K:CC - Kinross Gold: An Underwhelming Reserve/Resource Update

Summary

- Kinross released a maiden resource for its newly acquired Great Bear Project in Red Lake, as well as updated mineral resources/reserves last month.

- Unfortunately, the maiden resource at Great Bear came in well below my estimates and likely below most investors' expectations, reinforcing the view that it overpaid for GBR.

- Meanwhile, the level of reserve replacement was disappointing at existing assets as well, especially considering the 17% hike in the gold price assumption ($1,400/oz vs. $1,200/oz) to inform reserves.

- While KGC remains reasonably valued after 2 years of underperformance, I continue to see more attractive opportunities elsewhere, especially following the underwhelming Great Bear update.

The Q4 Earnings Season for the Gold Miners Index (GDX) is nearly complete, which means we get a look at how companies have done regarding replacing mining depletion and improving their pipeline for future potential conversion to reserves. While most companies reported positive reserve replacement among the majors given that we've seen gold price assumptions increased after years of holding assumptions at or below $1,300/oz, one name with disappointing reserve replacement was Kinross Gold ( KGC ). In fact, despite a 17% increase in its gold price assumption and excluding divestments, Kinross still saw a 7% decline in mineral reserves year-over-year, with material declines at key assets on a two-year basis (Tasiast, Paracatu, Fort Knox, Round Mountain).

The hope was that the Great Bear Project would exceed estimates and more than offset the lost ounces in the measured & indicated [M&I] category following a loss of ~2.77 million ounces from Chulbatkan, Dvoinoye/Kupol, and Chirano. However, the resource update didn't show nearly the ounces I expected, and didn't even cover the lost ounces from these assets. Worse, language around the project has changed for the worse, and while it could come close to Tier-1 status from a scale standpoint, I certainly don't see this being the case with a 10,000 tonne per day footprint over the life of mine. Let's take a closer look below:

{kind=link}

2022 Reserve & Resource Update

Kinross Gold released its FY2022 Reserve & Resource estimates last month, reporting total mineral reserves of ~25.5 million ounces of gold, and total M&I resources (exclusive of reserves) of ~26.2 million ounces of gold, plus ~10.5 million ounces of inferred resources. This represented a decline of over 20% in total gold reserves year-over-year, or ~7% when excluding the impact of its divestments (Chulbatkan, Kupol/Dvoinoye, and Chirano). Given that several majors posted solid reserve replacement, the results here were not ideal, especially when incorporating the increase in the gold price assumption from $1,200/oz to $1,400/oz.

Meanwhile, as the chart below shows, M&I resources fell 8% year-over-year despite the benefit of the massive Great Bear acquisition which represented ~20% of Kinross' market cap, and which was done near a cyclical peak for the gold developers (Q4 2021). Finally, inferred resources increased 15% (9.1 to 10.5 million ounces). The growth in inferred resources was solely due to the Great Bear Project contribution (~2.30 million ounces), and one would hope this segment would increase given the price paid for Great Bear of ~$1.39 billion before factoring in the contingent consideration discussed at the time of the acquisition (~$50 million).

Kinross - Total Reserves, M&I Resources & Inferred Resources (Company Filings, Author's Chart)

{kind=link}

Digging into the assets from a mine by mine standpoint, we can see a clear downtrend in mineral reserves at multiple assets, with a significant decline at Tasiast (~5.74 million ounces vs. ~6.4 million ounces), Paracatu (~6.6 million ounces vs. ~7.3 million ounces), Round Mountain (~2.2 million ounces vs. ~3.0 million ounces), and Bald Mountain (~625,000 ounces vs. ~1.14 million ounces in 2020 and ~798,000 ounces last year). Worse, not only did reserves decline but so did the grades at several assets, with Bald Mountain's grades declining to 0.50 grams per tonne gold (0.60 grams per tonne gold previously) and Tasiast's grades dipping to 1.7 grams per tonne of gold vs. 1.80 grams per tonne previously.

Kinross - Mineral Reserves by Mine (Company Filings, Author's Chart)

{kind=link}

Regarding the total grade of the reserve base, the loss of higher-grade assets impacted total reserve grades further, with two higher-grade assets divested with average reserve grades of 2.0 and 5.6 grams per tonne of gold, respectively (Chirano, Kupol). Meanwhile, Kinross lost significant ounces (~3.0 million ounces) from Chulbatkan which was expected to lift the company's margins on a consolidated basis post-2025 based on expectations of sub $650/oz all-in-sustaining costs [AISC] at the Russian asset. Lastly, La Coipa's grades dipped slightly, from 1.70 grams per tonne of gold to 1.60 grams per tonne of gold, resulting in a much lower reserve grade across the company combined with lower total gold reserves.

Kinross - M&I Resources by Mine (Company Filings, Author's Chart)

{kind=link}

Moving over to M&I resources, we saw a similar trend here, with sharp declines in M&I resources at Fort Knox and Tasiast, with a combined decline of ~1.67 million ounces at these two assets. This was partially offset by increases in M&I resources at Paracatu, Round Mountain, and Bald Mountain, plus a slight increase in resources at Kettle River, plus the maiden indicated resource of ~2.7 million ounces at Great Bear (~33.1 million tonnes at 2.57 grams per tonne gold). However, we saw a net loss in M&I resources due to the divestments of several assets across the portfolio last year (Chirano, Kupol/Dvoinoye, Chulbatkan). Plus, while we did see an increase in M&I resources, grades fell considerably.

At Bald Mountain, grades fell to 0.50 grams per tonne of gold vs. 0.60 grams per tonne of gold. At Tasiast, M&I grades fell to 1.0 grams per tonne of gold in addition to the sharp decline in total resources. Lastly, when it comes to inferred resources, Great Bear did help to pull up the total figure and offset divestments, but inferred resources slipped at most assets. This included declining inferred resources at Bald Mountain ([-] 147,000 ounces), Fort Knox ([-] 399,000 ounces), and Paracatu ([-] 661,000 ounces), offset by an increase in inferred resources at Tasiast and Round Mountain. In summary, there wasn't any reason to be elated with Kinross' reserve & resource update, with nearly every category down despite the benefit of a major acquisition.

To put this in comparison, Gold Fields ( GFI ) did not complete any major acquisitions in 2022 yet saw only a moderate decline in M&I resources of [-] 3%, and only a 2.6% decline in mineral reserve following the same increase to an updated reserve price of $1,400/oz to incorporate inflationary pressures, well below the decline seen in reserves by Kinross after adjusting for the impact of divestments.

Great Bear Project

For those unfamiliar, Kinross acquired Great Bear Resources in Q1 2022, with a total purchase price of ~$1.39 billion, or ~$1.40 billion when including a potential contingent consideration (assuming 8.5 million ounces of gold are proven up). This was a significant price to pay for a company without a resource estimate, especially in what was a relatively frothy environment for many developers, with the Asa Gold & Precious Metals Fund ( ASA ) up nearly 180% from its cyclical low in 2018. I noted at the time that I ranked this acquisition as an 8/10 for quality and its fit in Kinross' portfolio for three reasons:

1) The long-term potential for this asset appeared to be 10.0+ million ounces of gold in a safe jurisdiction (helping balance its Tier-3 jurisdiction assets like Ghana, Russia).

2) The project sat on a massive land package next to existing infrastructure along Highway 105 in Red Lake with a transmission line running along the length of the property.

3) Kinross was extremely bullish on project economics in its initial update with figures that exceeded my expectations, noting Tier-1 potential (500,000+ ounces per annum) and AISC between $600/oz to $800/oz, which would have made this one of the highest margin assets globally.

This 8/10 ranking for the acquisition assumed that the third point came to fruition because Kinross paid up massively, acquiring Great Bear with the stock up ~5,000% (C$29.00 vs. C$0.50) in barely three years. When paying a premium of this magnitude even in a mature uptrend for a stock and nearly a $1.5 billion price tag, the only way that this could be justified is if Great Bear was likely to deliver a maiden resource of 7.5+ million ounces which might have justified its $1.1+ billion valuation. However, the maiden resource delivered by Kinross came in at just 5.02 million ounces of gold, well below my estimate (7.0+ million ounces) and certainly below what many expected based on Kinross' unbridled enthusiasm in its initial update on the project when the acquisition was announced.

Not only did this maiden resource disappoint from a scale standpoint, but it highlights Kinross's lack of discipline from an M&A standpoint that some might have thought was in the rearview mirror after an expensive acquisition and subsequent divestment of Aurelian when the project ran into issues, and the mega Red Back Mining acquisition for $7.0+ billion. To be fair, management has changed since the previous two major acquisitions, which is why I was cautiously optimistic we wouldn't see a repeat of a mega-deal near a cyclical peak with a very generous offer. However, with an acquisition price of ~$507/oz on M&I resources, this was more expensive than Newcrest's ( NCMGF ) acquisition of Brucejack (~$386/oz on M&I resources), but that was partially justified because it was scooping up a producing asset.

Kinross Gold - Great Bear Project Maiden Resource (Company Presentation)

{kind=link}

My view on this lack of discipline on Kinross's part is because Great Bear's stock was heavily overbought and not cheap at the time of the acquisition (even before the 20% plus premium) given that investor expectations were for a maiden resource of 8.0+ million ounces of gold (M&I + inferred ounces combined). If Great Bear did not have the fortune of Kinross coming in with a very generous offer and had dropped a ~4.0 million ounce resource into the market, I believe the stock likely would have dropped over 35% on the news, sinking back to reality after two years of there being a relentless bid under the stock during any dips. If Kinross still wanted to acquire the project, it likely could have done so closer to C$22.00 per share (including premium) once the air inevitably came out of the stock, not at ~C$29.00.

{kind=link}

Some investors might believe that this is a stretch, but I completely disagree. This is based on Kinross drilling an additional 250,000 meters (just less than total meters drilled by Great Bear) since acquiring the project, suggesting that Great Bear wouldn't have had the required drill spacing to prove up over 2.0 million ounces in the M&I category, or over 4.0+ million ounces total when reporting its much-awaited maiden resource. Plus, resource scale aside, the ASA Gold & Precious Metals Limited Fund would plunge ~50% over the next 12 months, which likely would have dented Great Bear's share price further regardless of whether it held off on reporting a maiden resource. To summarize, the urgency to acquire Great Bear just before the bottom fell out of juniors likely cost Kinross over $300 million, which isn't an insignificant figure for a company of its size (~$6.8 billion).

If Great Bear Project's maiden resource came in at 8.0+ million ounces, I could easily excuse the price paid, since Kinross' technical team could have made a case that a resource of this size would have pushed Great Bear's stock even higher, making an acquisition even more impressive. However, as we know with the benefit of hindsight, the resource didn't even come close that figure despite spending ~$60 million on the project last year.

To put the Great Bear acquisition price in perspective, Agnico Eagle ( AEM ) acquired TMAC Resources after a ~90% decline in the stock for ~$250 million with existing infrastructure at a price of less than $50/oz on M&I resources. Although this isn't likely to be a 400,000-ounce per annum operation, it will head into production well ahead of Great Bear, it could easily churn out 300,000 ounces per annum, and it will require much less capex than what I expect to be closer to $1.2+ billion to build Great Bear.

Digging into the February update on Great Bear a little closer, we saw a material change in language in the 15-month period from December 2021 (time of acquisition) to February 2023. Initially, Kinross stated that it was looking at a plant capable of processing 10,000 to 15,000 tonnes per day), with a Tier-1 scale of ~500,000 ounces per annum and all-in-sustaining costs that would land between $600/oz to $800/oz when questioned about potential margins on the asset in the initial Conference Call related to the acquisition. The shift in language in the most recent update vs. the December 2021 call was night and day, and not for the better.

Starting with throughput, there was one silver lining, which is that Kinross now appears to be contemplating a 10,000 tonne per day plant which although it will translate to much lower annual production, it could shave up to $200 million off the initial capex estimate. This still won't be a cheap asset to build despite it benefiting from infrastructure with a total acquisition cost (price paid + drilling costs to put it into production + initial capex of ~$2.6 billion), but I see the potential for it to be built for $1.2 billion or less when incorporating inflation and a 2027 or later construction start vs. a view of ~$1.35 billion previously. Now for the negatives.

From a scale standpoint, the previous outlook of 450,000 to 500,000+ ounces over the life of the mine looks to be what I'd call a pipe dream. This is because assuming a 3.4 gram per tonne head grade (blend of open pit and underground), 362 operating days, ~3.62 million tonnes processed per annum and a 94.5% recovery rate, life-of-mine production is likely to come in closer to ~375,000 ounces. Meanwhile, though the first eight years will benefit from higher grades according to the company, using a 4.1 gram per tonne head grade to incorporate additional mining dilution (vs. 4.2 gram per tonne guided), and the same assumptions except a 95% recovery rate, the first 8-year average would land closer to ~450,000 ounces. So, the 500,000-ounce view looks to be closer to peak production for the best two or three years, and not life-of mine or even first-10 year production averages.

Finally, from a cost standpoint when questioned in the most recent Conference Call, the view on all-in-sustaining costs changed dramatically. As noted, the previous view that all-in-sustaining costs that could land between $600/oz to $800/oz, and I had assumed $775/oz at the top end of this range given that these costs looked ambitious especially when incorporating several years of inflation with a 2030 start to commercial production. On the last call, the language changed to "well below $1,000/oz" which even if we assume means $900/oz, that is 28% above the previous soft guidance mid-point ($700/oz). So, although this will still be an incredible operation, this doesn't appear to be a ~60% AISC margin project like some might have anticipated after listening to the December 2021 Call.

Great Bear - Targeted Path to Production (Company Presentation)

{kind=link}

So, what's the verdict?

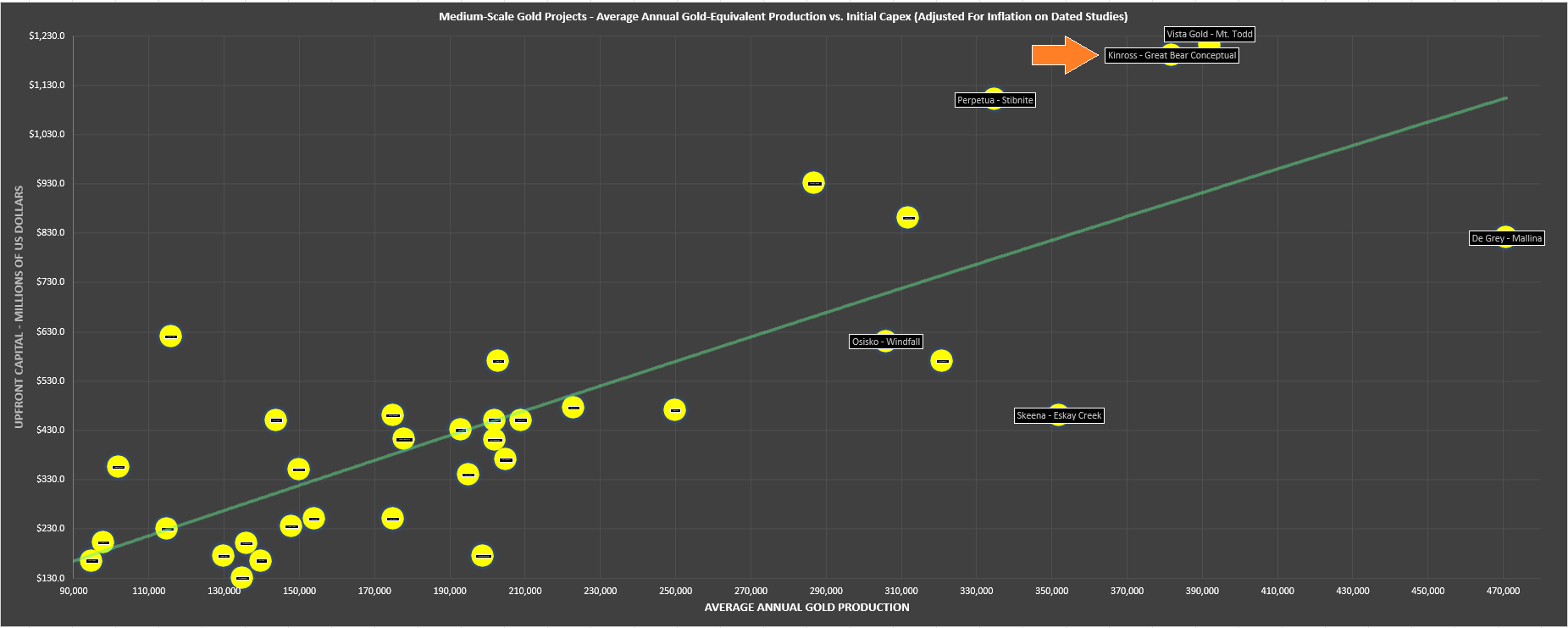

It's important to note that this is still an incredible asset and one of the best undeveloped gold assets globally, even if it will be lucky to pour its first gold by Q2 2029. As the charts below show relative to other undeveloped gold projects, this could have similar scale to De Grey's ( DGMLF ) Mallina Gold Project in the Northern Pilbara of Western Australia, and is well above the scale of Skeena's ( SKE ) Eskay Creek, Artemis' ( ARGTF ) Blackwater, and Kinross' former development project Udinsk, before it was divested. Plus, costs are expected to be more than 30% below the current industry average of ~$1,300/oz even if we assume AISC lands near $910/oz. Plus, I would expect a very robust IRR given that production should approach or top 500,000 ounces in the earlier years of the mine life.

Undeveloped Gold Projects - Projected GEO Production Profiles & Upfront Capex Estimates (Company Filings, Author's Chart & Estimates)

{kind=link}

Undeveloped Gold Projects - Average Annual GEO Production & Estimated AISC (Company Filings, Author's Chart & Estimates)

{kind=link}

That said, this does not appear to be anywhere near a Canadian Malartic 2.0 (800,000+ ounces per annum at sub $900/oz costs), and while margins will be robust, the recent language suggests that they'll nowhere near the initial estimates of $600/oz to $800/oz. Obviously, this will still complement Kinross' portfolio, but investors will be waiting several years to see the fruits of this massive investment, with commercial production not likely until Q1 2030 if we take a conservative approach on timelines for permitting a project of this size and construction. Hence, it won't help Kinross' bring down its costs in the interim, which are expected to come in at $1,320/oz this year, above the industry average and well above that of larger peers like Newmont ( NEM ) and Newcrest.

{kind=link}

To summarize, I think the underwhelming Great Bear update is a slight downgrade to the Kinross thesis, given that while this is an incredible asset, it's not the unicorn (450,000+ average annual production at sub $750/oz AISC) that it was initially made out to be, which suggested it might have similar attributes to NGM LLC's Goldrush that's set to begin production in 2024, or up to ~500,000 ounces at sub $700/oz with the inclusion of Fourmile which looks to be higher-grade than Goldrush and lies just north of the Goldrush property boundary.

Valuation & Technical Picture

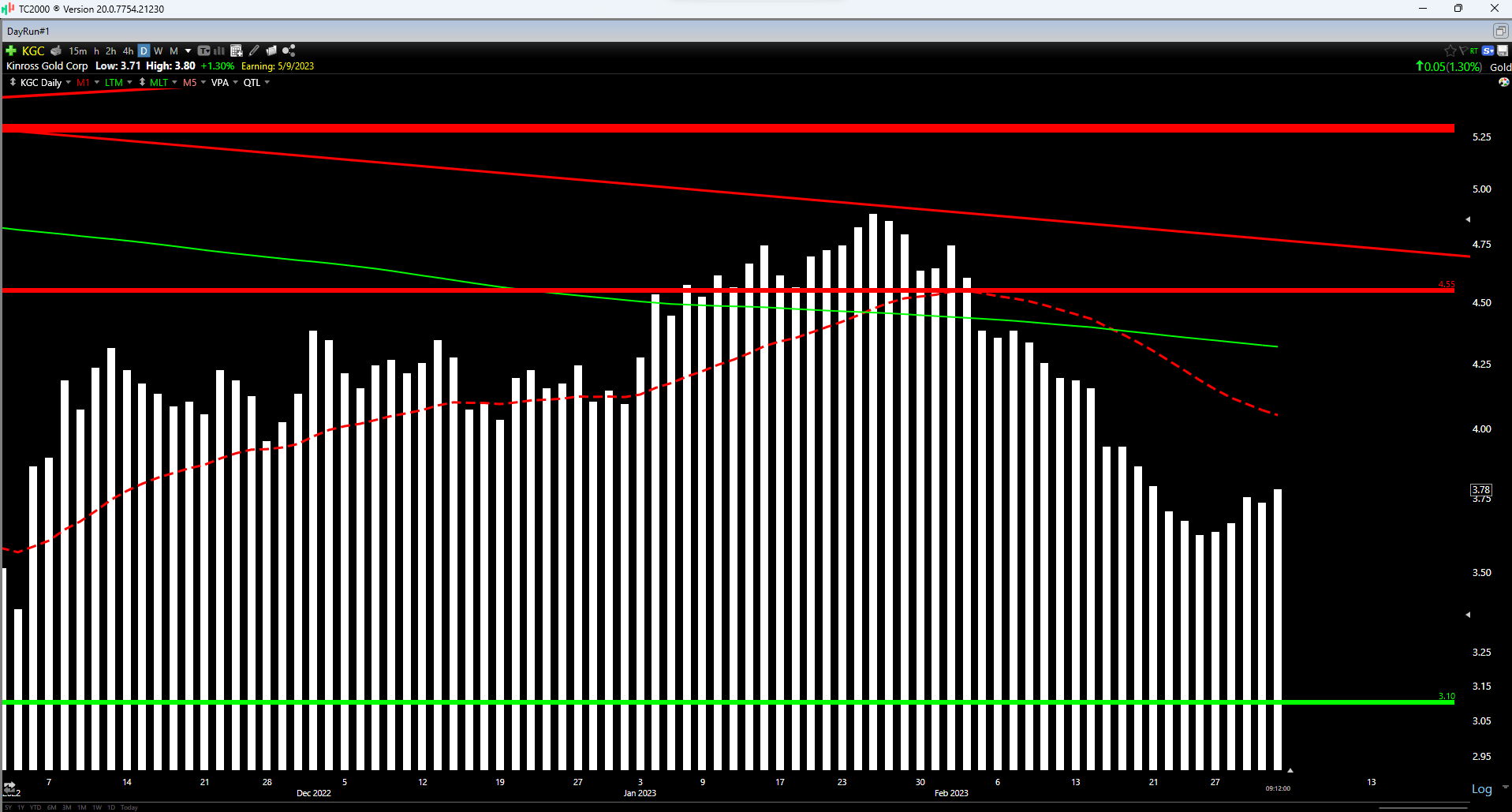

Based on ~1,230 million shares outstanding and a share price of US$3.78, Kinross trades at a market cap of ~$4.65 billion and an enterprise value of ~$6.8 billion. This remains a very reasonable valuation for a gold producer of its size that aims to maintain production at the 2.0 million ounce per annum mark long-term. However, while the stock has massively underperformed its peer group, it's not as cheap as some might expect after a 65% share price decline from its 2020 highs. This is because it's only trading at a 19% discount to its historical cash flow multiple (~5.2x) based on conservative FY2023 cash flow per share estimates of $0.88 (~4.3x cash flow).

{kind=link}

Using what I believe to be a fair multiple of 5.8x cash flow (12% premium to historical multiple) to reflect the divestment of assets in less favorable jurisdictions (Ghana, Russia), I see a fair value for Kinross of US$5.10. This translates to a 34% upside from current levels. Although this represents a meaningful upside, I prefer a minimum 35% discount to fair value for starting new positions in mid-cap cyclical names, and ideally closer to a 40% discount to fair value for industry laggards. Given that Kinross remains an industry laggard and has shown less discipline regarding acquisitions relative to peers (Aurelian, Red Back Mining, and Great Bear), I believe a 40% discount to fair value is more suitable. After applying this discount, the ideal low-risk buy zone for KGC is US$3.10 or lower.

{kind=link}

Looking at the technical picture, this confirms the view that KGC is not yet in a low-risk buy zone, with the stock sandwiched between resistance at US$4.55 and support at US$3.10. Based on a current share price of US$3.78, the stock's reward/risk ratio comes in at just 1.13 to 1.0, well below the 6.0/1.0 or better reward/risk ratio that's preferable for cyclical stocks. So, using this technical framework, the stock would need to decline below US$3.30 at a bare minimum to enter a low-risk buy zone. Hence, from a fundamental and technical standpoint, I don't see a low-risk buy zone just yet for KGC despite its sharp decline from its recent highs.

Summary

While several producers reported solid reserve replacement and considerable exploration success in 2022 at ore bodies such as Goldrush/Fourmile, Canadian Malartic, and Detour Lake, among others, Kinross' reserve replacement was disappointing, especially considering the lift in its gold price assumptions. Worse, the Great Bear update came in well below my expectations and the language around the project has changed considerably, suggesting the team may have been out over their skis a little in their initial projects for this asset. This doesn't mean that Kinross can't perform well in a rising gold price environment, but with less discipline than peers (M&A standpoint) and industry-lagging margins, I think there are better places to park one's capital, despite the very reasonable valuation.

For further details see:

Kinross Gold: An Underwhelming Reserve/Resource Update