E - KNOT Offshore Partners: No Distribution Increase Anytime Soon - Hold

2023-12-14 17:32:45 ET

Summary

- KNOT Offshore Partners LP reported stable Q3 results, but profitability and cash generation remain impacted by special survey requirements, higher interest rates, and ongoing weakness in the North Sea market.

- After signing additional contracts for a number of vessels, 2024 charter coverage now stands at 70%.

- However, the company has failed to secure follow-on work for two MR-size shuttle tankers, which consequently will be redelivered within the next few weeks and might end up being sold.

- As management continues to focus on building liquidity, common unit distributions are likely to remain unchanged for the time being.

- KNOT Offshore Partners continues to face near-term issues in both the North Sea and Brazil. However, with the medium- to long-term industry outlook remaining constructive, I am reiterating my "Hold" rating on the common units.

Note:

I have covered KNOT Offshore Partners LP ( KNOP ) previously, so investors should view this as an update to my earlier articles on the company.

After the close of Wednesday's regular session, leading shuttle tanker operator KNOT Offshore Partners LP, or "KNOP," reported stable third quarter results. However, profitability and cash generation continue to be impacted by special survey requirements, higher interest rates, and ongoing weakness in the North Sea market.

{kind=link}

In recent months, the company managed to secure additional work for a number of vessels:

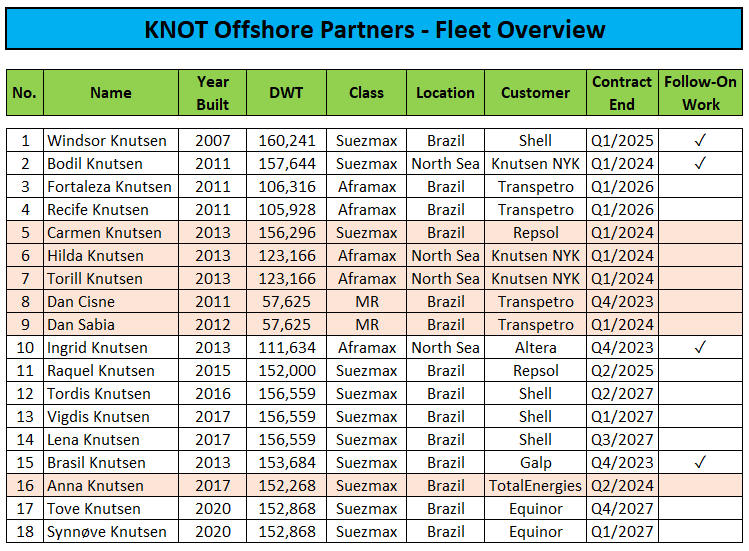

- Shell plc (SHEL) exercised its option to continue its charter of the Windsor Knutsen through to the first quarter of 2025. Subsequent to the end of the Shell contract, the vessel will commence a new two-year charter with another oil major.

- To facilitate the above-discussed follow-on work, the company has reached an agreement with Equinor ASA ( EQNR ) or "Equinor" to substitute the Brasil Knutsen for the Windsor Knutsen under a previously-disclosed contract. As a result, the Brasil Knutsen will be employed until at least the end of 2025.

- The partnership also signed an agreement with Shell to extend the current time charters for the Tordis Knutsen and Lena Knutsen by one year each, thus resulting in the vessels being employed until mid-2027.

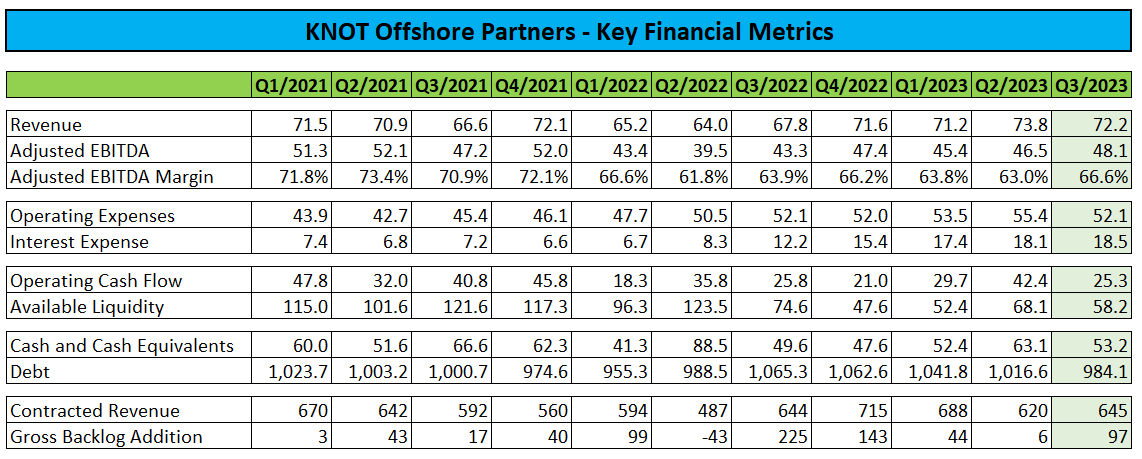

As a result, contracted revenue increased by 4% on a quarter-over-quarter basis to $645 million. Current charter coverage for 2024 now stands at 70%.

However, the company hasn't managed to secure follow-on work for the MR shuttle tankers Dan Cisne and Dan Sabia . Consequently, both vessels will be redelivered to KNOP within the next few weeks. Given their unusually small size for today's shuttle tanker markets, I would expect the vessels to be sold in the not-too-distant future.

During the third quarter , the company repaid $10.2 million in remaining debt related to the Dan Cisne with a final $6.5 million payment for the Dan Sabia due next month.

In addition, customer Repsol Sinopec or "Repsol" has not yet exercised its 12-month extension option for the Carmen Knutsen despite the vessel being scheduled to roll off the contract in approximately four weeks. Last year, Repsol exercised its option already in late November.

Based on past experience, I would not be surprised to see the shuttle tanker being redelivered to KNOP.

Please note that Carmen Knutsen is working offshore Brazil, a market which, according to the company, has been tightening in recent quarters. Given this issue, I am surprised that Repsol has been hesitant to charter the vessel for another year.

Moreover, customer TotalEnergies SE ( TTE ) has not yet exercised its option for an extension of the Anna Knutsen, with the current contract's firm term scheduled to end in Q2/2024.

{kind=link}

Upon redelivery, four ( Dan Cisne , Dan Sabia , Carmen Knutsen, Anna Knutsen ) out of fourteen vessels currently operating in Brazil would have to rely on support from parent Knutsen NYK Offshore Tankers ("Knutsen NYK") or otherwise face near-term idle time.

Moreover, with weakness in the North Sea expected to persist for several more quarters, the company will have to rely further on Knutsen NYK for short-term employment of the North Sea shuttle tankers Hilda Knutsen and Torill Knutsen at discounted rates while Bodil Knutsen will soon commence a new two-year contract with Equinor.

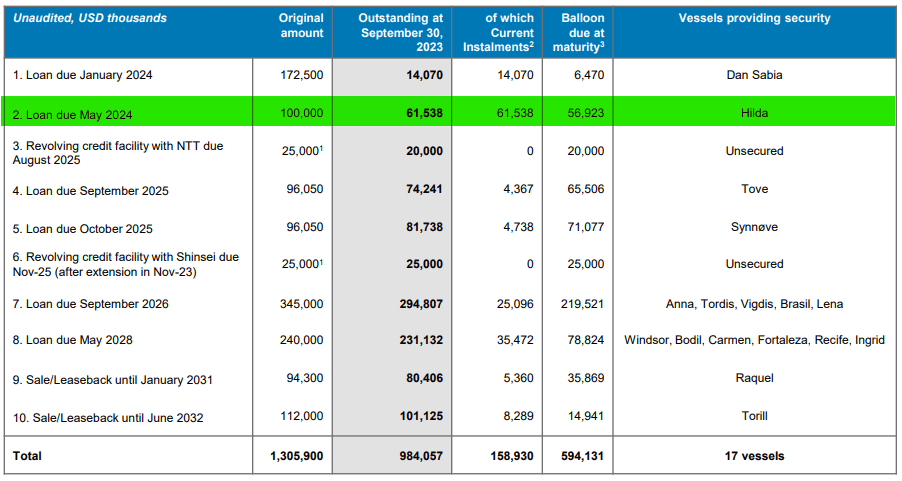

Over the past few months, the company managed to roll over two $25 million revolving credit facilities with Japanese lenders NTT Finance Corporation and SBI Shinsei Bank until August 2025 and November 2025, respectively.

Despite the 95% common unit distribution cut at the beginning of the year, net debt has decreased just slightly in recent quarters. At the current pace, it will take years to reduce debt to more reasonable levels.

Please note that the company is facing a $56.9 million balloon payment related to the Hilda Knutsen in May 2024. Without a long-term contract for the vessel, refinancing terms are not likely to be great.

{kind=link}

While a near-term sale of the Dan Sabia and Dan Cisne might result in estimated net proceeds of between $50 million and $60 million, cash flow from operations would take a further hit.

Remember also that KNOP has two Aframax-size shuttle tankers ( Recife Knutsen and Fortaleza Knutsen ) operating under bareboat charter agreements with a division of Petróleo Brasileiro S.A. - Petrobras ( PBR ) in Brazil. While these vessels are much larger than Dan Cisne and Dan Sabia , the Brazil shuttle tanker market is dominated by even larger Suezmax-size vessels these days.

Given this issue, Recife Knutsen and Fortaleza Knutsen might also be at risk of being redelivered to the company following the end of their long-term contracts in early 2026, particularly with Petrobras expected to take delivery of two newbuild Suezmax-class shuttle tankers from parent Knutsen NYK in late 2024 and late 2025 respectively.

In fact, this wouldn't be the first time that Knutsen NYK newbuilds replace the partnership's existing vessels in contracts with key customers.

Last year, Eni S.p.A. ( E ) decided to redeliver the North Sea shuttle tankers Ingrid Knutsen , Hilda Knutsen, and Torill Knutsen to KNOP after taking delivery of two newbuilds from the parent.

However, with Brazil offshore oil production expected to grow meaningfully over time, the Johan Castberg FPSO in the North Sea expected to come online by late 2024, and only five new shuttle tankers currently under construction, the medium- and long-term industry outlook remains constructive.

Bottom Line

While KNOT Offshore Partners LP reported stable third quarter results, the company continues to face near-term issues in both the North Sea and Brazil.

With Dan Cisne and Dan Sabia likely either being redeployed at lower rates or outright sold, the company will have a tough time improving profitability and cash flow generation next year.

As management continues to focus on building liquidity, common unit distributions are likely to remain unchanged for the time being.

Consequently, I would expect the common units to remain dead money for the time being.

However, with the medium- to long-term industry outlook remaining constructive and a potential buyout offer by parent Knutsen NYK still in the cards, I am reiterating my " Hold " rating on the common units.

For further details see:

KNOT Offshore Partners: No Distribution Increase Anytime Soon - Hold