KLBAY - Klabin - EV/EBITDA Near All-Time Low And Potential To Surf Brazilian Boom Market

2023-07-31 16:34:10 ET

Summary

- Klabin S.A., a leading Brazilian paper and packaging company, is a potential buy opportunity due to its resilience and growth potential despite challenging market conditions.

- The company has a diversified product portfolio, low production costs, and strong cash generation, and is undervalued compared to historical levels and peers.

- Despite potential risks such as fierce competition and cyclicality of paper and pulp prices, the expected decline in Brazil's interest rates could create a favorable economic environment for Klabin.

Investment thesis

Klabin S.A. ( KLBAY ), a leading Brazilian paper and packaging company, presents a possible buy opportunity at its current valuation and potential in the near term. The company's impressive first-quarter results , despite challenging market conditions, indicate its resilience and potential for growth. Below are some key factors supporting my investment thesis:

-

Resilient Performance : Despite facing headwinds like high inflation and restrictive measures, Klabin delivered impressive results in the first quarter. The company maintained stable volumes in the pulp market and exhibited strong growth in pulp production, showcasing its ability to manage market challenges effectively.

-

Diversification : Klabin's diversified product portfolio and customer base provide a competitive advantage. The company's presence in various segments and regions enables it to mitigate risks associated with changes in demand for specific products or regions.

-

Production Efficiency : Klabin benefits from low production costs, efficient processes, and cutting-edge technology, which contribute to its competitive position in the industry. Its development of Eukaliner, a cost-effective and environmentally friendly paper for packaging, demonstrates its commitment to innovation.

-

Strong Cash Generation : The company's solid cash generation and ability to manage its resources efficiently contribute to its financial stability. Despite increased cash costs in pulp production and inflationary pressures, Klabin achieved a remarkable 13% growth in adjusted EBITDA compared to the previous year.

-

Undervalued Sector : The pulp sector, including Klabin, seems undervalued compared to historical levels and peers. The company's valuation, when considered in comparison to sector competitors and historical multiples, indicates a favorable buying opportunity.

-

Expected Dovish Scenario : The anticipated decline in Brazil's interest rates ( Selic rate ) is expected to create a favorable economic environment for Klabin. As interest rates decrease, the company may experience increased revenues and further deleverage, leading to potential share price appreciation.

A brief description of Klabin

Klabin is a Brazilian company and one of the largest producers of paper and packaging materials in Latin America. The company was founded in 1899 and has since grown to become a significant player in the global paper industry.

Klabin is involved in various business segments, including:

Pulp : Klabin produces hardwood, softwood, and fluff pulp used in the paper industry and other applications.

Paper : The company manufactures a wide range of paper products, including kraft paper, linerboard, corrugated board, and specialty papers.

Packaging : Klabin produces diverse packaging solutions for various industries, such as food and beverages, hygiene products, electronics, and industrial goods.

Recycling : The company is committed to sustainability and has initiatives to promote recycling and minimize the environmental impact of its operations.

It's worth remembering that the company is the largest producer and exporter of paper in Brazil. It is also the largest single producer of cardboard and industrial bags. In other words, Klabin is the sole leader in all the markets it operates in. By the way, it does so in a vertically integrated manner: the company has forests from which it extracts wood, produces pulp and paper, then cardboard packaging and industrial bags.

As I write this article, Klabin has reported a $4 billion revenue, $1.55 billion EBITDA, and a 4-year average Dividend Yield of 3.93%.

A bit on last quarter’s financials

In my opinion, Klabin’s results are quite impressive and seem to have gone beyond my expectations. It's worth noting that the first quarter was influenced by factors like high inflation and restrictive measures imposed by the central banks of the United States and Europe, as well as the impact of China's reopening.

I find it interesting that despite a decrease in the consumption of virgin fibers in Latin America, Europe, and the USA, Klabin managed to maintain stable volumes in the pulp market. However, the company's exposure to the Chinese market, which is smaller, led to low demand during the quarter, resulting in increased producer stocks in that region.

The decline in reference prices for short and long fiber, as measured by the Foex index, is noteworthy – 12% and 2% respectively – compared to the previous quarter. Klabin's strategy of diversifying the portfolio of virgin fibers (short, long, and fluff) and being flexible in the geographical distribution of sales has led to a 6% reduction in realized prices during the same period.

Regarding the paperboard market, I believe it's encouraging to see the demand being driven by the growing trend of using sustainable packaging and the preference for essential products like food and beverages. It's particularly impressive that sales in the Brazilian market have surged by approximately 14% in the first two months of 2023 compared to the same period last year, as reported by the Brazilian Tree Industry ( Ibá ).

Production

In my view, considering the circumstances, Klabin's production performance in the quarter producing a total volume of 962 thousand tons, on par with the previous year, indicates a consistent effort to maintain production levels despite challenges in the market.

I find it particularly impressive that pulp production accounted for 408 thousand tons, showing a significant increase of 15% compared to the first quarter of the previous year. This growth can be attributed to the maintenance shutdown of the Ortigueira unit, which was originally scheduled for 1Q22 but took place in April 2023, leading to a positive impact on 2Q23's figures.

On the other hand, the 8% decrease in paper production, which reached 554 thousand tons compared to the previous year, is a point of concern. The decline is primarily linked to the slowdown in kraftliner exports, which might be an area that requires further attention and evaluation.

Sales

In the sales context, Klabin's sales volume (excluding wood – chart below) in the first quarter was 881 thousand tons, 2% lower compared to the previous year.

Investor Relations

The positive highlight of the sales was in the pulp segment, which experienced a growth of 12%. However, the paper and packaging segments had a negative impact on Klabin's sales, decreasing by 17% and 2%, respectively.

However, it's important to consider that the decline in these segments seems to be specific and can be reasonably explained by two factors. For instance, the reduced protein exports due to the embargo with China and the delays in fruit harvests caused by weather-related effects are significant contributors to this situation.

Results

Despite a scenario of declines in paper and packaging sales, Klabin recorded a total net revenue of R$ 4.8 billion in 1Q23, representing a 9% growth compared to the previous year (graph below). In my view, this increase reflects the price adjustments made over the last periods, which compensated for the decrease in volumes.

²: Includes wood sales and other revenues (Investor Relations)

However, there was a 5% decrease compared to the previous quarter – which I consider a natural consequence of the lower sales levels and the dollar fluctuation. On the other hand, cellulose costs increased by 5% compared to the previous year, resulting in a cash production cost of R$ 1,355 per ton at the end of the quarter. This rise, in my opinion, is justified by higher expenses related to third-party wood, a trend that is expected to continue during the first cycle of Puma II .

Looking at the graph below, it's evident that the cash cost with fibers experienced a notable increase, going from R$ 604/t in 1Q22 to R$ 806/t in 1Q23.

Investor Relations

Even with the challenges of increased cash cost in pulp production and inflation in services and labor, Klabin still managed to achieve a 13% growth in adjusted EBITDA compared to the previous year, reaching R$ 1.9 billion in 1Q23, which is quite impressive.

The company's cash generation, which considers adjusted EBITDA minus maintenance CapEx, amounted to R$ 1.46 billion in the quarter, or R$ 1,657 per ton. This 4% increase compared to the same period last year is a positive sign, indicating that Klabin is effectively managing its resources and operations.

Klabin is one of the most solid and robust companies in Brazil. It has a strong cash generation and operates in a sector where Brazil has several competitive advantages. The company maintains a comfortable debt level with a very manageable cost of debt, as indicated in the table below. Even during challenging times in the sector, the company continues to report a very robust net profit (R$ 1.26 billion in 1Q23), a solid growth/investment plan, and an EBITDA Margin ((TTM)) close to 40%.

{kind=link}

Investor Relations

Klabin’s strength points and competitive advantages

To make you understand better the overall picture, I’ll list below the points that I believe are the most important when it comes to Klabin’s edges within its sector. And then, I’ll address a few of them individually to expand a bit more on why those are indeed strength points.

-

Low production costs (scale, energy self-sufficiency, vertical integration, efficient machinery, and processes).

-

Long-lasting competitive advantage (scale with customer retention).

-

Resilient customer base (70% comprised of food producers).

-

Access to cheaper capital (presence in B3 stock exchange, scale, green bonds).

-

Cutting-edge know-how and technology (Eukaliner, productivity).

-

Lower exposure to recycled fiber price volatility.

- Product diversification: pulp (fluff, short, and long fibers); paperboard; kraft paper and recycled paper; industrial bags; cardboard.

-

Customer diversification: widespread customer base.

-

Geographical diversification: presence throughout Brazil and in various countries.

-

Production flexibility according to demand (adjusting the production mix between pulp, paper, and packaging).

-

Production flexibility according to exchange rates (increasing or decreasing exports).

Low production costs

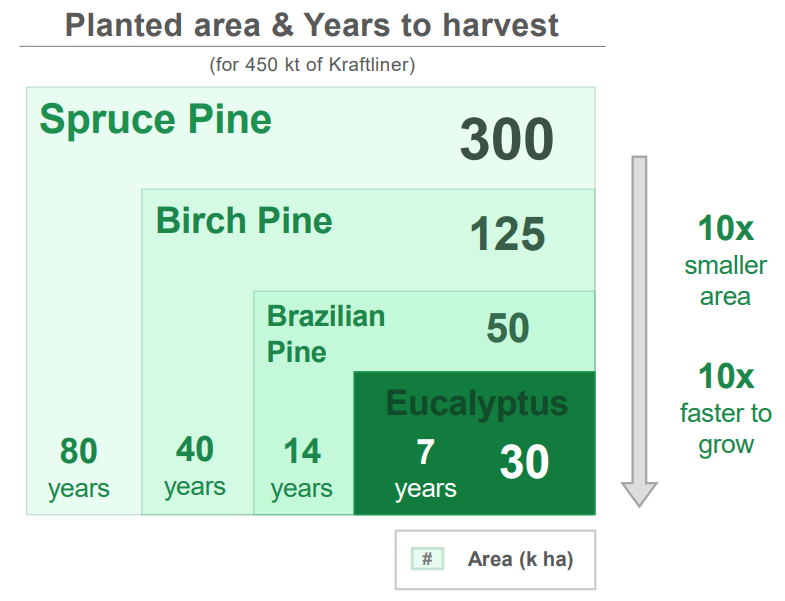

Due to its climatic and soil characteristics, Brazil has a comparative advantage in the production of eucalyptus and Pinus. It is the country with the highest productivity (volume of wood produced per hectare of land per year) and the shortest rotation (time between planting and tree harvesting). Through the development of good forest management practices and genetic improvement of seeds, Klabin achieves even higher numbers than the Brazilian average.

Eucalyptus and Pinus Productivity X Rotation (Brazilian Tree Industry)

The company also benefits from an enormous scale, efficient processes, state-of-the-art paper machines (much more efficient than the average), energy self-sufficiency, and a vertically integrated structure, which ensures a lower marginal cost. Furthermore, Klabin recently acquired a new railway terminal, ensuring cheaper and ecologically sustainable transportation. In essence, this is a commodities sector: the winner is determined by who has the lowest production cost.

Customer retention

Klabin maintains long-term relationships with its customers. They usually have two to three suppliers to avoid the risk of running out of packaging, which could halt production. The company also offers products of significantly higher quality along with competitive prices, thanks to its low costs (scale, efficiency, and vertical integration). Additionally, Klabin is the market leader in all the markets it operates, so many customers do not have significant alternatives.

Furthermore, Klabin's customer base is relatively diversified. These factors protect customer retention and reduce the risk of losing a major customer. In 2019 and 2020, only one customer accounted for more than 10% of the revenue. This customer, from the paper segment, contributed approximately 12% of the net revenue, which is around R$ 1.4 billion. In 2018, there were two customers with a 10% share. Together, they were responsible for approximately 33% of the net revenue, equivalent to R$ 3.3 billion - 11% (R$ 1.1 billion) in the paper segment and 22% (R$ 2.2 billion) in the pulp segment.

Know-how and technology

Despite being commodities, technology plays a significant role in Klabin's sector, particularly in the genetic improvement of seeds and the enhancement of product quality (such as print quality and the resistance of packaging and paperboard). Recently, Klabin has developed Eukaliner, a kraft paper made from short fiber (eucalyptus). This represents a major innovation that has received numerous awards in the market.

At first glance, this paper promises to be less expensive than regular kraftliner. The reason behind this is that short fiber (eucalyptus) is cheaper than long fiber (Pinus), in addition to having higher wood productivity per area and a shorter time between planting and harvesting. Furthermore, Eukaliner has demonstrated better performance in terms of print quality, resistance, and water retention. Not to mention that, due to its higher productivity, eucalyptus is theoretically more sustainable. In short, Klabin has created a paper for packaging that is superior, cost-effective, and more environmentally friendly.

{kind=link}

Investor Relations

Valuation and price multiples

Currently, Klabin is trading at an EV/EBITDA multiple of 6.61x, considering the EBITDA of the last 12 months ((TTM)). As shown in the chart below, this multiple is historically very low for the company, close to historical lows, which, statistically speaking, may indicate an excellent buying opportunity.

Klabin's EV/EBITDA over the years (StatusInvest)

However, when we compare the price multiples P/E and EV/EBITDA with sector peers, namely Sonoco Products Company ( SON ), Sealed Air Corporation ( SEE ), Graphic Packaging Holding Company ( GPK ), WestRock Company ( WRK ), and Billerud AB ( BLRDY ), we come to the conclusion that Klabin is trading in line with the sector. We observe that some companies appear to be expensive, while others are cheaper than Klabin. So, in general, Klabin is somewhere in between them.

Klabin's valuation metrics against its peers. (Seeking Alpha)

Additionally, we can compare Klabin's price multiples with its major competitor in the Brazilian sector, Suzano S.A. ( SUZ ). If we consider only the ratios, we see below that Suzano may be even more undervalued than Klabin, with an EV/EBITDA of 4.39x and a P/E ((TTM)) of 3.48x. In summary, the pulp sector seems to be undervalued at the moment, presenting several opportunities at the same time. Therefore, I don't consider Klabin to be a unique opportunity, but it certainly stands out from the others due to all the factors and strengths I mentioned before.

Suzano's valuation grade and metrics (Seeking Alpha)

Potential risks

Although I am indicating a buying position for Klabin, it is essential for investors to know that this decision is not without risks. Klabin is a great company that has survived hundreds of adverse factors; however, being resilient does not guarantee that it cannot generate poor returns for investors in certain periods. Below, I am listing the main potential risks investors should be aware of when holding Klabin for the long term.

Delay in factory expansion or construction of new factories : Part of Klabin's strategy is associated with increasing its market share and improving competitiveness through larger economies of scale. As the expansion of its factories involves numerous risks - including those related to engineering, construction, and regulation - the company is subject to significant challenges. These challenges can delay or hinder the smooth functioning of its projects, or they can significantly increase the costs and investments involved.

Decreased demand for products due to a possible global economic slowdown: The demand for Klabin's products is directly linked to global economic conditions, as well as the economic conditions of the markets where its products are traded. Therefore, a lower demand for paper and pulp can negatively impact the prices of these products in the market, which may harm the company's margins and profitability. It can also make it more difficult (and costly) to obtain financing for investment operations or future refinancing.

Fierce competition in the sector: Klabin has competitors in all the segments it operates in. For example, in the paper and packaging segment, its main domestic competitors are WestRock Company ((WRK)), Irani Papel e Embalagem S.A., and Trombini Embalagens S.A. In the paperboard segment, its main domestic competitors are Suzano, Ibema, and Papirus. In the pulp segment, its main competitors are Suzano, Cenibra, Braswell, and Eldorado Brasil Celulose. Finally, there are international competitors in all segments except corrugated cardboard.

Cyclicality of paper and pulp prices, which are subject to factors beyond the company's control: The performance of the paper and pulp industry is cyclical, influenced by periods of global economic expansion and contraction. Additionally, other factors impact the prices of products manufactured by Klabin, such as global production capacity and the availability of substitutes for these products.

Events related to water scarcity: The company's production process is highly dependent on water. Therefore, droughts in some regions of Brazil can lead to water scarcity and rationing, especially in areas where the company has manufacturing units.

The possible catalyst that might put Klabin ahead of international competitors

In my opinion, Klabin’s current low price multiples pose a good opportunity for investors who wish to hold the stock for the next couple of years. The reason for that is the expected dovish scenario in the Brazilian economy, which would definitely help Klabin increase its revenues through a new heated economy.

As of now, the national's interest rate, the Selic rate, is at 13.75%, which is historically high for the country and incredibly high when compared to any developed economy. Since the national CPI seems to be managed to a certain degree, I feel that the market is predicting cuts in the Selic rate by September this year already, which would probably be the first of multiple cuts ahead. These cuts would definitely provide a dovish environment for businesses in the next years and probably drive the entire economy and stock market up, including all companies in the paper sector, which seem already discounted.

In addition to that, this decline in interest rates will probably lead to Klabin’s further deleveraging, thus reducing the company's debt burden. Also, the company’s underlying assets will naturally get more valuable, reflecting on the share price. The lower interest expenses might also free up cash that can be used to invest in new ventures or opportunities.

Brazil's inflation rate since July 2022 (Trading Economics)

Final words

In conclusion, I believe that now is a good option to buy Klabin shares for several reasons. Firstly, the company's recent results have been impressive, exceeding expectations despite challenges in the market, such as high inflation and restrictive measures. The production performance has been consistent, with significant growth in pulp production, showcasing the company's ability to maintain production levels even in adverse circumstances. Additionally, Klabin's sales in the pulp segment have experienced growth, demonstrating resilience in that area.

Moreover, Klabin's robust net revenue growth, efficient cost management, and strong cash generation are positive indicators of the company's financial health. It operates in a sector where Brazil has competitive advantages, and its strong customer base and product diversification provide stability. Furthermore, the company's valuation appears attractive, and it is trading in line with its sector peers. But, the potential for a dovish economic scenario in Brazil, with expected interest rate cuts, could further provide Klabin and the entire Brazilian paper sector an edge against other international peers.

Of course, there are risks associated with investing in Klabin, such as competition, cyclicality in paper and pulp prices, and events related to water scarcity. However, considering the strengths and competitive advantages of Klabin, along with the potential catalyst of a more favorable economic environment, I believe the stock holds promise for investors looking to hold it for the couple of years ahead.

For further details see:

Klabin - EV/EBITDA Near All-Time Low And Potential To Surf Brazilian Boom Market