AMLP - KMF: Expensive Way To Access Infrastructure Assets

Summary

- The KMF fund is marketed as a 'NextGen' energy infrastructure fund.

- However, only 18% of the fund is in 'renewable infrastructure' while the vast majority of the fund's assets are invested in energy midstream and natural gas infrastructure assets.

- Investors can get better returns and comparable distributions from cheaper energy infrastructure ETFs.

The Kayne Anderson NextGen Energy & Infrastructure, Inc. (KMF) is a closed-end fund that markets itself as a 'NextGen' energy infrastructure fund. However, its holdings are mostly energy midstream and natural gas & LNG infrastructure assets. I believe investors can get similar exposures and better returns via the much cheaper ETFs.

Fund Overview

The Kayne Anderson NextGen Energy & Infrastructure, Inc. is a closed-end fund ("CEF") that aims to provide total returns with an emphasis on cash distributions. The KMF fund has $436 million in net assets.

Strategy

The KMF fund markets itself as focusing on 'NextGen' energy and infrastructure companies that are meaningfully participating in, or benefiting from, the energy transition.

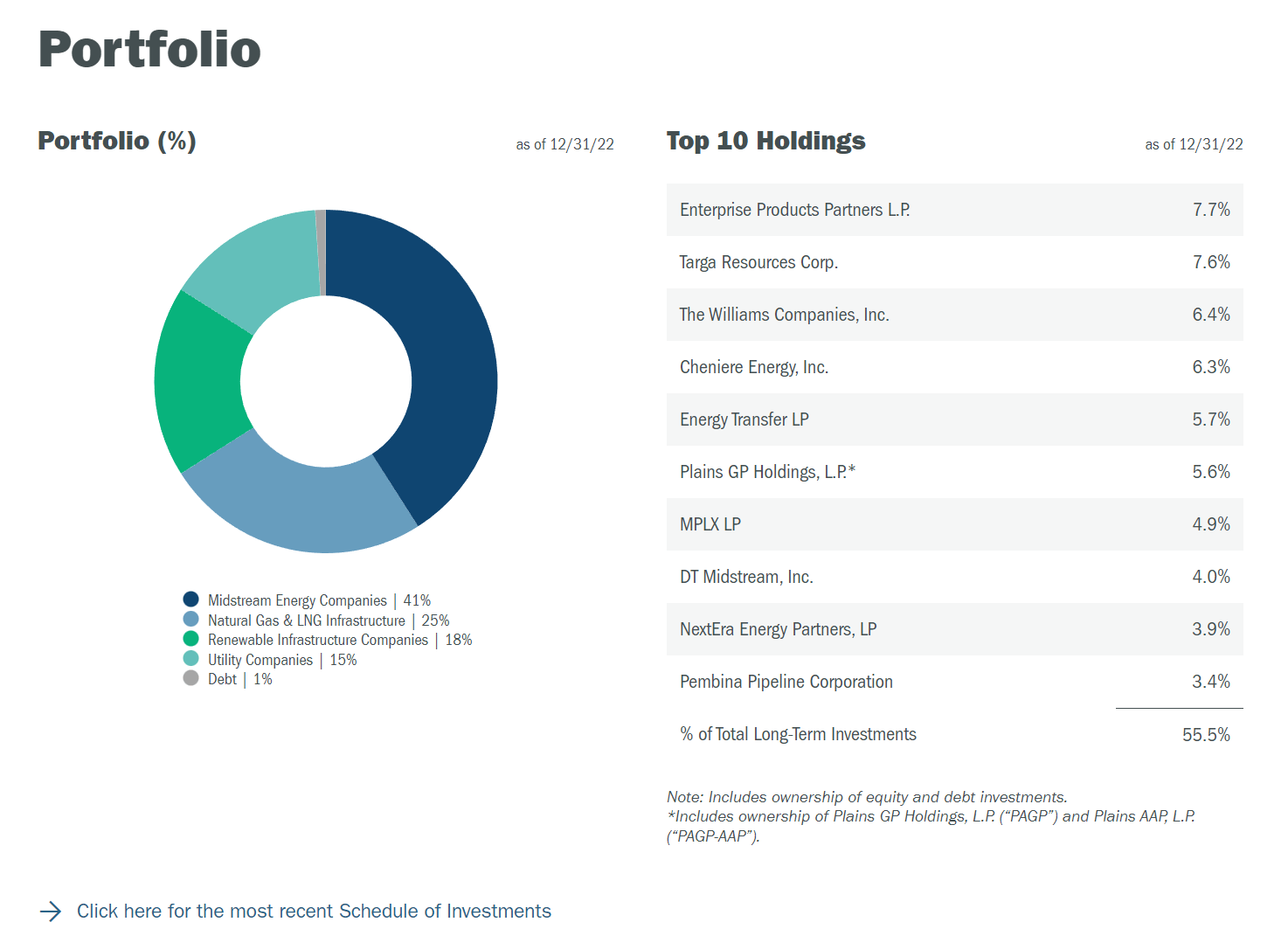

Portfolio Holdings

Figure 1 shows KMF's sector allocation and top 10 holdings. The fund has 41% of assets invested in midstream companies, 25% in natural gas & LNG infrastructure, and 15% in utilities. Despite having 'NextGen' in its name, the fund's energy transition exposure appears to be a relatively paltry 18% weight in renewable infrastructure.

The fund's top 10 holdings comprise 55.5% of assets and are dominated by energy midstream companies like Enterprise Products Partners L.P. ( EPD ).

Figure 1 - KMF sector weights and top 10 holdings (kaynefunds.com)

{kind=link}

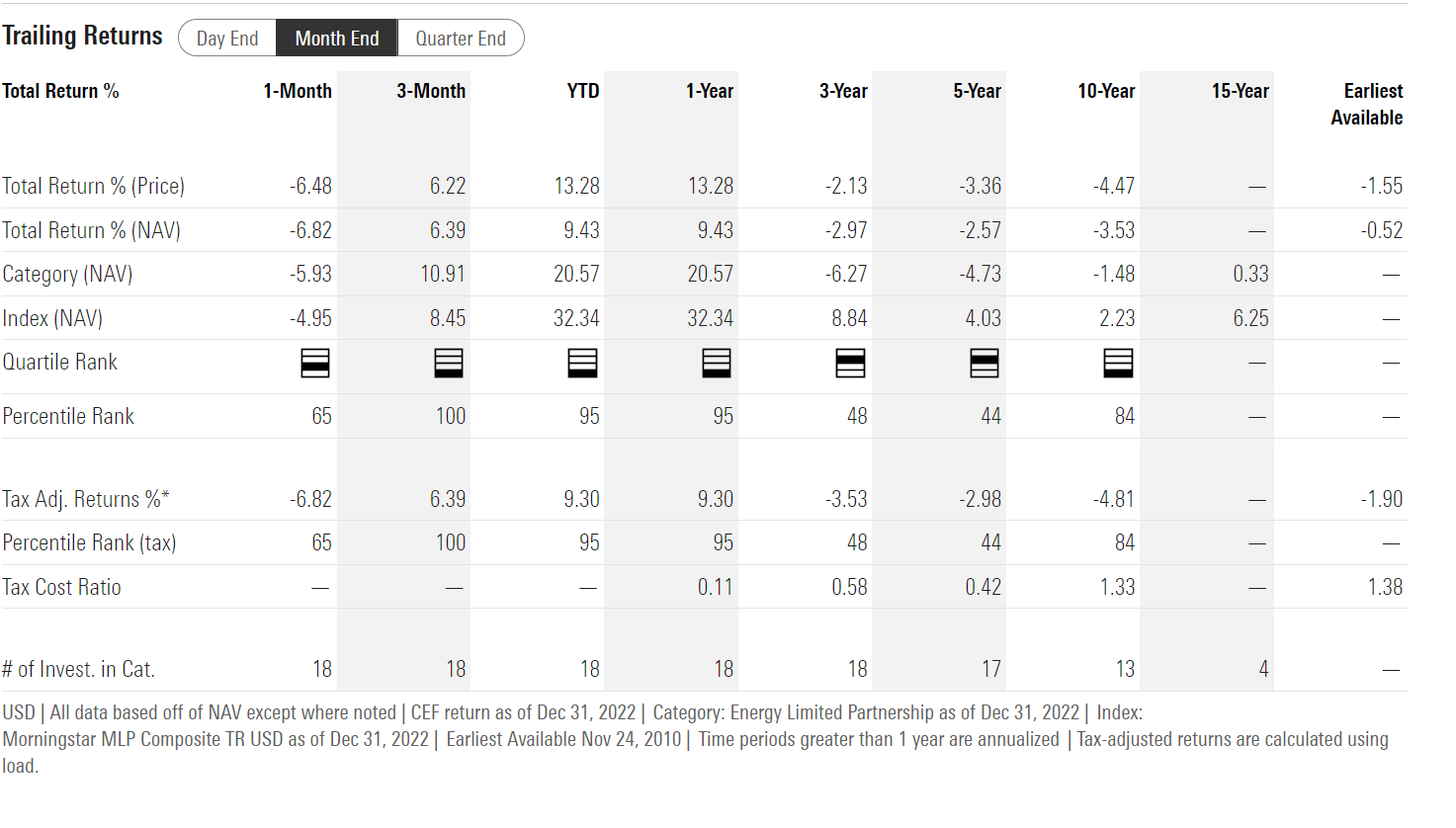

Returns

KMF's returns were strong in 2022, returning 9.4% when the S&P 500 suffered an 18% drawdown. However, longer term historical returns for KMF have been poor, with 3, 5, and 10Yr average annual total returns of -3.0%, -2.6% and -3.5% respectively to December 31, 2022 (Figure 2).

{kind=link}

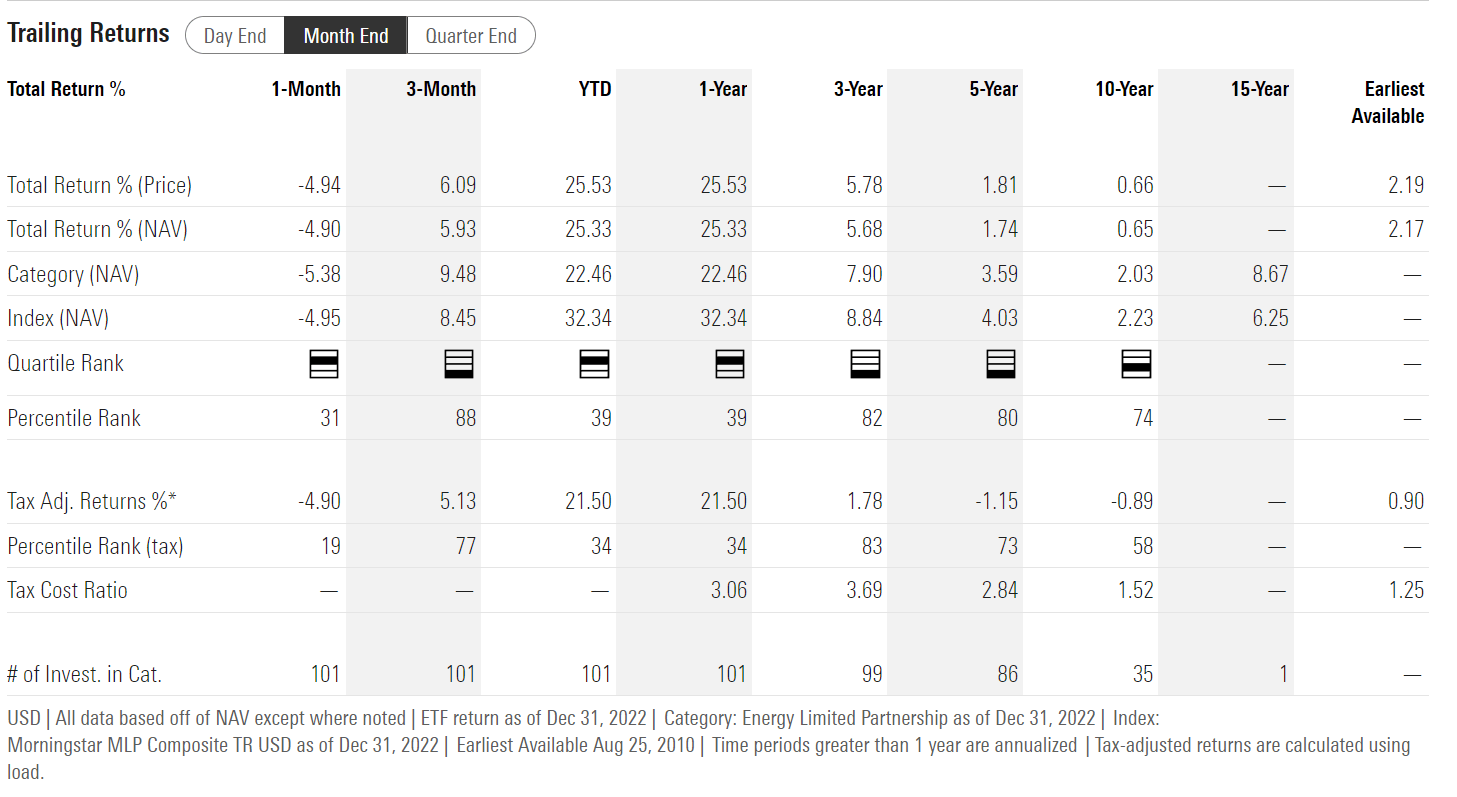

Furthermore, if we compare the KMF to the ALPS Alerian MLP ETF ( AMLP ), a passive ETF of energy infrastructure companies, we can see that KMF has lagged far behind AMLP in terms of historical performance on all timeframes (Figure 3). AMLP has 1/3/5/10yr average annual total returns of 25.3%/5.7%/1.7%/0.7% to December 31, 2022.

{kind=link}

Distributions & Yield

The KMF fund pays a high distribution rate of $0.16 per quarter, or an annualized 8.2% distribution yield.

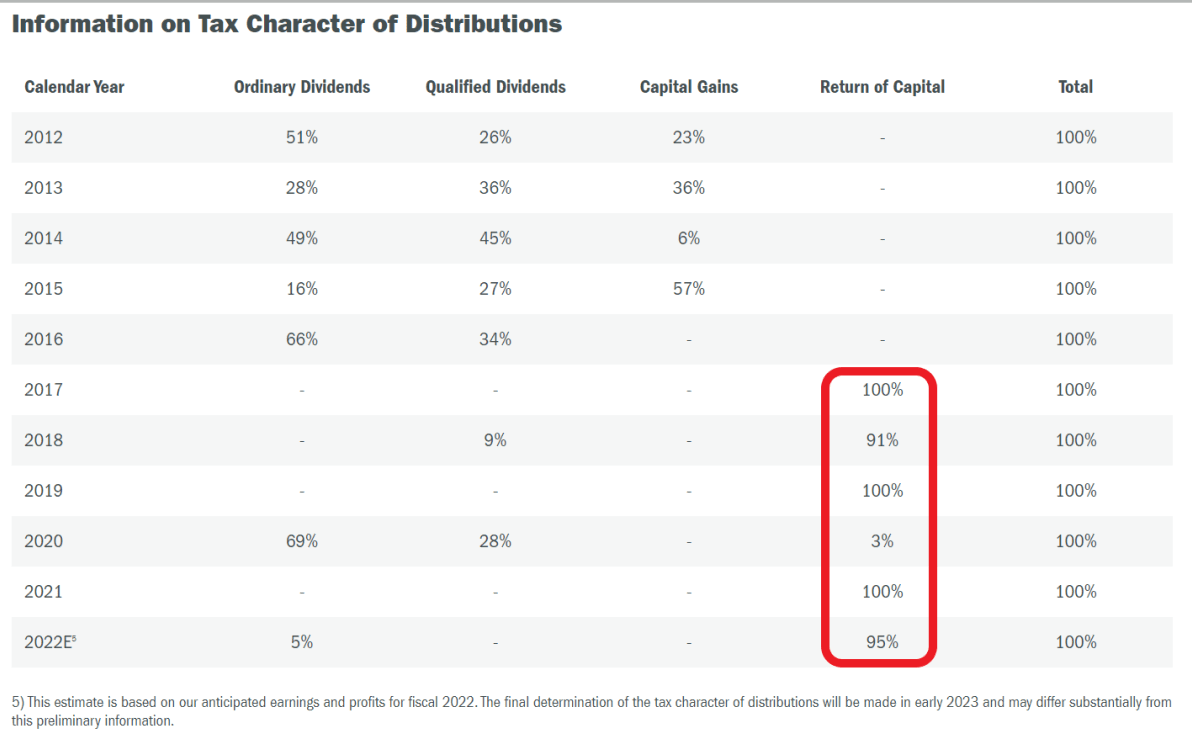

However, investors should note that according to the fund's website, the vast majority of the fund's distribution has been funded by Return of Capital ("ROC") in the past few years (Figure 4).

{kind=link}

This is puzzling, as many energy midstream companies pay large dividends. For example, EPD, the KMF fund's largest holding, pays a 7.6% dividend yield . Dividends received should count towards the fund's net investment income ("NII").

It is unclear why 95% of the fund's distribution for 2022 is estimated to come from ROC. Investors should consult a tax professional to clarify the tax status of KMF's distributions.

ROC Not Necessarily A Bad Thing

Investors should also note that ROC is not necessarily a bad thing, as long as a fund earns its distributions, it should not matter whether the distribution is funded through capital or income.

In my opinion, the best yardstick to measure if a fund has earned its distributions is compare the fund's long-term historical returns to its distribution rate. Using this metric, KMF's historical returns are negative on a 3, 5, and 10Yr basis, so it has not 'earned' its distribution.

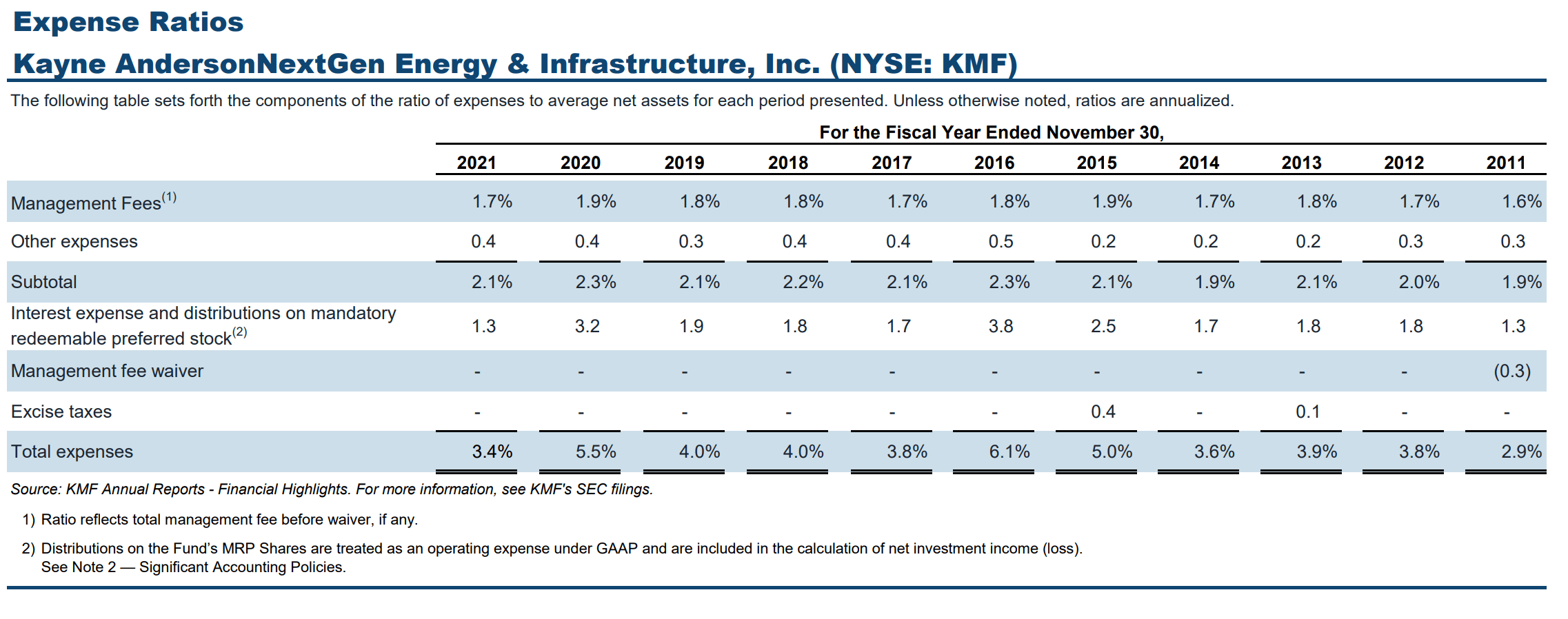

Fees

The KMF fund is a very expensive fund, charging a 1.7% management fee in fiscal 2021. Combined with leverage and other expenses, KMF's total expense ratio came out to 3.4% (Figure 5).

Figure 5 - KMF charged a 3.4% expense ratio in 2021 (kaynefunds.com)

{kind=link}

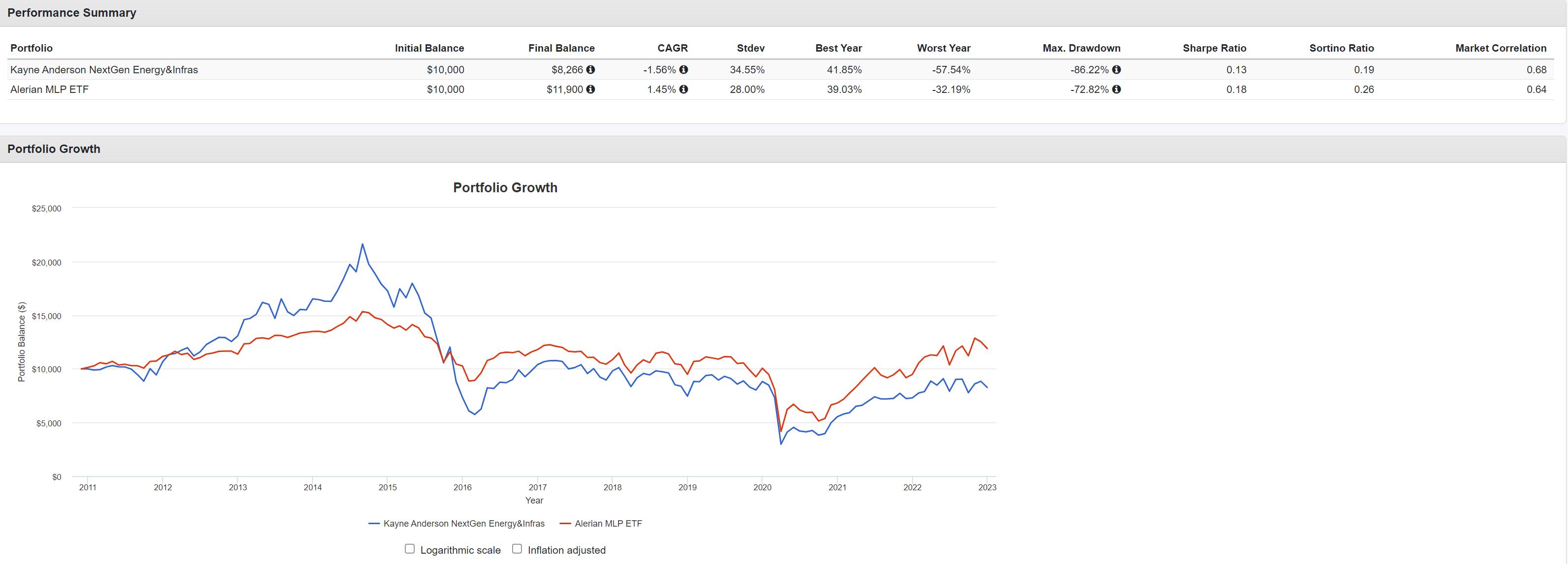

KMF Vs. AMLP

With a 3.4% total expense ratio, KMF appears to be an expensive way to access energy infrastructure assets. A good alternative may be the AMLP ETF that I mentioned above. Not only does it outperform the KMF fund in historical returns, it also pays a comparable 7.3% trailing distribution yield and only charges a 0.85% expense ratio.

Figure 6 shows a comparison of KMF vs. AMLP using Portfolio Visualizer and the period December 2010 to December 2022. AMLP has higher returns CAGR of 1.5% vs. -1.6% for KMF. AMLP also has lower volatility of 28.0% vs. 34.6%.

Figure 6 - KMF vs. AMLP (Author created using Portfolio Visualizer)

{kind=link}

Conclusion

The KMF markets itself as a 'NextGen' energy infrastructure fund. However, its holdings are mostly energy midstream and natural gas & LNG infrastructure assets. I believe investors can get similar exposures and better returns via the much cheaper AMLP ETF.

For further details see:

KMF: Expensive Way To Access Infrastructure Assets