KLPEF - Klépierre: Continues To Trade Below NAV Despite Good Results

2023-08-17 04:57:19 ET

Summary

- There are multiple factors that make European malls much more resilient to e-commerce than their US peers.

- I present these and look at the second biggest European mall landlord Klépierre which recently reported very good H1 2023 results.

- The stock offers a nearly 8% dividend yield and trades 20% below NAV.

Dear readers/followers,

I started coverage on a French-based shopping mall REIT Klépierre ( KLPEF ) back in February with a BUY rating at EUR 24.20 for the native share (LI, traded in Paris). Since then, the stock has outperformed the S&P 500 by about 50% and returned 12.5%.

Judging by the comments, many investors decided to stick with the US-based REIT Simon Property Group ( SPG ) which has done equally well. I still believe, however, that Klépierre is better positioned than SPG which is why today, following Klépierre's solid Q2 2023 earnings , I want to publish an update and highlight why I prefer it.

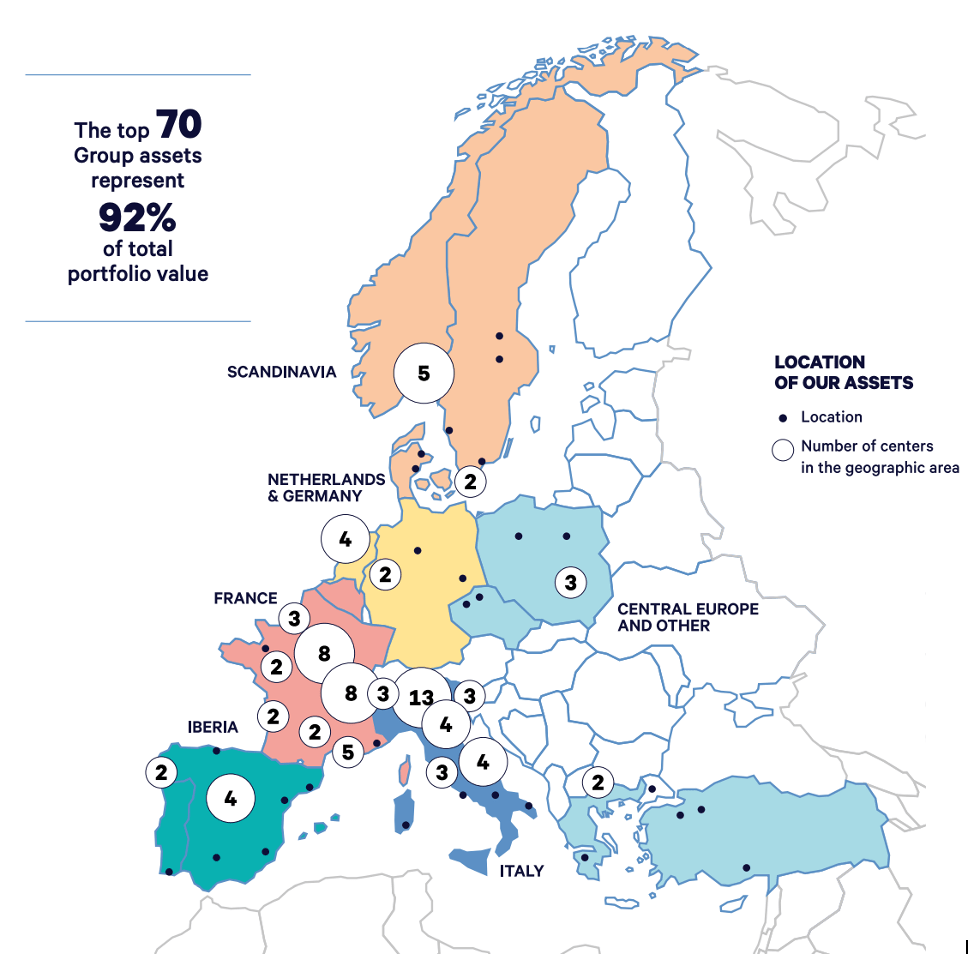

Klépierre owns over 70 high-quality, A-Class shopping malls in large European cities and is most heavily concentrated in France (38%), followed by Italy (21%) and Spain (13%). Importantly, these are trophy assets in city centers, rather than strip malls or outlet centres in more rural locations.

{kind=link}

US vs Europe

Before diving into the numbers, it's important to understand the key differences between US and European malls, because these are in large part what drives my preference for Klépierre over SPG which is entirely US-based.

Firstly, the shopping culture in Europe is quite different and I'd argue it's more resilient to e-commerce, which is probably the biggest threat to traditional retail, as the proportion of sales done online is expected to double by the end of the decade (from 14% today to 30% by 2030).

What makes European malls more resilient is the fact that malls in Europe are about much more than shopping. They are a destination, a meeting point, where people come to gather, to eat-out, exercise, watch movies, enjoy a sauna or simply dress-up and be seen in public with their Starbucks ( SBUX ) coffee. Such experience oriented tenant mix is likely to continue to attract footfall even in light of the increasing proportion of e-commerce.

The second part of my thesis for EU malls, has to do with anchor tenants. In the US, there are often large department stores such as Sears, which are of course very threatened by online shopping. In Europe, malls are almost always anchored by grocery stores, which are of course much more stable and also drive additional traffic to the mall. For Klépierre in particular, fashion stores account for 28% of all space and grocery stores for 27%.

The last piece to the puzzle is as simple as demand and supply. You see, the US has the most saturated mall market in the world with 23.5 sft of retail space per capita, while most European countries have just 3.5-4 sft of space. That makes the EU market 5-6x less saturated, which again is supportive of prime shopping malls as there's less competition.

Recent Results

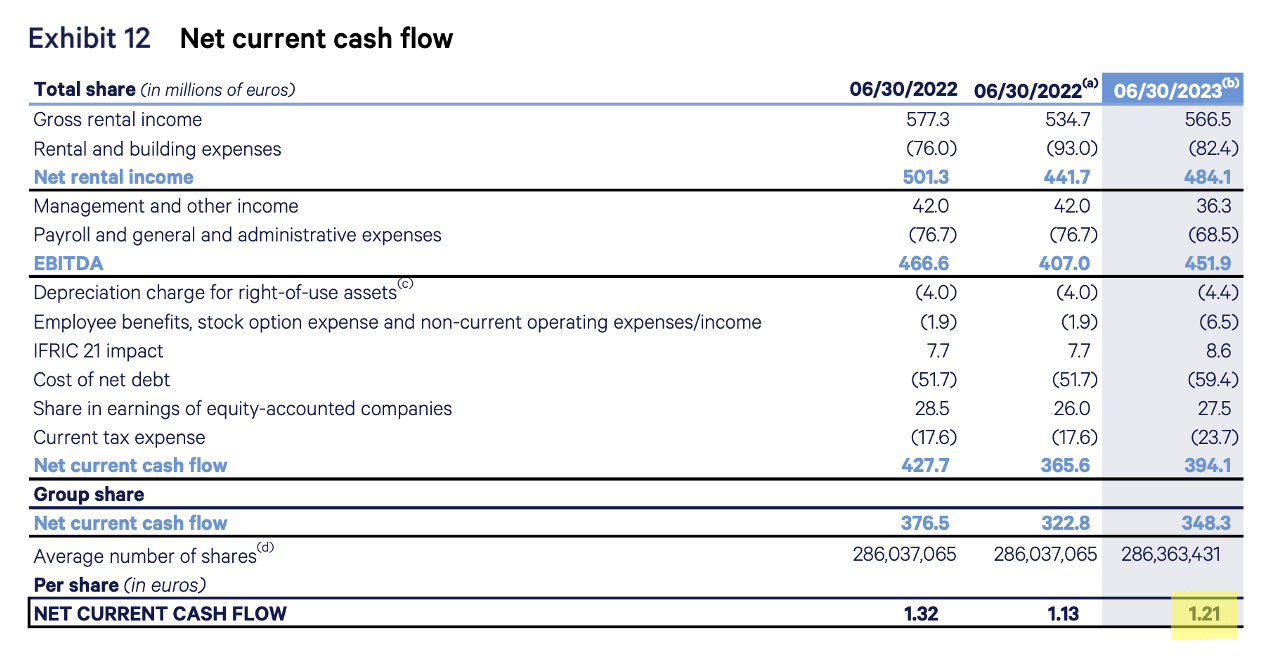

Klépierre's results over the first half of the year have been quite good as the REIT continues to recover nicely from Covid. In particular, occupancy has increased by 1 percentage point to 95.7%, collections were at 96.5% and net current cash flow for the 6 months increased by 7% YoY to EUR 1.21 per share.

{kind=link}

As a result, management has increased their full year net current cash flow guidance by EUR 0.05 per share to EUR 2.40, which represent a 7% YoY increase over 2022 numbers.

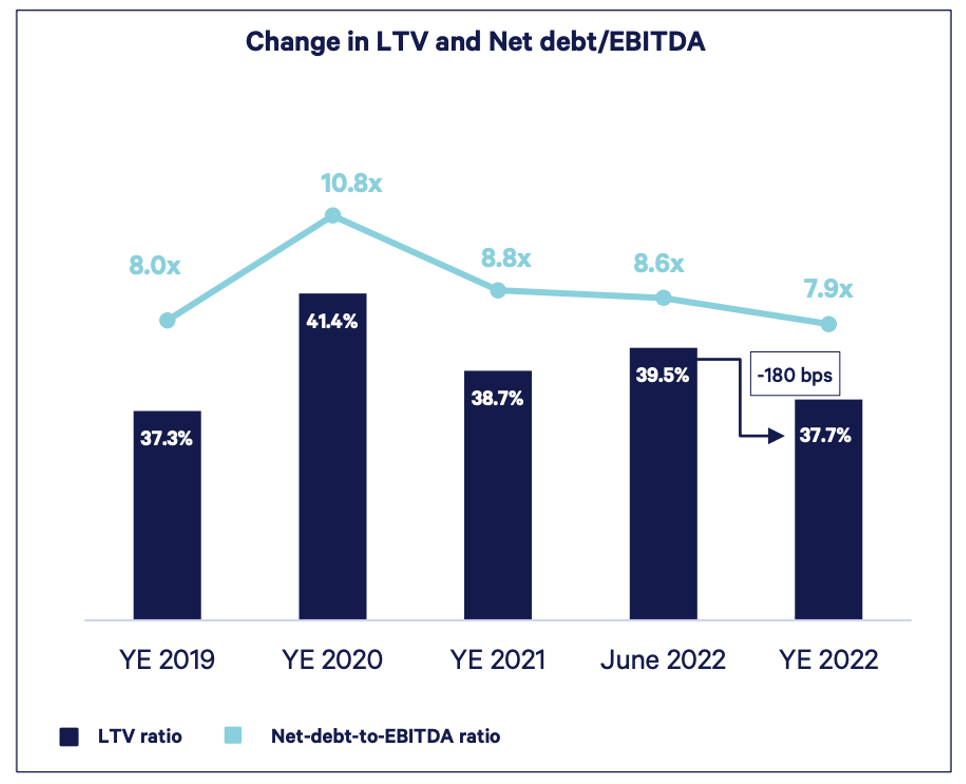

In the meantime, the REIT's balance continues to enjoy a BBB+ rating and an improving net debt / EBITDA of 7.9x (as of June 2023). Thanks to the majority of loans being denominated in EUR, their cost of debt continues to be incredibly low at just 1.4% and with 100% of interest rate risk hedged this year and 98% next year, it's unlikely that there will be any negative surprises.

{kind=link}

In terms of dividends, the REIT has increased it by 3% from last year to EUR 1.75 per share, which has already been paid. Since net current cash flow has grown nicely and the REIT currently has very reasonable forward payout ratio of 73%, I do expect a dividend hike next year in the range of 5-10%. At midpoint, that would translate to a dividend of EUR 1.88 per share or a yield of 7.8% on today price of EUR 24 per share. (Note: do your own research on withholding taxes in France as they depend on your jurisdiction).

Valuation

Looking at this year's net current cash flow, which is roughly equivalent to FFO, the stock trades at a multiple of 10x, which is in line with SPG.

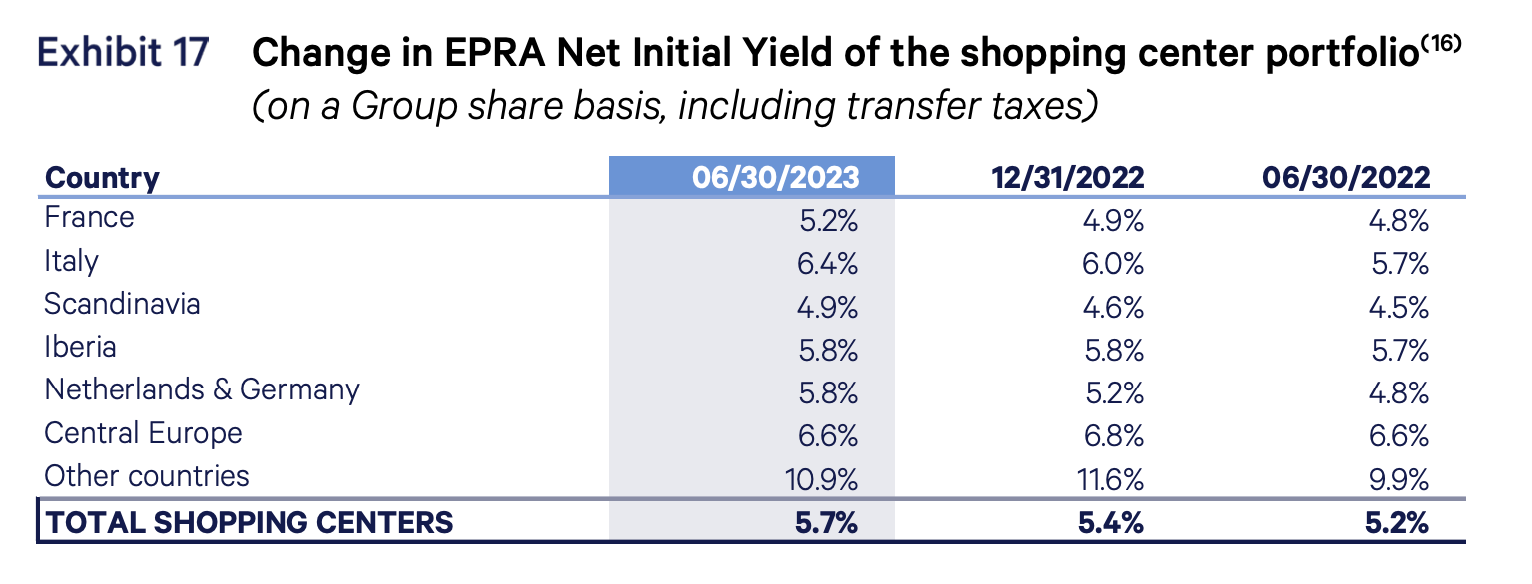

The REIT routinely updates valuations of the properties on their books (via external valuation firms such as CBRE) and currently reports the value at EUR 30.00 per share. This value is calculated with a 5.7% net yield (cap rate), which is up from 5.4% in Q4 2022 and 5.2% in Q2 2022.

{kind=link}

While I don't consider a 5.7% cap rate particularly conservative for their assets, there are some supporting arguments here:

- It's in line with market pricing according to Savills

- During the first 6 months of 2023 the company has disposed of EUR 82 Million worth of assets at these prices

Also, at the current price, we're buying the stock at a 20% discount to the reported value, which represent a large enough margin of safety, in my opinion.

I continue to rate Klépierre as a BUY at EUR 24.00 per share and continue to prefer it over SPG. I recognize that upside beyond the current valuation will likely be limited to 10-15%, but combined with a nearly 8% dividend yield, that can still produce double-digit total returns over the next couple of years.

Risks to consider

As with any investment in REITs, the main risk remains that interest rates will remain elevated for years to come. This would inevitably lead to an increase in the company's cost of capital. But I see Klépierre as well prepared for this risk with their reasonable leverage, high hedging and a low cost of capital today.

Moreover, since their tenants are retailers, there is a risk that severe recession could significantly reduce consumer spending, which would negatively impact the retailer's sales and would likely result in (1) some tenants not being able to pay rent or (2) rent discounts on lease renewals just to retain the clients. So far, however, the economy remains strong and retailer sales keep growing YoY.

For further details see:

Klépierre: Continues To Trade Below NAV Despite Good Results