KIGRY - KION: So Did You 'Buy'? The 2023 Thesis

Summary

- Sometimes it seems I'm shouting myself hoarse trying to convince people that a company is undervalued, even a European one.

- At times, vindication and recovery and alpha may take years, but when it does come, it typically comes with a vengeance.

- KION has started its recovery from the doldrums. My position is already firmly in the green, but I expect much more.

- My thesis on KION for 2023 is here.

Dear readers/followers,

Since my latest article on KION ( OTCPK:KIGRY ), and I added more to my position, the company has come back to life with a roaring vengeance. A 40% bounce in a time when the market is up 2.5% means that this is more than 15x as good as the market at the same time.

Seeking Alpha KION (Seeking Alpha)

So, in this article, I'll be taking a look at why KION remains a good investment even after the latest set of data from the company and going into the 2023 fiscal.

While the company is doubtful to solve everything in a quick manner, I do believe investors are in for an excellent couple of months - and years.

KION - Revisiting the Company

So, just to be clear - 40% RoR doesn't mean it's in any way done, or that my original stance is vindicated. It's still negative from back then after all - but that is why we buy in increments, and not all at once. And KION can be a volatile business, especially in today's volatile environment.

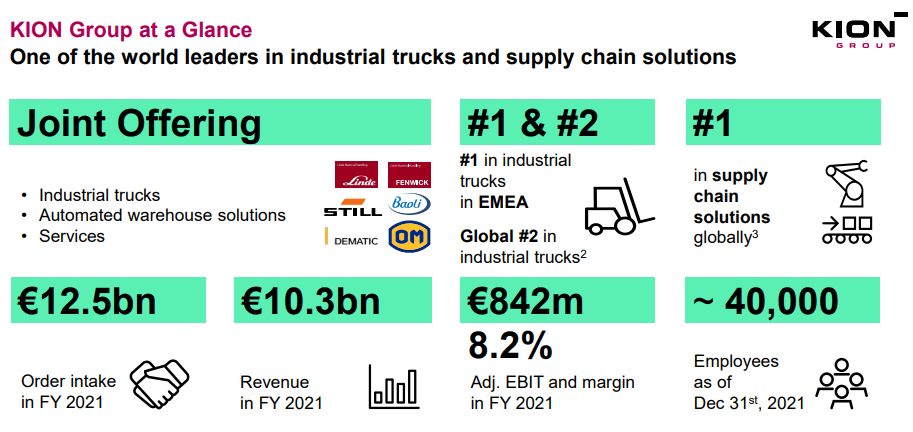

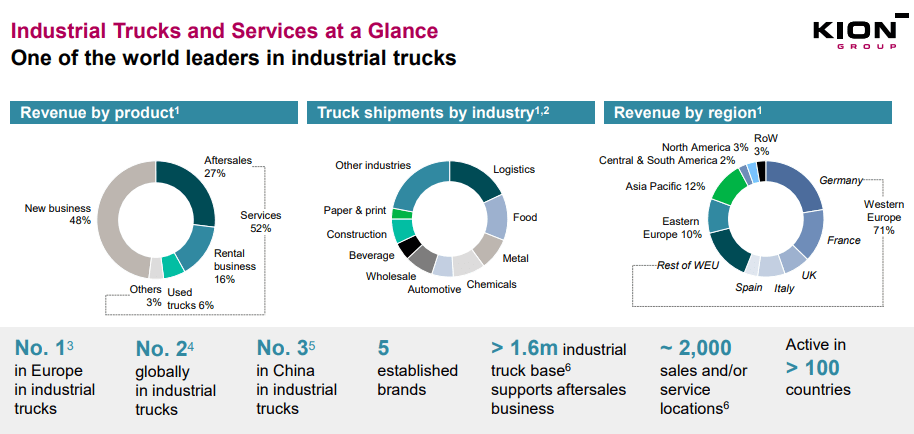

This German truck solution leader with a global 1-3 place in every single segment it operates in, including a coveted #1 in global supply chain solutions has seen some significant market and macro pressures turn its business upside down for the past few years. It hasn't been easy, but it also has had no real potential to de-rail the fundamentals of a market leader, as is evidenced by how KION has been doing during the 22 fiscal. Managing close to a billion euros in EBIT from €12.5B in orders, and employing 40,000 people across the world, this company has one of the more attractive business models that exist in the segment.

Now, the fundamentals for the business or the reasons why I believe you should invest in this company haven't changed materially since my last piece. Neither have the targets - not as such, at least. But a 40% change in price is a reason for an update, no matter what has happened, and we do have some new numbers to look at.

{kind=link}

KION is one of those companies that becomes extremely attractive at a low valuation. Slightly undervalued, or fully valued, it's not all that great. Its yield isn't superb, and it doesn't grow much as such compared to some other businesses. It has solid operations and solid management, but the real appeal comes when that price dips and we can pick it up on the cheap - because that's when this company can cause 100-300% ROR.

3Q22 is the latest set of financial results we have presented to us. The company is slated to present 4Q22 and FY relatively soon, and I may provide an update to this article when this happens if the update changes the thesis in a material way. However, I believe the forecasts are clear enough to where this shouldn't be necessary, and we should be able to work off guesstimates and actuals for the first 3 quarters.

The company has assigned a new CFO starting in April, refreshing the company's C-suite somewhat. These are small changes, and they don't detract from the ongoing 3Q22 challenges, including the major things such as SCM, Inflation, availability of components, macro, and backlog pricing. The pricing issues will likely continue until KION has either managed to re-negotiate already agreed-upon contracts or work through an unprofitable backlog in the way of Alstom ( OTCPK:ALSMY ) did with its Bombardier backlog.

Current forecasts for 4Q22 and for 2022 as a whole is for the end of the year, and for the beginning of 2023, to be far better than the 2022 fiscal so far. That is not to say that there haven't been company achievements last year - market share gains during a difficult time are always to be applauded.

With regards to pricing and contracts, KION has addressed repricing with a 4th price increase as of last month, and all of the company's contracts now include price adjustment clauses, with continued work on backlog repricing. It will still take some time for this to really flow down through the backlog, but it's a good start.

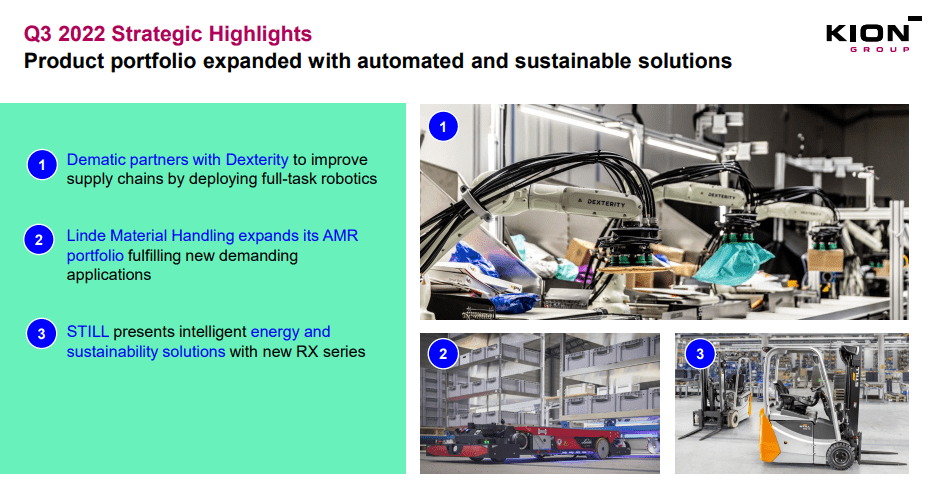

The company is also expanding its already-impressive set of offerings.

{kind=link}

And on a forward basis, not a current-level basis, the margins that the company achieves and targets, are quite impressive, with no segment showcasing lower than 10%, and Supply chain solutions at upwards of 14%.

2022 is going to be a low point, there's no doubt about that. But would you like to see the reason I'm almost at 4% KION, and why I'm even considering increasing that stake if we see another dip?

Take a look at this.

{kind=link}

No matter which way you slice it, I believe that the market leader in industrial handling here is going to be following a blockbuster trajectory of earnings for the next couple of years. These earnings will not only catapult the respective YoC to well above 6-7%, but they will also generate some truly outsized rates of return.

My thesis as of this time is largely based on this materializing, and to spend a lot of time making sure that the company's results, the company's plans, and ambitions move toward this goal. Of course, in my valuation sensitivity table (more on that in the valuation section), I do account for a bearish, base, and bullish thesis, but no matter which one ends up playing the dominant part, the upside is there.

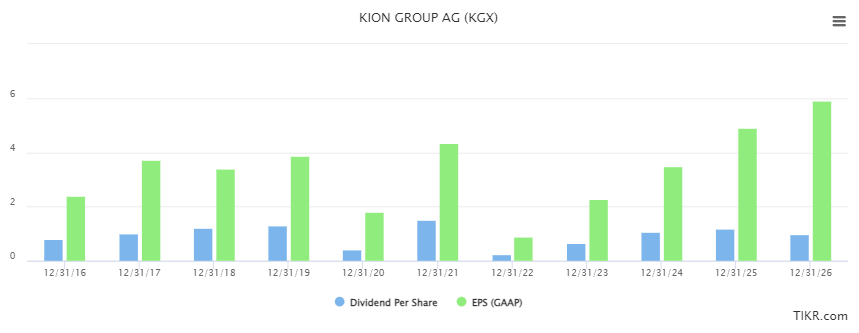

KION's 2027E strategy is leading things here, and it includes geographical diversification, more products, and more software offerings - essentially developing every part of the company with a higher R&D spend, which is what I was looking for (as opposed to trying to conserve capital, the wrong approach for a company like this). The planned shift to SCS that's going to drive much of this revenue growth is costly, which means by 2023E, the R&D split is going to be 45% SCS already, compared to less than 35% of R&D spend back in -21.

The company's products are needed worldwide - regardless of segment, product, or region, making KION a global power player in a very attractive industry.

{kind=link}

This leads me to my current valuation targets for KION, which for 2023E are as follows.

KION Valuation for 2023 - it remains attractive, and downsides are few

While the company is up over 40% since my last article, and I want to reiterate, my vindication isn't there until we see good RoR from my first article, this does not mean that the company is in any way "done". I've called the company undervalued a few times now - and this is not something that has changed for this particular time, even with that 40% price change. What has changed is the overall appeal of the company, as opposed to my last article when I "backed up the truck".

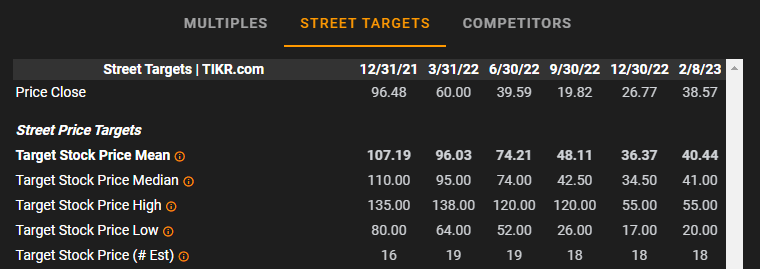

To clarify this, my PT for KION in my last article was €78/share. I'm not moving this PT at this particular time. I remind you that the analysts following KION first started with an average PT of nearly €110 about a year back in late 2021, going down to €36.3 per share at an average as of December 2022, and now back to around €40.44. The degree of uncertainty here, and "following earnings" as opposed to looking to longer-term stances is staggering to me.

KION at €100 is too expensive. KION at €20-€30 is far too cheap for what the company offers. This should be a surprise to exactly no one. As of right now, 13 out of 18 analysts are at a "BUY" or equivalent rating, but their upside based on the average is only 5% at today's share price.

I would very strongly disagree with this. I believe the ongoing growth in earnings and EBITDA going from 2022 will result in a big push. This can be seen from the contract backlog and orders, which implies that KION's appeal and demand flows haven't changed. KION will continue to sell products - just at a lower margin for as long as SCM remains impacted and input variables remain unfavorable - and this is likely to go into 2023. Once this normalizes and newer orders and contracts make up a bigger portion of the mix, the unfavorable margin impacts here will normalize, and things will likely go higher.

For KION, I use DCF, NAV, and peers as a method of evaluating. I'm not too keen on the ADR as I view it as too thinly traded - so I believe you should go for the native. The native ticker on the XETRA is KGX, and the current price for that particular listing is €38.5.

For peers, the company remains undervalued. Only Komatsu Ltd (KMTUY) is cheaper here, other than that KION is still looking appealing here. That's especially considering that current earnings metrics are heavily impacted by the way EPS is troughing at this time.

DCF is a good way to look at this company, despite earnings uncertainty. I model for a discount rate in the double digits (up from single), with a terminal growth rate beyond the reversal of about 3-4% - slightly above GDP, which implies a fair value range between €58-€79. My own PT is close to the top of that range. Why?

Because I believe the next few years of outsized growth in earnings will do much to catapult this company upward in terms of valuation - as will the increases we're likely to see in dividends. This coupled with the continued, low valuation we're seeing for what I see as a qualitative albeit cyclical company, means that my current thesis nearly writes itself. I obviously mix the various valuation approaches - but in none of the approaches or methods - peers, DCF of forecasts, we can see that €70-€80/share would be an outlandish sort of price target.

I refuse to change my targets to appease or follow other analysts, and just to illustrate my point in how this has gone for S&P Global, take a look at these trends.

{kind=link}

I'm not sure why any analyst who has a low-ball target of €80/share in December changes it to €26 in September without any sort of material deterioration of fundamentals. Same obviously, and even worse for the high-range targets.

This is not as rare as I would like it to be, but I believe it bears mentioning in this particular thesis, and to deliver understanding to you how many of the analysts you read about work with respect to targets.

Thesis

My thesis on KION is as follows:

- KION Group is an attractive capital goods play with an emphasis on intralogistics solutions, automation, and warehouse technologies - things like forklifts, to put it simply.

- The company is undervalued and forecasts imply a significant upside over the coming 5 years, with an upside of 80-110%.

- KION is a "BUY" with a price target of €78/share.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (Italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansion/reversion.

That means that the company still fulfills all of my criteria for attractive valuation-oriented investing. This is despite a 40% share-price outperformance since my last article on KION back in November.

For further details see:

KION: So, Did You 'Buy'? The 2023 Thesis