KNYJF - KONE: Exercise Caution Reiterate 'Hold'

2023-06-28 05:22:35 ET

Summary

- I previously labeled KONE stock as a "HOLD" due to unfavorable margin trajectories and internal difficulties.

- The rate of return since the last article has justified my cautious stance on the company.

- The company still has some ways to go before a turnaround or positivity can be expected, and for that reason, I'm still somewhat cautious here and call it a "HOLD".

Dear readers,

When I last wrote about KONE ( KNYJF ), I called the company a "HOLD" due to generally unfavorable margin trajectories as well as internal difficulties, leaving me with a very small overall watchlist position in the company. I've been watching KONE and other Finnish companies carefully, knowing that at one point, they'll become attractive investments once again.

The RoR we've seen in the meantime has justified my cautious stance on the business. I gave the company a native target of €42/share last time I wrote about it. Let's see how this stance has held up in the face of recent trends. Here are the results from the latest article.

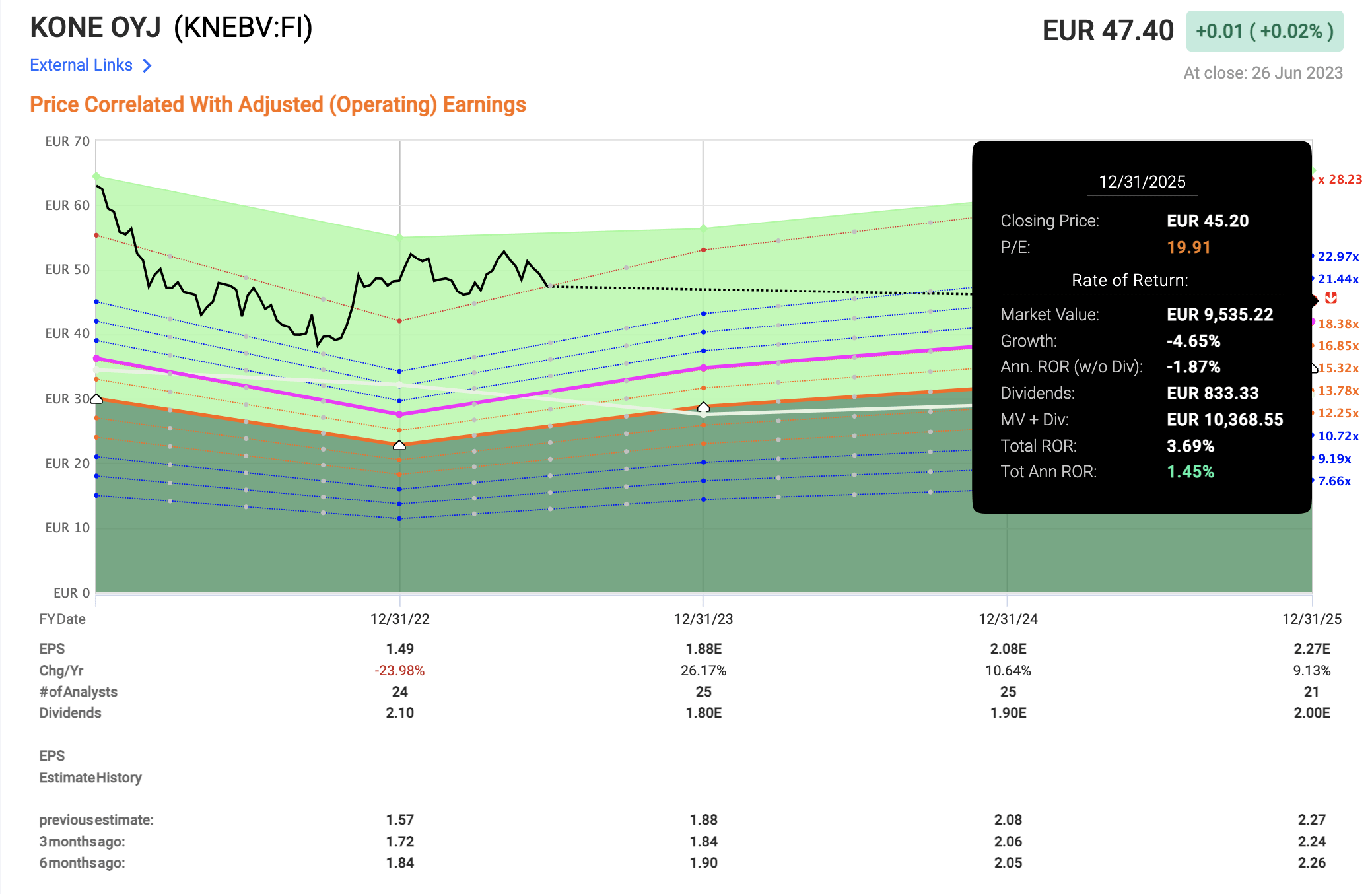

Seeking Alpha KONE RoR (Seeking Alpha)

Obviously, some of the challenges we expected here, but it still seems that the company has some ways to go before we can expect a turnaround or positivity here.

Let's see about the latest set of results.

KONE - The latest results in 1Q23

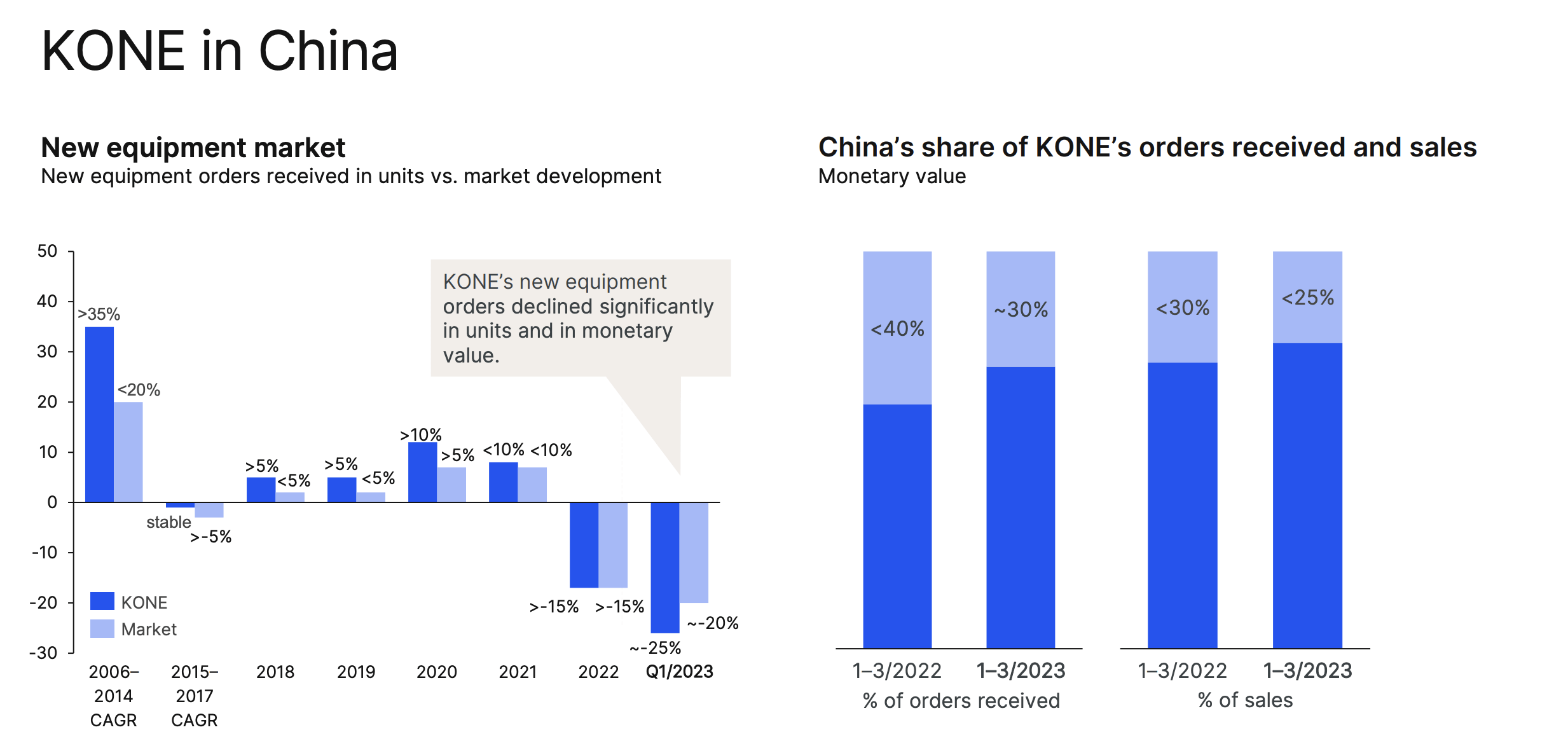

1Q23 was a good quarter for KONE, in that sales momentum was actually good. Services saw good trends as well, but some of the main trends in why the company is seeing such significant weakness is still very much in play for KONE - specifically China. The Chinese market remained a weak segment in the quarter, even though the company was able to report the first policy-related improvement in construction.

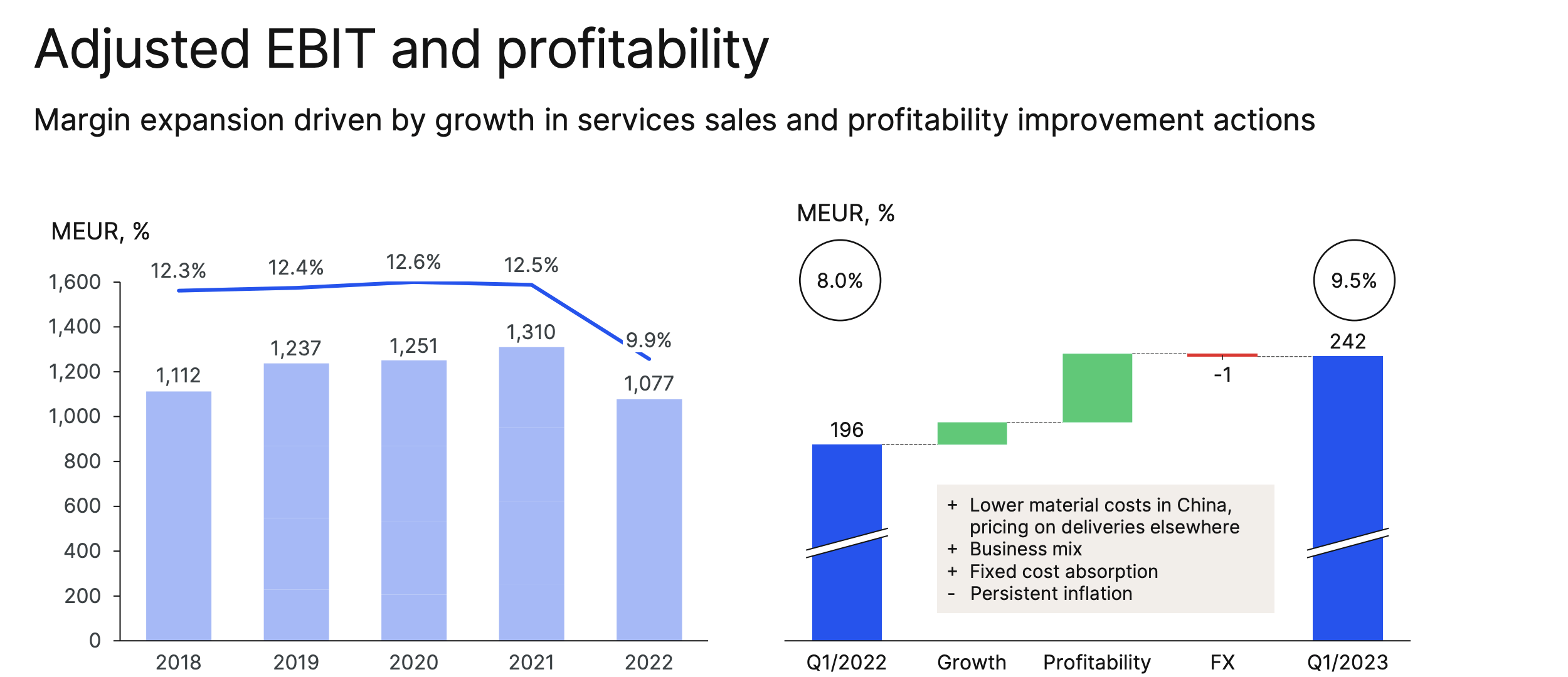

Remember, a big part of why the company has so significantly underperformed is the trends in Construction and the fact that construction/infrastructure in China which has been a tailwind for the company for several years, has turned sour. So despite talk about profitability improvements, which are there, it's important to note very clearly that orders are down over 6%, and the order book is shrinking almost 1% YoY, with around a 1.5% improvement in EBIT margin. This has improved earnings substantially - 42.2% from a basic EPS perspective - but it's also from a very low overall level compared to what the company has actually managed historically.

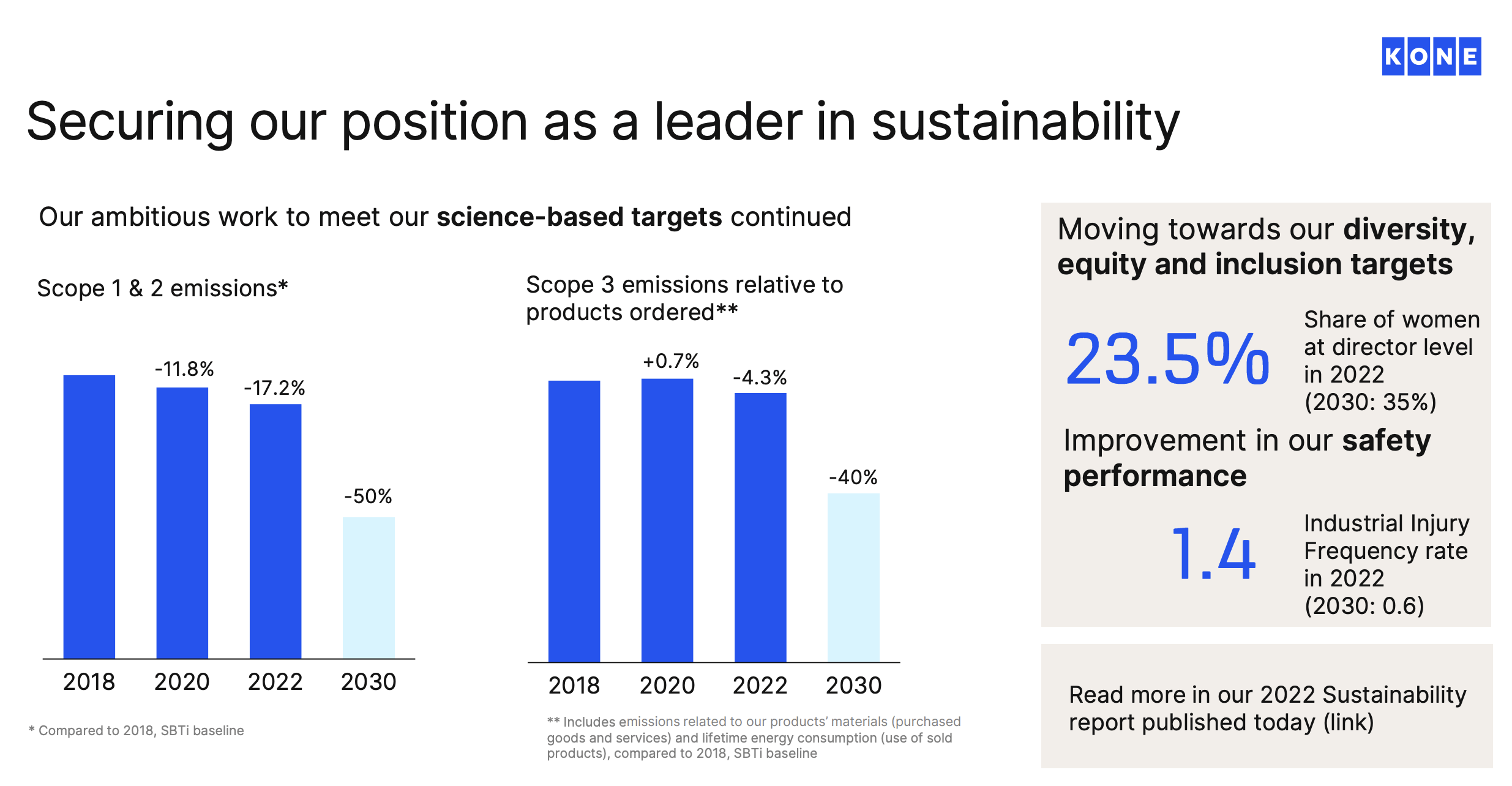

As with other companies, I know that when a company starts off talking about sustainability and ESG, diversity, equity, and inclusion targets, that tends to mean that other targets might not be doing so well. This is not me saying that these things are not important - they most certainly are - but I as an investor care more about the hard numbers relating to profit, and KONE isn't a concrete company where they have to essentially pay carbon taxes/credit in the same way.

{kind=link}

So the fact that KONE is leading sustainability, as above, would be a great set of news. But it also comes with the fact that KONE is losing market share. The company has dropped to #2 in EMEA as a New Equipment supplier, and holding steady or growing in other geographies/in the maintenance segment. The new equipment market has been declining by over 10% in 2022, meaning the total new equipment market came in at about 1,000,000 units overall, while the maintenance market grew by about 5%, or maintaining 20M worldwide units while modernizing grew 5-10% during the year as well, depending on geography and segment. This makes sense in light of global trends where companies are being more careful and refurbishing, as opposed to buying new equipment.

It's unfair to say that KONE is in "dire straits" - but it's not wrong to say that the problems in KONE are far from over. Unless the new equipment market picks up, there is a possibility that we'll see continued pressured development from this for the foreseeable future.

{kind=link}

The fact that service and refurbishment are so positive should be seen as nothing but a natural overall development - not necessarily something that's a positive surprise.

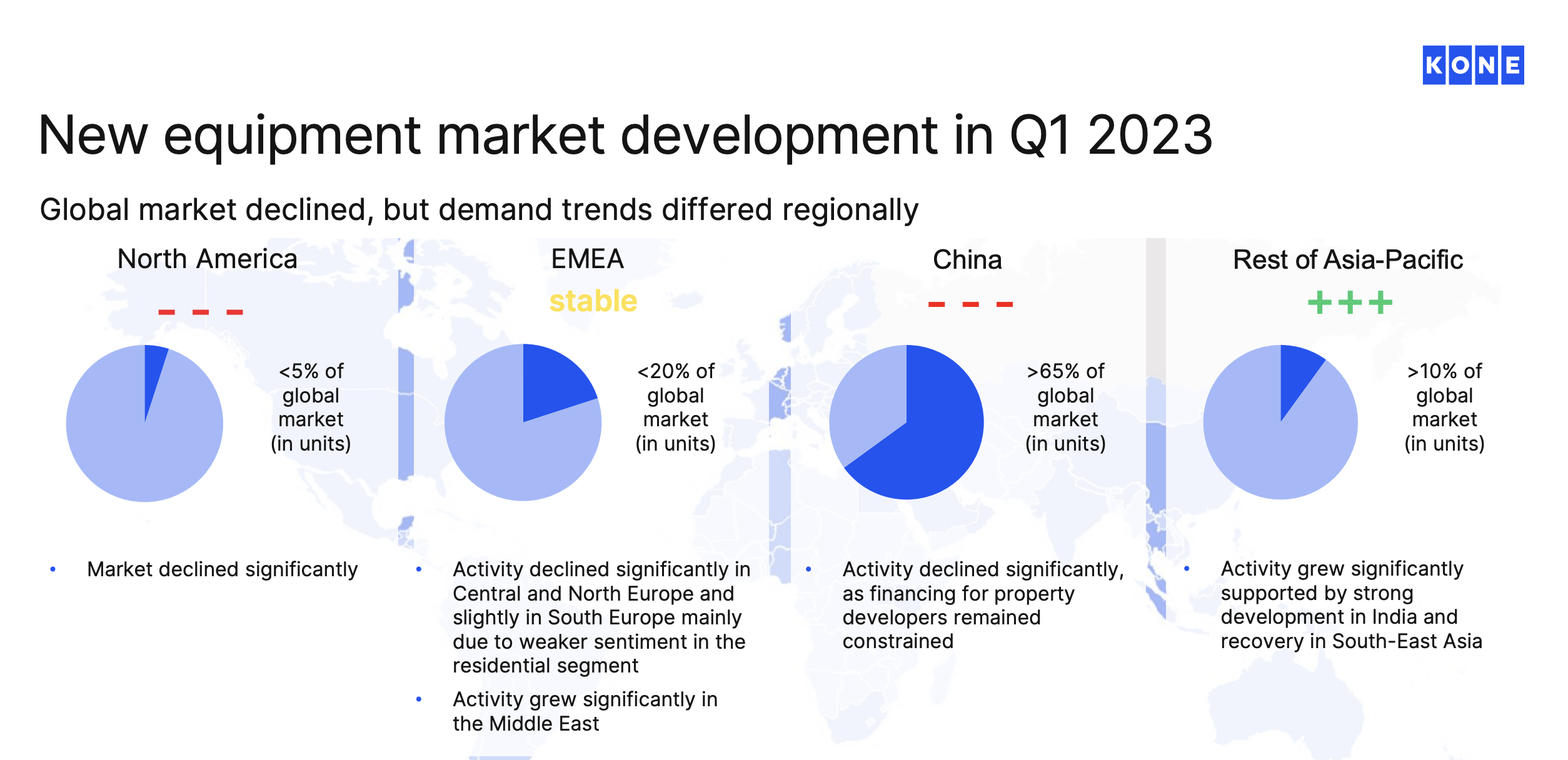

The risks to focus on here is market activity, not only in China but in negative segments here. New equipment demand is going to remain low as long as financing costs are high and developers, regardless of market, are constrained. It's wrong to characterize China as the only market with constrained development activity at this time.

In China though, the problem is intense competition for contracts, leading to margin pressure that still is leading to negative Real estate investment numbers, sales numbers, completions, and new home prices - which are no longer going up and have been declining in some areas for over 2 years here.

The point can show a strong sales growth in service, somewhat compensating for the negativity in new equipment - but this only goes so far. Because when we compare with double-digit profitability numbers from before COVID-19 and the China crash, things aren't looking all that profitable here.

{kind=link}

The company market outlook unfortunately isn't much better here. KONE expects the new equipment market to decline by double digits in 2023E as well. Activity is expected to start picking up again at the end of that year, mostly due to government stimulus measures. While new equipment markets are expected to be problematic for some time, activity in refurbishing and modernization as well as maintenance is expected to grow in all regions, especially APAC - so this can weigh up the company's overall results.

The simple fact remains that the company's recent historical overfocus on China hasn't brought much good to the table in a market where the Chinese market has essentially gone to a standstill.

{kind=link}

These negatives are especially tough for a company like KONE which relies to almost 50% of its overall mix on new equipment historically, and which now is down to below 45%. This is especially true because KONE isn't any sort of market leader, but a challenger, in the services industry.

To give you a picture of what sort of decline this company has been through, KONE's gross margins are down to less than 13% of revenues, which is one of the worst gross margins in the sector, that sector being Industrial products, including peers such as Siemens ( SIEGY ), General Electric ( GE ), LG, Schneider Electric, Eaton ( ETN ) and others. A single-digit net margin isn't as terrible, but its significantly lower than KONE has managed in the past, and is especially bad when you consider that KONE is more of a company with escalators, elevators, and people transportation rather than a broad portfolio appeal some of these other businesses have. What I mean is that KONE is far more exposed to infrastructure and construction than some of its peers.

Many analysts consider KONE to be undervalued here. I am not one of them. While the company is a profitable one with good debt, only 0.38x to EBITDA, I see continued issues for profitability in the near term. There is an expectation for things to go better this year already, with further improvements over the next few years - but this is really only an improvement next to a relatively poor 2022A.

Let's look at the valuation and see what sort of upside we have here.

KONE - Upside is only possible if you like paying 25-30x P/E

The problem with KONE is that it has traded at a long-time premium for a company that really only has managed a sub-2% growth rate for the past decade or so.

An upside to a 30x P/E for this time when the company is trading at around 28x, is around 19% per year. But you have to decide if a company that's managed 1-2% for the past decade per year could be worth 30x P/E. A 15-20x P/E, with a 20x P/E as the highest upside, gives you a potential RoR on an annual basis of less than 2%, with a total RoR of 3.69%, with a total RoR of exclusive dividends is negative.

{kind=link}

That's my base case, and it goes to some way to explain as to why I am not yet positive about the company here. The one thing I want to see for the company is a normalization indication. We're seemingly seeing a bit of this here, but given the continued negative trends in new equipment, I'm not ready to invest in KONE at a normalized P/E of over 20x. Analyst accuracy is so-so - 25% negative miss ratio even with a 10% margin of error - and especially in the last 6-8 years, where at times analysts have missed by more than 25% in their estimates.

S&P Global gives us averages of €52/share based on 25 analysts, which do not go below €39/share, but go as high as €63/share. Despite a very high average, only 5 out of those 25 analysts are at a "BUY" here. Over 15 analysts are either at a "HOLD" or "Underperform" rating for the company here. I, therefore, have some issues reconciling these recommendations/ratings with where the company views the company as being valued.

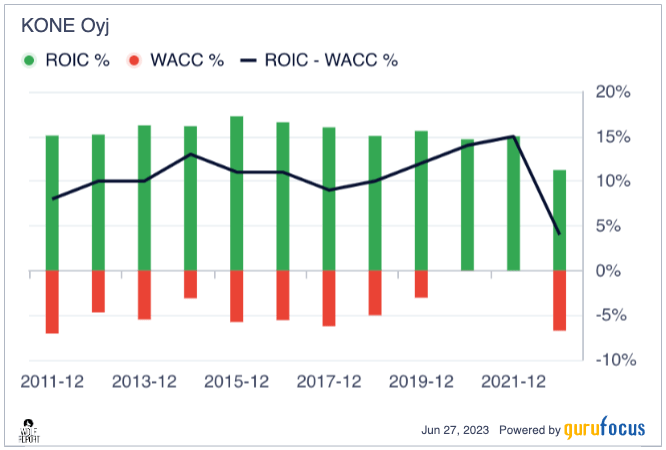

The company might be viewed as very ROIC-profitable even now, but I hasten to show you what sort of history the company is coming from, and that this is actually not necessarily a positive here.

{kind=link}

The same is true for other metrics, such as shareholder equity % of total assets - which might be good in total assets for the past 10 years, but is actually negative in how high of a percentage of total assets are now owned by shareholders- because that percentage has been flat or dropping since 2018.

The company also doesn't share much in the ways of numbers beyond geographical or segment-basic numbers. We don't have much in the way of margin numbers for individual segments or nations, which makes the company difficult to compare.

Some analysts consider the company, based on P/S numbers and general profitability numbers, to be worth as much as €64/share (Source: GuruFocus). I take a firm stance against any such assumption and view this to be way too positive in how the company has performed in the last few years.

I talked about it in the last article - but I view these forecasts as way too optimistic. I'm impairing my forecasts for KONE, which still result in a share price no higher than €41.5, but I won't adjust my PT from €42/share.

I still see the company heading into even more of a margin crunch that won't abate anytime soon, and the turnaround in the Chinese property sector seems somewhat doubtful at this time. While I don't see any fundamental worries for the company's cash flows, I do not see a positive thesis that would call for an investment at this price.

This leads me to the following thesis for KONE.

Thesis

- KONE is a great, fundamental business in access and transportation technology. It's a market-leading innovator with a great portfolio and a market-leading penetration across the world. However, investments have left it overexposed to a fragile Chinese property market and geography, which combined with current macro trends in inflation, wages, and pricing, are wreaking havoc with margins in a most unappealing manner.

- The company maintains a relatively unattractive valuation in the context of an unclear recovery and margin reversal. I don't see 1Q23 providing any more clarity as to any fundamental longer-term improvements here.

- I won't touch KONE at above €42/share. I don't view the upside as attractive enough at this time.

- Based on this, my stance is currently "HOLD".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

KONE: Exercise Caution, Reiterate 'Hold'