190-205 million and they raised it to $200-215 million after the first quarter report, and to $220-230 million after the second quarter report. The range was unchanged after the third quarter report, but management did note net sales were trending toward the high end of the range. They managed to exceed the high end by reporting $233.1 million in net sales in 2023.

Based on the execution in 2023, the guidance for 2024 does not look very demanding. I would expect Arcalyst net sales to be closer to the high end of the $360-380 million range. The question is whether there is upside from that guidance range as analysts will adjust expectations accordingly, and the upside may be limited if execution is in line and if there are no increases in the full-year guidance range.

The chart below shows a rough estimate of what sequential net sales need to look like for Arcalyst to hit the high end of the guidance range and the trailing 4-quarter average.

Kiniksa Pharmaceuticals earnings reports, author's estimates

Q1 is the worst quarter of the year due to seasonal factors, and we see generally strong sequential growth for the remainder of the year. The expected growth to get to $380 million in 2024 looks somewhat demanding but ultimately achievable through increased adoption, improved productivity of the existing sales force, and additional sales force expansion.

Kiniksa announced plans to further expand the sales force from 50 reps at the end of 2023 to 85 reps, which the company believes will be sufficient to cover 85% of the recurrent pericarditis population in the United States, up from 70% with 50 reps, and to reach 11,000 top and mid-tier prescribers compared to 7,000 previously.

A step-up in sequential sales from the late 2022 sales force expansion can be seen in the chart I shared earlier, and the inflection point was almost immediate in Q2 2023 and after a seasonally slow Q1. We should see a similar or even better impact in absolute numbers since the number of new reps this year is 35 versus 20 last year.

There is still plenty of room for growth, as Arcalyst has just scratched the surface in the U.S. recurrent pericarditis market. The company estimates that market penetration at the end of 2023 was around 9%.

I have kept my long-term revenue estimate range unchanged since launch at $600-700 million, as it was tracking generally between the lower end of the range and the mid-point, but the change in the trajectory in 2023, the expected effect of the additionally expanded sales force, and what I see as at least achievable guidance have improved the outlook. I am tightening up the range to $650-700 million, which increases the lower end of the valuation range from $25 to $27 and the new range is $27-30 per share.

Conclusion

The results from the phase 2 trial of KPL-404 are underwhelming but ultimately not relevant and I expect Kiniksa Pharmaceuticals, Ltd. to quickly switch its focus to less prevalent diseases such as Sjogren’s syndrome. The improved outlook for Arcalyst is what matters in the near and medium term.

For further details see:

Kiniksa Pharmaceuticals: Early 2024 Corporate Update A Mixed Bag