BAM.A:CC - KKR: Private Markets Will Outperform

- KKR allows you to own its fund management side, as well as some of its private investments.

- Credit and real estate is positioned to outperform, due to their interest-linked income.

- KKR has an impressive OPM of over 54% and has been growing revenue at around 20% p.a. for over a decade. KKR's valuation does not reflect this.

- We thus rate KKR a buy.

Investment Thesis

With economic conditions deteriorating and public markets suffering, we are in search of alternative assets which can outperform markets and generate alpha in trying times. As part of our search, we have identified KKR ( KKR ).

With investments in the private markets, KKR's funds are not subject to the price swings driven by market sentiment and recent news. Thus, there is a greater importance on the fundamental value of the asset and KKR's add-value. Our bullish view is derived from the belief that KKR is able to identify and invest in the best quality assets, and in the case of PE, create value as a means of generating alpha. KKR's portfolio is positioned well, giving investors in the corporate entity access to the underlying investments, as well as income from the fund management side.

Company Description

KKR is a global alternative asset manager, founded by three ex-Bear Stearns employees who transacted some of the earliest leveraged buyouts ((LBO)). They took this expertise to KKR, famously taking over RJR Nabisco in 1989 and TXU in 2007 (The largest LBO to date). KKR is likely the premier buyout firm in the world, with very few able to transact at the scale KKR does and bring the expertise they have in turnarounds.

Beyond buyouts, KKR also has private equity, infrastructure, real estate, hedge fund and credit strategies. As of Q1 2022, KKR has $ 479BN in AuM.

Two of KKR's founders, Kravis and Roberts, still own a portion of the firm through a partnership which controls the company. They act as co-Chairman.

KKR's shares have had a turbulent time, falling 37% YTD. This is following an over 300% rise from its COVID lows to November 2021.

Recent News

KKR is one of maybe 5-10 firms globally who can regularly transact in large cap deals. Most recently, the management / board of Japanese business Toshiba ( TOSBF ) has descended into chaos , as a result of shareholder pressures and poor performance. KKR and Blackstone ( BX ) were strongly linked with a joint bid for the business, with offers in the region of $22BN. It is now being reported that KKR has taken a step back, with a preference to carve out areas of the business. This is classic KKR and likely a shrewd move. This has the potential to be the largest Japanese buyout in history and will likely involve large hurdles and agreements with the Government. Further, Toshiba is a mammoth of a business with operations across many industries. Taking a step back will allow KKR to focus on what part of the business it actually wants, reducing its risk and exposure to a business which has serially underperformed for many years.

Private Markets

JPMorgan ( JPM ) is of the belief that private equity is well positioned for the future ahead. The reason for this is the disruptive nature of innovation in many established and growing sectors. PE can provide businesses with funding to grow, and also execute large operational turnarounds.

JPMorgan's view of credit markets is less straight-forward. Their belief is that competition will increase and the key to succeed is sourcing advantages and strong fundamental analysis involved in the underwriting. This is good news for us as KKR has incredible expertise in this space and its name will inevitably open doors. I have several years of experience in the Credit space and have found that sourcing and ability to close quickly is key to the industry. KKR have the team to execute on this.

Finally, the view is that Real estate will also have a good 12-18 months, due to macro-economic factors. It is inflation-linked in both its income, through rent increasing and also value appreciation.

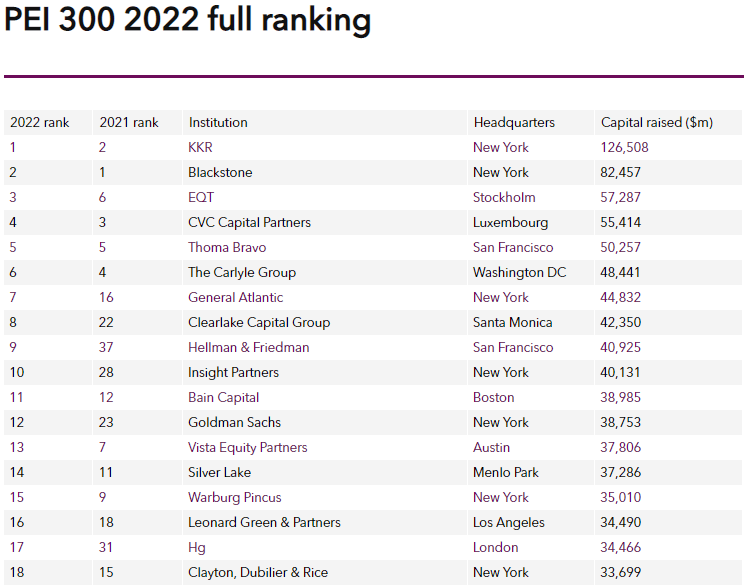

KKR can fashion itself as the most attractive PE house in the world, having raised $126.5BN in 2021, over 50% more than the No.2 player Blackstone.

PEI 300 2022 PE ranking (PEI 300)

{kind=link}

To access private markets, you need to meet certain requirements, the largest of which is capital requirements. With large amounts being invested, clearly you want the custodian of this money to be the investor with the best risk-to-return ratio historically and an attractive forward-looking pitch for how its current funds will perform. Investors have given their vote of confidence to KKR.

As of December 2021, KKR has completed more than 650 PE deals, with an enterprise value of $675BN . When we look at their current track record, it is incredibly impressive.

Private Equity

{kind=link}

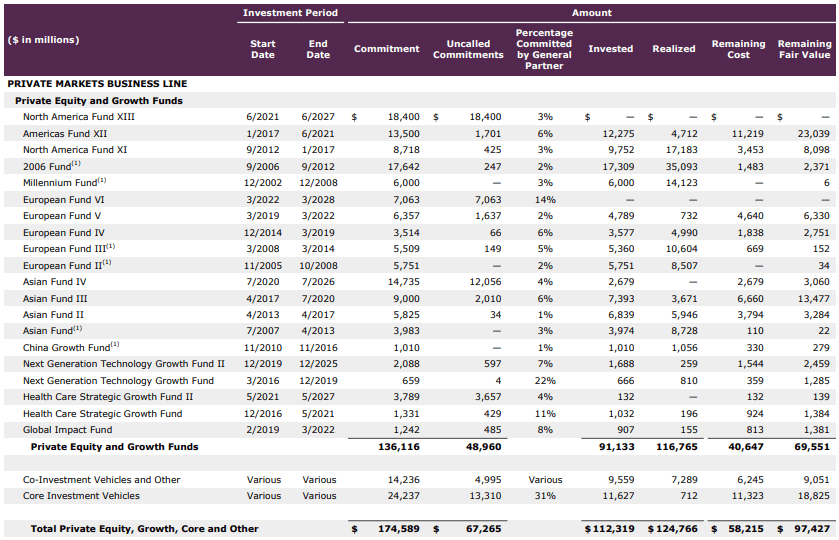

The following are KKR's current PE and Growth funds. We note that the remaining costs of the funds equal $58.2BN, with a fair value of $97.4BN. This represents an upside of 67.4%. What is more impressive is that many of these funds have a vintage within the last 3 year. Given the J-curve nature of PE, these gains are likely to increase for those funds.

Real Estate

{kind=link}

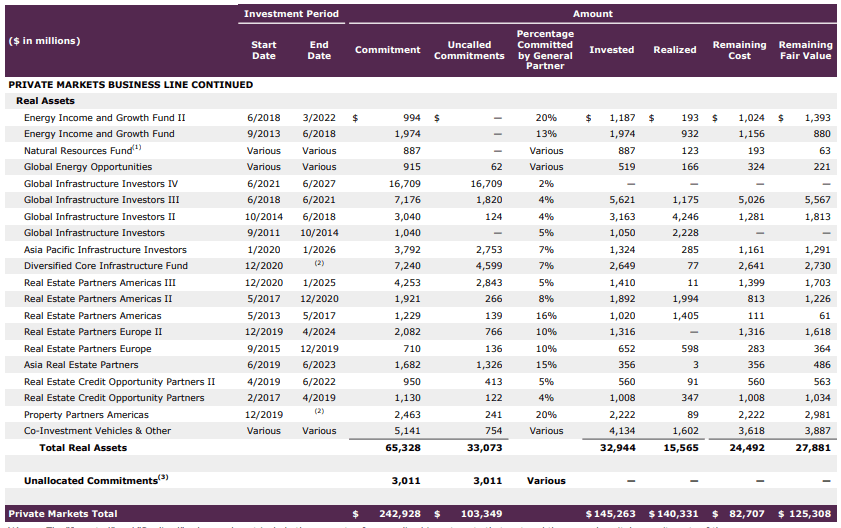

KKR's RA funds are performing equally well. Given the nature of the industry, we expect a lot less appreciation in fair value. Rental income is the main alpha generation from RE funds and infrastructure projects have a ramp up phase as the project is built.

Credit Markets

KKR Credit funds - Q1 22 ((KKR))

{kind=link}

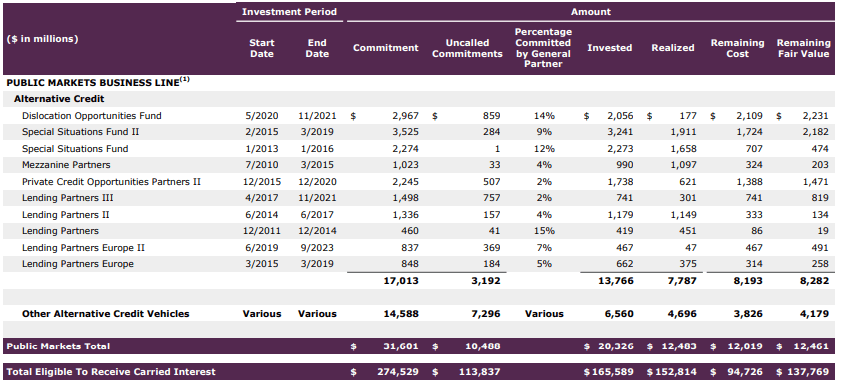

Finally, credit markets. These act similar to RE funds where the primary alpha generation is via interest repayments, as well as other debt-associated fees. It is impressive to see the fair value is slightly greater than the remaining cost, which suggests impressive risk management with low delinquencies.

With these funds being private, we are not privy to further details, such as income generation, but from what we can see KKR is clearly generating strong alpha. We will later assess KKR's profitability, which will be a proxy for whether returns are greater on a margin basis (greater returns mean more fees for KKR).

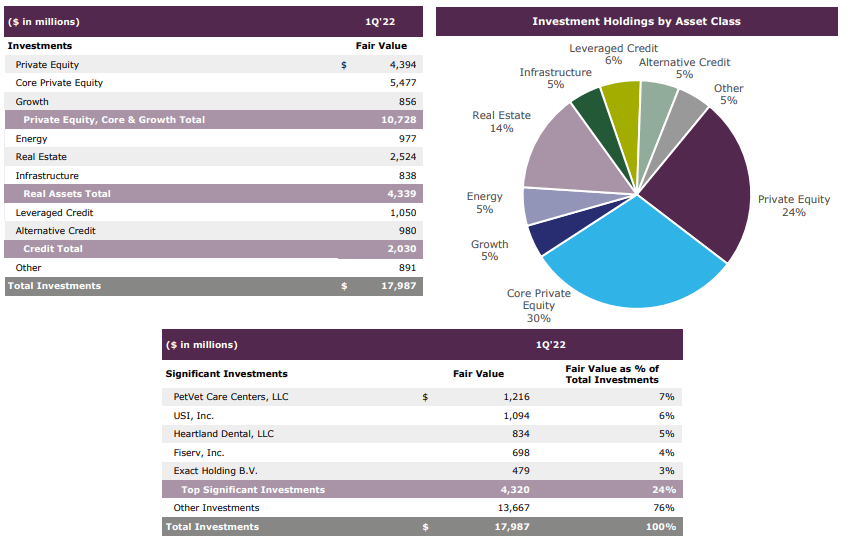

What you may be thinking is "why do we care about the funds, they are not what we own through KKR". That is certainly true, but KKR's fees are derived from the performance of the funds, with the high performance fees usually agreed for outstanding returns. Further, KKR actually owns some investments, valued at C.$18BN, as of Q1 2022. They break down as follows.

{kind=link}

We note that these investments are heavily weighted towards PE, which is slightly different to their new AuM allocation.

New AuM allocation - KKR ((KKR))

This is a logical step however, the one thing the corporate entity has that the funds do not is Asset management-related fees (Management / performance fee etc). This provides the cash income annually which can replace that coming from RA / Credit.

Financials

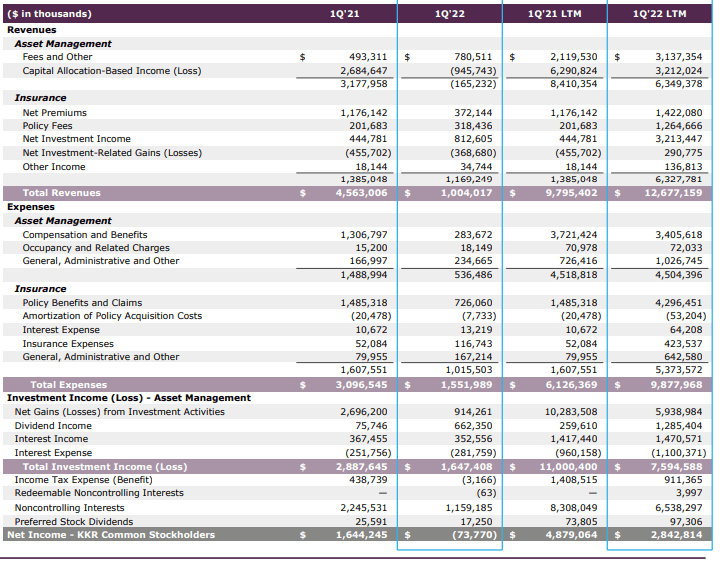

Q1 2022 Financial Performance ((KKR))

{kind=link}

KKR's financial performance has been extremely strong in recent years, as a result of the general appreciation across all asset classes. Market hesitation began in late 2021, with large falls in Q1 2022.

Historically, KKR's investment income has been greater than its AM revenues, this has now changed by a considerable amount. Given the level of AuM raised in recent years, this is likely to remain the case. The benefit of this is that it is more reliable income generation.

Since 2016, KKR has grown its revenue by a CAGR of 23.8% (Source: Tikr Terminal), this is greater than its nearest rival Blackstone. Efficiencies have allowed KKR to improve its OPM from 36.1% in 2016 to 54.6% in 2021. The business is clearly highly profitable and has benefited from the quality of the market in recent years. That being said, revenue growth from 2010 to 2017 was 19.3%, suggesting the recent spurt in AuM is not the only driver. This underpins the quality of KKR's operations. Further, OPM has only fallen below 50% for a period of just over a year, in the last 12 years. Therefore, we are not concerned about markets cooling, KKR is fundamentally a quality investor and so the growth will come regardless.

Finally, KKR's dry powder sits at $115BN, which is 24% of AuM. Contrast this with Blackstone, whose AuM is 915BN has $139BN in dry powder, representing 15.2% of AuM. Therefore, proportionately, KKR is in a much better position to support its current portfolio investments and fund new deals. Given that commitments are off balance sheet, this will not reflect in any efficiency metrics, but clearly the corporate entity's earnings are more efficient based on dollars invested.

Valuation

Peer valuation (Tikr Terminal)

When we look at valuations, KKR looks fairly undervalued. It is trading at a discount to all comparable peers, especially so when compared to BAM (APO normalized is c.10x). A partial reason for this we believe is their ratio of corporate held investments. Markets are expecting asset classes across the board to struggle and so with KKR earning a greater percentage of its revenue from this source compared to competitors, it is likely to struggle more. Our view is that downturns are inevitable, what is more important is the quality of assets held and we trust KKR's management. There is enough dry powder and cash to mean liquidity issues are not a concern.

Investment Risks

One key risk we believe is embedded within the nature of private markets. As the assets are not listed anywhere, they need to be marked-to-market. The reality of this is that we see a lag between listed asset prices moving and private, as analysts begin down-valuing their investments. Therefore, as markets continue to fall, KKR's underlying assets may still have more to go. We are not concerned from a valuation perspective, we are well aware valuations will fall further or remain stagnant for a while, causing unrealized losses. We are more concerned from a market sentiment perspective. If PE firms begin aggressively discounting their investments in the coming months, market sentiment could move quite negatively against KKR, causing short-term price action.

Final Thoughts

KKR is an alternatives stalwart. There is probably not a single individual in the industry who does not respect the firm and what they have accomplished. Our view is that their fundamental analysis is market leading and will allow the firm to generate strong alpha for its funds, and in extension its corporate shareholders via fees and direct ownership.

Economic conditions are not great but real assets and credit could do quite well, as a result of their inflation-linked income. We are not deluded enough to think this will offset equity losses, but will act as a natural hedge limiting unrealized losses.

KKR's financials are extremely attractive and a testament to their bargaining power when negotiating fees. This will certainly give investors exposure to the returns of private markets.

We thus rate KKR a buy.

For further details see:

KKR: Private Markets Will Outperform