KMF - KMF: Vote With Your Feet; Tender For Cash

2023-05-20 03:35:41 ET

Summary

- The KMF fund is marketed as a 'NextGen' energy infrastructure fund.

- However, management is now proposing a merger into a 'vanilla' energy infrastructure fund.

- Investors on the sidelines should stay away. But current unitholders can vote 'Yes' but elect to receive cash, to preserve their optionality.

A few months ago, I wrote a cautious article on Kayne Anderson NextGen Energy & Infrastructure, Inc. ( KMF ). My main issue was that while the KMF fund markets itself as a 'NextGen' energy infrastructure fund, its holdings are mostly energy midstream and natural gas & LNG infrastructure assets. I believe investors can get similar exposures and better returns via the much cheaper ETFs.

Since my article, things have not gone well for the KMF fund, with the fund returning -6.7% in total returns, lagging the S&P 500 by 10% (Figure 1).

Figure 1 - KMF has underperformed the market (Seeking Alpha)

In fact, before a recent bounce due to a proposed merger with the Kayne Anderson Energy Infrastructure Fund ( KYN ), the KMF fund was down by over 15%. With a proposed merger in hand, I want to take this opportunity to update my thoughts on the KMF fund.

Management Claims KMF Is Not Just An Infrastructure Fund...

One of the biggest pushback I got from my initial article was from management, who complained that I misrepresented their view of what is considered 'NextGen'. In management's view, 'NextGen' infrastructure "includes Natural Gas & LNG Infrastructure and Utility Companies that are meaningfully participating in, or benefiting from, the Energy Transition." Overall, KMF management believes 58% of the fund's portfolio was concentrated in 'NextGen' companies as of November 30, 2022.

I bring up this anecdote because I find it curious that four months after my article, when management was adamant the KMF fund is differentiated because of its 'NextGen' infrastructure assets, they, and the board of directors, decide to merge the 'NextGen' KMF fund into the 'vanilla' KYN fund.

...But Elect To Merge It Into An Infrastructure Fund

The merger between KYN and KMF is billed as a NAV-for-NAV merger that will ' position the resulting fund for the future to capitalize on long-term tailwinds in the energy infrastructure sector' . KMF unitholders will be issued KYN shares, and the merger is expected to qualify as a tax-free reorganization.

To entice KMF unitholders to vote for the merger, management initially proposed that KMF conduct a tender offer for 15% of outstanding shares after the closing of the merger and the manager will implement new management fee waivers for KYN.

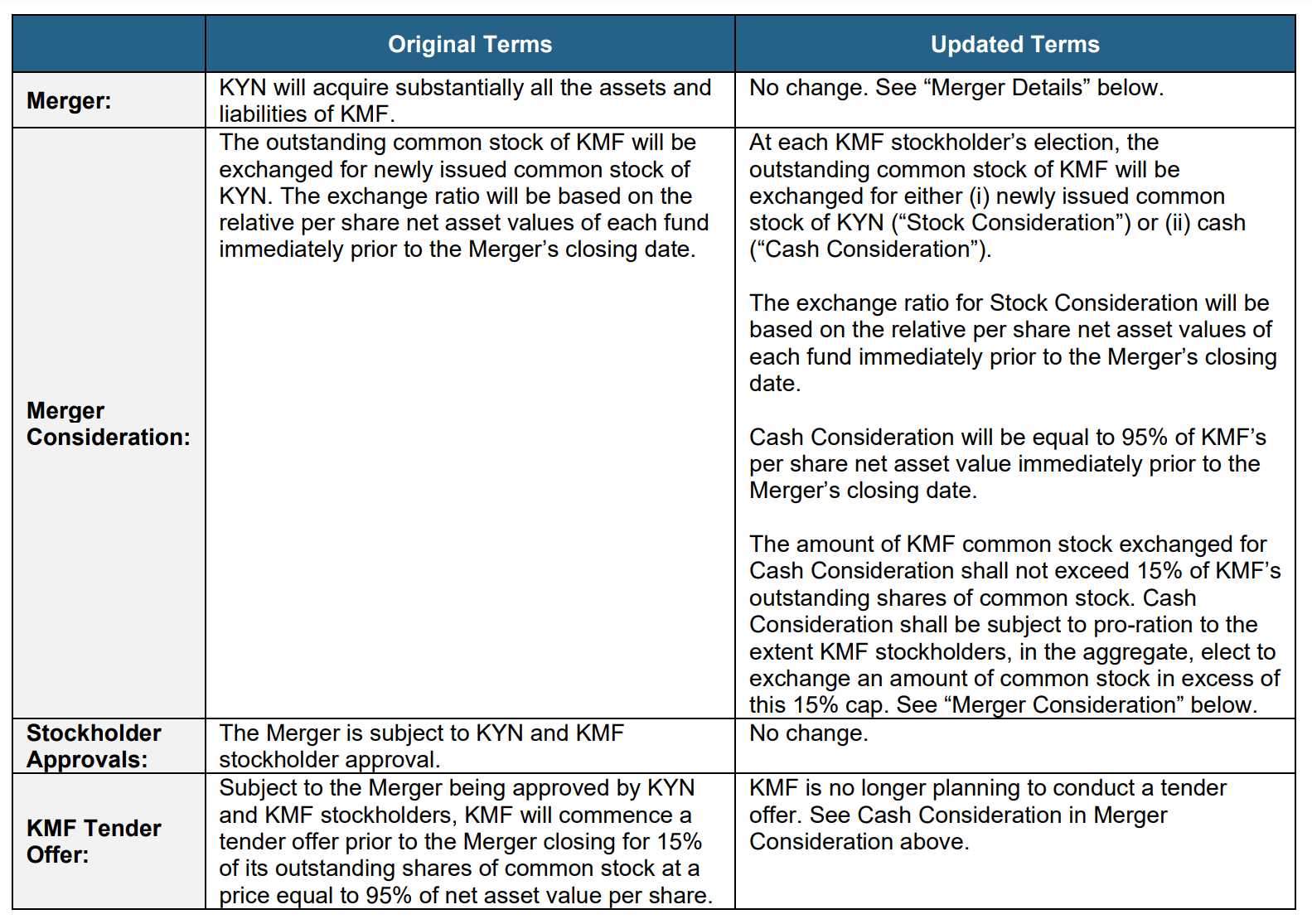

However, on April 24th, 2023, management proposed updated terms for the merger, which replaces the tender offer with the ability for KMF unitholders to receive cash consideration for 95% of NAV in lieu of KYN units (Figure 2).

Figure 2 - Updated merger terms (kaynefunds.com)

{kind=link}

In my opinion, this is a slightly better deal, as the original tender offer is contingent on the merger being approved and may involve additional time delay and NAV uncertainty whereas in the updated deal, unitholders who wish to exit can do so immediately prior to the merger.

Furthermore, management is also recommending an additional 1 cent per share increase in KYN's distribution (to 22 cents per share) following the merger. The merger is expected to be voted on at a shareholder meeting to take place on June 20, 2023 with a record date of March 27, 2023 .

Additional Fee Waivers Does Not Address Another One Of My Concerns

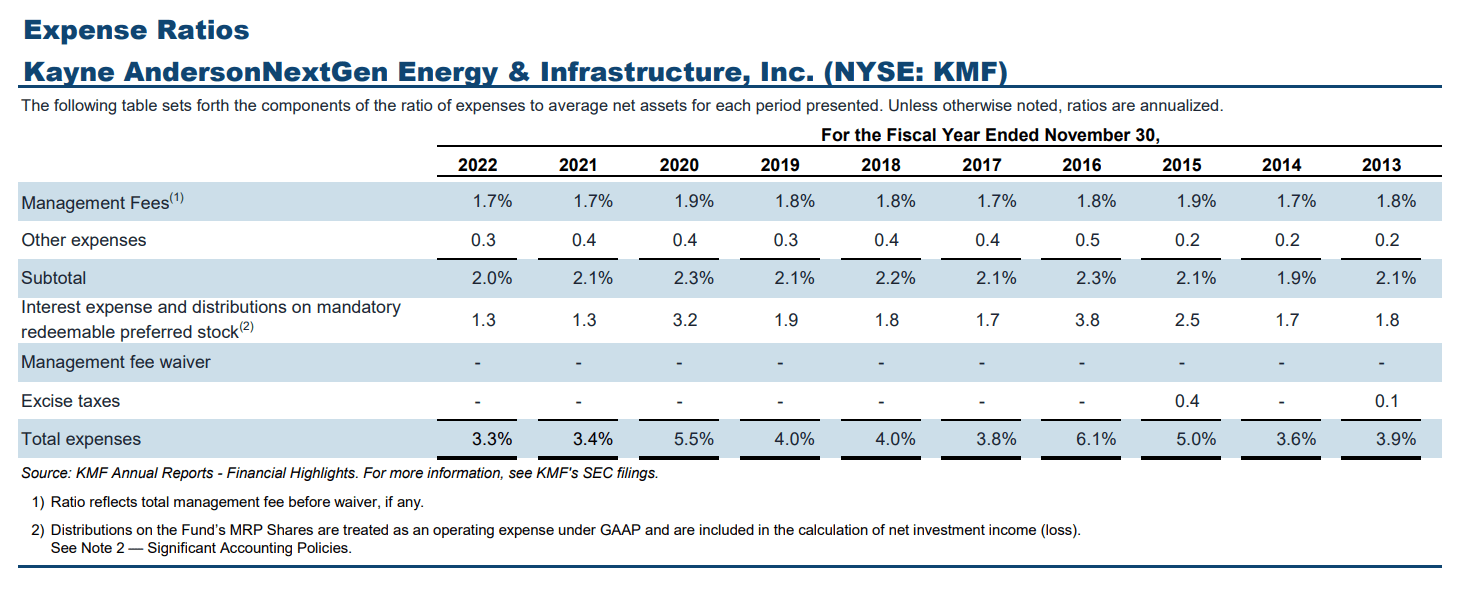

Another of my criticism of the KMF fund was its fee structure, which came out to a total expense ratio of 3.3% in fiscal 2022, expensive compared to passive ETFs (Figure 3).

Figure 3 - KMF fee structure (kaynefunds.com)

{kind=link}

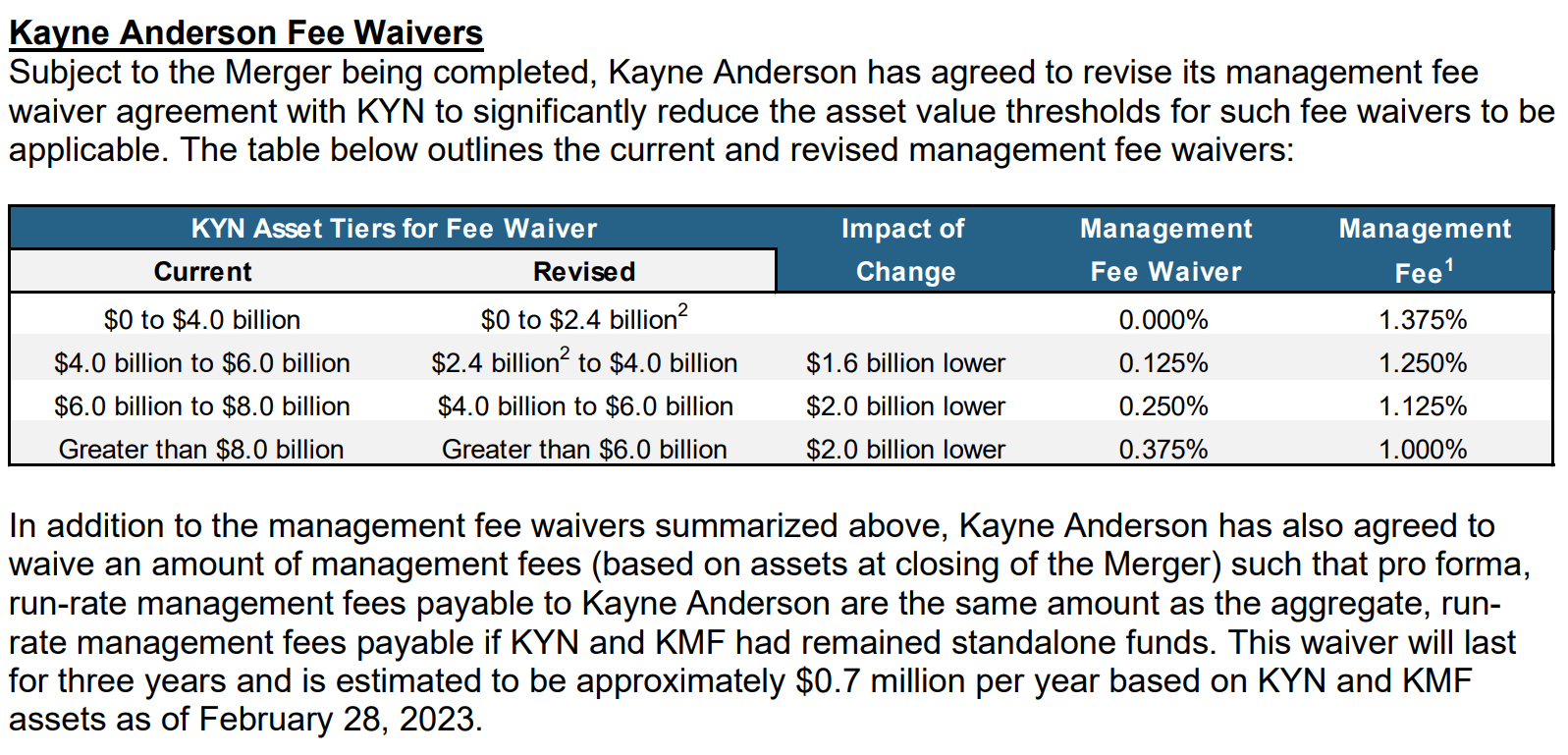

As part of the proposed merger agreement, the manager has agreed to revise the management fee waiver agreement to reduce the asset threshold where fee waivers will apply. At first glance, reduction in fees is a good thing for unitholders, who doesn't like lower fees (Figure 3)?

Figure 3 - Revised fee waiver agreement (kaynefunds.com)

{kind=link}

However, upon closer inspection, there is less than meets the eye. Currently, the KMF fund has $540 million in total assets while the KYN fund has $1.9 billion in total assets for a combined $2.4 billion. The merger agreement is struck such that the first tier threshold will be the combined total assets of the two funds at the time of merger. So a fee waiver will only apply if the fund gains assets (through price appreciation or inflows) after the merger.

If performance continues to be poor and/or the fund sees outflows (fund mergers usually trigger a bout of asset churn), there will be no impact to management fees.

Could Activist Investor Be The Reason For The Proposed Merger?

Another interesting angle we have not yet discussed is the possibility of alternative motives for the fund merger between KYN and KMF.

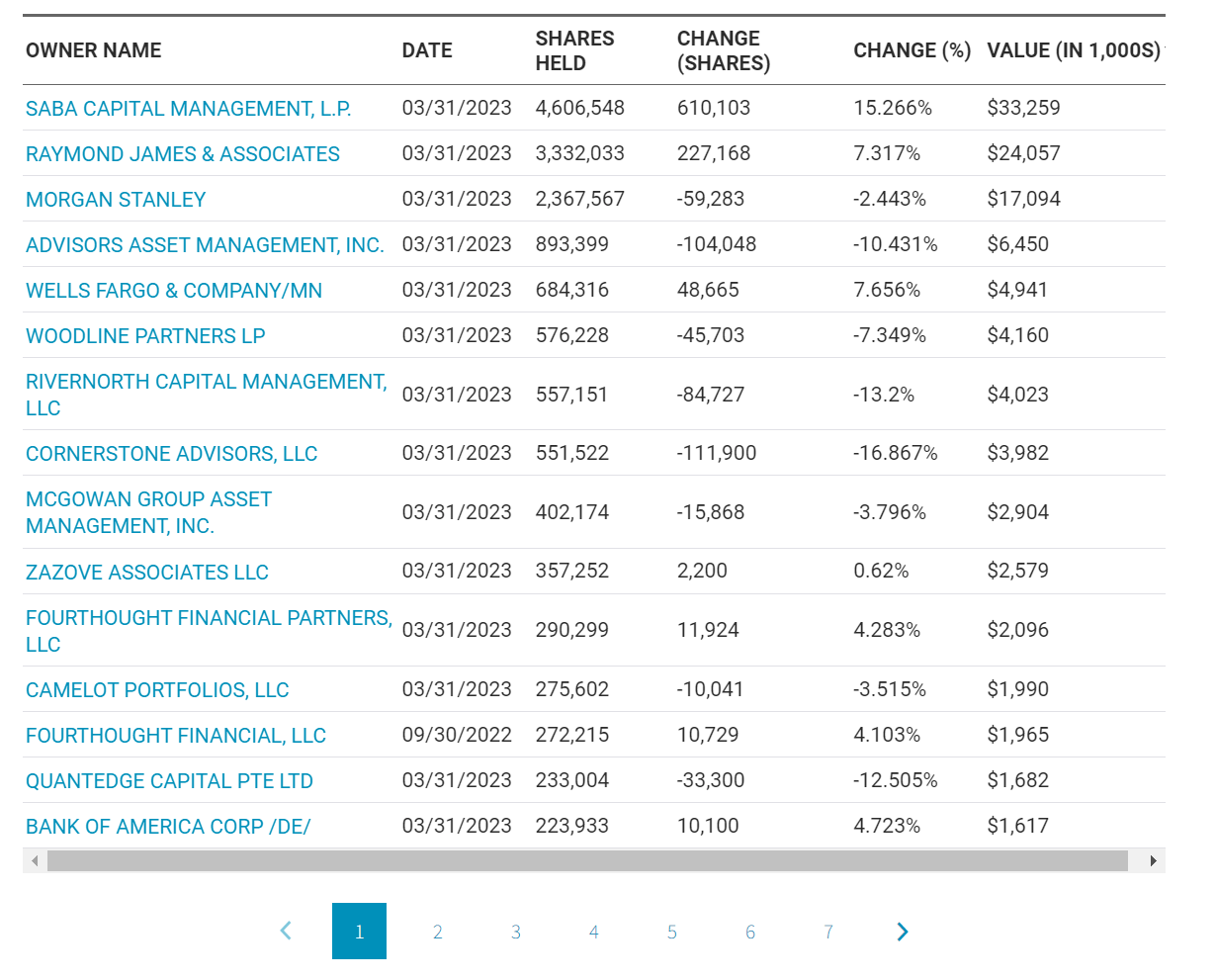

According to data from the Nasdaq , Saba Capital Management currently holds a 15.3% stake in the MF fund that has grown in the past few months (Figure 4).

Figure 4 - KMF institutional shareholders (nasdaq.com)

{kind=link}

As a bit of background, Saba Capital Management is an investment advisor / hedge fund manager led by Boaz Weinstein, one of the most prominent hedge fund managers in recent history. Saba Capital is known for its acumen in credit markets and leading activist campaigns against underperforming closed-end funds ("CEF") like the Saba Capital Income & Opportunities Fund ( BRW ) that Saba took over from Voya in 2021, and the Templeton Global Income Fund ( GIM ) that Saba is in the process of ousting management.

According to SEC filings, Saba first announced a position in the KMF fund in late October , with an announced stake of 3.4 million shares. However, by March 31, 2023, Saba has increased its stake to 4.6 million shares or 9.8%.

Perhaps the proposed fund merger is not to 'position the fund for the future' but a defensive strategy by entrenched management to protect its lucrative management contract with the KMF fund, since Saba's stake in a combined KYN/KMF fund may be greatly diluted and it would be more difficult for Saba to effect change in management and/or strategy. However, this is purely speculation on my part.

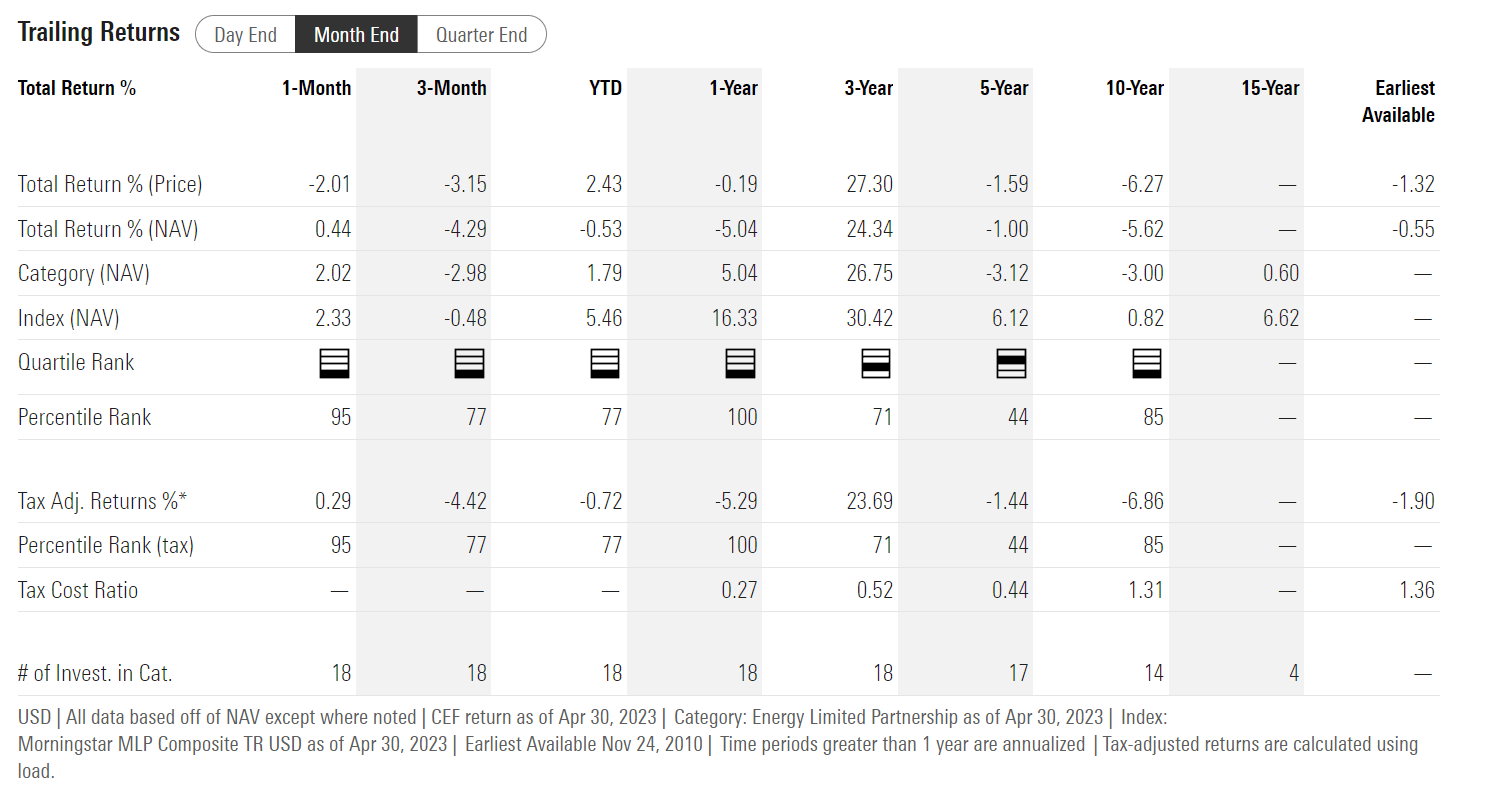

KMF Fund Continues To Lag

While management has been distracted by the activist investor, it appears the KMF fund has continued to perform poorly, returning -4.3% and -5.0% in the past 3 months and 1 year (Figure 5). Overall, the KMF fund has continued to deliver poor performance, with 3rd and 4th quartile returns on most time frames against the Energy Limited Partnership category in Morningstar.

Figure 5 - KMF continues to deliver poor performance (morningstar.com)

{kind=link}

It is no coincidence that KMF's poor performance has attracted the attention of activist investors like Saba who is looking to replace management.

Should Unitholders Vote Yes?

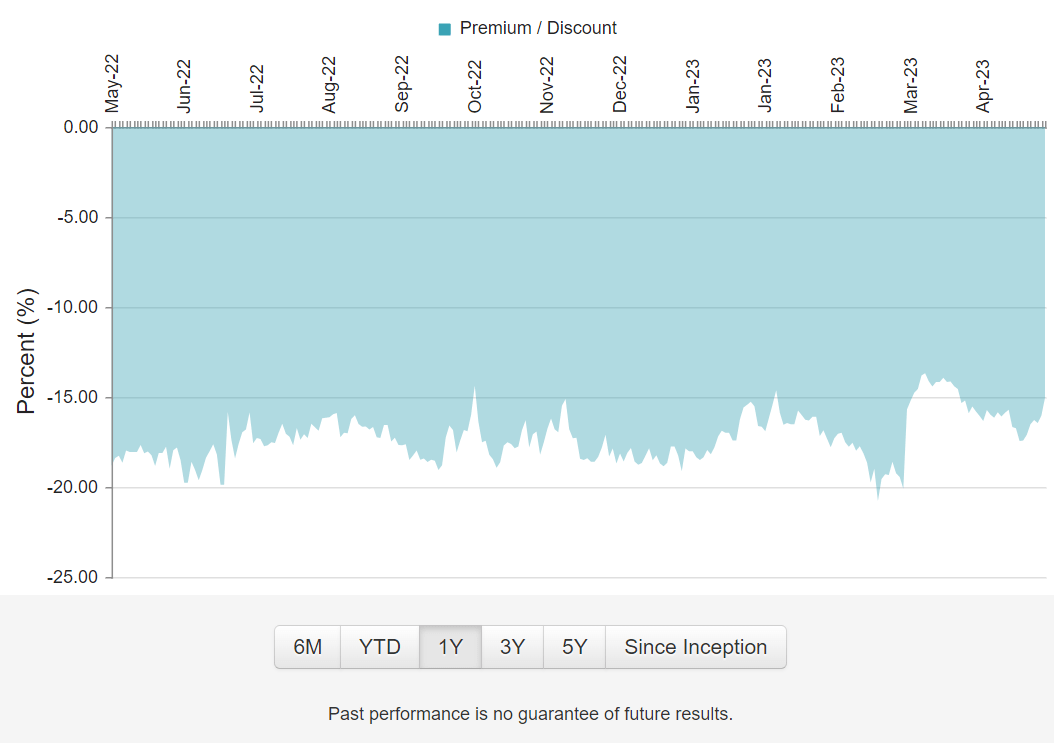

For investors currently invested in the KMF fund, I believe the upcoming merger proposal could be an interesting inflection point. Currently, the KMF fund is trading at a 15% discount to its NAV.

Figure 6 - KMF trades at a steep discount (cefconnect.com)

{kind=link}

So if KMF unitholders vote 'Yes', but opt to receive the cash option, they could see an immediate ~12% return (from 85% to 95%) on their units. However, if too many unitholders vote 'Yes' but choose to receive cash, they could be issued proportionate shares of KYN instead. They will then have to assess whether KYN would be a good long-term investment.

On the other hand, if KMF unitholders vote 'No', there is no guarantee that management can turn around performance of the KMF fund as an independent entity. Furthermore, they may continue to get distracted with an ongoing proxy battle with Saba.

Overall, I think the best course of action is to vote 'Yes' but choose to receive cash, as it preserves optionality for unitholders. If they get cash, then it would be a quick way to surface value. f they get issued proportionate KYN shares instead, there is always the option to sell their KYN shares as soon as the deal completes. Finally, if the deal falls apart, they will just be at the same place as voting 'No'.

Conclusion

At the end of the day, what should investors do with the KMF fund? For investors on the sidelines, I would continue to advise they look elsewhere for their energy infrastructure exposure. There really isn't much to get excited about here.

For current unitholders, I recommend they tender but elect to receive cash, as it maximizes their optionality.

For further details see:

KMF: Vote With Your Feet; Tender For Cash