KNYJY - KONE: Beware The China Risk

2023-07-03 21:06:14 ET

Summary

- KONE has started 2023 on a positive note, largely due to the resilience of its service business.

- But its outsized China real estate exposure is a concern, particularly with macro data continuing to deteriorate.

- Most of the positives are already priced in at the current premium valuation.

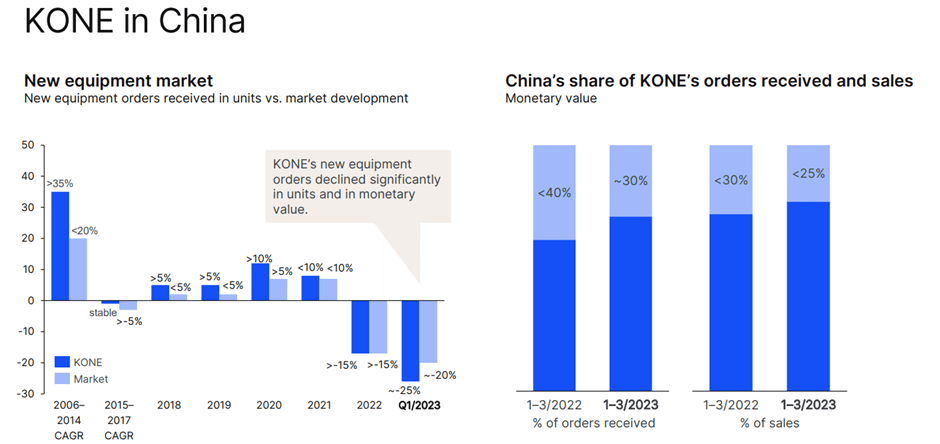

Global elevator/escalator supplier KONE Oyj ( KNYJY ) isn't losing its market leadership anytime soon, but its exposure to the China elevator market should concern investors. While Q1 showed that overall sales growth remained robust in the mid-single-digits %, its outsized China contribution (~30% of orders; <25% of sales) means its near-term earnings trajectory is ultimately tied to a recovery in the still-troubled Chinese real estate market. Yet, recent macro data out of China indicates the outlook for property and industrials is worsening, which doesn't bode well for new installations this year (recall that last year also saw a contraction on the back of China headwinds). In contrast, KONE's share valuation remains lofty at >30x P/E, a premium to historical levels, likely in hopes of policy support for the Chinese real estate market. In the likely event that the scale of stimulus measures disappoints and macro continues to disappoint in the near-term, KONE stock could have the wind taken out of its sails. Pending visibility into an improvement in the Chinese property/local government debt situation, I remain neutral here.

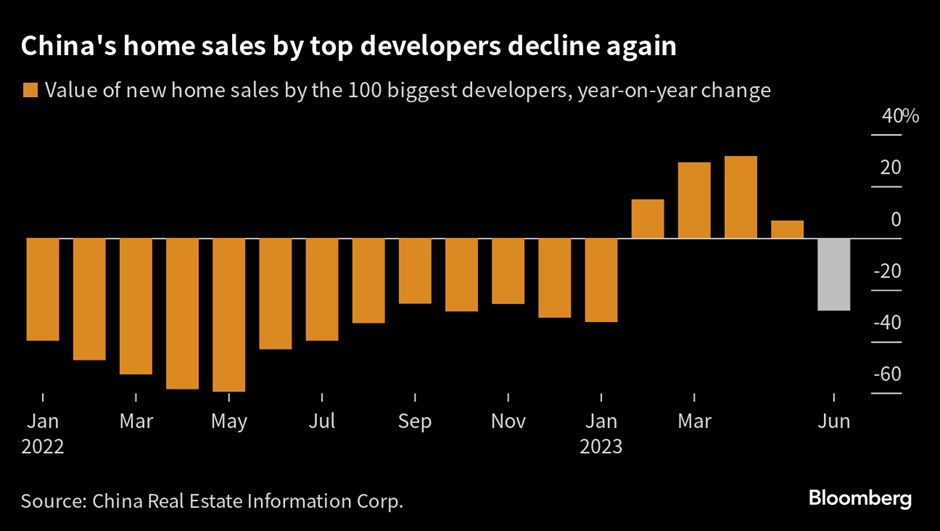

The China Real Estate Turnaround Isn't Turning

The deteriorating property sector in China has been a key drag on the post-reopening recovery. Following an underwhelming first four months, the decline in property sales by floor area steepened in May to 0.9% YoY, along with new construction starts at -22.6% (vs. down 21.2% through April). Per China Real Estate Information data , housing sales of China's top hundred real estate developers also fell low-double-digits % YoY, reflecting demand weakness rather than supply-side factors. The gloomy real estate data contrasts with management's upbeat expectations in Q1 for a recovery in apartment constructions and order flow (note many unfinished properties don't yet have elevators installed). Alongside deteriorating PMIs, a wave of property debt defaults (sized at a massive 12% of GDP by Bloomberg ), and a persistently high youth (aged 16-24) unemployment rate of >20%, there is now a material risk that a full-blown Chinese real estate crisis is on the horizon.

{kind=link}

In response, chatter about a new stimulus package (targeted at the troubled real estate sector) has ramped up. Possible measures include support for local governments and a step up in infrastructure investment via policy bank loans, as well as regulatory easing for housing transactions (e.g., lower down payment and brokerage fees). We'll probably get some answers at this month's Politburo meeting, but for now, it seems presumptuous to underwrite unconfirmed policy support. And even if stimulus comes through, the scale and impact of the support measures are far from certain, given the government's balance sheet constraints (note the $10tn of local government debt ). Plus, more fiscal easing doesn't bode well for KONE's CNY-linked revenue base. Having already suffered a steep decline relative to the EUR this year due to the PBoC's monetary easing, more rate cuts (to facilitate fiscal easing) and further FX headwinds post-Q2 will weigh on the top line.

{kind=link}

2023 Bridge at Risk from Emerging Global Headwinds

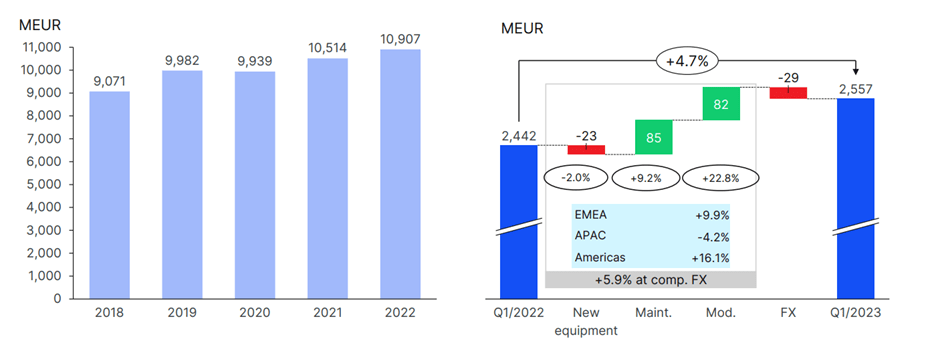

KONE posted stronger than expected Q1 2023 orders of EUR2.3bn – while this was still down ~5% YoY on a like-for-like basis, it represented a deceleration from the ~11% decline in Q4 2022. Helped by low-single-digit % order book growth, sales were up ~6% YoY to EUR2.6bn on a like-for-like basis, however, accelerating from Q4 2022. Despite the good start to the year, management noted the equipment market in North America has already "declined significantly" and appears to be pacing continued declines into 2024. With no respite from China ("activity declined significantly") and Europe ("activity declined significantly in Central and North Europe and slightly in South Europe"), I would be cautious about underwriting a mid-single-digit % organic growth algorithm on the equipment side.

On the other hand, the service market (maintenance and modernization) has been resilient, growing low to mid-single-digits % through Q1 and offsetting ongoing declines for equipment. Expect more of the same in Q2 as new price escalations roll through a 'sticky' KONE installed base. Whether this will be a sufficient buffer against deeper YoY China equipment declines in H2 remains unclear, though, particularly against the low-single-digit % organic sales growth target this year.

{kind=link}

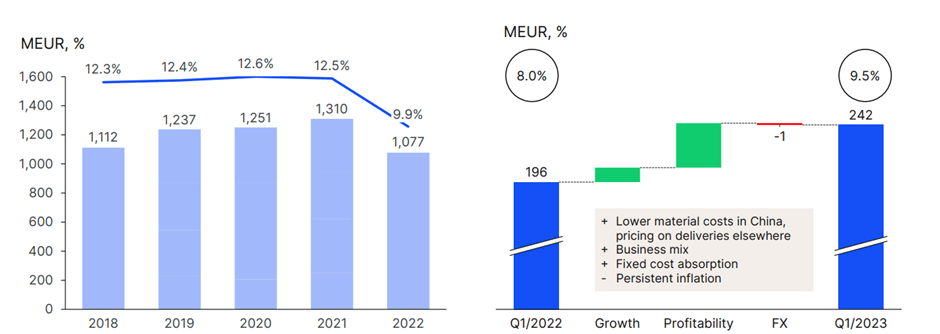

The Q1 margin performance was more upbeat – adj EBIT of EUR242m (+23.1% YoY) equated to a margin of 9.5% or +150bps of expansion YoY. Improving logistics and materials costs were key contributors, along with a positive mix shift toward services sales. With cost savings poised to add EUR25m for the year (EUR75m in 2024), KONE is well placed to grow its EBIT vs. 2022 despite persistent wage pressures. On the flip side, limited operating leverage benefits from the equipment side will be a material headwind. And while the China business is currently being boosted by lower post-COVID costs, accelerating wage costs into H2 in its other operating geographies (in response to higher consumer inflation) could weigh on overall margins. Finally, management has also pinned its hopes on higher pricing moving through the backlog (led by the Americas), which could prove challenging on the equipment side in light of deteriorating PMIs globally.

{kind=link}

Beware the China Risk

KONE remains a quality operator, and investors shouldn't have much trouble underwriting its leadership positions in the North American, European, and Asian elevator markets over the long term. While the quality of its business is hard to dispute, KONE remains highly exposed to the troubled China real estate market. In contrast to the reopening boost expected at the start of the year, the recovery has been uneven, with industrials and property lagging the consumer rebound. In turn, worsening Chinese macro and real estate data point to significant headwinds for KONE's near-term earnings trajectory. Given the uncertainty surrounding the developer/LGFV debt situation as well, I wouldn't rule out structurally lower China property growth either. The stock hasn't yet reflected this pessimism, and the stimulus optimism in recent weeks certainly doesn't help the valuation case. Pending a meaningful de-rating, I would steer clear.

For further details see:

KONE: Beware The China Risk