KLPEF - Klepierre: Prime European Malls With A 7.2% Dividend Yield

Summary

- Cultural differences make European malls more resilient to the e-commerce thread compared to their US peers.

- Retailer sales have finally returned to pre-pandemic levels enabling the second biggest European mall REIT Klepierre to post solid 2022 results.

- The company grew its net rental income by 18% YoY, has a cost of debt of only 1.2% and trades at a 20% discount relative to adjusted net asset value.

- Check-out the article for a detailed breakdown of their NAV and why I think it's a good BUY.

Note: Klepierre can be found under two tickers - the native one traded in EUR in Paris ((LI)) and the OTC one traded in USD ( OTCPK:KLPEF ). Unless indicated otherwise all numbers are in EUR.

Dear readers/followers,

My first ever article ( linked here ) on Seeking Alpha focused on a European real estate company Vonovia (VONOY). This was no coincidence as I am based in Europe and have spent all of my professional career analyzing and developing European real estate. And although the majority of my investments are now concentrated in the US, I do have investments in Europe as well (around 10-15% of my portfolio). I like having exposure to both continents for the sake of diversification as well as the ability to rebalance based on current developments.

In this article I want to have a look at Europe's second-biggest publicly traded mall operator, a French-based REIT Klepierre ( OTCPK:KLPEF ). European REITs have taken a big hit last year due to increasing interest rates but have rebounded nicely since last October. The chart below compares the performance of KLPEF (in USD) to that of the Vanguard Real Estate index and Simon Property Group ( SPG ). Why SPG? Because it's one of the most similar peers and also a 22% shareholder of Klepierre. The correlation between the two is very apparent and actually Klepierre has outperformed SPG by 7% (though mainly due to a weakening dollar). Klepierre just reported their 2022 Earnings so let's examine them and see whether it makes a good addition to the portfolio.

Shopping Mall Culture: Europe vs USA

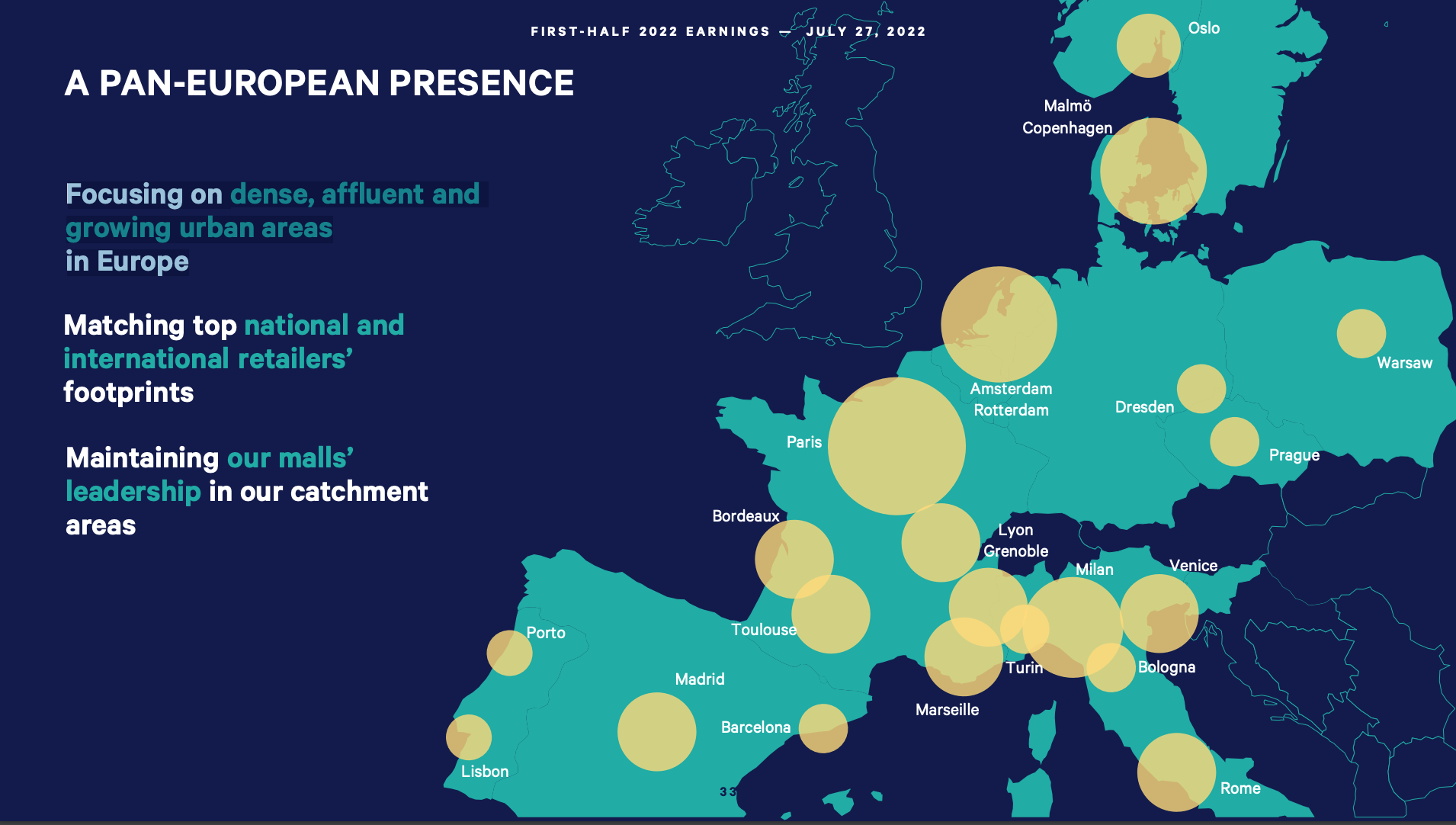

The company owns and operates over 100 premier shopping malls across Europe, focusing on dense, affluent and growing cities with a heavy focus on France, Netherlands, Italy and Denmark. Importantly the company focuses on the highest quality malls within each city and a lot of these are truly a work of art, with great architecture and a great location.

Having been to many malls in Europe and in the US myself, I can tell you that the shopping mall culture in Europe is very different (with the exception of large US cities such as NYC or LA). European shopping malls have become a destination and a place to show status. People don't go there to simply shop, they dress-up and go there to eat, drink, have fun and most importantly to be seen. This is crucial as it significantly reduces the risk that these high quality malls will become obsolete due to e-commerce. This is why I prefer having European malls in my portfolio as opposed to US malls.

The fact that European malls act as destinations rather than a convenience means that they are often larger and there are only a handful of them in each major city therefore creating higher barriers to entry - this is well illustrated by mall density. The US has the highest square footage of mall space per capita worldwide (22 sqf per person) while Western European countries only have 3-4 sqf of mall space per person. This is a major difference and reiterates that European malls are scarce assets that often occupy the best locations and with very few good locations left, these assets are likely to retain their value and make a good investment.

{kind=link}

Klepierre Investor Presentation

2022 Results

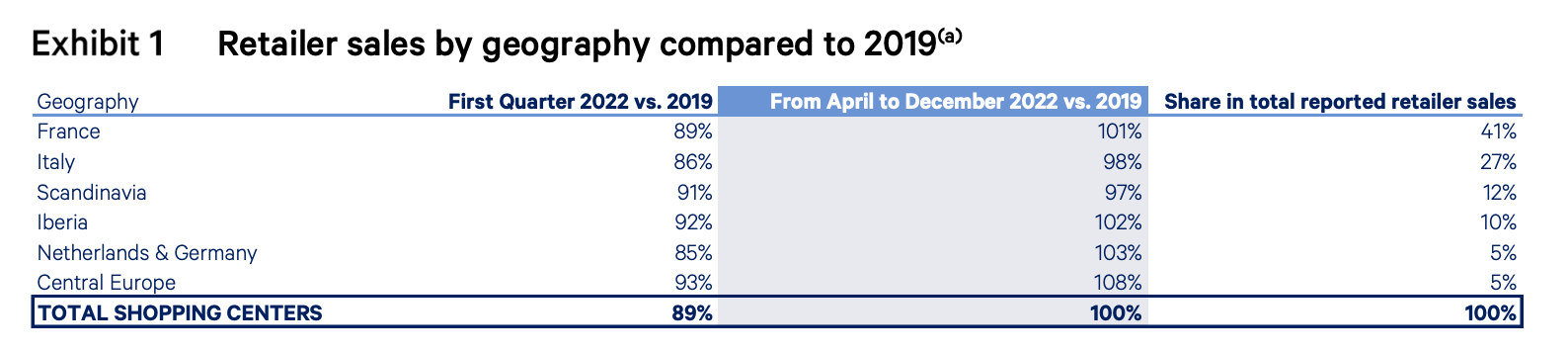

The company just reported their results for 2022 and they have been pretty good. Firstly, retailer sales have finally picked up and reached pre-pandemic levels in the last nine months of the year (April - December).

{kind=link}

Klepierre Q4 2022 Report

The company recorded a 17.7% YoY increase in net rental income (compared to 2021 which was frankly still affected by Covid shutdowns), primarily driven by over a 40% increase in France. Occupancy increased by 1.1% to a total of 95.8% and the company expects to achieve collection rate of 96.4% for the year. In short, it seems that things are almost back to business as normal and the company is doing well. In 2023, the Group expects to generate net current cash flow per share of EUR2.35, representing a growth of 5% compared to the adjusted figure for 2022 of EUR2.24.

The company has announced that the dividend for 2023 will be EUR1.75 per share . Given the current price of EUR24.20 this represents a dividend yield of 7.2%. This is above SPG's yield, but note that since the native stock is traded in Paris, foreign investors may be subject to French withholding tax.

Balance sheet

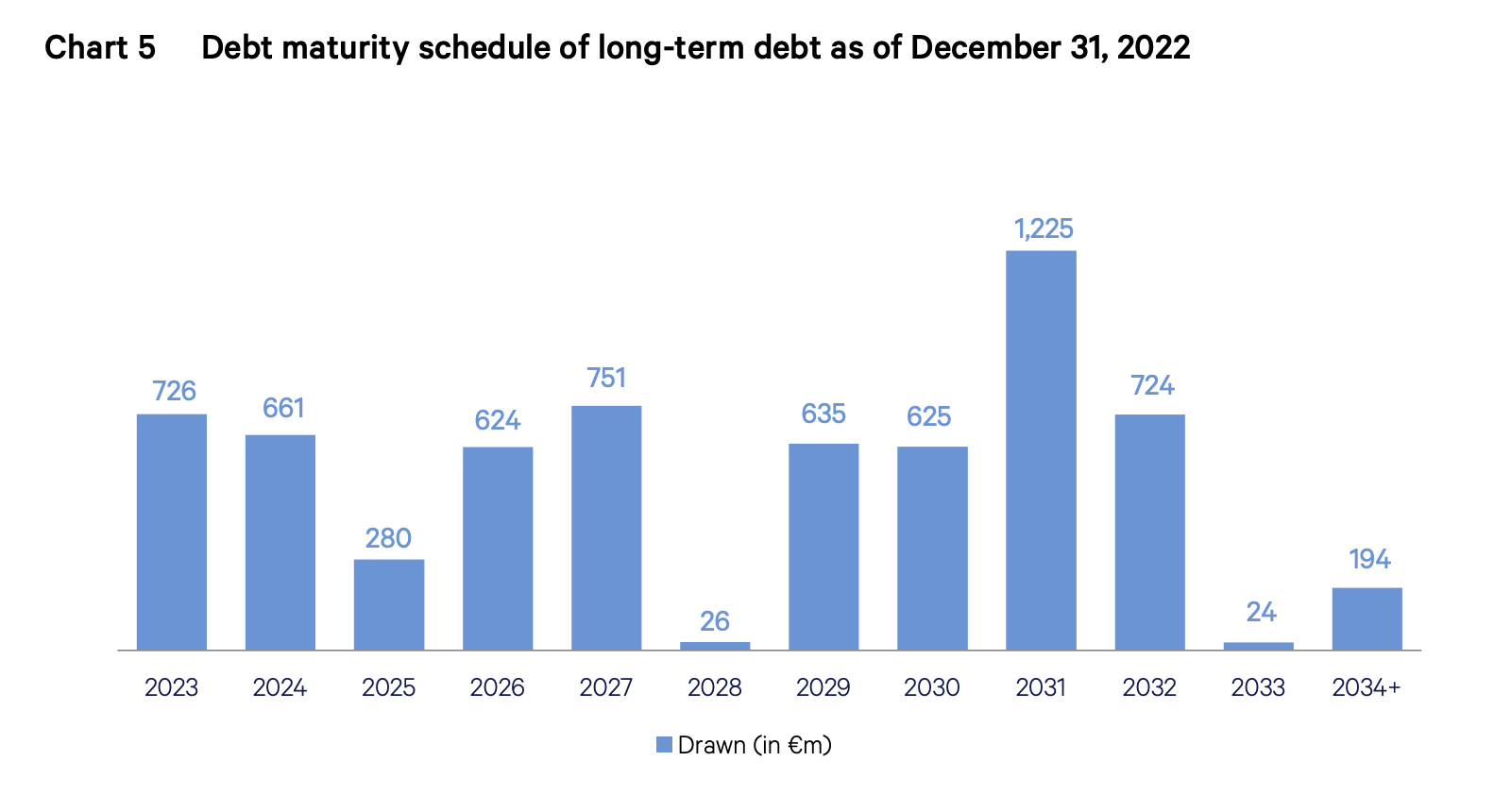

A quick overview of the balance sheet reviews that the debt of EUR7.5 Billion is spread over time, but there are significant maturities in 2023 and 2024 that the company will have to deal with. This will likely mean an increase in interest expense as the company refinances at a higher rate. Currently, 94% of the outstanding debt has fixed interest and thanks to the EUR exposure the company benefits from a very low overall cost of debt of just 1.2%.

When the company refinances its EUR1.4 Billion of debt due in 2023 and 2024, I expect that they will likely get an interest rate of about 5.0% (4.0% base rate + 100bps margin). This will translate into additional EUR53 Million in interest expense and will bring the overall average cost of debt to 1.8%. While a 50% increase is substantial, it is still substantially lower to what US peers are paying and even below treasury yields in Europe.

{kind=link}

Klepierre Q4 2022 Report

Valuation

In terms of multiples, Klepierre currently trades at a P/FFO multiple of 9.8x. This is below a historical average P/FFO multiple of 12x. This average encompasses the period from 2016 to 2022 and frankly a lot has changed during that time (rise of e-commerce, covid and an increase in interest rates). The average may be a point of reference, but I wouldn't rely on it too much. Compared to SPG's multiple of 10.5x, Klepierre stock is trading a slight discount.

{kind=link}

Fast graphs

The best way to value a real estate business in my opinion is to look at the company's NAV, make sure that the implied cap rates used to calculate fair value on the books are in line with the market and compare the NAV with the price we are paying for it.

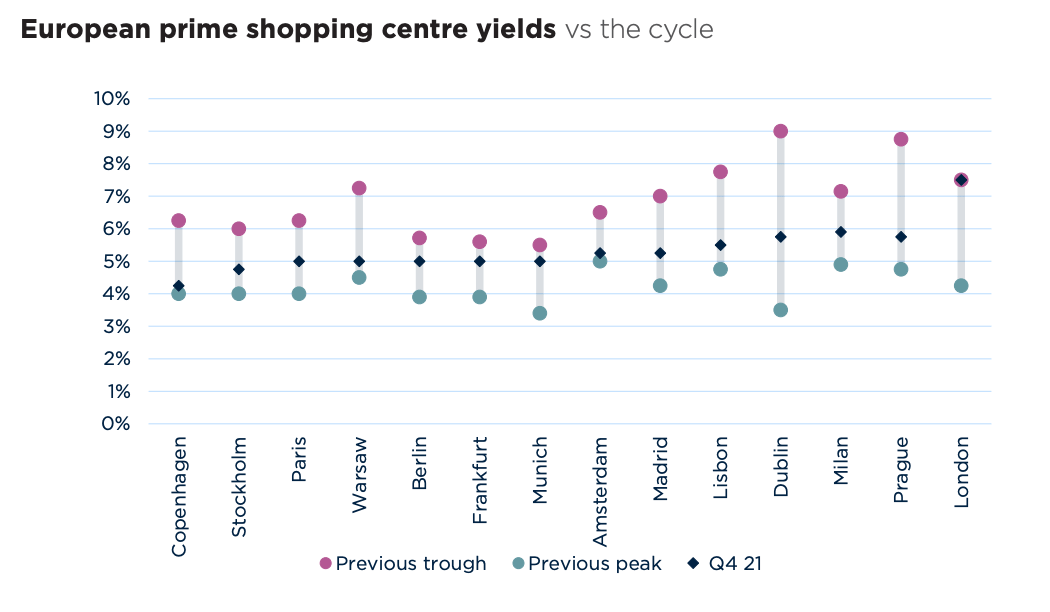

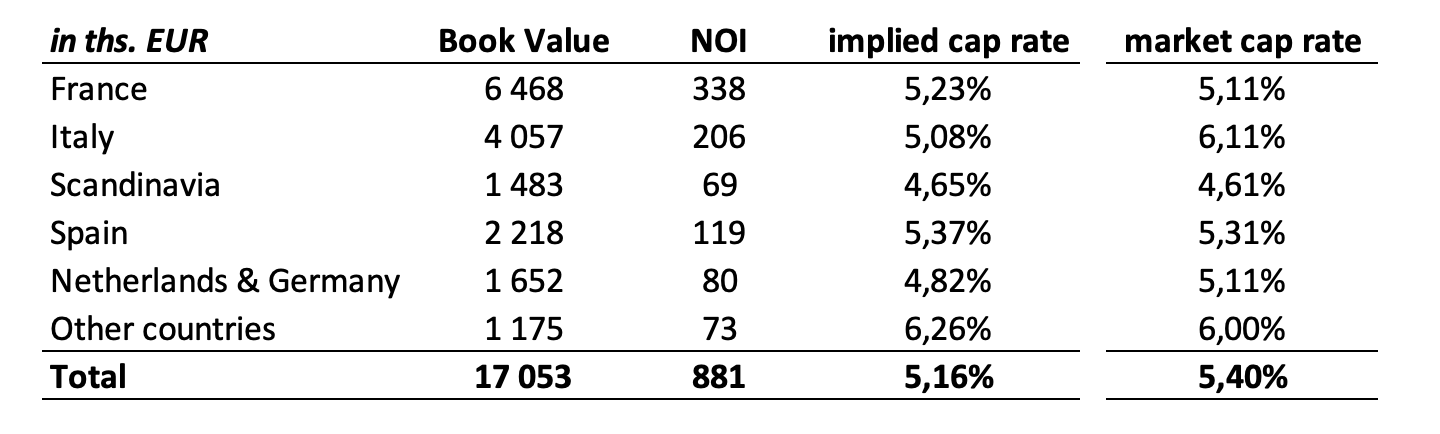

On a group level Klepierre keeps their properties on the books at EUR17.0 Billion. Throughout 2022 these properties have generated a net rental income of EUR0.88 Billion. This means an implied cap rate of 5.16%. To see if this is actually in line with the market let's have a look at market cap rates below.

{kind=link}

Savills research

Note: 2022 numbers are not yet published, so for the sake of the calculation I will use the numbers from Q4 2021 ( chart above ) and add an 11bps premium based on what Savills said in Q3 2022 regarding their expectations for 2022.

The retail sector is about to face another storm, with the European purchasing power about to decline. Hence, prime shopping centres' yield decompression is continuing. By the end of the year, we expect the average prime SC yields will move up by 11 bps yoy.

Looking at Klepierre's book value region by region and comparing the implied cap rates to the market rates, the portfolio actually seems priced quite fairly, only 20bps below the market level (5.16% vs 5.40%).

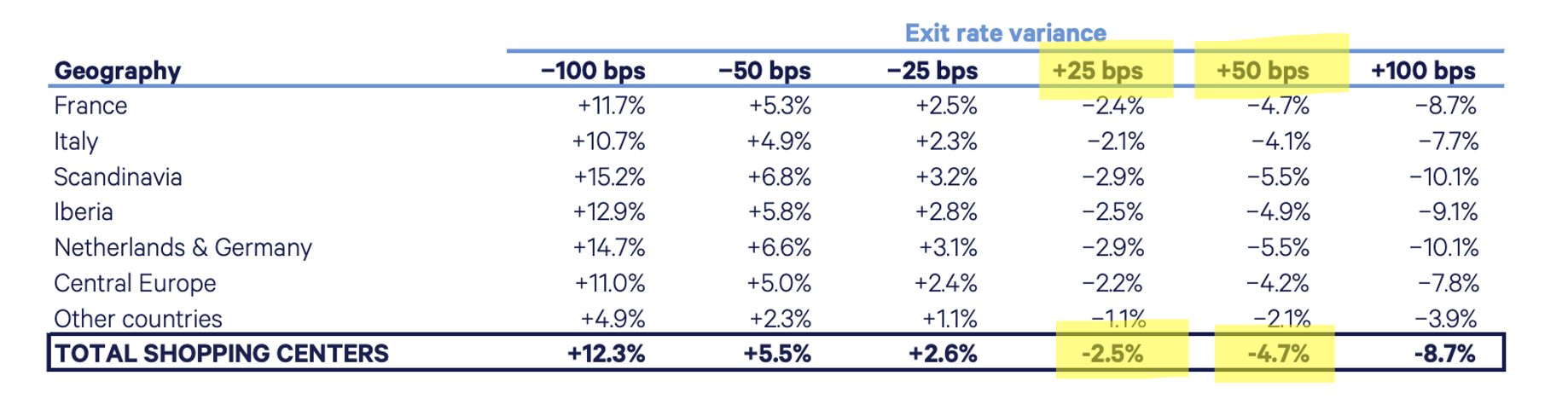

{kind=link}

Created by Author based on data from Klepierre

Klepierre provides the following sensitivity analysis of their book values to cap rates. Since their rate is a bit below what Savills estimated as fair and I want to be conservative in my analysis, I am going to assume an increase of 50bps in the cap rate across all of their properties (overall cap rate increase to 5.16% + 0.5% = 5.65%). This will translate into a 4.7% decrease in the fair value of assets to EUR16.2 Billion.

{kind=link}

Klepierre Q4 2022 Report

With net debt of EUR7.5 Billion, we get NAV of EUR8.7 Billion. With 287 Million shares outstanding, this means NAV of EUR30.30 per share. Currently the share is trading at EUR24.20 implying a 20% discount to net asset value (using a conservative asset value with a 50bps higher cap rate).

Takeaway

The company has been through a lot over the past few years but with retailer sales reaching pre-pandemic levels again, the company reported really good results for 2022, growing their net rental income by 18% YoY and improving their occupancy to almost 96%. The balance sheet is in a good shape as the company enjoys a very low average cost of debt of just 1.2%. And while it will likely increase to about 1.8% as the company refinances its debt due in 2023 and 2024, it will remain significantly below yields on government bonds denominated in EURs as well as US peers. In terms of valuation, the stock still trades about 20% below its fair net asset value, even when conservative cap rates are assumed.

Overall I think Klepierre is worth buying and I rate it as a " BUY " here at EUR 24.20. The next few years might be a little bumpy, especially if Europe slips into a recession and people stop spending money, but with over a 7% dividend yield (now confirmed for 2023) I think it's worth it.

For further details see:

Klepierre: Prime European Malls With A 7.2% Dividend Yield