K:CC - Kinross Gold Will Trade Much Higher If My Gold Thesis Is Correct

Summary

- In this article, I start by giving you a detailed explanation of my view on gold prices, as I believe that gold will break $3,000 after the next correction.

- The market is too dovish, which will likely pressure growth stocks, the dollar, and metals in the next few months.

- After that, I expect a situation to occur where the Fed is forced to pivot, as it cannot achieve a soft economic landing.

- My go-to investment is Kinross Gold, thanks to its low breakeven prices, healthy balance sheet, and terrific valuation.

Introduction

Last year, I became bullish on gold. Hence, I've written several bullish articles on gold, including this one . In this article, I want to do two things.

- Update my bullish call on gold, which now sees a pause in its rapid uptrend, followed by a steep surge the moment the Fed is forced to pivot.

- Explain why the Kinross Gold Corporation ( KGC ) remains one of my go-to picks for capital gains and dividends.

The recent surge in gold was impressive as investors started to bet on the Fed becoming dovish. This caused the dollar to weaken, which is generally a big driver of gold prices. Moreover, yields were plunging while growth stocks started to fly like there was no tomorrow.

As a result, I'm now cautious again, as it looks like the market has become too dovish. Inflation is still sticky, and more work needs to be done before the Fed can declare victory.

Because I'm not a believer in a soft landing, I'm looking for a situation where the Fed is forced to cut rates. At that point, I think we could see a much steeper increase in gold prices than most might expect.

Now, allow me to elaborate on all of this!

My Long-Term View On Gold Is Very Bullish

However, I expect an attractive mid-term buying opportunity.

I spent a lot of time talking with and listening to experts and enthusiasts in the gold industry. There are two things that I notice. The first one is that most seem to be always bearish and expecting the financial Armageddon the Great Financial Crisis wasn't able to achieve. The second thing is that most people struggle to find a pattern in the gold price. When do we buy gold? Is it when inflation is rising? Do we buy it when economic growth is about to implode (recession)? Do we buy it when the economy accelerates (higher inflation)?

Essentially, gold is a long-term hedge against inflation. It's a shiny metal that will still be shiny and valuable thousands of years after we're gone. Moreover, while mining operations consistently increase the amount of gold, it's fair to say that the supply of gold is limited. The same cannot be said about fiat currencies.

Note that gold has protected investors against inflation since it became deregulated in the 1970s:

{kind=link}

Reuters

Moreover, like silver, gold can be used as a currency in a situation where people stop trusting fiat currency issuers. Especially in times of central bank digital currencies, people want to be independent.

That said, I don't believe in actively trading the price of gold unless you're a professional macro trader who uses futures or similar instruments.

I believe in holding physical gold, mining companies (for dividends), or trading gold proxies like volatile miners. I do not hold physical gold, although I believe it's a good investment. The reason is safety. Holding and talking about physical gold on the internet while using one's real name is asking for trouble. That's not worth the risk, which is why I stick to miners.

What Drives The Price Of Gold?

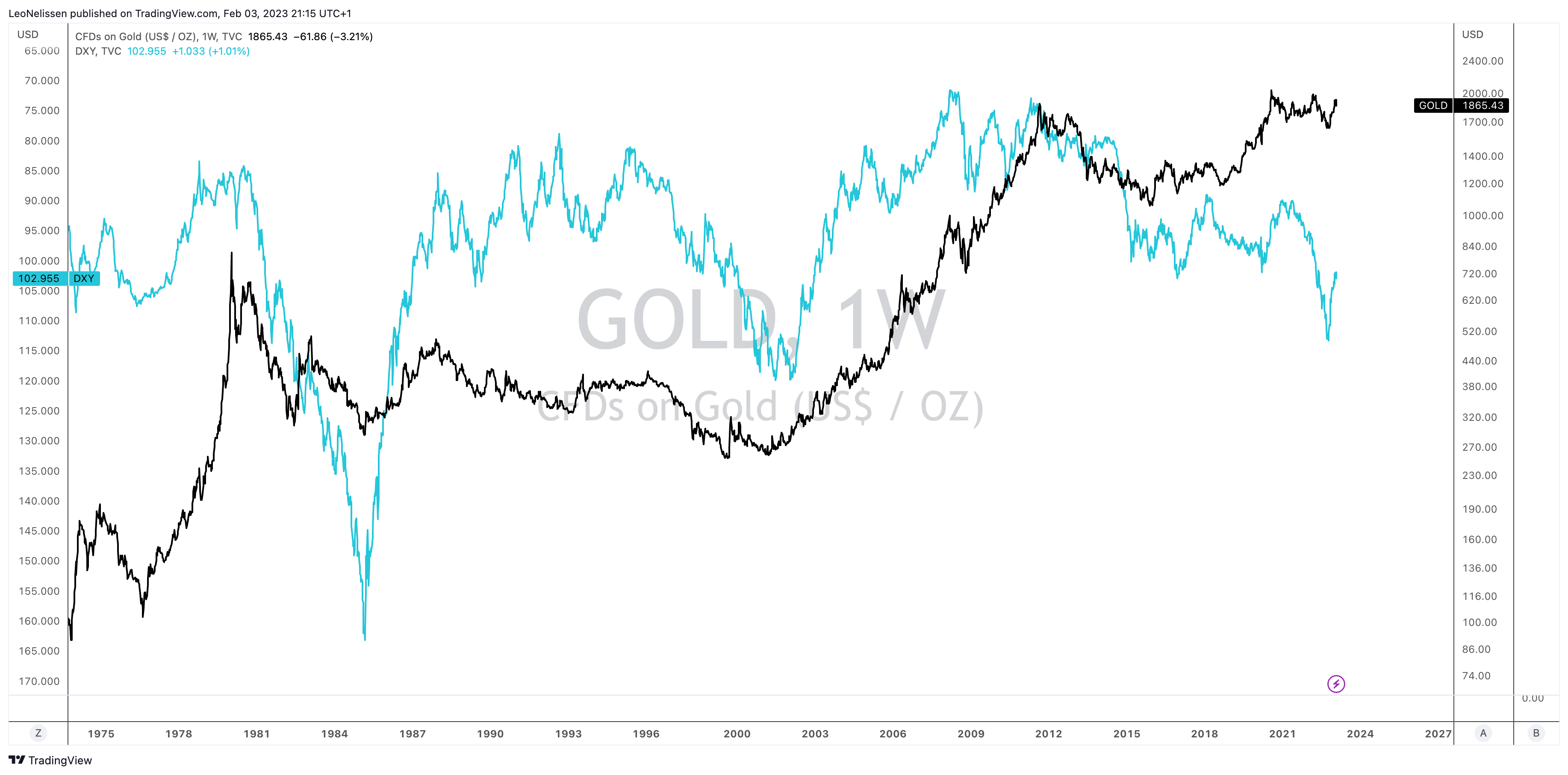

That said, a major driver of gold is not inflation - at least not directly - but the dollar. After all, gold competes with the world's reserve currency. When the dollar falls, gold benefits. When the dollar strengthens, gold has a hard time rising.

The chart below shows the inverted dollar index (blue) and the price of gold (using a log scale). Note that short-term periods show little correlation. What matters are longer-term trends.

For example, the most recent massive bull run was between 2000 and 2012, when gold rose by more than 600%. This move was supported by significant weakness in the dollar, above-average inflation rates, and a huge growth spurt in China. Then, the dollar weakened, putting pressure on the gold price, which is now trading close to its 2011 highs. That's zero returns in more than ten years. Moreover, as gold doesn't pay a dividend, investors are highly dependent on market timing to avoid holding a pet rock.

{kind=link}

TradingView (Gold (Log), DXY (Inverted))

Concerning my inflation comment, inflation soared from 1.3% in 2020 to more than 9% by mid-2022. Yet, gold prices went sideways.

But then again, making the case that gold is not an inflation protection tool is wrong - very wrong. Gold rises in anticipation of higher inflation. It has become a tool to predict what the Fed may be up to. Between the spring of 2019 and the summer of 2020, gold prices rallied by nearly 60% as the Fed began easing its monetary policy.

Essentially, gold is a global currency, except one that does not pay interest. So to go back to my earlier comment that gold competes with the dollar, it's bad news when the Fed raises rates. It means investors have a better alternative. An alternative that does pay interest.

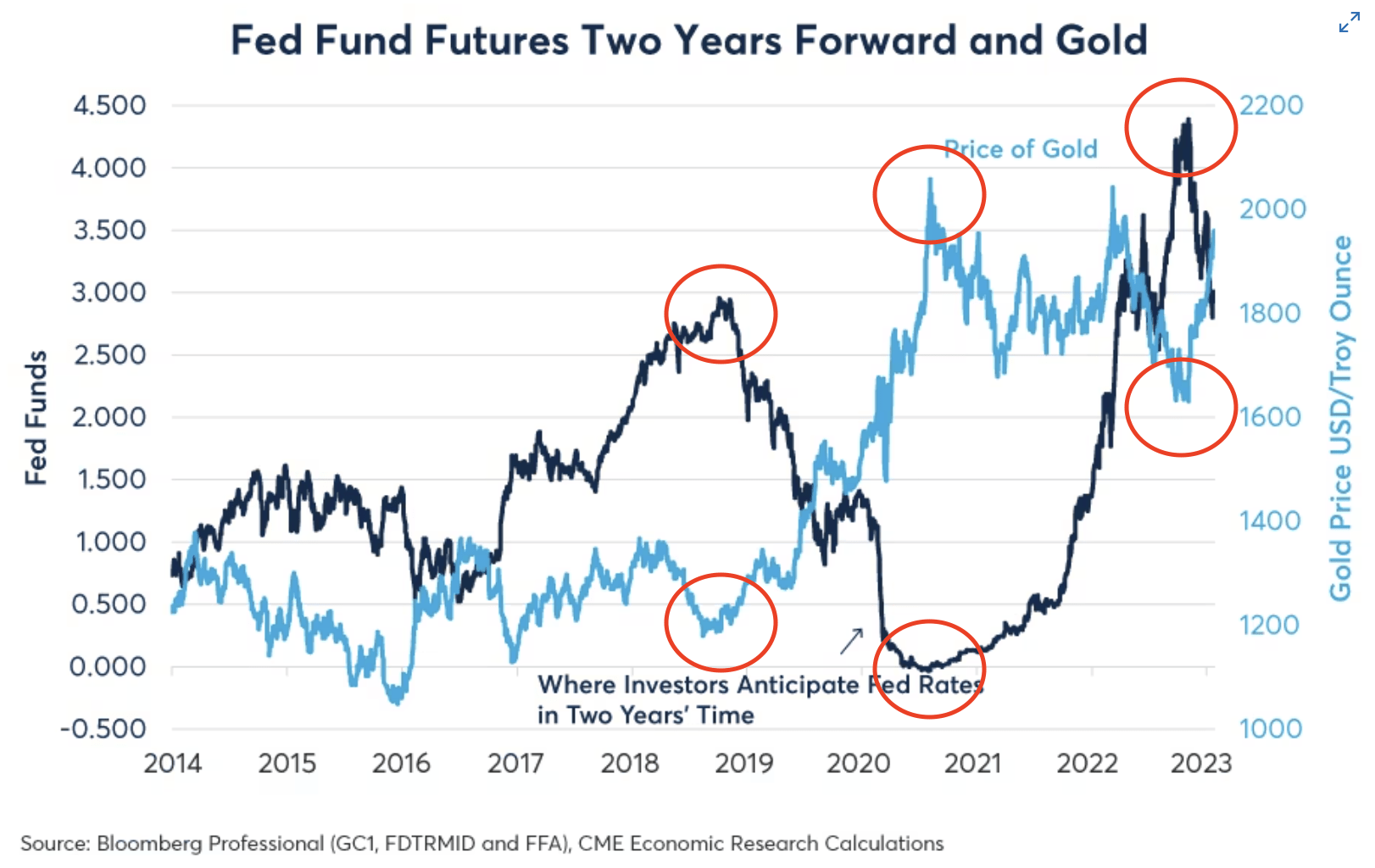

Hence, it is no surprise that gold and silver prices are negatively correlated to the 2Y forward of Fed funds rates .

- If investors expect rates to increase, gold falls.

- If investors expect lower rates down the road, gold soars.

CME Group

An even more fascinating chart is the one below, as it clearly shows that forward rate expectations are driving the price of gold. In mid-2018, rate expectations peaked. Back then, global economic growth peaked as well. So, expecting lower rates makes sense. Gold immediately bottomed back then at roughly $1,200. Rate expectations dropped to 0.0% in mid-2020 when global growth slowing was made worse by the pandemic. Gold peaked the moment rate expectations bottomed. Gold had soared to roughly $2,100. That's a 75% return in just a few years.

And guess what? That relationship still holds. Gold has been on a tear lately, which is entirely driven by market participants pricing in a more dovish Fed.

{kind=link}

CME Group (Author Annotations)

With that said, I do agree with traders and investors who bought gold. The risk/reward was good. Stocks that I have covered in the past are flying. This includes Kinross Gold, which has risen by 25% over the past six months.

However, I also believe in a new buying opportunity.

Why I Expect Weakness In Gold

Readers who frequently read my articles likely know that I believe that markets are too dovish when it comes to Fed expectations.

Markets are currently pricing in 50 basis points worth of cuts. These are expected to happen in November and December of this year.

Bloomberg

This has caused a massive buying pandemic in growth stocks, as Tesla ( TSLA ) has almost doubled. The ARK Innovation ETF ( ARKK ) has added 37% year-to-date.

That said, I see one major problem. Inflation has not been defeated, and Jerome Powell is keen on fighting it until his job is done. As summarized by Wells Fargo :

The FOMC said that "inflation has eased somewhat," which Chair Powell reiterated in his post-meeting press conference. But he also noted that the Committee "has more work to do" in terms of monetary tightening to bring inflation back to the FOMC's target of 2% on a sustained basis. Powell also stated that policy would need to be restrictive for some time.

There are a lot of reasons to believe that the Fed might either hike more than expected or keep rates elevated for longer than expected.

For starters, financial conditions have eased to levels not seen at any point since the start of the current hiking cycle.

Bloomberg

Meanwhile, inflation remains sticky, with core services inflation remaining at elevated levels. Note that Powell is watching these numbers.

Bloomberg

And, to make things worse (for the Fed), structural issues are likely to prevent sticky inflation from easing.

For example, job openings remain strong, and the US economy just added 517K jobs in January.

Bloomberg

That's good news for the economy, yet bad news for the market, which cannot count on the Fed becoming dovish soon. After all, why should the Fed cut rates if:

- Key economic indicators like employment are strong.

- Financial conditions are very loose.

- The weaker dollar has caused inflation expectations to bottom.

- People are panic buying crypto, growth stocks, and even bankrupt companies like Best Buy (BBY).

I honestly feel like I'm in 2021 again.

Hence, after the employment report on Friday, growth stocks and gold weakened as the market started to realize that the Fed may have to be hawkish for longer.

Gold is now down 3% over the past five days.

And I'm celebrating a lower gold price, as I believe that gold will rise once the Fed is forced to pivot.

Why I Believe In Buying Gold Price Weakness

To make things more complicated, while inflation remains persistent, underlying economic fundamentals are deteriorating.

For example, manufacturing expectations are now in contraction. The ISM Manufacturing Index fell to 47.4 in January, with new orders falling to 42.5.

Bloomberg

While the service economy continues to expand, new manufacturing orders are pointing at a recession.

Bloomberg

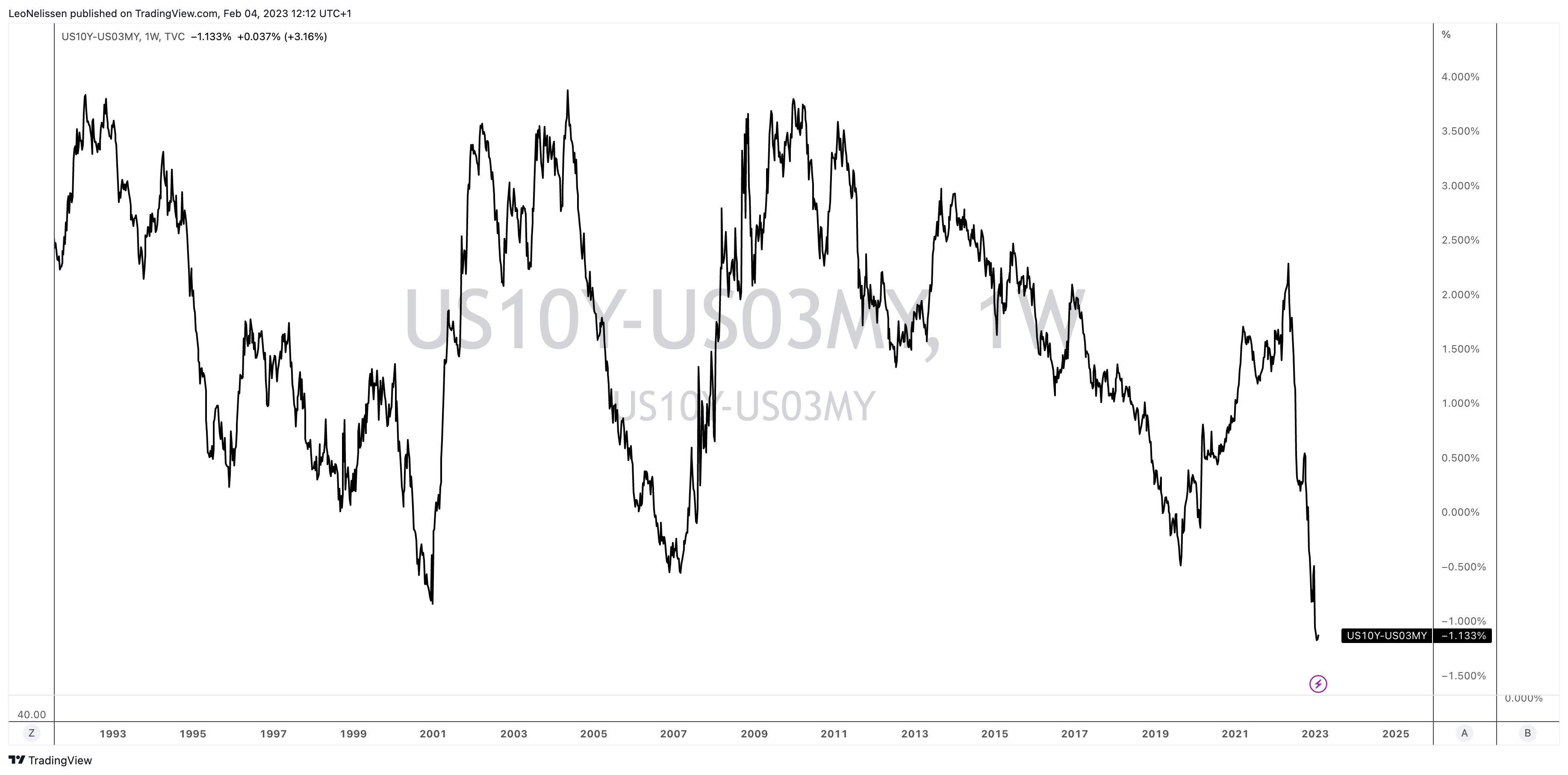

The same goes for the Fed's favorite recession indicator, the yield curve based on the US 10-year and 3-month government bond yields. The difference is 113 basis points, which has always (correctly) predicted a recession in modern history.

{kind=link}

TradingView (US10Y/US03M Yield Curve)

In other words, I believe the Fed will first have to be more hawkish than the market expects to fight sticky inflation. After that, I believe that the Fed will not be able to achieve a soft landing. Meaning a steeper recession is likely.

That's why I am so bullish on gold (long-term), as I believe that the Fed will be forced to cut rates. That could likely start going into 2024 (or earlier).

If my thesis is right, I think gold prices could soar to more than $3,000 in the years ahead.

Now, I'm trying to get a good entry, which includes picking the right trading tools. One of my favorites is Kinross Gold, the star of this article.

Why I'm Buying Kinross Gold

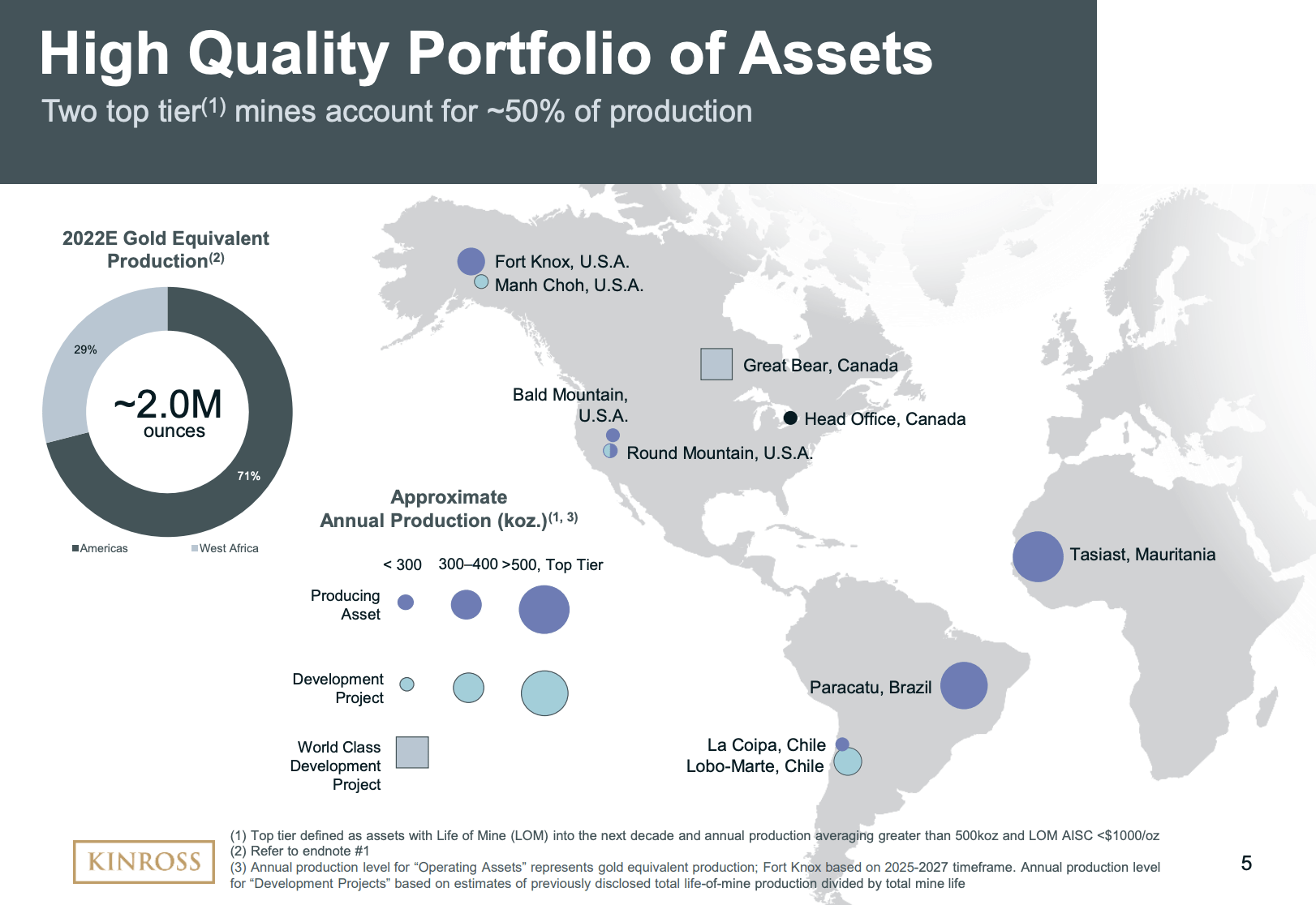

With a market cap of $5.6 billion, Kinross Gold is the 11th-largest publicly listed gold miner.

The Canadian miner mined roughly 2 million ounces of gold last year. This year, the company is expected to mine 2.1 million ounces. 71% of these ounces were mined in the Americas. The remaining 29% were mind in West Africa, where the company has a major mine in Mauritania. The company sold its Russian operations after the invasion of Ukraine roughly one year ago.

{kind=link}

Kinross Gold

One of the benefits that come with Kinross' operations is subdued geopolitical risk. While I'm not making the case that Brazil and Chile are nations without political risks, the company has most of its operations in stable nations, unlike miners, who have most of their mining operations in South America and Africa.

With that in mind, there are more reasons to believe that this miner is the right way to play a higher (expected) gold price.

The company is efficient. Its 2022E all-in-sustaining cost ("AISC") is $1,240 per troy ounce of gold.

As Gold Hub's Adam Webb described, the average AICS in the industry was close to 1,300 in 3Q22.

Gold Hub

Close to 10% of gold operations were operating at a loss, mainly caused by high inflation. This is bullish for gold, as it tends to keep a lid on production growth.

Gold Hub

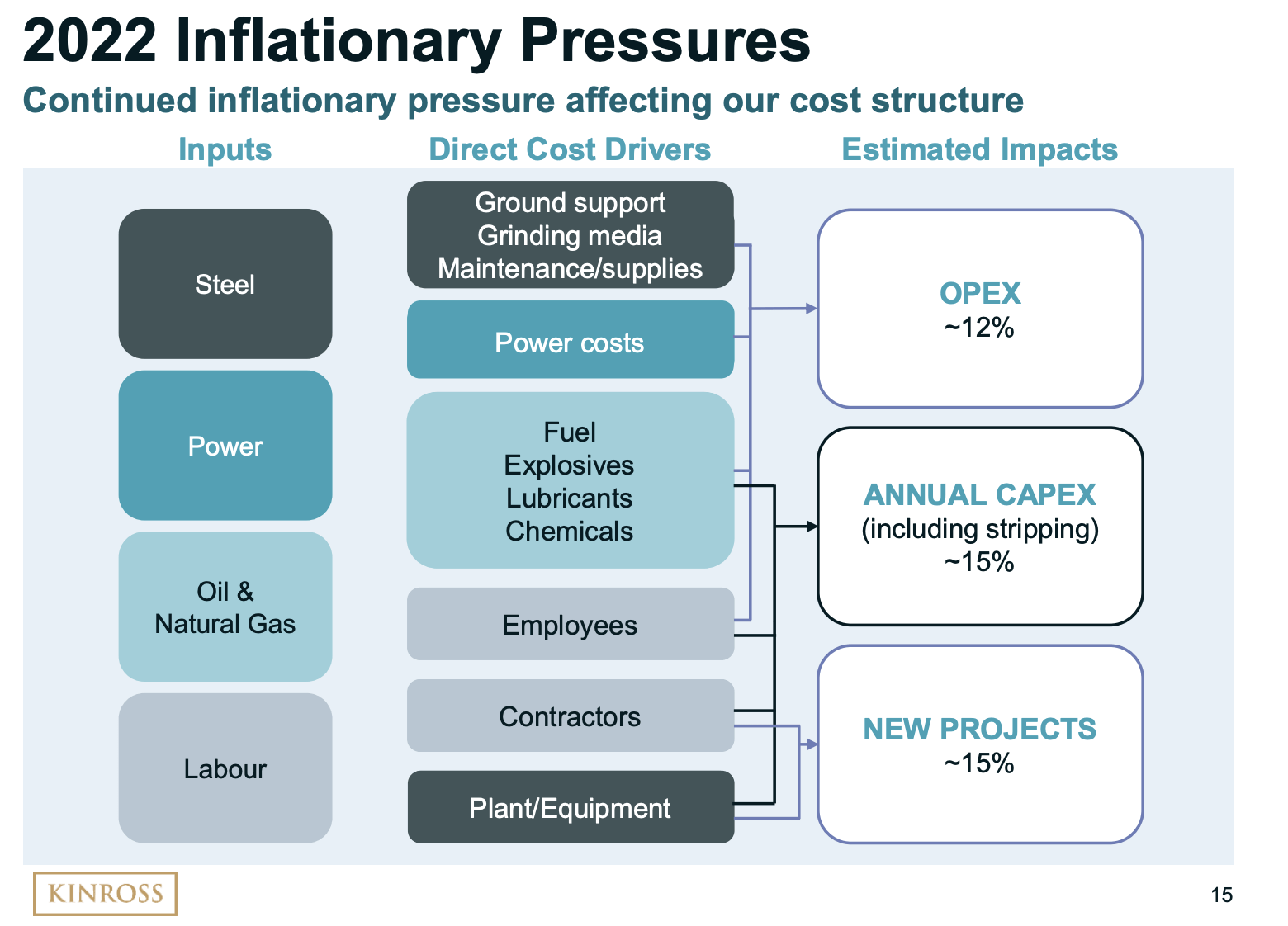

I expect Kinross Gold to maintain its cost advantage going forward, even though its complex operations are prone to higher inflation, as the overview below shows.

{kind=link}

Kinross Gold

With that said, there are more benefits. The company believes that it is substantially undervalued. For example, the company believes that its 0.7x price/net asset value ratio is way too cheap. Most peers (often with less production exposure in the Americas) are trading at higher multiples.

Its Tasiast and Paracatu assets alone would justify a fair valuation. Note that these two assets have an expected resource life of at least 15 years. The same goes for all other assets, excluding La Coipa, which is expected to have a resource life of roughly nine years.

Moreover, the company is using improving free cash flow to reward investors via buybacks.

In addition to maintaining a quarterly dividend (2.7% yield), the company bought back $300 million worth of shares in 2022 and looks to use 75% of excess free cash flow to repurchase shares in 2023 and 2024. Excess free cash flow is free cash flow minus interest and dividend payments. The company will refrain from buying back shares once its leverage ratio rises above 1.7x, or if its rating is impacted, major operations are disrupted, or the price of gold drops significantly.

The buyback program is a result of intervention from the Elliott hedge fund, which recognizes KGC's low valuation and the need to unlock value. As reported by GlobeNewswire in September 2022:

Elliott Portfolio Manager Mark Cicirelli stated, “We have appreciated our constructive dialogue with the Kinross management team, and we believe the enhanced buyback program announced today demonstrates their commitment to shareholders and to unlocking shareholder value. Kinross today possesses a high-quality, Americas-focused portfolio with strong potential for future growth through Great Bear, yet it trades at a significant discount to both its peers and to the value of its assets. We believe that with this new capital allocation framework, Kinross is taking a major step toward closing that gap and realizing the upside potential in its stock. We look forward to continuing our engagement with the Company.”

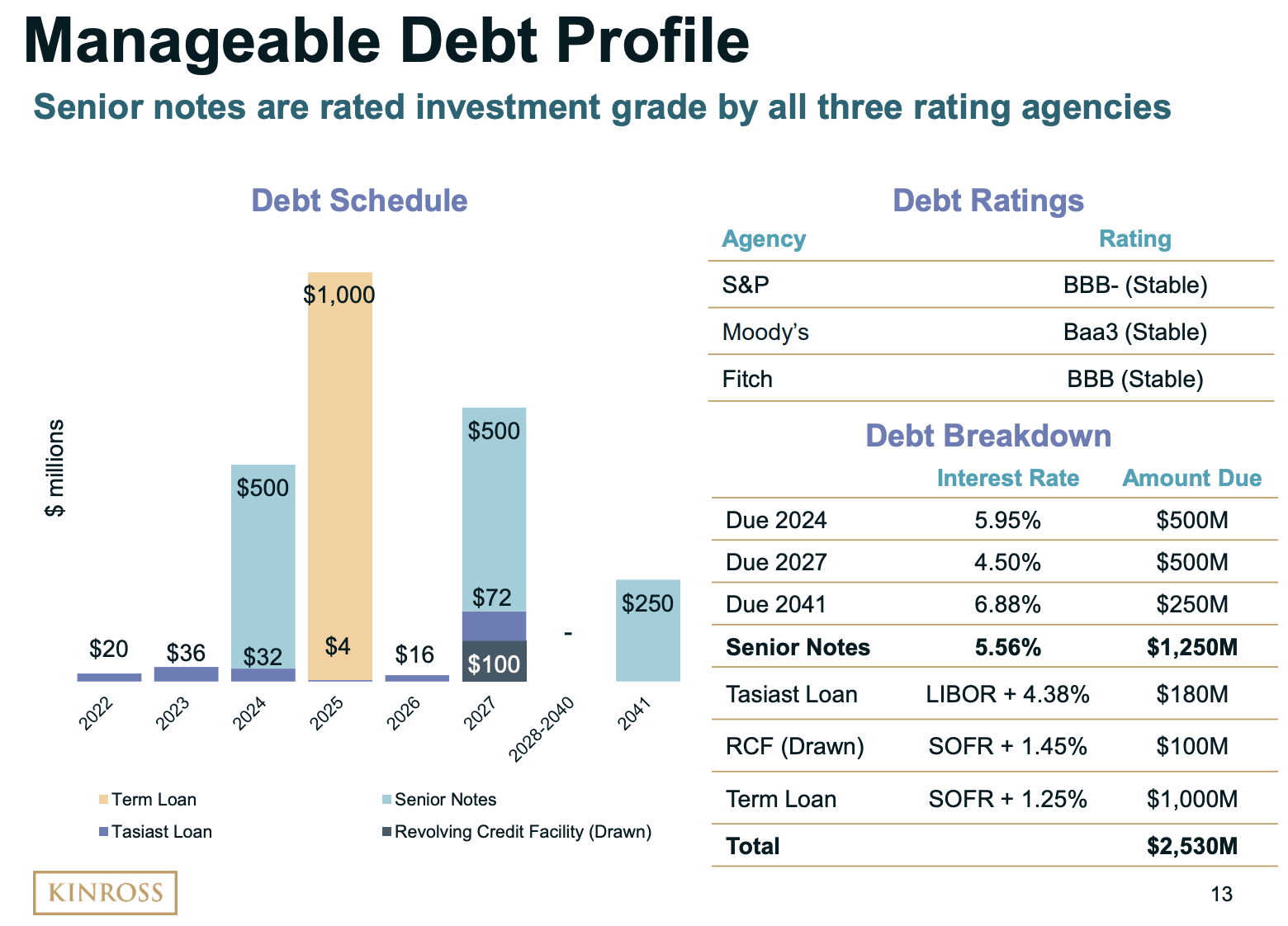

Hence, it helps that KGC has a stellar balance sheet. The company has $2.0 billion in available cash. A quarter of this is cash. 75% are available credit.

The company has a BBB-rated balance sheet (just one step below the A-range) and no major debt maturities in 2023. In 2024, it has roughly $530 million due. $500 million of this is a portion of its senior notes.

{kind=link}

Kinross Gold

Moreover, since the gold bottom of the summer of 2022, KGC shares have outperformed their peers by roughly 10 points. I expect outperformance to continue, albeit not during gold price declines. The VanEck Gold Miners ETF ( GDX ) is overweight in large miners with subdued volatility, including gold streamers. It's hard to beat these companies when gold prices are down. So, I expect KGC to underperform in the weeks ahead until my gold bull case starts to unfold. Once that happens, I think KGC shares will return far more than GDX.

With that said, here's my takeaway.

Takeaway

In this article, I explained my view on the price of gold and how I'm trying to capitalize on it. I believe that gold is in a long-term uptrend with room to rise to at least $3,000 in the years ahead. I believe that the Fed will get to a point where it is forced to pivot, triggering a wave of bets that rates will move much lower in the years ahead.

However, my mid-term view is that markets are too dovish. Inflation remains sticky, and the Fed has communicated its willingness and duty to pressure inflation to its 2% target. Getting inflation from 9% to 6% isn't that hard. Getting inflation from 5% to 2% is much harder.

Hence, I believe that gold is in for a price correction, which I will use by buying gold miners. One of my favorites is Kinross Gold, which enjoys production in stable regions, a relatively low breakeven cost, and a valuation that is way too cheap.

Hence, in the months ahead, I'll be on the hunt to buy KGC at lower prices, as I believe the stock has room to run to prices north of $10-$11.

Note that my rating is bullish despite my belief that the stock will provide us with a correction in the months ahead. Also, be aware that KGC and its peers are very volatile. Do not go overweight in gold mining stocks if you decide that these investments are right for your portfolio.

(Dis)agree? Let me know in the comments!

For further details see:

Kinross Gold Will Trade Much Higher If My Gold Thesis Is Correct