K:CC - Kinross Gold Is Outperforming: But Is The Stock A Buy?

2023-12-14 17:48:20 ET

Summary

- Kinross Gold Corporation has been performing well, with its shares rising by 16% and outperforming the S&P 500 and gold mining sector indices.

- The company reported strong Q3 financial results, including increased production, cost efficiency, and strong cash flow.

- Kinross Gold's strategic expansion at the Round Mountain mine is a solid investment, with impressive financials and potential for prolonged operations.

- However, there are concerns about the stagnant production outlook and the significant capital requirements of the Great Bear project.

As we near the end of 2023, Kinross Gold Corporation ( KGC ) has been performing impressively, particularly following its recent third quarter financial results . The company seems well on its way to achieving its annual targets, thanks in part to its performance from its Tasiast mine, which recorded its highest quarterly production ever in Q3.

However, the decision to invest in Kinross Gold at this moment is up for debate.

As a quick reminder: Kinross Gold's second-quarter results in 2023 were also quite positive, as the company surpassed investor expectations. A key driver was the $100 increase in the average gold price compared to the previous year. But Kinross also achieved a 22% jump in gold production, reaching 555,036 ounces, and maintained lower-than-expected production costs at $1,296 per ounce. This performance led to a strong operating cash flow of $529 million.

Since these results, Kinross Gold's shares have risen by 16%, outperforming the 5% rise of the S&P 500 Index (SP500) and surpassing gains in the gold mining sector indices, including the VanEck Gold Miners ETF ( GDX ) and the VanEck Junior Gold Miners ETF ( GDXJ ).

I previously called the stock a HOLD in my prior coverage. Given these developments, investors are now pondering whether Kinross Gold represents a valuable buy in the current market scenario. Here's what I think.

Kinross Gold's Stellar Q3 Financial Results

Kinross Gold has reported a robust performance for Q3 2023 , staying on course to meet its annual guidance for production, cost of sales per ounce, all-in-sustaining cost, and capital expenditures.

Key Highlights

-

Production: Achieved an 11% year-over-year increase, with 585,449 gold equivalent ounces produced.

-

Cost Efficiency: A production cost of sales was $911 per gold equivalent ounce, with an AISC of $1,296 per ounce.

-

Profit Margins: Kinross realized margins of $1,018 per gold equivalent ounce sold.

-

Strong Cash Flow: The company generated an operating cash flow of $406.8 million and an adjusted operating cash flow of $470.6 million, with a free cash flow of $122.9 million.

-

Net Earnings: Kinross reported net earnings were $109.7 million, equating to $0.09 per share, and adjusted net earnings were higher at $144.6 million, or $0.12 per share.

-

Financial Health: The company concluded the quarter with cash and cash equivalents of $464.9 million and total liquidity of approximately $2.0 billion.

Despite a year-over-year increase in AISC, Kinross's profitability surged due to high output and effective asset performance, notably at Tasiast, Paracatu, and La Coipa mines.

Looking ahead, Kinross says that it is on track with its 2023 production guidance of 2.1 million gold equivalent ounces and cost of sales guidance. For 2024 and 2025, the company expects stable annual production of around 2.1 million and 2.0 million gold equivalent ounces, respectively.

Other Notable Developments

-

Dividends: Kinross declared a quarterly dividend of $0.03 per share, payable in December 2023, with shares currently offering a yield of just over 2%.

-

Operational Achievements: Tasiast recorded its highest quarterly production and sales in Q3; Paracatu saw increased production year-over-year, and La Coipa was the lowest-cost mine in the portfolio.

-

Future Prospects: The Manh Choh, Round Mountain, and Great Bear projects are proceeding as planned, with significant exploration success and plans to extend mine life and production, according to Kinross Gold.

Balance sheet update

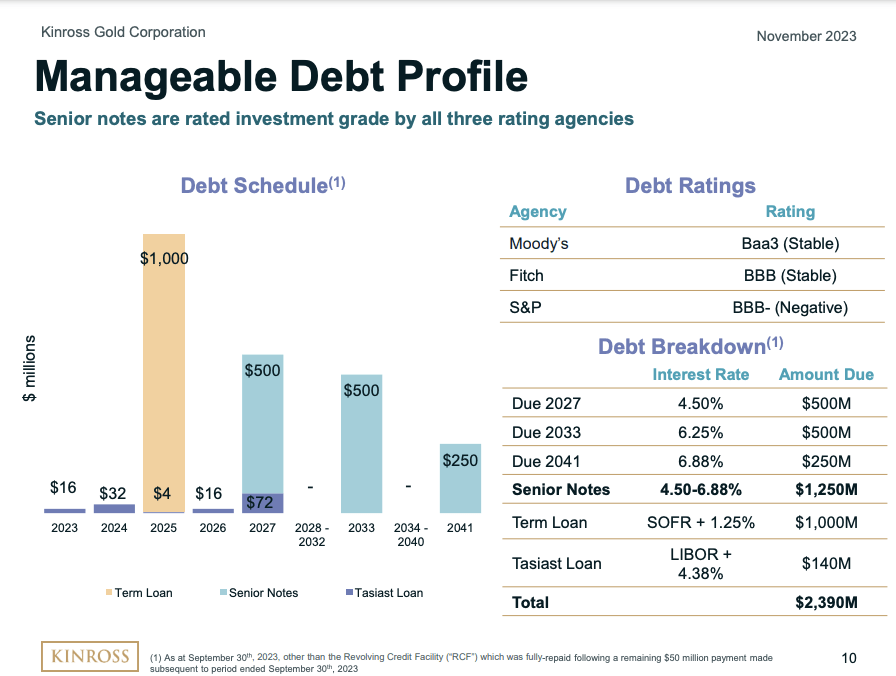

Kinross Gold's financial standing , as of September 30, 2023, included $464.9 million in cash, a minor decrease from $478.4 million in June. The company's total debt slightly dropped, however, to $2.38 billion from $2.55 billion the previous year.

Kinross has a relatively stable financial position with access to about $1.5 billion in credit and total liquidity of approximately $2.0 billion, up from $1.9 billion in June.

{kind=link}

In Q3, Kinross issued $500 million in new senior notes at 6.25%, due in 2033, using these funds to clear older notes maturing in March 2024. The company also repaid $100 million of its revolving credit in this period.

While Kinross has higher debt than some peers, most aren't due until 2025 or later, offering potential refinancing benefits if interest rates fall. However, investors should note that developing the Great Bear mine in Canada might require significant capital in the coming years, potentially leading to further debt and impacting the balance sheet.

Q3 Summary

Kinross Gold had a great third quarter in 2023. They produced more gold, managed costs well, and earned strong cash flow, although higher gold prices also helped a bit. This strong performance suggests that the company is set to outperform on its Q4 expectations, and perhaps carry that momentum into 2024.

Round Mountain Expansion: A Solid Investment

Kinross Gold's strategic expansion at the Round Mountain mine in Nevada, a premier mining location, is a noteworthy development.

Last year, the mine produced 226,374 ounces of gold, with an estimated four-year life. However, Kinross's 2023 decision to mine the optimized Phase S open pit is set to prolong operations until the end of the decade, adding approximately 750,000 ounces of gold equivalent to the mine's output.

The financials behind the Round Mountain expansion are impressive. With gold at $2,050 per ounce (around the current spot price), the internal rate of return ("IRR") is a robust 70%, and the net present value ("NPV") stands at $288 million.

The project remains viable even at lower gold prices, offering an IRR of 33% and an NPV exceeding $100 million at $1,750 per ounce. The low upfront capital expenditure pegged at just $30 million (excluding stripping costs), ensures a fast return on investment, making this expansion a smart move for Kinross.

But is Kinross Gold Stock a Buy Here?

Yet, I still don't think the stock is a buy, at least not at the present moment.

While Kinross Gold had a strong start to the year, and it has a seemingly attractive valuation, with a forward P/E of 15 and an EV/EBITDA of 5.52, according to Seeking Alpha, several considerations could temper enthusiasm for the stock.

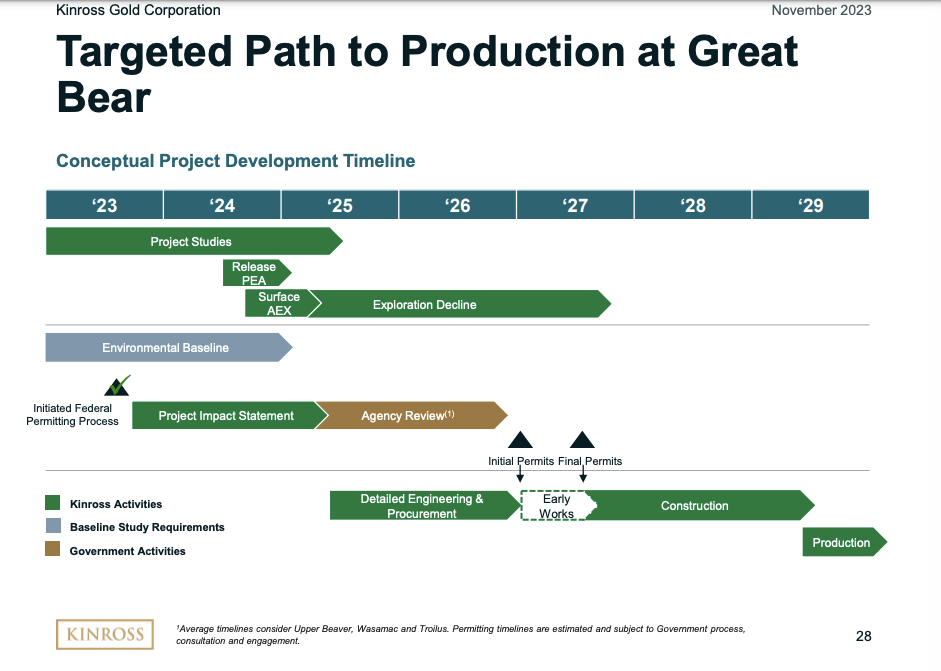

One key concern is the company's static production outlook up to 2025-26. This situation remains unchanged from the last quarter's reports. It appears unlikely that Kinross will experience any significant increase in gold production until around 2028-29, which aligns with the expected start of production at the Great Bear project. Until then, annual production is anticipated to hover around 2 million ounces through 2025, despite the Round Mountain expansion.

A snippet from Kinross Gold's corporate presentation shows flat production. (Kinross Gold )

Another point of caution is the projected AISC of around $1,300 per ounce in the coming years. This level is certainly low enough to maintain reasonable cash flow at current gold prices, but it is also higher than some of Kinross's competitors. (A reduction in these costs may not occur until the Great Bear project begins production, or until inflation declines substantially.)

My primary concern revolves around the Great Bear project , acquired from Great Bear Resources for $1.8 billion. The initial resource estimate of 2.7 million ounces indicated and 2.3 million ounces inferred, while significant, carries a hefty purchase price. The full potential of the resource, possibly reaching 8-10 million ounces, is promising, yet production is still several years away. (Industry norms suggest a 5-7 year timeline for constructing a mine of this scale; Kinross estimates 2029-30 production start.)

{kind=link}

Moreover, the cost of bringing Great Bear into production remains uncertain. Still, it is expected to be substantial given the size of the mine, potentially ranging from $2-$3 billion, maybe even higher with inflation adjustments. A clearer picture of these costs should emerge with the release of the initial Preliminary Economic Assessment study in 2024.

In summary, while Kinross Gold Corporation presents some attractive aspects, investors should weigh these against the company's near-term stagnant production outlook, relatively high sustaining costs, and the significant capital requirements and timeline of the Great Bear project. I still view the stock as a HOLD, and would re-visit my rating if the stock sells off a bit, and after the PEA on Great Bear is released.

For further details see:

Kinross Gold Is Outperforming: But Is The Stock A Buy?