KIRK - Kirkland's: Still Weak Trade Trends And Deleverage Effect (Rating Downgrade)

2023-06-27 19:04:55 ET

Summary

- Revenue dynamics continue to be under pressure due to the negative traffic trend in the chain's stores.

- A decrease in revenue may lead to pressure on the operating margin due to deleveraging effect.

- Negative traffic trends in Q2 2023 still persist, in line with management comments.

Introduction

Shares of Kirkland's ( KIRK ) have fallen 16% YTD. I previously wrote about the company's shares , where I recommended waiting for the results for the next quarters before making a purchase decision. However, I adhered to the HOLD recommendation, now I would like to change my recommendation to SELL due to the lack of improvement in financial performance and the low expectations of the company's management regarding, in my opinion, key indicators.

Company Overview

Kirkland's is a home decor and furnishing retailer. The main sales channel is the company's retail stores, which account for about 63% of revenue, while online sales account for about 27% of revenue. As of the end of the 1st quarter of 2023, the company operates 341 stores in 35 states. The company operates in the US market.

Investment Thesis

I believe that the dynamics of the company's financial performance will continue to be under pressure in the coming quarters. Firstly, in Q2 2023 traffic in the stores of the network, in accordance with the comments of management , continues to be in the negative zone, which has a negative impact on the company's revenue dynamics. Secondly, the company's business model is sensitive to the effect of deleveraging, since most of the costs of distribution, rent, and wages are fixed. Thus, a decrease in business volumes can lead not only to a decrease in revenue, but also to a decrease in profitability. In addition, the company did not provide guidance for 2023, which, in my personal opinion, suggests that management is not confident in the pace of financial recovery during the year.

1Q 2023 Earnings Review

The company showed weak results in the 1st quarter of 2023 . The company's revenue decreased by 6.2% YoY and reached $96.9 million. The main reason for the decrease in revenue is a 4% YoY decrease in comparable sales due to a decrease in traffic in the chain's stores. Comparable sales continue to be in negative territory even from the relatively low base of Q1 2022, when we saw a 15.8% decline. You can see the details in the chart below.

Comparable sales (%) (Company's information)

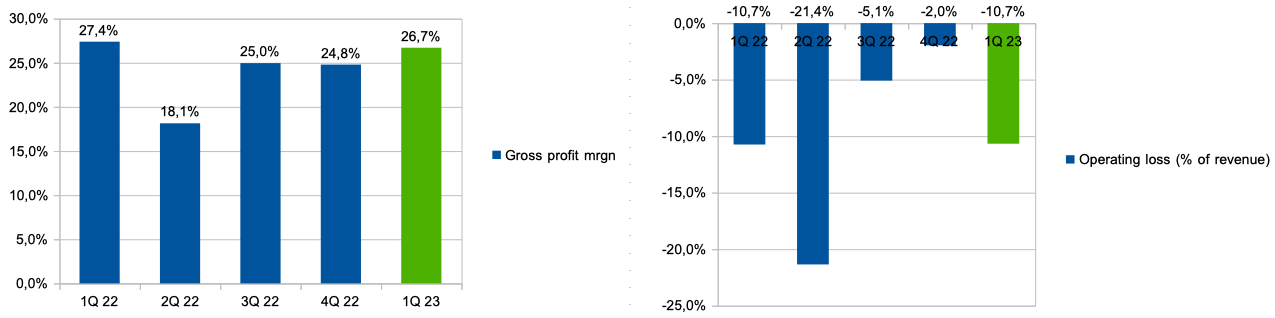

Gross margin decreased from 27.4% in 1Q 2022 to 26.7% in 1Q 2023 due to deleveraging and reduced economies of scale, resulting in distribution costs increased by 100 basis points YoY to 5.6% of revenue. The decrease in gross margin was partially offset by a decrease in freight prices. Operating expenses (% of revenue) decreased slightly from 38.1% in Q1 2022 to 37.4% in Q1 2023 due to lower advertising and salary costs. Thus, the operating loss (% of revenue) remained at the same level of 10.7%.

{kind=link}

I would like to point out that, in my personal opinion, the reduction in wage costs is due to the reduction of the variable part of wages in view of the reduction in revenue and profit. In addition, I believe that the reduction in marketing costs cannot be taken unequivocally as a positive factor, because it may lead to lower revenue in the future.

I would also like to note that the company did not provide guidance for 2023.

My Expectations

For now, I expect the pressure on revenue and margins to continue into the next quarter. Based on management comments during the Earnings Call following the release of Q1 2023 results , we can see that store traffic is still under pressure.

In the early part of the second quarter, we continue to see challenging trends in traffic counts, both in stores and online.

I believe that pressure on the top line will continue to weigh on margins as the deleveraging effect will continue because a high proportion of operating expenses such as rent and salaries are fixed. In addition, the gross margin in Q2 2023 will traditionally be at a low level due to the seasonal nature of the business and the increased volume of discounts.

I would also like to point out that earlier management has been more optimistic about the pace of business recovery in 2023 , however, we see continued pressure in Q1 2023 and I believe operating and financial pressure will continue into the next quarter.

Risks

Revenue: a decrease in demand for the company's products due to lower consumer incomes or high competition in the sector may lead to lower traffic in the chain's stores and lower sales in the online segment.

Margin: a decrease in business volumes can lead to pressure on operating profitability due to the deleveraging effect, because a high part of operating expenses is fixed (rent, salaries). In addition, the need to invest in prices due to increased competition may lead to a decrease in the gross margin.

Macro: a decline in real consumer incomes could have a negative impact on consumer spending in the discretionary segment, which could put pressure on business revenue growth rates.

Competition: the company operates in a highly competitive environment where most players have a large business scale and, investigators, large players have stronger purchasing power and higher economies of scale, which allows them to be more efficient than other companies. Thus, a high level of competition can lead to a decrease in the company's market share.

Conclusion

As such, I believe we will see continued pressure on the company's financials in the coming quarters due to weak traffic trends and continued pressure on revenues, declining economies of scale and lack of growth catalysts. At the moment, I am on a SELL recommendation for the company's shares. I will continue to monitor the company's financials in the coming quarters and will gladly change my recommendation if I see an improvement in the business's operating and financial performance.

For further details see:

Kirkland's: Still Weak Trade Trends And Deleverage Effect (Rating Downgrade)