KIO - KIO: Setting The Story Straight For This 12%-Yielding Credit CEF

2023-09-27 08:31:45 ET

Summary

- We take a look at KIO - a credit CEF which has attracted a number of misconceptions.

- These relate to the fund's absolute and risk-adjusted performance relative to both stocks and other credit CEFs.

- KIO is not an attractive holding at present given extremely low-quality allocation in an expensive credit market environment.

In this article, we take a look at the credit CEF KKR Income Opportunities Fund ( KIO ) which raised some queries from our subscribers about its performance and risk profile.

Our main takeaway is that investors should avoid a happy-go-lucky style of investment analysis and instead, carefully interrogate any statements made about risk and performance. This will help avoid nasty surprises and behavioral pitfalls and should increase the likelihood of investors achieving their goals.

Our view is that KIO is not an attractive fund at present despite its high yield and wide discount. This is because KIO has one of the lowest-quality holdings in the CEF space and credit valuations remain expensive. An up-in-quality allocation makes more sense at the moment as they would remain much more resilient in a likely sell-off. Once valuations come off the boil, KIO will be worth a look.

Key KIO Misconceptions

In this section, we discuss some of the misconceptions that we have seen around KIO.

KIO is attractive because it allows income investors to invest alongside professional money managers who invest millions of dollars for living.

This sounds sensible however it's a tautology. Any publicly traded fund is, by definition, run by professional managers. We are not aware of any public fund that has less than a million dollars of total assets which also means that these professional managers invest "millions of dollars" for a living. In this sense, nothing separates KIO from any other publicly traded fund.

KIO is attractive because it allows investors to earn equity-level returns without exceeding equity-level volatility

A lot of income investment analysis is of the have-your-cake-and-eat-it-too variety. This type of analysis suggests that income investors don't need to make the usual trade-offs between risk and return when they allocate to credit over equities.

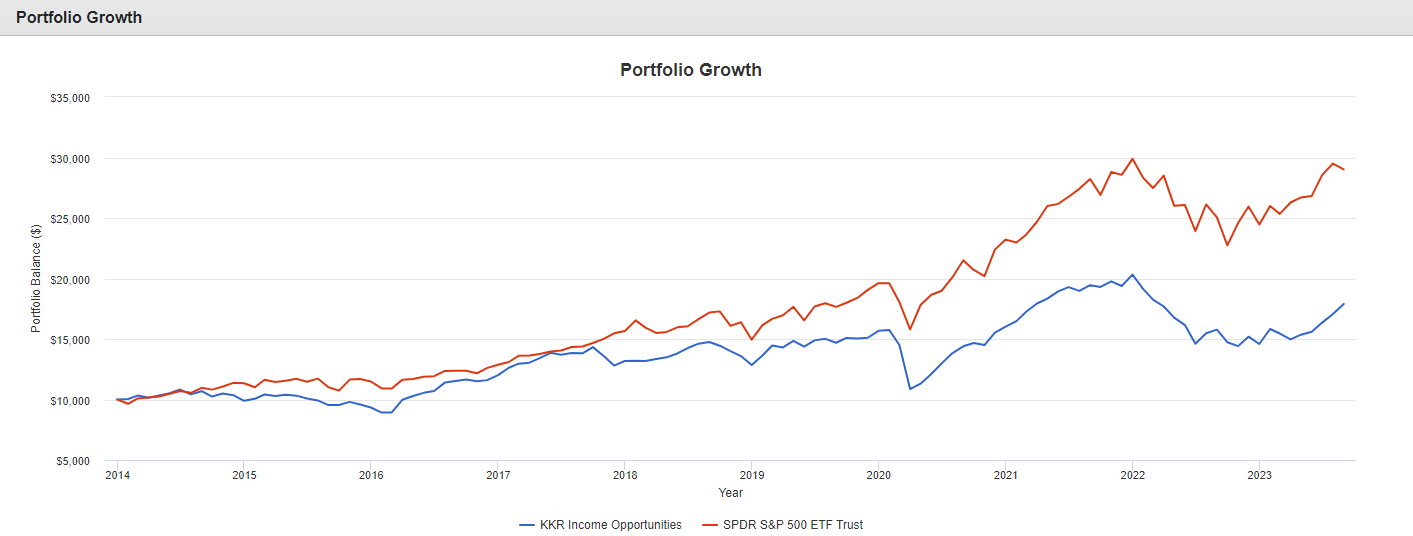

This is precisely the opposite, however. As the chart and table below shows KKR (blue line) has underperformed stocks (proxied by SPY - red line) by a large margin while having a higher volatility in the process. It's true that KKR NAV has a lower volatility than stocks (if not by much) however its Sharpe ratio (return / volatility) is exactly half that of stocks. Moreover, both the price and NAV drawdowns of KIO exceeded those of stocks.

{kind=link}

{kind=link}

None of this is to say that investors shouldn't own credit. KIO has some of the lowest-quality assets across credit which largely explains its high level of volatility - more prosaic credit assets exhibit much lower levels of volatility.

However, while credit assets remain compelling holdings in income portfolios, there is no reason for investors to delude themselves and think that there is no trade off to be made by holding credit over stocks, particularly in the context of long-term returns. Stocks have delivered higher returns over the long-run than credit historically. This is not an argument to avoid credit but it remains a fact.

KIO is attractive because its 10Y return is among the best of its bond fund peers and because its 1-year return is very strong.

There are several pitfalls when analyzing KIO returns, many of which are contained in this statement.

For one, KIO does not have a lot of peers. Its allocation is roughly split between corporate bonds and loans - that's fairly unusual for CEFs most of which tend to lean to one asset class or another. ARDC is among a handful of other CEFs that have fairly balanced bond and loan allocations. For this reason a "peer" comparison is either largely meaningless (as it would only encompass a handful of funds) or misleading as it implies a pure bond or pure loan CEF is a peer of KIO which it obviously is not.

Two, it's always important to consider structural tilts in performance analysis and avoid viewing funds as a black box. When comparing KIO to bond CEFs (CEFConnect puts KIO in the bond sector) the most important structural tilt is its low duration at just 1.87. This low duration is a direct consequence of its low allocation to bonds. CEFs that allocate primarily to high-yield corporate bonds tend to have duration on the order of 4-5.

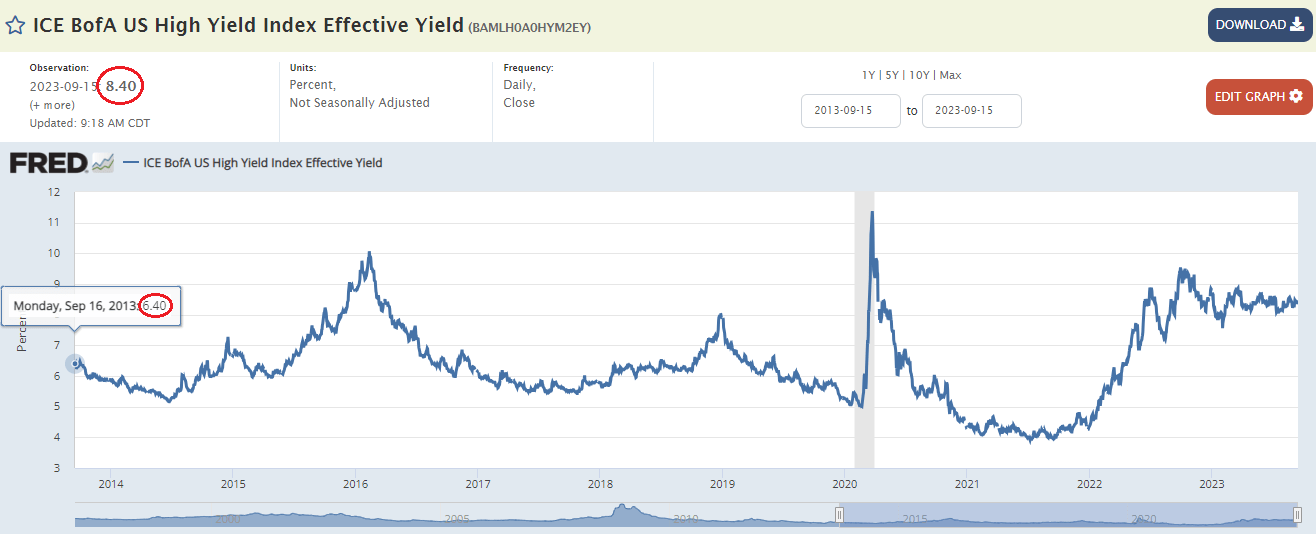

What has happened to high-yield corporate bond yields over the last 10 years? They have risen by about 2%. What this means is that KIO was not hurt as much as an average bond CEF by this dynamic.

{kind=link}

In other words, comparing KIO performance versus bond CEFs over nearly every historic period is not really apples-to-apples as it ignores the impact of interest rates.

Once we take this into account it comes as no surprise that KIO has underperformed the Loan CEF sector over all 1Y, 3Y and 5Y historic periods. The thing that drove most of its outperformance against HY bond CEFs is also the thing that drove its underperformance against loan CEFs.

Systematic Income CEF Tool

Let's turn our attention to the 1-year performance. As we highlighted above KIO has another unusual structural tilt which is its extremely low-quality profile at 40% of the portfolio in CCC assets - 2-3x that of most other sub-investment-grade focused CEFs.

Let's ask the question - what has happened to various sub-investment grade assets over the past year? The answer is that credit spreads of these assets have rallied sharply. What tends to happen is that lower-quality asset spreads tighten more during rallies and vice-versa. This is a kind of beta that credit assets tend to feature.

CCC spreads have tightened by 2.8% while B spreads have tightened by only 1.1%. In other words, KIO did well over the past year not because of any special nous but because of its higher beta profile. In fact, its NAV volatility is among the highest across credit CEFs - just as we would expect. Had markets fallen over the past year, KIO would almost certainly have underperformed.

Systematic Income

KIO generates a high level of income for investors and enjoys capital gains over and above this generous level of income.

We can easily cherry pick various periods to show how KIO delivered a high level of income while also driving strong capital gains. However, to understand what is really going on we only need to look at two things.

One, is the fund's total NAV return since inception of around 5.1% and compare that against the fund's yield of around 11%. The difference is roughly capital gains which comes out not positive but negative at around -6% per annum.

The second metric to consider is simply the fund's NAV profile. Had KIO truly enjoyed capital gains over and above its distributions, the NAV would be rising rather than falling over time.

Systematic Income

In short, KIO has not enjoyed any sustained capital gains over its life as its total return has significantly lagged its historic yield.

Takeaways

The misconceptions that seem to surround KIO also relate to other credit assets. For investors to make the most clear-eyed decisions, they need to be made in light of facts rather than wishful thinking. A happy-go-lucky investment approach where credit investors don't have to make any trade-offs in their allocation is unlikely to deliver in the long-term.

In fact, KIO, as other credit assets, has underperformed stocks over the long-term in both absolute and risk-adjusted terms. It is also not an appropriate holding at the moment given its very low-quality profile and expensive credit valuations facing investors today.

Once credit valuations correct, as they always do, KIO is nearly assured to underperform. This is why an up-in-quality allocation makes more sense to us at the moment and why we are avoiding KIO at present.

For further details see:

KIO: Setting The Story Straight For This 12%-Yielding Credit CEF