GME - Kirkland's.: Ignore The Crazy Stock Price Volatility A Turnaround Is Afoot

2023-12-08 19:27:59 ET

Summary

- Kirkland's Inc. has shown clear signs of a successful turnaround, with evidence of "green shoots" and improved financials.

- The company has paid down $27 million on its revolver in November 2023, exceeding expectations.

- Kirkland's has seen positive comps and traffic in November, indicating a potential return to growth.

Before we dive in, I just want to remind readers that I've been closely following and have invested in Kirkland's Inc. ( KIRK ) at various points in the past, starting back in May 2020.

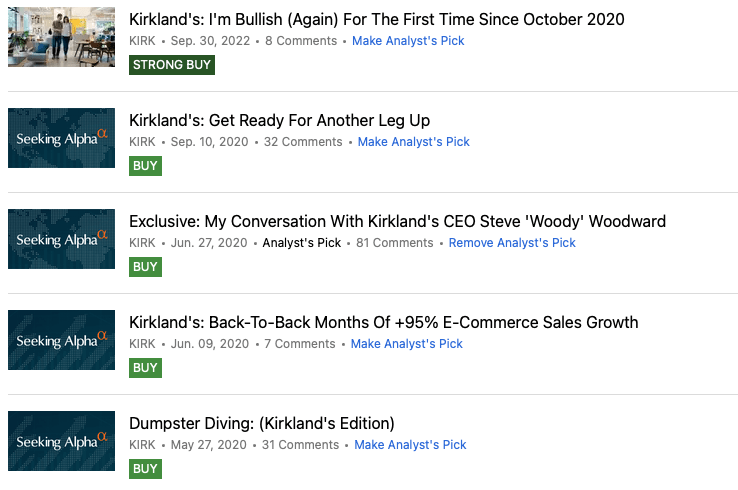

Enclosed below are the five public site articles I've written on Kirkland's.

{kind=link}

Seeking Alpha

The first write up was in late May 2020, and published at $1.14 per share. As I continued work on the name, I wrote an update piece two weeks later, in early June 2020. Then, later in the month, back mid June 2020, I had the chance to interview the then new CEO Steve 'Woody' Woodward. As I had a big Real Estate Renaissance thesis , arguably many months before some of the best minds on Wall Street, KIRK was one of names in my top names, in my long basket. Moreover, as part of a way to play that real estate renaissance thesis, I loved Kirkland's valuation and was impressed by Woody, so I loaded up on the stock between $1.75 and $2.25. Over the next six to nine months, KIRK's EBITDA power exploded upwards, as they did in fact meaningfully benefit from the COVID induced real estate renaissance along with a number of favorable business changes made by management.

Lo and behold, from the initial $1.14 stock price, trough to peak, and again driven by then record earnings power (this wasn't a Meme stock), KIRK shares went on soar to over $30, during the first half of 2021. Candidly, I started selling some shares at $7 and sold the majority of shares, between $11 and $12. A nice 4 to 6 bagger (on my average cost basis) and one of my best realized percentage wins of my young career (as of today, I'm only 43 and hope to have another 40 great years ahead). That said, selling out between $11 and $12 meant missing a 15 or 16 bagger.

In September 2022, after being on the sidelines for a few years, around $3 per share, I got back on the horse. I think I was in the stock for a few months, but the turnaround was slower to develop than I expected and I ended up taking a 15% loss, around $2.50.

{kind=link}

Fidelity

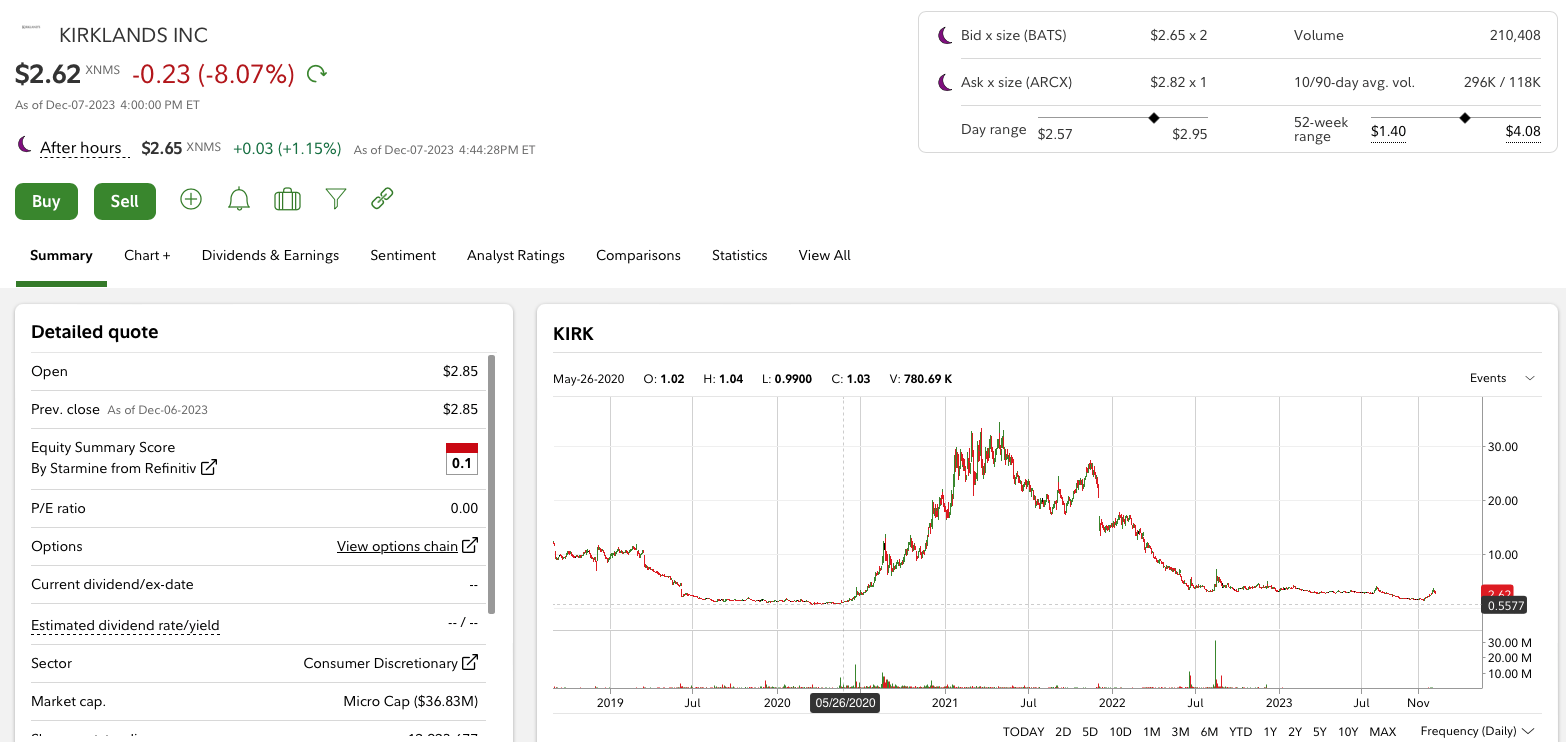

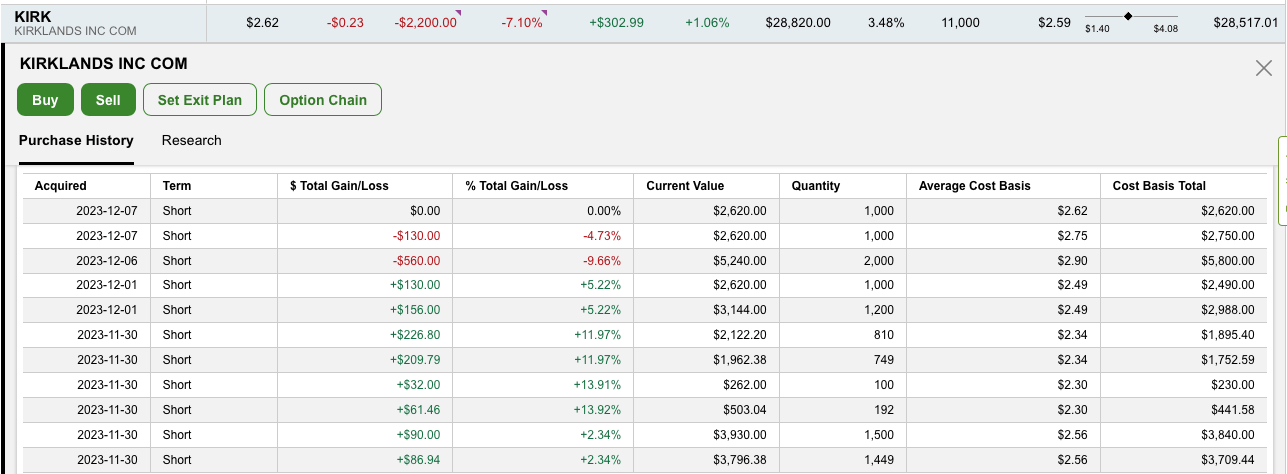

Having been on the sidelines since, on November 30, 2023, after listening to KIRK's Q3 FY 2023 conference call, I bought back into Kirkland's, at around $2.50 per share. By December 4, 2023, or only three trading days later, KIRK shares leapt as high as $3.54, resulting in a 40% unrealized gain. I did sell 30% of my position, at $3.35, but starting buying it back, between $2.62 and $2.90. Therefore, and you can see below, via my Fidelity account snapshot, I think KIRK shares are worth $4, and possibly $5 plus, otherwise I would have simply printed the 35% to 40% winner, in three trading days, and moved on.

See here:

{kind=link}

My Fidelity Existing Long Position in Kirkland's

Sorry in advance for the rather long introduction. However, I believe it is highly relevant, as it establishes that I've been closely following Kirkland's since May 2020. Secondly, has I've more or less round tripped, albeit briefly, a 40% unrealized winner (by holding 70% of the position), I figure it is worth sharing my December 1, 2023 write up, originally written to my Investing Group's members, now with the broader SA audience. To that end, enclosed below is that write up, from December 1, 2023. (I have only updated a few minor pieces to reflect a slightly different stock price and upwardly revised analyst estimates).

This Sure Looks And Feels Like An Inflection Point

Simply put, I'm about 85% to 90% confident that Kirkland's, Inc.'s management has put in a motion all of the elements required for a successful turnaround. Despite the difficult macro backdrop, we're seeing clear and compelling evidence of 'green shoots'.

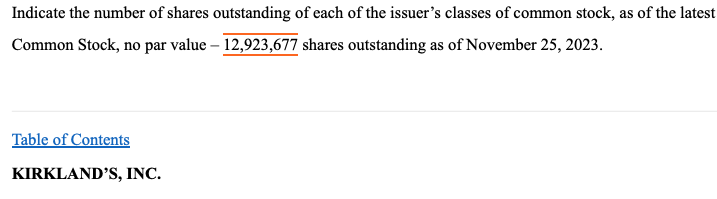

Let's start with valuation. As of November 25, 2023, KIRK has 12.92 million shares outstanding.

{kind=link}

KIRK's Q3 FY 2023 10-Q

So $2.62 per share x 13 million shares equals a market capitalization of only $34 million.

As the end of Q3 FY 2023 (October 28, 2023), KIRK had $5.8 million of cash, $105 million of inventory, $55.7 million of accounts payables, and $62 million drawn on its revolver.

So pro-forma, at the end of October 2023, we're talking about an enterprise value of $67.5 million.

However, and KIRK's November 30, 2023 press release, KIRK had a fantastic November 2023. Specifically, they were able to pay down $27 million on the revolver!

See here:

As of October 28, 2023, the Company had a cash balance of $5.8 million, with $62.0 million of outstanding debt under its $90.0 million senior secured revolving credit facility. As of November 30, 2023, the Company had $35.0 million of outstanding debt under its senior secured revolving credit facility.

The Trajectory Of Q3 Comps And Traffic

On Kirkland's Q3 FY 2023 conference call , we learned that the trajectory of comps improved nicely through the quarter.

Traffic:

- Aug.: -14%

- Sept.: -6%

- Oct.: -4%

Comps:

- Aug.: -13%

- Sept.: -9%

- Oct.: -6%

As a result, our omnichannel traffic declines improved from down 14% in August to down 6% in September, and down 4% in October. Our Q3 comparable sales improved from down 13% in August to down 9% in September to down 6% in October.

(Source: Kirkland's Q3 FY 2023 conference call)

Now get this......

In November, comps were up low single digits and traffic was positive for the first month all year!

We were able to cut our ecommerce traffic decline from negative 17% in the first half of the fiscal year to only negative 3% in October. On the brick-and-mortar front, we improved traffic from a decline of 11% during the first half of the fiscal year to down 4% in October. In November, traffic to our stores stayed positive for the first time in 2023.

(Source: Kirkland's Q3 FY 2023 conference call)

See here:

As a result, we are encouraged by a low single-digit increase in comparable sales at a much improved merchandise margin in November, which includes Black Friday.

(Source: Kirkland's Q3 FY 2023 conference call)

Wait.....it gets better:

In Q4 FY 2024, November was the toughest comp month to lap. Their upcoming December 2023 and January 2024 comps are much easier, at down 11% and down 8%, respectively!

As a reminder, November was the toughest monthly sales comparison to last year when comps were flat. Last year, December comps were down 11% and January comps were down 8%. Traffic also turned positive in November, but we remain cautious about assuming the same trend for the rest of the quarter, given continued macro uncertainty.

(Source: Kirkland's Q3 FY 2023 conference call)

Here Is Another Big Positive: They Have Taken $10 million (YTD) of costs out of the business!

For the year-to-date, operating expenses are down approximately $10 million versus the same nine months for 2022. We expect operating expenses to be down again in Q4 versus the prior year when adjusted for the additional week in this year's retail calendar.

(Source: Kirkland's Q3 FY 2023 conference call)

If you've spent any time modeling KIRK then you quickly realize that this business is super torqued to growing its comps. That is just how its financials move, at least historically.

See here:

As a result, we expect a solid year-over-year improvement in adjusted EBITDA for the fourth quarter. In the fourth quarter of 2022, adjusted EBITDA was $2.6 million.

(Source: Kirkland's Q3 FY 2023 conference call)

Qualitative 'Green Shoots'

(All quoted materials is from Kirkland's Q3 FY 2023 conference call.)

Exhibit A - Merch Margins Are Up

The five components of this year-over-year change were as follows; first, merchandise margin increased 110 basis points to 54% versus 52.9% in the prior year quarter. Lower freight rates and inventory levels, along with improved product flow, drove the increase in merchandise margin.

Exhibit B - Winning Back Lapsed Customers

During the quarter, we continue to see other promising indicators from the pivot in our marketing strategy. It is mission-critical for us to reengage our loyal customer and we are very encouraged to see a 20% increase in lapsed customer reactivation during Q3. We are seeing sequential improvement in traffic and conversion with less discounting and improved profitability. We believe those trends are a result of the strategic shift in product mix and marketing.

Exhibit C - Leaner And Cleaner Inventory Coming Into Q4

See here:

Shifting the focus to operations. We have continued to improve our discipline and accuracy in our inventory flow. We ended Q3 with 17% less inventory than last year, along with being in stock and on time with products for the holiday season, putting us in good position to meet the demands of our peak season.

Our supply chain efficiencies are continuing to increase through effective use of technology, contract negotiations, and process improvements. For example, we closed our two ecommerce hubs and have consolidated our ecommerce operations in our Jackson, Tennessee distribution center.

And here:

With more normalized levels of inventory this year, our supply chain has stabilized, allowing us, with the help of process improvements in labor management, to achieve approximately $500,000 in savings in Q3.

Exhibit D - Smartly Taking Out Costs

Our supply chain efficiencies are continuing to increase through effective use of technology, contract negotiations, and process improvements. For example, we closed our two ecommerce hubs and have consolidated our ecommerce operations in our Jackson, Tennessee distribution center.

Exhibit E - Clear Line Of Sight To 30% Gross Margins in Q4

On the other components, we continue to improve our supply chain efficiency. I think that's going to be in our favor in the fourth quarter. And if we can get some topline momentum to continue through the rest of the quarter, I think we would get back not to those historical levels, but certainly into that 30% range in the fourth quarter on gross profit, and it will depend on the leverage and the sales results as to how well we do, plus or minus. But I just think the overall positioning is better coming into this year as you look at that to last year.

Exhibit F - Getting Back To The Basics

And I think the pricing, along with furniture got too high for our customers. So, we really turned that one completely upside down, got back into sort of basics and high-value, high-unit velocity items and saw a ton of success there.

You've heard me mention a couple of times the impact and the importance of the seasonal business for us here. And I would say one kind of is a tale of two stories. If you think about Q3, Halloween had just a runaway success, probably the fastest and earliest season demand that we have seen for that business in my time here.

Exhibit G - Getting Back To The Basics (Part 2)

And then the other thing I would say is I mentioned the gift and sort of impulse category. And you've been with us long enough to know that used to be a really important part of our business, and we reintroduced that this Q4 and it's doing amazing.

Short Interest

Although the short interest isn't GameStop ( GME ) like, it is a bit elevated, at just shy of 10% of the entire share count.

As a quick throwback, as I've written on the subject of short squeezes, from time to time, enclosed is a snapshot from my April 2020 short squeeze article on GameStop.

{kind=link}

Seeking Alpha archives

{kind=link}

Nasdaq.com

Basic And Back Of The Envelop Modeling

Last year, in Q4, KIRK posted $162.5 million of sales, or a down 6.1% comp and gross margins were a disgusting low 24.8%.

If you model a 4% increase in comps given the solid November, business momentum, and the easier December and January comparisons, you arrive at something like $168 million of Q4 sales (pro-forma FY 2024).

30% x $168 million equals $50.4 million of gross margin dollars. With $10 million of run rate operating expense taken out of the business, $40 million of SG&A is possible compared to last year's $43.5 million.

There was $62 million on the revolver, as October 28, 2023, but $27 million has been paid down, in November 2023. So SOFR +250 Bps is about 8%. Based on this, Q4 FY 2023 interest expense should be no more than $1.2 million, for the quarter.

So operating income of $10 million less $1 million of interest expense plus loss carried forward and now we're cooking with gas. Depending on your tax rates assumptions, it plausible they could put up a $0.50 to $0.60 Q4 FY 2024 EPS figure.

{kind=link}

Kirkland's IR

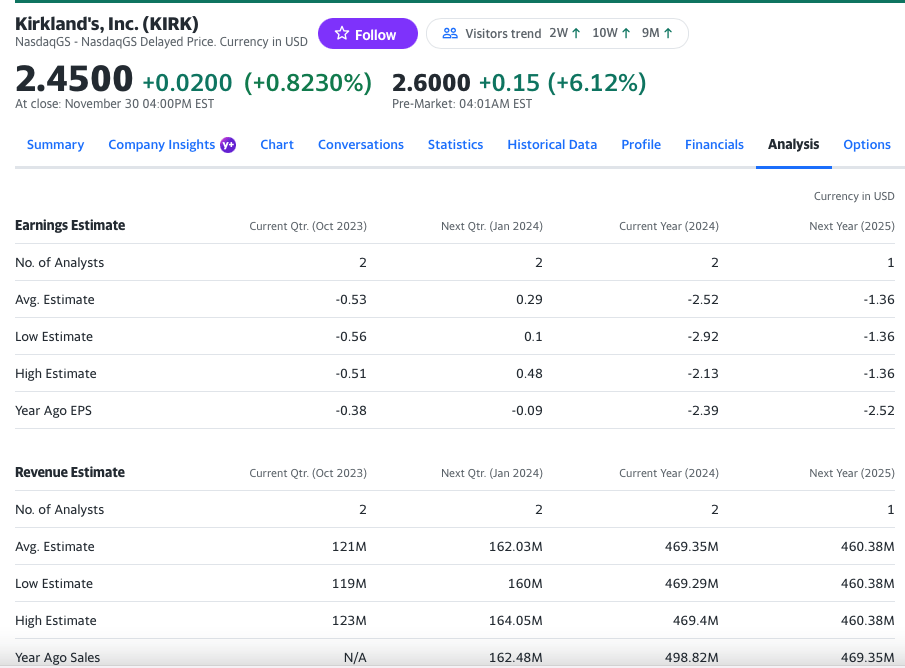

Lo and behold, as of November 30, 2023, the street was only modeling a $0.29 of Q4 EPS and no growth in sales.

{kind=link}

Yahoo Finance, as of November 30, 2023

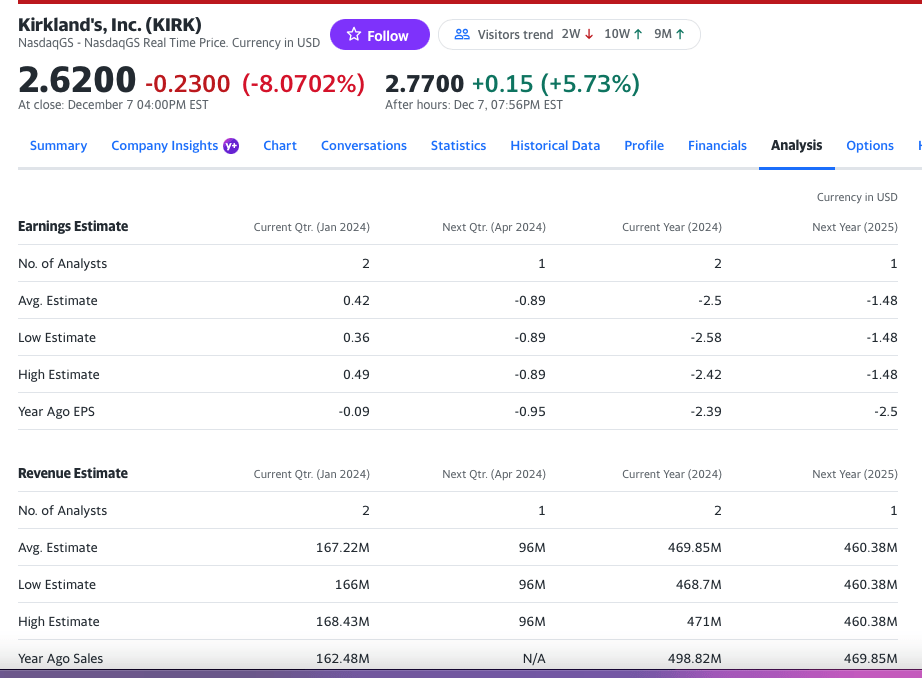

Incidentally, and subsequently to KIRK's November 30, 2023 conference call, analyst estimates have been increased, to $0.42 in EPS (from $0.29) and revenue estimates have been lifted to $168 million (from $162 million).

See below:

{kind=link}

Yahoo Finance (as of December 7, 2023)

Risks

Although I'm really excited and encouraged by Kirkland's Q3 FY 2023 conference call, notably its fantastic November 2023, which showed a major debt pay down and undeniable business momentum, Kirkland's needs to prove it to the street, and Mr. Market, that they can deliver in both calendar December 2023 and January 2024. Secondly, although its debt balance is manageable, this is still a leveraged business is that losing a little bit of money. With a very small market capitalization of only $34 million, there is limited margin of safety here. Kirkland's must continue apace on its turnaround in order to re-established its mid-single digit EBITDA power, in FY 2024, which is required to shore up its balance sheet. Lastly, as this goes without say, as this is a small retailer, with just shy of $500 million of annual sales, the company is always subject to macro headwinds, as well as merchandising and executional risks.

Putting It All Together

About three weeks ago, KIRK shares were circling the drain and changing hands around $1.50 per share. Yes, the stock is up about a $1 per share, in a short period of time. However, that is only a $13 million move in market capitalization, given the very tiny share count here. Secondly, the pay down in the revolver, of $27 million, in one month's time, is much faster than the street anticipated.

Finally, for the first time in ages, KIRK's business has some real turnaround momentum and the new CEO has correctly course corrected and reengaged with its lapsed customers base in the face of a much tougher macro backdrop. Woody was the right CEO, for that moment in time, during the Real Estate Renaissance, back when consumer discretionary spending on furniture and home decor was robust. Post the boom to bust of the business cycles, Kirkland's new management team has smartly course corrected and set off on a wiser and better business path, a plan that matches up much better with a tougher macro back drops and where they are bring everyday value and fresh variety to engage and win back its customer base.

To make a long story short, I think it is logical to suggest a strong case can be made that KIRK shares are worth $4, with a shot at $5. Again, there are only 13 million shares outstanding, the short interest is somewhat elevated, and Mr. Market (outside of a small number of hot money day traders) is slow on the uptake here. Kirkland's turnaround looks and feels real, at least to me. We shall see when they report Q4 numbers, in mid March 2024.

For further details see:

Kirkland's.: Ignore The Crazy Stock Price Volatility, A Turnaround Is Afoot