KLPEF - Klepierre: A Rare Income Opportunity Among The European Real Estate Sector

2023-06-27 21:51:12 ET

Summary

- Klepierre, a French real estate company, is considered a top income pick in the European real estate sector due to its high-dividend yield and attractive valuation. The company's strategy focuses on owning large shopping centers in major urban areas, and it has a strong presence in France and Italy.

- Despite the pandemic's impact, Klepierre's financial performance has shown signs of recovery, with net rental income increasing by 17.7% from the previous year. The company has also taken a conservative approach to balance sheet management, resulting in a loan-to-value ratio below the sector's average.

- Klepierre's dividend yield is close to 8%, making it attractive for income investors. The market does not expect a dividend cut in the medium term, and the company's valuation is in line with its historical average, indicating potential for earnings growth in the coming years.

Klepierre ( KLPEF ) offers a high -dividend yield and attractive valuation, making it one of the best income picks among the European real estate sector right now.

Company Overview

Klepierre is a French company focused on the real estate market, being one of the largest European players within the shopping center segment. Its current market value is about $6.8 billion and trades in the U.S. on the over-the-counter market. However, its primary listing is in France, where its shares have better liquidity, thus investors who have access to this exchange should trade it in its domestic listing rather than in the OTC market.

Klepierre’s major shareholder is Simon Property Group ( SPG ), the largest U.S. mall REIT, which has been a large shareholder in the company since its initial investment back in 2012, owning nowadays 22% of Klepierre’s capital.

At the end of 2022, Klepierre was present in 12 countries across Europe, had more than 70 shopping centers, and a portfolio value of about €19.8 billion. Geographically, its two most important markets are France (41% of total portfolio value) and Italy (21%), while other countries have smaller weights. Its main competitor is Unibail-Rodamco-Westfield ( UNBLF ), the largest shopping center operator in Europe, which I’ve covered previously .

Klepierre’s strategy is to own relatively large shopping centers in major urban areas, being a competitive advantage to smaller peers. Indeed, the shopping center business model is to a large extent based on size, given that large scale is an important factor to have pricing power in the industry, when negotiating lease tPTGGDDOM0008erms with large retailers. Moreover, generally speaking, scale also brings economies of scale in management costs, plus usually large companies have better access to external capital and at lower costs.

Regarding its retail mix, Klepierre’s shopping centers rent a good part of their footfall to fashion stores and supermarkets, which usually serve as anchoring stores. The rest is spread across different categories, as shown in the next graph.

Retail mix (Klepierre)

This retail mix is also important to maintain strong occupancy rates, as this type of stores require a physical presence (especially supermarkets), even though retailers increasingly want to have an ecosystem between their physical and online offerings. While e-commerce is a structural headwind for shopping centers, the recent experience with the pandemic show that people still prefer to shop physically, as retail sales recovered rapidly when lockdowns and restrictions were lifted.

Moreover, the penetration of ecommerce is lower in Europe than compared to the U.S., which is justified by cultural differences and the fact that European shopping centers have adapted better the retail mix and leisure offerings in their properties.

E-commerce (Klepierre)

This means that Klepierre’s long-term growth prospects aren’t impressive as shopping centers is a mature business in its current geographies, thus its growth is highly geared to overall economic growth and retail sales trends, plus some expansion or extensions projects the company may decide to pursue.

Indeed, Klepierre’s strategy in the past has been on a capital recycling strategy, which consists in selling underperforming assets and pursuing acquisitions in urban areas with better growth prospects. Moreover, it usually performs refurbishments and extensions of its existing assets, plus modernization works, to increase the appeal of its portfolio both to retailers and customers. Historically, Klepierre has sold about 150 assets since 2012, for total proceeds of around €8 billion, while it has invested an aggregate amount of billion, showing that it pursues an active portfolio management strategy to create value over the long term.

Financial Overview

Regarding its financial performance, its track record is mixed given that it reported positive operating momentum until 2019, but its business was naturally affected by the pandemic, which had a significant negative impact on its operating performance. More recently, its performance has recovered from bottom years in 2020-21, but still is at a lower level compared to 2019.

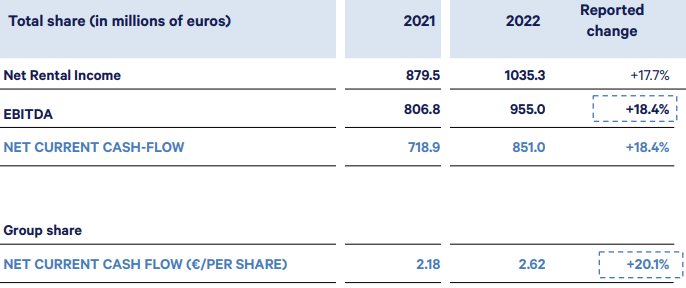

In 2022 , Klepierre’s net rental income was €1.035 billion, an increase of 17.7% from the previous year, but lower than its €1.13 billion reported in 2019. This increase in rental income was supported by much higher retailer sales during the past year (+25% YoY across the group), which also led to higher rent payments to Klepierre.

Reflecting an improved backdrop for retailers, Klepierre’s vacancy rate dropped to 4.2% in 2022, compared to a peak level of 5.8% reached in 2020. However, this is still higher than its 3% vacancy rate reported in 2019, showing that the pandemic led to more vacant space across its shopping centers, that hasn’t yet been rented again.

Regarding its profitability, Klepierre’s EBITDA amounted to €955 million in 2022 (+18% YoY), representing an EBITDA margin of 91.8% (vs. 93.2% in 2019), which is a very good level of profitability. This shows that Klepierre had a good cost control despite inflationary pressures in recent quarters and higher energy costs, which the company was able to pass to retailers to a large extent. Its cash flow per share was €2.62, up by more than 20% compared to 2021.

Key financial figures (Klepierre)

{kind=link}

While in the past few years the real estate sector benefited from low interest rates, this has changed markedly since mid-2022 when the European Central Bank started its current hiking pace. As I’ve analyzed in previous articles , this has negatively impacted real estate companies, and Klepierre has been no exception.

Like many companies in the sector, Klepierre’s strategy has shifted recently from growth to cash preservation, as the market started to worry about high debt levels across the sector. Due to this changing landscape, Klepierre performed several disposals over the past year to strengthen its balance sheet, resulting in gross proceeds of €602 million at valuations close to book value.

By taking a conservative approach in its balance sheet management, its loan-to-value (LTV) ratio has been below the sector’s average, given that its LTV ratio was 38% at the end of 2022. This compares quite well with Unibail (LTV of 45%), and the most indebted companies in the sector that have LTV ratios above 50%.

Its strong balance sheet, and good credit metrics, explain why Klepierre was able to maintain a dividend distribution during the past few years, while its peers have suspended dividend payments. Nevertheless, Klepierre cut its dividend by more than half related to 2020 earnings, which haven’t recovered yet to 2019 levels.

Indeed, its last annual dividend was €1.75 per share, an increase of 3% from the previous year, and still a lower level compared to 2019 (€2.20 per share). At its current share price, Klepierre offers a dividend yield of close to 8%, which is quite attractive for income investors.

Given that its cash flow per share guidance is to generate some €2.35 in 2023, its dividend is well covered by organic cash flow and seems to be sustainable, which means its high-dividend yield is not due to a high risk of a potential dividend cut. Indeed, according to analyst’s estimates, its dividend is expected to be around €1.70-1.80 over the next few years, showing that the market is not expecting a dividend cut in the medium term.

Regarding its valuation, Klepierre is currently trading at 9.4x FFO, in-line with its historical average over the past five years, which seems undemanding considering that Klepierre’s operating momentum is improving and some earnings growth is possible in the next couple of years.

Conclusion

The European real estate sector is currently out of favor among most investors, leading to some attractive yield and value propositions. Klepierre’s strong focus on Continental Europe is bearing fruits, while its closest peer Unibail is lagging due to its exposure to the U.S. and U.K., making it a better income investment than most peers due to a high-dividend yield that is sustainable.

For further details see:

Klepierre: A Rare Income Opportunity Among The European Real Estate Sector