KNSA - Kiniksa's Diversified Pipeline Augments Arcalyst Potential

2023-10-06 05:54:29 ET

Summary

- Kiniksa's Arcalyst shows strong clinical efficacy in recurrent pericarditis, driving revenue potential conservatively estimated at $300-400 million.

- Solid financials, including a long cash runway and robust current ratio, add confidence; however, patent vulnerabilities and Regeneron obligations pose risks.

- Considering growth prospects and financial stability, but acknowledging inherent risks, the investment recommendation leans towards a "Strong Buy."

At a Glance

Kiniksa Pharmaceuticals (KNSA) finds itself at a pivotal juncture, both clinically and financially. On the clinical front, Arcalyst is rapidly carving out a substantive role in the niche yet significant market of recurrent pericarditis. A 96% risk reduction in recurrence implies not just a revenue stream but potentially a new standard of care. However, vulnerabilities such as expiring composition-of-matter patents and obligations to Regeneron (REGN), including a 50/50 profit split, put a slight damper on the robustness of the asset. Financially, a cash runway extending into 2027 and a current ratio of 5.2 indicate solid footing, although operational shifts, especially in R&D, could alter this trajectory. Coupled with an enterprise valuation appearing to underestimate pipeline potential, Kiniksa's profile is rife with actionable insights for a discerning investor eyeing long-term stakes in biotech. Therefore, the stock invites a closer examination for those navigating the risk-reward matrix of the healthcare sector.

Q2 Earnings

To begin my analysis, looking at Kiniksa Pharmaceuticals' most recent earnings report for Q2 2023, the company posted a notable uptick in total revenue to $71.5M, up from $27M in Q2 2022, mainly driven by a surge in both product revenue ($54.5M) and new streams of license and collaboration revenue ($17M). The increase in operating expenses to $74.6M, however, led to a narrow operating loss of $3.2M, improved from a $19.4M loss YoY. Encouragingly, a tax benefit turned a pre-tax loss into a net income of $15M. Share dilution remains minimal, with weighted average common shares outstanding increasing from 69.3M to 69.9M in basic terms.

Financial Health

Turning to Kiniksa Pharmaceuticals' balance sheet , as of June 2023, the firm reported 'cash and cash equivalents' of $112.6M and 'short-term investments' of $72.4M, totaling to $185M in highly liquid assets. The company's 'total current assets' amount to $246M, and when juxtaposed against 'total current liabilities' of $47.5M, the current ratio is a robust 5.2. Over the last six months, 'Net cash used in operating activities' was $8M, translating to a monthly cash burn of approximately $1.33M. Accordingly, the company's cash runway is roughly 139 months under current conditions. It's imperative to note that these values and estimates are based on past data and may not necessarily forecast future performance.

Given a substantial cash runway and a robust current ratio, the necessity for Kiniksa to secure additional financing within the next twelve months seems low. However, unforeseen R&D expenses or market variables could alter this outlook. These are my personal observations, and other analysts might interpret the data differently.

Equity Analysis

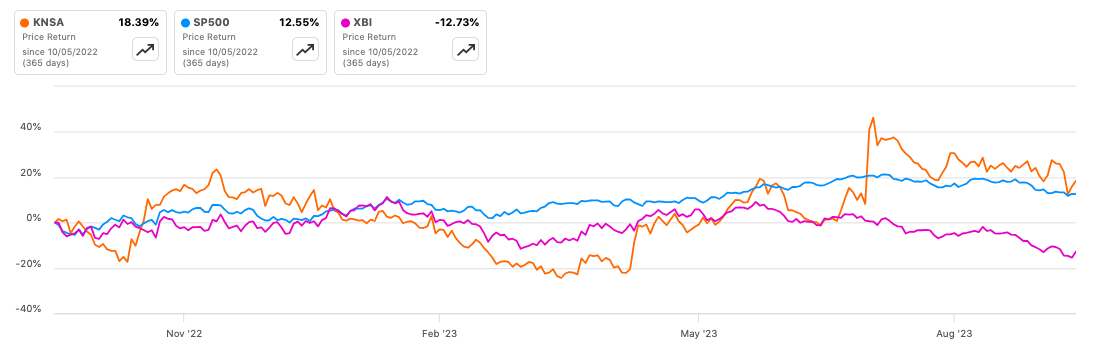

According to Seeking Alpha data, Kiniksa Pharmaceuticals has a market capitalization of $1.12B, signaling a moderate level of market confidence, supported by a YoY revenue growth projection of 16.23% to $255.92M for 2023. Relative to SPY, KNSA's 12-month momentum at +12.51% is slightly underperforming, but its 6-month gain of +51.75% indicates positive short-term dynamics.

{kind=link}

Options expiring in January show higher open interests at $17.50 calls, indicating market sentiment is cautiously bullish and projecting limited volatility. Short interest is 12.77%, a level high enough to be a concern for potential short squeezes. Ownership is primarily institutional at 44.06%, hinting at a general endorsement by sophisticated investors. New institutional positions outnumber sold-out positions, contributing to a net positive influx of shares. Insider trading has been relatively limited , not signaling strong sentiment in either direction.

Arcalyst: A Heartening Solution for Pericarditis

Kiniksa Pharmaceuticals' Arcalyst (rilonacept) is progressively cementing its role in the treatment of recurrent pericarditis, a market with an incidence rate of approximately 6.0 cases per 100,000 persons per year in the U.S. This translates to a potential patient pool of around 19,800 given the current U.S. population. Priced at about $20,000 per month , Arcalyst targets a high unmet need with its dual inhibition of IL-1? and IL-1? cytokines, a mechanism that has demonstrated a 96% reduction in the risk of recurrence .

Financially, a conservative peak annual revenue for Arcalyst could range between $300 to $400 million. This estimate assumes robust market penetration, retention rates, and a stable pricing environment. Clinicians appear to increasingly adopt Arcalyst, reflected by the over 1,250 prescribers and 50% of patients resuming therapy within 8 weeks of discontinuation.

On the patent front, Arcalyst enjoys a strong protective landscape . Two key U.S. method-of-use patents extend its protected term until 2038, specifically for recurrent pericarditis. The international patent portfolio is also substantial, with 25 granted patents in multiple jurisdictions including Europe, Asia, Canada, and Australia. Pending patent applications in these regions could further reinforce this position. Additionally, the FDA's granting of a seven-year marketing exclusivity in the U.S. as of March 2021 adds another layer of competitive edge.

However, there are points of vulnerability. The U.S. composition-of-matter patent expired in 2020, and its international counterparts are expected to expire in 2023. While the method-of-use patents and FDA-granted exclusivity offer some protection, the absence of a composition-of-matter patent introduces the risk of competitive formulations. Additionally, the strength of these patents is contingent on the terms of the ongoing Regeneron Agreement .

In summary, Arcalyst appears poised for significant market penetration in the treatment of recurrent pericarditis, bolstered by compelling clinical data and a strong patent portfolio. Yet, it is crucial to consider potential vulnerabilities, including the expiry of composition-of-matter patents and the dependencies tied to the Regeneron Agreement.

Beyond Pericarditis: Kiniksa's Quiet Arsenal

Building on the strengths and market potential of Arcalyst, it's worth noting that Kiniksa Pharmaceuticals isn't a one-trick pony. The company has a diversified pipeline that extends beyond recurrent pericarditis.

-

KPL-404: Targeting the CD40-CD154 interaction, this monoclonal antibody is currently in a Phase 2 clinical trial for rheumatoid arthritis, with data expected in the first half of 2024. If successful, KPL-404 could provide a new approach to a market where the demand for targeted therapies remains strong.

-

Mavrilimumab: This monoclonal antibody targets GM-CSFR? and is under investigation for its potential role in rare cardiovascular diseases. Kiniksa's pursuit of collaborative study agreements suggests a strategic approach to risk-sharing and may accelerate the drug's time-to-market, given that GM-CSF mechanisms are increasingly recognized in cardiovascular pathology.

-

Vixarelimab: With a $15.0 million development milestone achieved in Q2 2023, this monoclonal antibody, inhibiting signaling through OSMR?, is under a global license agreement with Genentech. The milestone implies that the asset has met specific development criteria, signaling promising progress and potentially adding another revenue stream to Kiniksa's portfolio. Cumulatively, Kiniksa could receive approximately $600M in contingent payments. Importantly, the agreement also includes tiered royalties on annual net sales that range from low-double digits to mid-teens, subject to specific conditions.

My Analysis & Recommendation

In wrapping up the financial and clinical landscape surrounding Kiniksa Pharmaceuticals, several salient points come into focus for discerning investors. Firstly, Arcalyst's annual revenue potential, positioned conservatively at $300-400 million, presents a substantial upside. Let's not overlook that profits from recurrent pericarditis treatments are subject to a 50/50 split with Regeneron, but even with that in consideration, the revenue stream appears robust. Coupled with Kiniksa's diversified assets like KPL-404 and Mavrilimumab, and partnerships with big pharma, the revenue prospects look favorable.

From a valuation standpoint, an enterprise value under $1 billion appears undervalued when contrasted with the revenue prospects of Arcalyst alone, let alone the entire asset portfolio. Financial health indicators such as a strong current ratio of 5.2 and a cash runway extending into 2027 add layers of comfort for long-term investment.

In terms of immediate catalysts, investors should closely monitor clinical data for KPL-404, expected in 1H 2024, which may present a substantial inflection point. Keep an eye on how the market reacts to options expirations, particularly given the cautiously bullish market sentiment and the risk of short squeezes given a 12.77% short interest. Any movement in institutional buying could provide added confidence, especially if it shifts the risk-reward paradigm further into the "reward" category.

However, don't dismiss the risks tied to expiring composition-of-matter patents and vulnerabilities in the Regeneron Agreement. These are not just footnotes; they could become focal points that may alter the risk profile of Kiniksa.

In conclusion, the confluence of market need, strong financials, and strategic partnerships positions Kiniksa as a compelling opportunity. The firm's valuation may yet reflect some market skepticism, but the fundamentals suggest a strong growth trajectory. Therefore, considering the outlined factors and a prudent risk assessment, my investment recommendation for Kiniksa is a "Strong Buy."

Investors would be well-advised to conduct further due diligence but should be prepared to act swiftly on upcoming catalysts that could further validate Kiniksa's value proposition.

Risks to Thesis

While my overarching recommendation for Kiniksa Pharmaceuticals is a "Strong Buy," several factors could challenge this stance. Firstly, a market cap of $1.12B in the volatile biotech sector introduces valuation risks, especially if Arcalyst doesn't secure its place as the standard of care for recurrent pericarditis. Secondly, the market's appetite for new therapies could be smaller than projected, putting peak revenue estimates for Arcalyst at risk. Thirdly, my analysis might underemphasize the competitive threats that could come with the expiry of the composition-of-matter patents. Lastly, a 12.77% short interest signifies that a portion of the market is betting against the stock; an adverse event could trigger a short squeeze, leading to volatile price movements. Therefore, while the stock shows promise, due diligence should include these potential counterpoints.

For further details see:

Kiniksa's Diversified Pipeline Augments Arcalyst Potential