KGC - Kinross: Strong Operational Performance Lately

2023-07-06 13:43:43 ET

Summary

- Kinross has delivered operationally over the last few quarters.

- The stock price has YTD outperformed many peers in the industry.

- The valuation is far from excessive, but it is much less attractive compared to the more depressed levels seen in 2022.

Investment Thesis

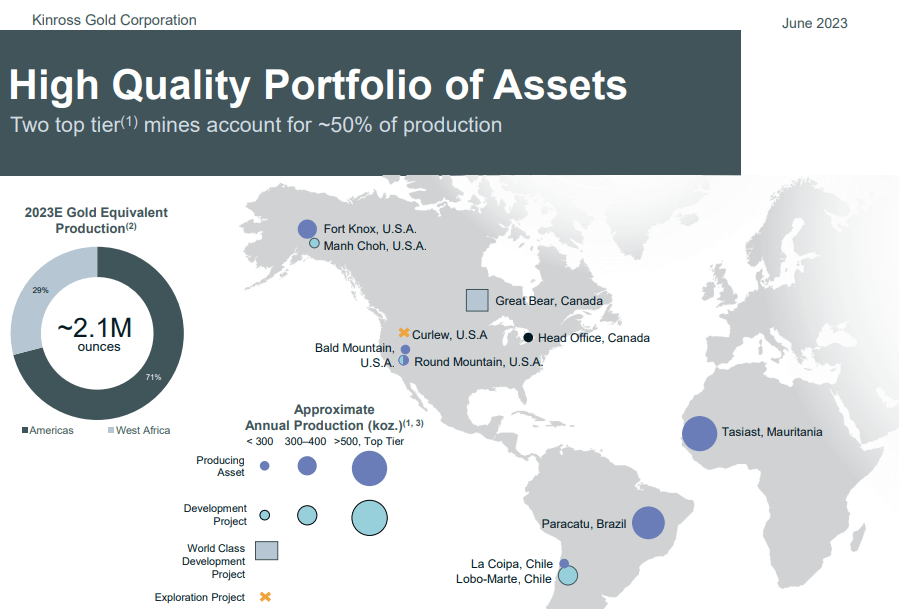

Kinross (KGC) is a mid-size gold producer, with most of its operation in the Americas. It is a stock I have owned in the past and covered a few times on Seeking Alpha, those articles can be found here .

Figure 1 - Source: Kinross Corporate Presentation

{kind=link}

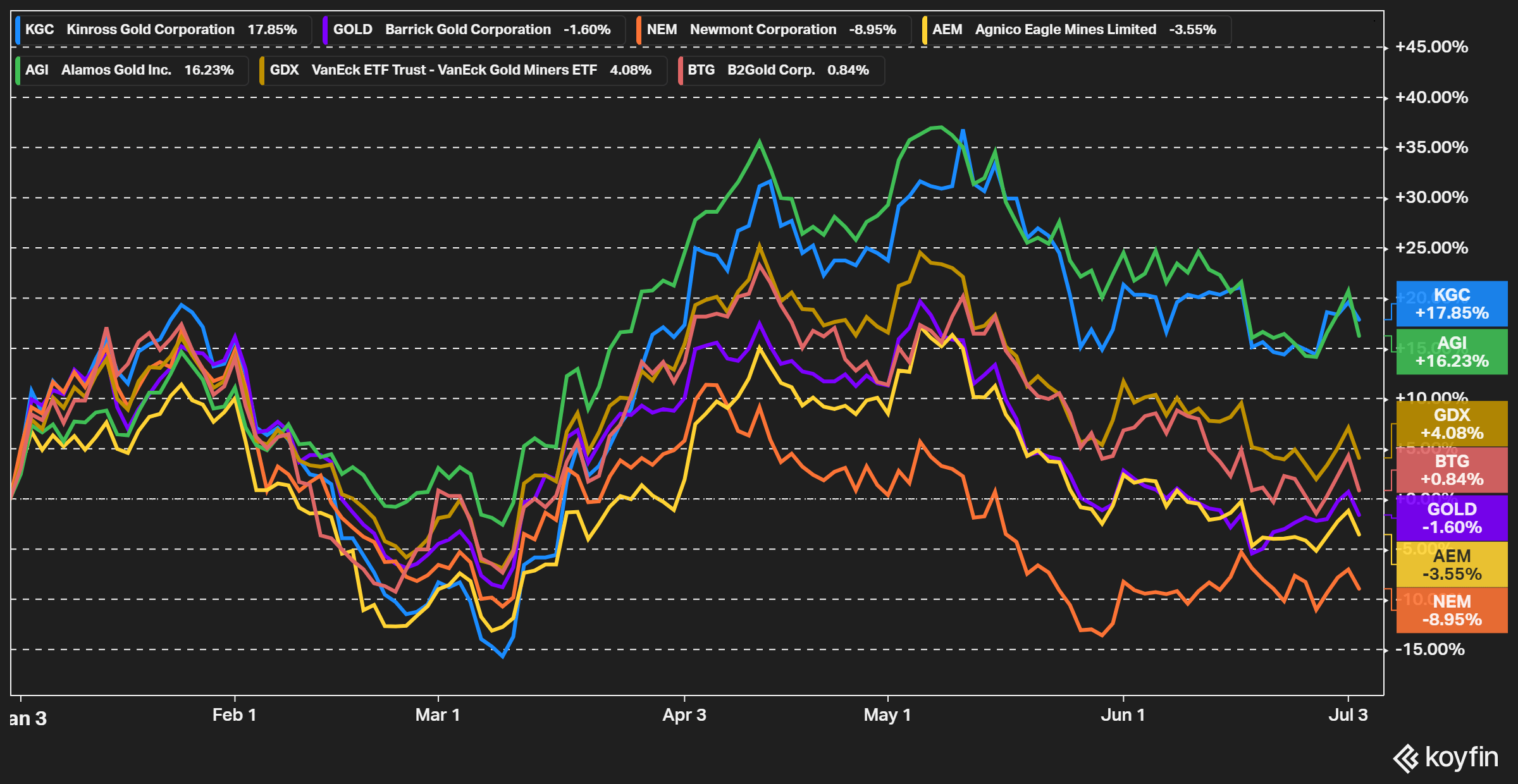

Kinross has so far held up relatively well in 2023, which is most likely due to the strong operational performance and a good capital allocation strategy. The stock has outperformed the GDX and most of the larger gold producers so far this year.

{kind=link}

Last year, Kinross implemented a new capital allocation framework, and the stock price has since that time performed well on an absolute and relative basis. The company has committed to using 75% of excess cash in buybacks, where excess cash is defined as free cash flow minus interest and dividends.

Operational Performance

Since Kinross divested some of its assets in higher risk countries last year, the company has primarily been focused on the Americas. With that said, the low-cost Tasiast mine in Mauritania is a very important source of cash flow for the company, which is not without geopolitical risk.

The producing assets in the United States; Fort Know, Round Mountain, and Bald Mountain have continued to deliver consistent production. Even if we have seen more cost pressure in those assets over the last few quarters.

That cost pressure has to a large degree been offset by higher production volumes and lower costs in Tasiast and Paracatu in Brazil. The ramp up of La Coipa in Chile means that mine has started to have more of a material impact lately as well.

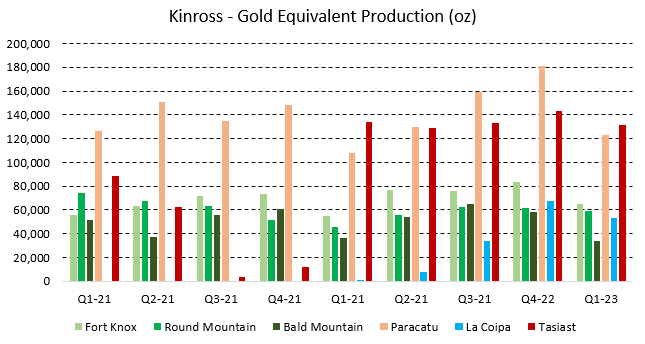

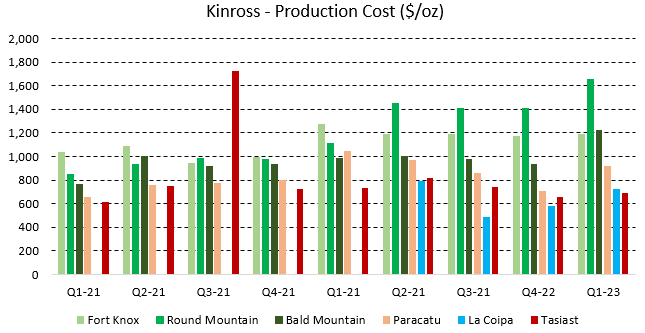

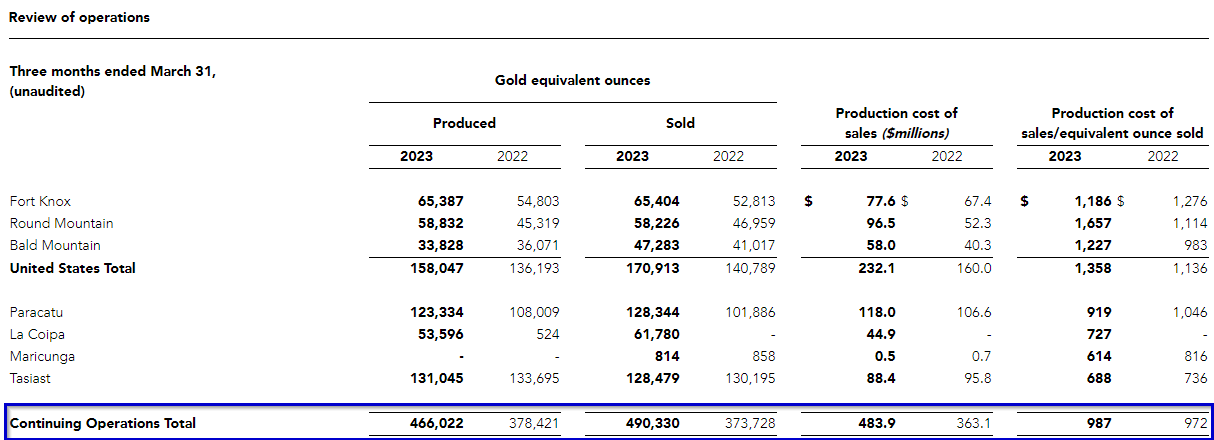

Figure 3 - Source: Quarterly Reports Figure 4 - Source: Quarterly Reports

{kind=link}

{kind=link}

The divested Kupol and Chirano assets were still included in Q1 last year, but if we just look at continuing operations in Q1-23 on a consolidated level, we can see that the company has seen a healthy production growth year-over-year and cash cost is about flat compared to last year, which is better than many peers.

Figure 5 - Source: Q1-23 Result Press Release

{kind=link}

Valuation

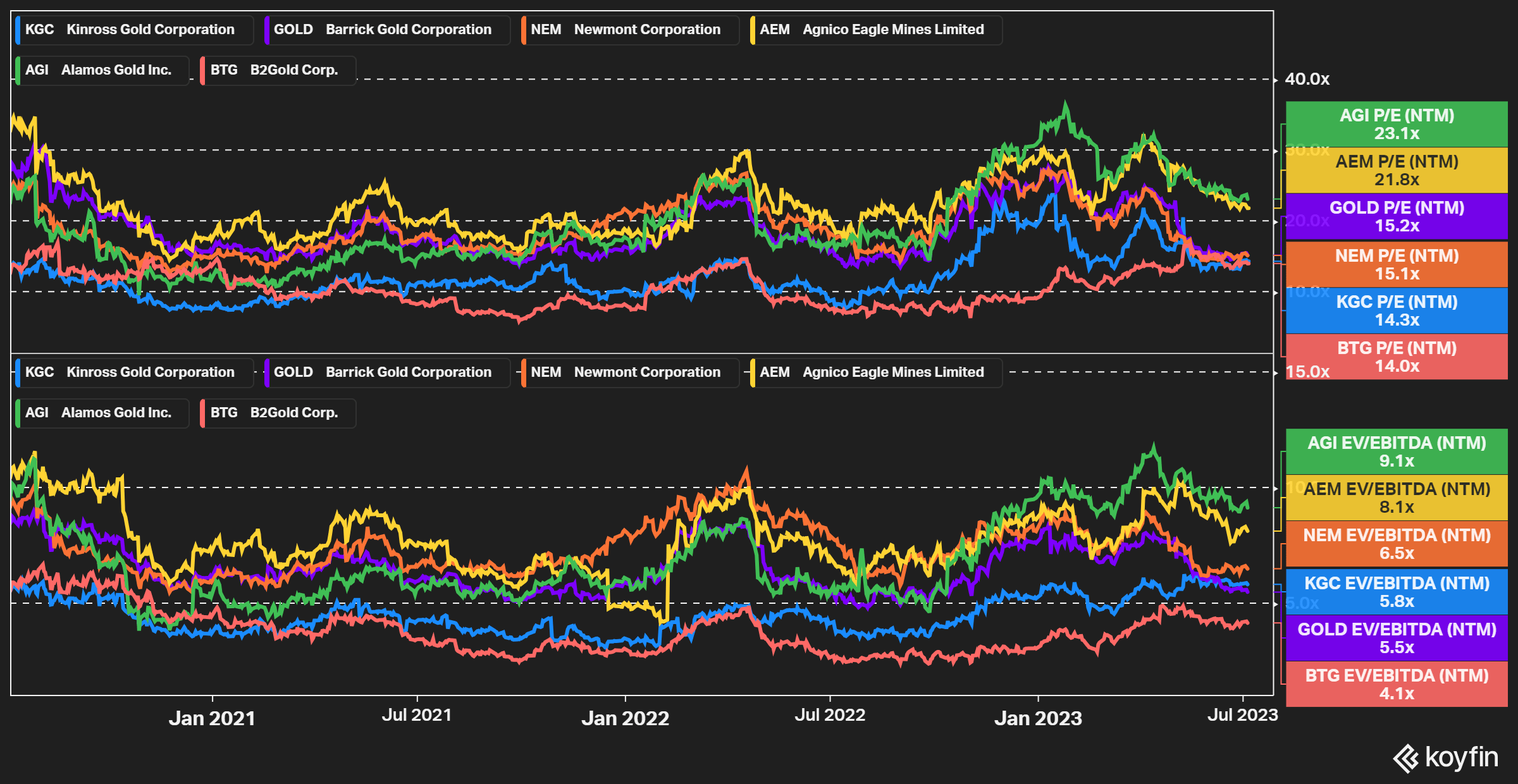

In the chart below, we can see the forward-looking EV/EBITDA and Price/Earnings ratios for Kinross and some peers in the industry. The valuation has increased compared to the more depressed levels in 2022, for both Kinross and the other companies. Even I don't view an EV/EBITDA of 5.8 and a Price/Earnings ratio of 14.3 particularly expensive though.

{kind=link}

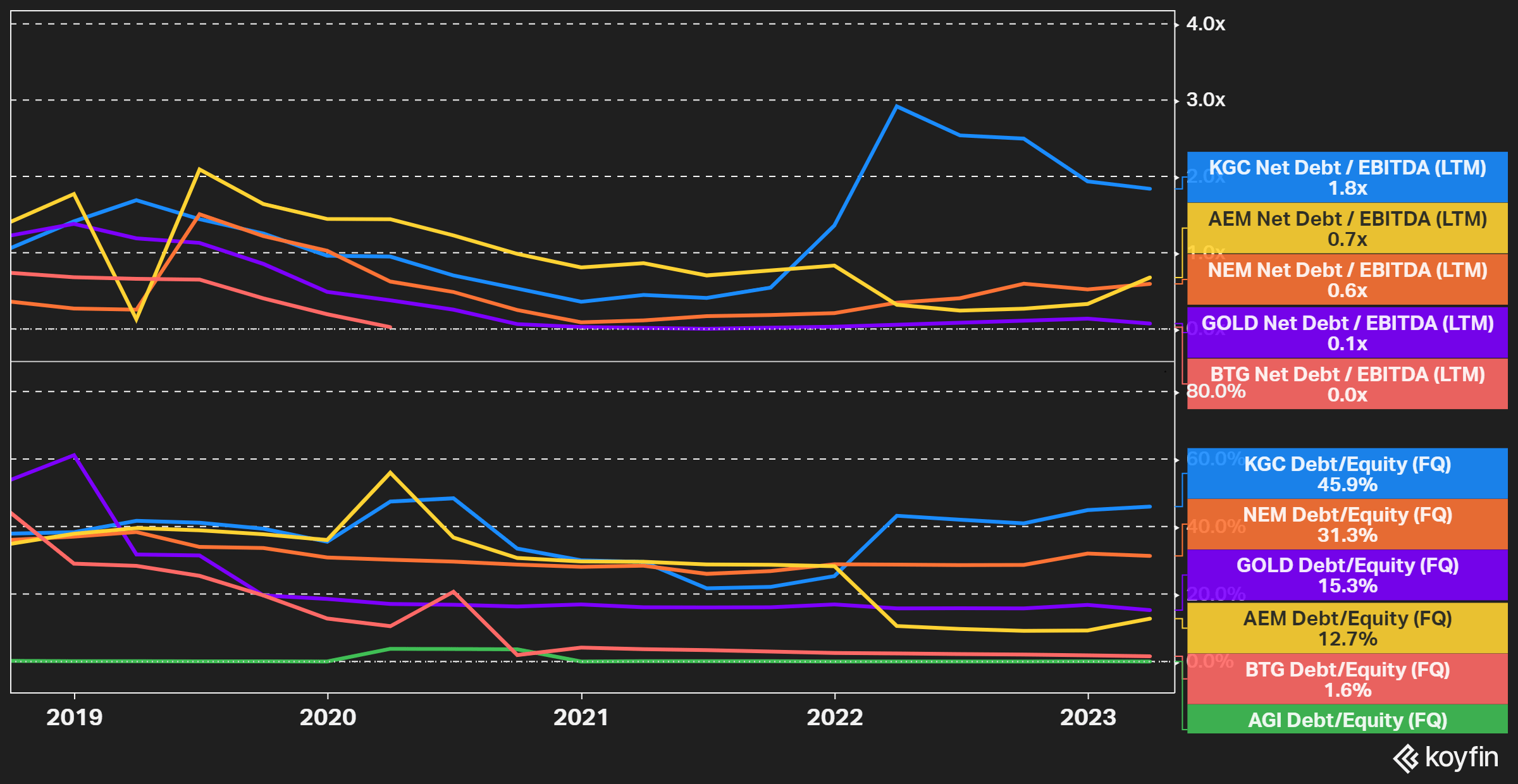

It is worth pointing out that while many other gold producers have chosen to deleverage substantially over the last few years, Kinross has instead focused on returning more cashflows to shareholders. I certainly prefer the Kinross approach, but the higher financial leverage is a potential risk to be aware of.

{kind=link}

I don't think a Debt/Equity ratio of 46% is particularly excessive. It is also worth noting that Kinross was very recently able to issue $500M of debt for 10 years , at a fixed interest rate of 6.25%, which is a sign that the market probably does not view the leverage of the company as excessive either.

Conclusion

Kinross has done a good job with its operation over the last year, which shareholders have been rewarded for.

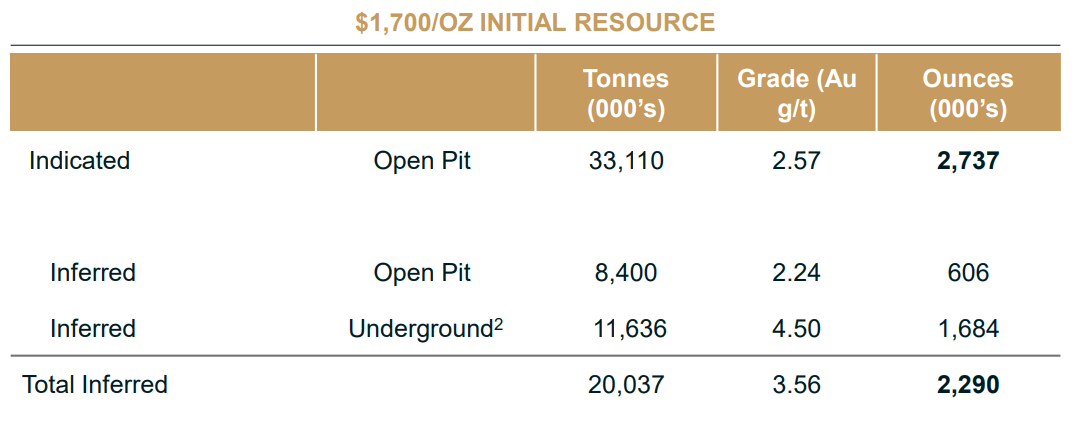

The company also has some very interesting development projects in the pipeline. Great Bear is the most interesting project, with good long-term potential. However, in retrospect, when we consider the total ounces to date and how other development projects are valued today, it is certainly fair to say Kinross overpaid for this asset.

Figure 8 - Source: Kinross 2022 Annual Report

{kind=link}

In 2030 and beyond, Great Bear might become the flagship mine for Kinross. We will probably get a better indication of the potential with a preliminary economic assessment, due in 2024, but we are still likely 5+ years from production.

Figure 9 - Source: Kinross Corporate Presentation - Great Bear

{kind=link}

I like Kinross, which has delivered operationally lately and has a good capital allocation strategy. The valuation is relatively attractive, but far from the extreme levels we saw last year. I wouldn't expect the stock to get that depressed in the near-term, but I would need more of a correction to consider adding it back to the portfolio.

For further details see:

Kinross: Strong Operational Performance Lately