KN - Knowles Corporation Is Highly Profitable But Investors Should Be Price Sensitive

2023-08-19 07:17:09 ET

Summary

- Volumes are declining due to weak demand and high customer inventories.

- Profit margins have recently improved thanks to productivity initiatives and some restructuring efforts.

- The company's balance sheet is virtually debt-free, as net debt is just $3 million.

- The company is ready to carry out significant acquisitions in the foreseeable future.

- The recent share price decline represents a good opportunity for investors, but averaging down is highly advisable as the P/S ratio is still slightly above the average of the past few years.

Investment thesis

The past few quarters have left a bittersweet feeling among Knowles Corporation's ( KN ) shareholders, with investors remaining cautious as the share price has declined by 31% since January 2022. Although efficiency improvement initiatives and fixed cost reductions have recently produced a significant improvement in profit margins, they remain weak compared to what shareholders were used to before the current headwinds, and now revenues are starting to decline caused by weaker demand and high customer inventories.

Despite this, the restructuring efforts carried out in recent years have left us with a smaller company (in terms of revenues) but with greater growth potential and a completely healthy balance sheet. In addition, the company's profit margins are high, which makes it possible to cover interest expenses and capital expenditures through cash from operations with ease and generate excess cash, which is currently being used to repurchase shares in order to reward shareholders (albeit at a slow pace) and should allow for bigger acquisitions from now on. This is why I consider that the current headwinds, which in my opinion are of a temporary nature due to their direct link with the current macroeconomic context, represent a good opportunity to start adding shares and wait for the company to improve its long-term prospects by making further acquisitions while share repurchases slowly expand per-share metrics.

A brief overview of the company

Knowles Corporation is a global provider of advanced micro-acoustic microphones and balanced armature speakers, audio solutions, and high-performance capacitors and radio frequency filtering products. The company's products are used in the medtech, defense, consumer electronics, electric vehicle, industrial, and communications markets. It was founded in 1946 and spun off from Dover ( DOV ) in 2014, and its market cap currently stands at $1.51 billion, employing around 7,000 workers in 13 countries.

Knowles logo (Knowles.com)

The company operates under three main business segments: Precision Devices, Medtech & Specialty Audio, and Consumer MEMS Microphones. Under the Precision Devices segment, which provided 32% of the company's revenues in 2022, the company manufactures high-performance capacitors and radio filtering solutions for the defense, medtech, and electric vehicle markets. Under the Medtech & Specialty Audio segment, which provided 30% of the company's revenues in 2022, the company manufactures balanced armature speakers and microphones for leading hearing health manufacturers and premium audio markets. And under the Consumer MEMS Microphones segment, which provided 38% of the company's revenues in 2022, the company manufactures micro-electro-mechanical systems ((MEMS)) microphones and audio solutions for the ear, Internet of Things, computing, and smartphones markets.

The company has a strong cyclical nature, which is reflected in the share price swings that took place over the years, and therefore, it is very important to take advantage of times of high pessimism for investing in order to increase potential returns once optimism returns to investors when the company's prospects improve. Despite this, averaging down is highly advisable as price volatility is currently high.

Currently, shares are trading at $16.49, which represents a 30.74% decline from recent highs of $23.81 on January 5, 2022, which reflects investors' growing pessimism as profit margins remain weak, despite recent improvements, while volumes have recently declined as a consequence of postponed orders in the defense industry, weakening of demand in the telecom industry, and high customer inventories in the Precision Devices segment at a time when the economy could face a potential recession as a consequence of the recent interest rate hikes to contain the high inflation rates in the world.

Recent acquisitions

Since the spin-off from Dover, Knowles has made extensive restructuring efforts by divesting lower-margin businesses and deleveraging its balance sheet, which has significantly reduced long-term risks as the company currently has higher cash and equivalents than long-term debt.

In July 2015, the company acquired Audience, Inc. in order to expand capabilities in intelligent audio and signal processing solutions, for $85 million. A year later, in July 2016, the company sold its mobile consumer electronics speaker and receiver product line to Loyal Valley Innovation Capital for $45 million due to the low margins that the business delivered.

The restructuring process continued in November 2017 when the company sold its timing device (oscillator) business to Microsemi Corporation ( MSCC ), as the business offered limited growth prospects and a low margin profile, for $130 million and used the proceeds to reduce debt exposure, and later, in December 2019, the company acquired the MEMS microphone ASIC design business from ams AG ( AMSSY ) for $58 million.

In short, the company has significantly restructured the business and, as a result of a stronger balance sheet (and positive profit margins) the management expects bigger acquisitions in the foreseeable future as stated by CEO Jeffrey Niew during the earnings call conference of the second quarter of 2023. Meanwhile, Knowles keeps deleveraging its balance sheet and performing share repurchases in order to reward long-term shareholders by passively expanding their positions.

Revenues are receiving another blow

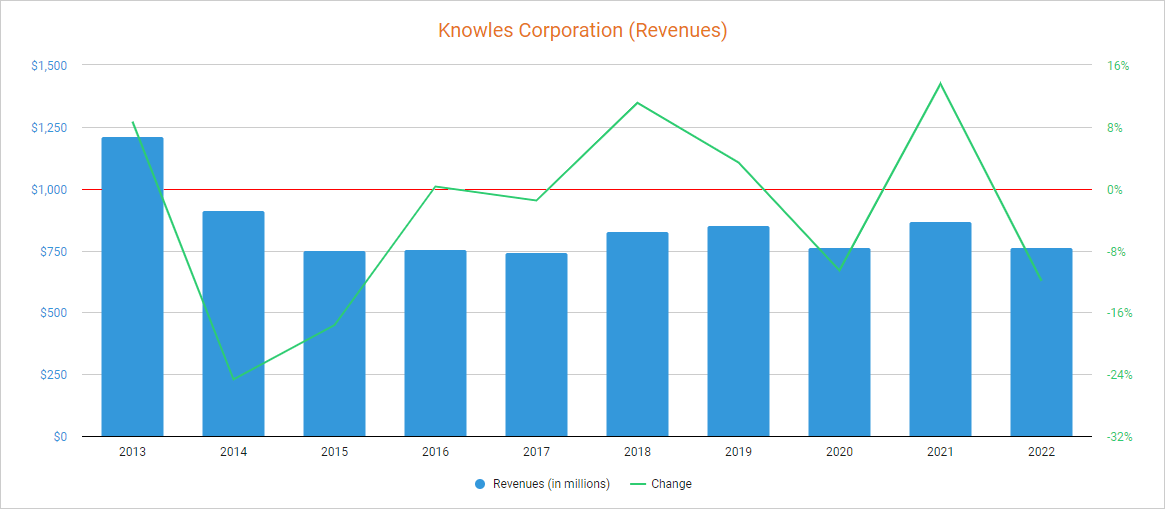

Since the spin-off, the company's sales have been reduced due to restructuring activities, and although the trend was positive before the coronavirus pandemic (revenues increased by 11.11% in 2018 and by 3.37% in 2019), the coronavirus pandemic caused a decline of 10.59% in 2020 compared to 2019. Sales seemed to recover in 2021 as they increased by 13.58% year over year, but weaker demand and high customer inventories caused another decline of 11.91% in 2022.

{kind=link}

As for 2023, net sales declined by 28.35% year over year (and by 26.79% sequentially) during the first quarter, and by 7.98% year over year during the second quarter (but increased by 19.89% compared to the first quarter). This further decline during 2023 has been primarily caused by high customer inventories, especially in the Precision Devices business, as well as order delays for warfare programs in the defense industry, as revenues in the segment declined by 20% year over year during the second quarter, but headwinds started to ease in the second quarter as the MedTech & Specialty Audio delivered revenues over 30% higher compared to the first quarter (despite a 2% decline year over year) and the management expects the positive trend to continue for the rest of the year.

Due to current weaknesses in the industrial and telecom markets and unusually high inventory levels, the management expects sales to remain weak through the second half of 2023 as revenues are expected to decline by 10.07% for the full year to ~$688 million. Nevertheless, inventory headwinds should be of a temporary nature as revenues are expected to partially recover in 2024 as they are expected to increase by 7.32% compared to 2023, and the excess cash generated through operations should allow investments to expand the company's reach either through expansions of manufacturing capabilities or new acquisitions.

But despite the recent decline in revenues, an even faster decline in the share price has caused a mild decline in the P/S ratio to 2.180, which means the company generates $0.46 in revenues for each dollar held in shares by investors annually.

This ratio is still 9.36% higher than the average since the spin-off from Dover in 2014 but represents a 21.16% decline from the highest point of 2.765 reached in 2015, which means investors' pessimism is growing as they are placing less value on the company's sales, despite a stronger balance sheet, due to weaker-than-usual margins, decreased volumes, and growing fears of a potential recession due to recent interest rate hikes, but pessimism has been even more damaged in other times as can be seen in the chart, so averaging down should help partially cushion the risk of further volatility in the share price. Still, it is important to note that the company is highly profitable and profit margins are showing strong signs of recovery as inflationary pressures and supply chain issues are easing, so it should be able to generate enough cash to continue strengthening its balance sheet and perform significant acquisitions and share repurchases.

Margins are showing strong signs of recovery

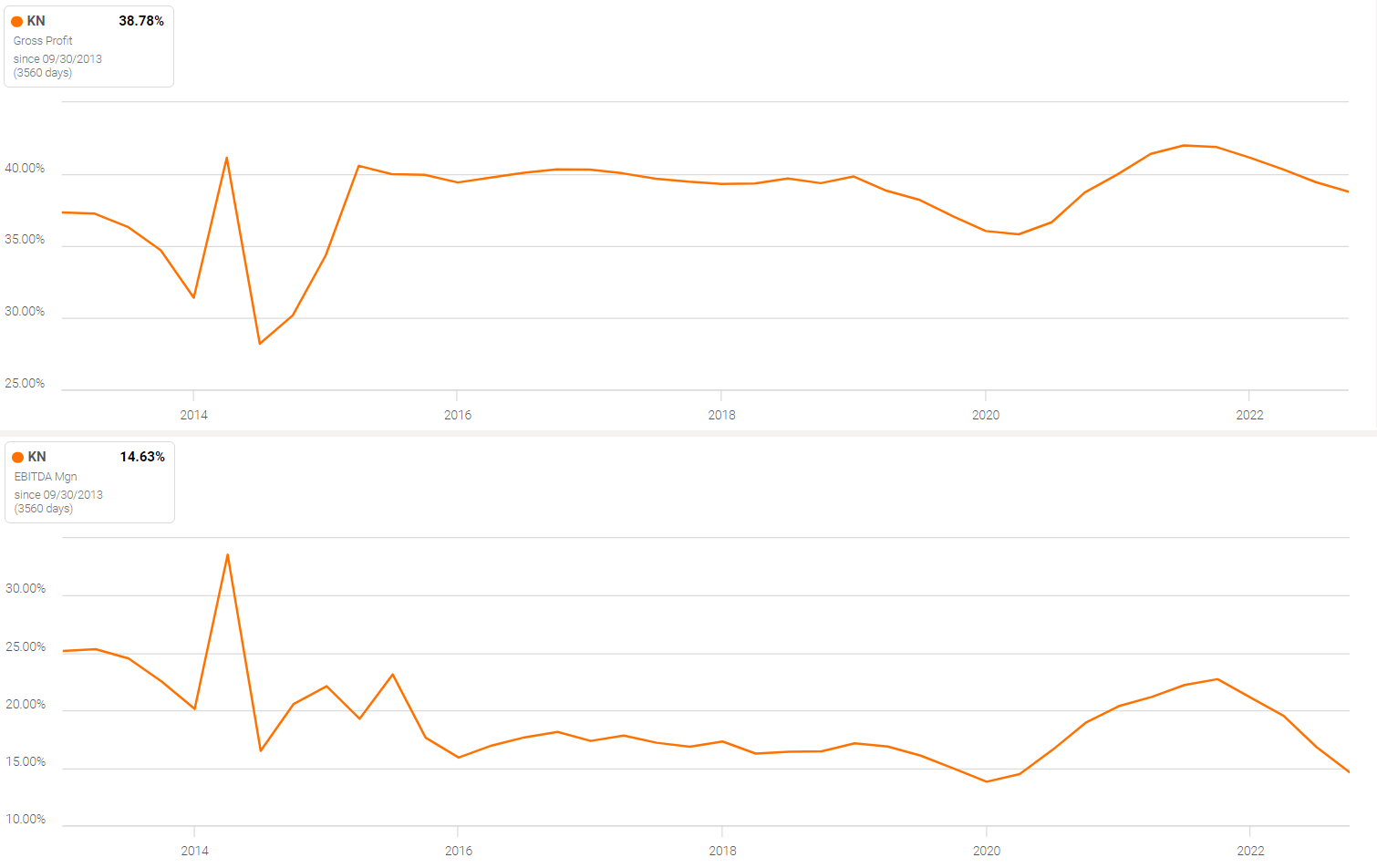

As a consequence of unfavorable capacity utilization due to weakened volumes, the company has suffered declining margins in recent quarters. In August 2022, it announced a restructuring program in its MEMS Microphones product line (which is already finished) in order to right size manufacturing capacity and thus achieve annual savings of $25-$30 million, but margins remained weak despite these efforts. In this regard, the trailing twelve months' gross profit margin currently stands at 38.78%, and the EBITDA margin at 14.63%, which means the company is highly profitable.

{kind=link}

Furthermore, the gross profit margin improved to 42.60% during the second quarter of 2023, and the EBITDA margin to 16.94% as the company is carrying out efficiency improvement initiatives and fixed cost reductions to offset increased production costs and decreased volumes. Furthermore, the management expects this margin expansion to continue its positive trend during the second half of 2023 and beyond as ongoing profitability initiatives should be more strongly reflected as volumes recover. Meanwhile, they expect to reduce annual operating costs by $5 million in the Precision Devices segment by the end of the year, which coupled with recovering volumes should result in margins similar to those of 2022, when the EBITDA margin surpassed the 20% mark, in the foreseeable future.

The deleveraging phase is complete

Since the spin-off of the business, the company has divested those businesses with limited growth prospects and below-company-average profit margins, and although it acquired some businesses in the meantime, the excess cash from the divestitures, as well as positive profit margins, have enabled a reduction in the long-term debt from $399 million at the end of 2015 to $45 million in the past quarter. Despite this remaining long-term debt, the company is virtually debt-free as its net debt is just $3 million thanks to cash and equivalents of $54.4 million.

Furthermore, in addition to having managed to get rid of virtually all its debt, the company continues to generate excess cash through operations as trailing twelve months' cash from operations of $88.30 million is more than enough to cover interest expenses of $3.90 million and capital expenditures of $26.10 million.

During the past quarter, the company reported cash from operations of just $0.5 and inventories declined by $16.7 million, but accounts receivable increased by $8.5 million while accounts payable declined by $22.2 million, and the company reported a net income of $13.6 million.

Regarding capital expenditures, they have been significantly reduced in recent years and they are currently allocated to the design of new products for the defense, MedTech, and electric vehicle industries, and while trailing twelve months' cash from operations is below what the company used to enjoy, inventories have risen significantly to $192 million, suggesting that the company should eventually be able to convert those inventories into actual cash once volumes begin to recover.

In this sense, the excess cash from operations after covering interest expenses and capital expenditures is currently being used to reduce long-term debt and perform share repurchases, although the management expects that the end of the deleveraging phase will open the door to significant acquisitions in the short to medium term as it will soon no longer need to pay down any long-term debt.

Share repurchases are reducing the total number of shares outstanding very slowly

Although the company's shares suffered some dilution in the early years after the spin-off from Dover as the total number of shares outstanding increased by 7.19% since then, the management has set out to reverse the trend and begin to reduce them as they announced a share repurchase program of $100 million in In February 2020. In April 2022, they announced a $150 million addition to the existing share repurchase program, and the company repurchased $5 million worth of shares during the second quarter of 2023, which means share buybacks continue in force.

This means that each share represents an increasingly larger slice of the company, and although the impact so far has been very limited as the total number of shares outstanding has been reduced by just 0.61% since 2020, the pace seems to have started to pick up since the addition of the $150 million during the second quarter of 2022 as shares outstanding declined by 0.92% year over year during the second quarter of 2023. Even so, CEO Jeffrey Niew stated that investors should expect further share repurchases in the future:

As far as the stock buyback, I think we've committed not 50%, but more than 50% of our free cash flow to go towards share repurchase. I think year-to-date, for the full year, we've actually spent more than 50% of the cash flow year-to-date through Q2 on share repurchases. And we'll continue to buy back shares in line with what we've talked about in the past.CEO Jeffrey Niew - Q2 2023 Earnings Call Conference .

In this regard, investors could expect their positions to gradually grow (albeit at a slow pace) as the management appears to be committed to keeping the pace of buybacks and expects to continue making buybacks as the long-term debt has already been almost fully paid off.

Risks worth mentioning

Overall, I consider Knowles' risk profile to be low thanks to cash and equivalents of $54.4 million compared to a long-term debt of $45 million. In addition, high inventories should eventually enable stronger cash from operations in the medium term, and the company is currently highly profitable as it has relatively high gross and EBITDA margins. Despite this, there are certain risks that I would like to highlight, especially for the short and medium term.

- If inflation rates do not return to healthier levels soon or rise again, the company's profit margins could further deteriorate, leading to another reduction in the company's ability to generate cash.

- Recent interest rate hikes could spark a global recession, which could have a significant impact on the demand for Knowles' products. This could cause a further decline in volumes, which would negatively impact revenues and profit margins.

- Having finished deleveraging the balance sheet, it appears that the company is reaching a point where it will have to make major acquisitions to expand its business. In this regard, the acquisitions carried out may not deliver the expected results.

- If volumes don't recover as expected, the company may have a difficult time emptying its inventories, which could result in low cash from operations.

- The rate of reduction of outstanding shares is currently very slow, so if the management decides to slow down share repurchases to make room for potential acquisitions, the total number of outstanding shares could stop declining or even begin to grow as it did up to 2020.

Conclusion

It is certainly normal for Knowles Corporation shareholders and potential investors to have bitter feelings regarding the current state of the company, and I consider that the 31% decline in the share price since January 2022 is actually justified. Despite the fact that profit margins have improved significantly in the last quarter, these are still below the margins the company used to enjoy before the current headwinds, and cash from operations is suffering as a result. In addition, lower volumes have created a significant increase in inventories which, despite representing a significant strength for the balance sheet, will eventually have to be converted into cash, for which the company will have to wait for volumes to improve. Of course, we must not forget that a potential recession could have a significant impact on the growth opportunities of the company as its operations could be seriously damaged due to a further reduction in volumes.

Despite this, I believe that the current fall in the share price represents a good opportunity for investors interested in acquiring shares as not all aspects are negative and the future seems to be full of opportunities for Knowles. The company has high profit margins despite depressed volumes, so it is expected to generate strong cash from operations in the future as profit margins should improve even further along with recovering volumes. In addition, long-term debt has been reduced to very low levels while high inventories should eventually allow for stronger cash from operations, which should allow the management to make significant acquisitions in the foreseeable future.

But despite this, I believe that recent high volatility in the share price and a P/S ratio slightly above the average of the past few years suggest that investors should be wary of the share price and, instead of betting on a relatively quick recovery, should average down if the share price keeps declining.

For further details see:

Knowles Corporation Is Highly Profitable, But Investors Should Be Price Sensitive